“If everybody indexed, the only word you could use is chaos, catastrophe…The markets would fail.”

– Jack Bogle, the Vanguard founder and the creator of index investing

“Once you open up that curiosity door, anything is possible.”

– Mr. Clarke from Stranger Things

______________________________________________________________________________________________________

DISCLOSURE: Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. Please see important disclosures following the piece.

Up-front warning: This will be the strangest Evergreen Virtual Advisor (EVA) you’ve ever read. Considering some of the far-out stuff I’ve written over the years—such as speculating the Fed was going to violate its charter and buy corporate bonds—that’s quite a declaration.

Yet, even casual readers of this newsletter know that I am a macro economic research and fundamental security analysis kind of junkie guy. In other words, I study enormous (some would say insane) amounts of big picture data and reports in order to ascertain, to the best of my abilities, where interest rates, earnings, inflation, the unemployment rate, etc, are likely heading.

Similarly, my team and I spend hundreds of man- (and woman-) hours every week reviewing the investment merits, or lack thereof, of specific companies. We also are willing to invest pretty much anywhere in the capital structure, which is a fancy way of saying we’ll consider stocks, preferreds, or bonds as potential investments for our clients. This makes Evergreen Gavekal highly unusual these days when most investment advisory firms eschew company-specific research and, increasingly, simply utilize ETFs.

A key part of our ability to do this with respectable results is due to our partner firm Gavekal. Inarguably, it is one of the most-respected global macro research firms. This is evidenced by their frequent interviews in publications such as Barron’s, The Wall Street Journal, and The Financial Times, to name just a few. Additionally, an impressive list of premier money managers are Gavekal clients.

Several years ago, Evergreen and Gavekal linked up our company-focused investment process. As a result, we have an unusual number of professionals devoted to the time-consuming task of analyzing individual securities.

Admittedly, in a roaring bull market, especially one dominated by trillions of Fed-fabricated funds and also by momentum-chasing computers and day-traders, these competitive advantages may seem of dubious benefit. But that’s actually a good segue into what I’ll call “Stranger Things…”

In the late 1990s, I began to develop a grudging respect for that renegade sect of the investment business known as technical analysis. Certainly, there are more than a few practitioners of this “dark art”, as many traditionalists view it, but they are definitely vastly outnumbered by fundamental analysts and portfolio managers. The latter, in turn, are even more numerically overwhelmed by passive “investors” who supposedly ride the coattails of those, like Evergreen Gavekal, who do actual analysis.

This is really the cornerstone of the Efficient Market Hypothesis; namely, that with a vast number of firms, like ours, doing the analytics, the overall market will rationally incorporate nearly all available information. Thus, securities will be priced so accurately that it’s impossible for most investors to do any better than the market itself. Thus, again, the dominant belief is to simply index which has morphed into the ETF (exchange traded fund) tsunami that now sweeps through the markets on a daily basis.

This is a topic I’ve written on many times in the past so I’m only going to go superficial on it this time. However, there are some obvious big holes in this concept, the most glaring of which are the undeniable existence of market bubbles. Also, undeniably, these are happening with escalating frequency. Another glaring defect in the EMT is that once the thinkers are marginalized by the no-thinkers, the entire concept of an efficient market falls apart at the seams. Even the father of index investing admitted this point, two years prior to his passing in 2019.

I know, I know—what about Stranger Things? (I love that show by the way). Ok, here it is, sports fan (those who are left, that is): My tentative embrace of technical analysis has become a full-on love affair…at least with one simplistic aspect of it. Simplistic? How can that possibly add value? Anything obvious must be easy to replicate, right? The answer is yes and maybe that’s a key part of my thesis.

But first a bit more backstory. It was in the late 1990s that I began to notice a strange phenomenon. Almost invariably, when a stock I owned for clients broke below the lowest price it had traded at over a three-year period, it would continue to fall--usually a lot. Conversely, when a stock would break above a three-year resistance, or ceiling, price it would nearly always keep running.

This was a hard epiphany for me since I’m a congenital contrarian and I think it’s difficult for most fundamental investors, who typically view technical analysis as akin to science fiction. (Like, for example, how a super-secret government research lab in a small Indiana town may have inadvertently opened a portal into an inverted dimension.) Candidly, for years I was embarrassed to explain my belief that using this process was important, much less vitally important. That’s a key reason I believe this phenomenon has gone largely unexploited over the years, at least until lately (more on that in a moment).

For sure, indexers can’t utilize this tactic. If you don’t know this—and you definitely should—indexers merely replicate the composition of the S&P 500 or whatever benchmark they have chosen. (Another ultra-popular example of that today would be ETFs that mimic the NASDAQ 100, which is increasingly the NASDAQ 5 these days, the usual suspects of the FANGM*).

Consequently, even if a very large holding within the ETF breaks multi-year support—or, even worse, several over-sized positions break down—the ETF is stuck holding them. And believe me, as sure as the Seattle Mariners will once again fail to make the playoffs, and politicians will sell their souls to win the next election, this day is coming for today’s exalted market members.

Moreover, as crowded as these mega-cap tech stocks are right now, when they experience their inevitable crucial support break, the financial pain will be enormous. Investors will discover that the virtuous cycle of increasing flows into the countless ETFs--that are loaded to the gunnels with extraordinarily pricey tech stocks—will flip into a vicious circle (more like circling the drain), of selling begetting selling, when the flows eventually, and inevitably, reverse. And because they are so incredibly extended right now, the eventual losses from their bubble peaks will be huge well before long-term support comes into play.

Let me make this a bit more tangible and, certainly for me, more painful. For a variety of reasons, I’ve personally maintained a short portfolio over most of the last fifteen years or so. At this point, let me be clear we don’t do this for Evergreen clients (though in the past we’ve utilized some inverse ETFs, that benefit when the subject prices fall, with mixed results). Outright shorting, vs using inverse ETFs, is extremely risky because there is no limit to how much you can lose. If you buy a stock at $10, the most you can lose is that amount even though that represents 100% of your investment in this security. However, if you short it at $10 and it goes to $100, you’ve lost 10 times your initial commitment.

Let’s take it to an even more specific example by saying you were suspicious of the accounting at Tesla (ticker, TSLA), and the behavior of its highly promotional CEO. You may have believed, as did several high-profile, but increasingly endangered (by Fed binge-printing), short-sellers, that it could become another Enron or Worldcom (or, using a current fraud event, Germany’s Wirecard). Accordingly, you might have been moved to short TSLA around $300 per share back in the long-bygone days of March, 2019. With the shares now trading at $2,278, you’re nursing a loss of about 650%! Take it from me, that’s not a joyous experience. (As you may have seen, TSLA will soon be splitting 5 for 1, creating absolutely no real economic value; yet, this announcement has generated around $168 billion of increased market cap, at least temporarily. Apple, another red-hot tech stock, has similarly surged by an astounding $324 billion since they announced their split on July 31st, which is equivalent to 60% of its market value in the summer of 2016.)

(In defense of my short-selling history, I did come into the Global Financial Crisis of 2008/2009, the near-bear of late 2018, and this year’s March meltdown, with sizable short positions in place. The large sums released when my shorts crashed in price allowed me to cover most of them at low levels and rotate the funds received into bombed-out issues which I did in all three incidents.)

However, if you were paying attention to the multi-year price chart, you would have realized a break-out above $400 was a really big deal and you would have/should have covered your short. On the other hand, if you rationalized this as a fluke development and convinced yourself to sit tight because that was not much below the fraudulently misleadingly hyped takeover price of $420, you would now be able to buy a fleet of Tesla cars for what you’ve lost (again, take my word for it!).

Source: Bloomberg, Evergreen Gavekal

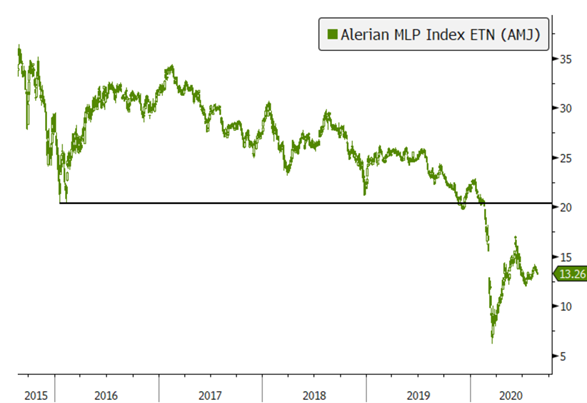

Next, let’s review another costly but, eventually happier, situation. This newsletter has often recommended the energy infrastructure vehicles popularly known as MLPs (actually, these days they are unpopularly known as MLPs). While there were times we’ve advised taking profits, or at least reducing exposure, for the most part we’ve been bullish on them, unfortunately, since they were poleaxed in 2015. (To our credit, we were vocally bearish on this energy sub-sector when they were ragingly popular in 2013.)

MLPs started this year in fine fashion continuing a rally that began in the fall of 2019. By January 14th, 2020, they were up roughly 15% from their early December trough, which was essentially $20, a critical level as we shall see. And then came COVID. Since the virus crisis initially hit China, a massive energy consumer, MLPs were among the first to get slammed. On February 25th, even as the S&P 500 was only about 6% below an all-time high, the MLP index clearly broke below the critical $20 long-term support level, as you can see below.

Source: Bloomberg, Evergreen Gavekal

This development forced the Evergreen investment team to reduce our exposure to MLPs, despite extremely attractive yields. It was a very difficult move and one that we took some heat over at the time. Yet, as you can see, the red-headed step-child also known as mid-stream energy (mostly pipelines) was destined to crash below $7 during the worst of the March Madness, a decline of 70% from the crucial support level.

In hindsight, we should have lightened even more but our sell-downs did give us vital “headroom” to buy more as MLPs were slaughtered (along with almost everything that was energy-related or economically sensitive). By “headroom”, I’m referring to our self-imposed discipline of how much exposure we allow our clients to have to MLPs, or any other asset class, using cost, not current market value. The latter is a key distinction because when a sector is crushed you can convince yourself you don’t have that much exposure and become far too invested based on actual cost.

However, the nice thing about sectors, even sub-sectors, as opposed to stocks, is that they don’t go to zero, at least not overnight (presumably, a century ago, the buggy-whip sub-sector gave its true believers several years to see the writing on the wall!). Thus, once a sector has been annihilated you can begin to gradually re-accumulate it and the same is true with stocks though, for the just mentioned reason, special care needs to be exercised with individual names. In fact, our studies of breaking key support levels is that once the devastation plays out, the returns going forward are far better than even upside break-out situations (there are many exceptions but this is referring to on-average).

For example, the MLP index, which almost no one would touch in March, proceeded to rise 140% by early June, a mere month and a half later. Unsurprisingly, after such a monster move, it then corrected by almost 30% before beginning to rally again.

Fortunately, because we lightened up in February, Evergreen was able to go aggressively on the buy-side. Again, in hindsight, we should have splurged on MLPs even more; however, in our defense, we were busy buying enormous amounts of other totally pummeled securities in a wide variety of sectors and asset classes.

MLPs are an excellent illustration of what I believe is the best attribute of following long-term support and resistance levels. In my view, the number one killer of investment returns is getting blasted out of the water by something that crashes (or, for a short-seller, that goes ballistic) and where no protective action is taken. If one steadfastly follows this process, you will systematically exit styles, sectors, or securities that are cracking (or, if selling short, minimizing the losses from stocks going vertical). It also avoids the cardinal sin of what I call the Premature Accumulation Syndrome. As all EVA readers likely know, I am a big fan of dollar-cost averaging UNLESS a critical support break is triggered.

Now, does this work all the time? Of course not, but it does work most of the time. In fact, in my experience, head-fakes are rare. We’ve also gone back internally to statistically verify our real-time, real-world experience. Additionally, we commissioned a study with Ned Davis Research to verify our verification. Verily I say to you, it came back very conformational. (Personally, I always put more stock in actual results than back-tested studies but it’s nice when they synch up.)

One major flaw is with takeovers. Decent companies (and even some of the indecent variety) will occasionally attract takeout bids from competitors or private equity once they’ve been pounded. We’ve had that happen on at least one occasion. Further, sometimes a smashed stock will report stunningly positive earnings and that will overwhelm the technical sell signal. Yet, that’s extremely rare with companies that are under enough selling pressure to take out a support level that has persisted for years.

The other thing we’ve learned is to mostly ignore three-year support breaks late in bear markets. At that point, almost everything is cracking, though one could rationally make the case that those securities which aren’t breaking down (like mega-cap tech in March) are showing unusual comparative strength and may lead on the way out of the bear phase. This certainly has happened with tech in recent months. In our view, that’s why it’s nice to have a mixture of stocks that have been nuked along with those showing considerable positive momentum. Please check out the chart below of the NASDAQ that both illustrates the relative strength in March (the “NAZ” only fell 28% vs 38% for the S&P) and the break-out, with upside follow-through, that happened in late June.

Source: Bloomberg, Evergreen Gavekal

Is there anything magical about the three-year timeframe? Not that I know of, but it works, again, most of the time (we’re also more dismissive of three-year upside break-outs late in bull markets). In my opinion, borne of years of watching these situations play out, the longer the trading range the better. In other words, if a stock has been trading between $20 and $50 for ten years and then suddenly and decisively moves above or below that range, you best pay very close attention. Conversely, a range that has been in place for only a few weeks, doesn’t mean much--if anything.

Another crucial question to ask is: When is enough, enough? In other words, how do you know when something that broke down or broke out and then has moved significantly in that same direction is either a buy or a sell? The simple and most accurate answer is, you don’t. However, there are some important clues that can help you get closer to a positive outcome.

First, in the case of a sector or stock that was been vaporized, like MLPs in March, a key question is: Has it quit falling on bad news? In the case of MLPs, even as oil went to minus $40 per barrel in April*, MLPs barely flinched. They clearly didn’t make a new low despite the fact that they have been highly sensitive to the price of oil, right or wrongly (and I think mostly wrongly), since 2015. The same is true on the upside when a security doesn’t react well to positive news.

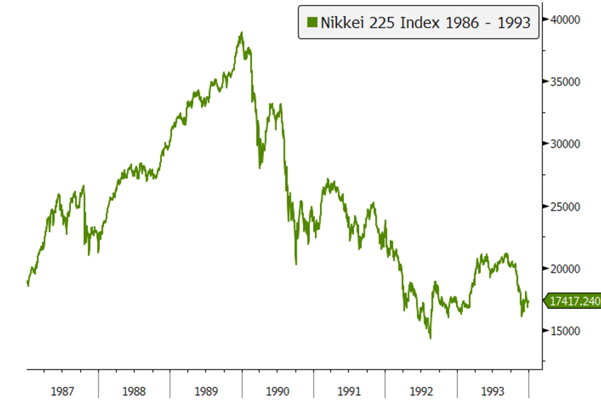

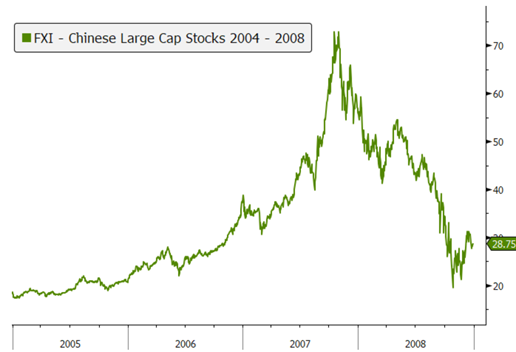

The other important consideration is the price chart itself. Once you see a vertical line up or down, you are probably dealing with either a bubble or an anti-bubble (the latter being a total inverse of the kind of absurd pricing we are seeing today with so many high-growth “story” stocks, like anything related to “The Cloud,” a subject we wrote about in May). The chart on MLPs above gives a classic illustration of an anti-bubble event while the charts of the Japanese stock market in 1990, the Nasdaq in 2000, the Chinese stock market in 2007, and the US semiconductor ETF of late are classic bubble patterns. Let me throw in one individual chart, Shopify, with the caveat that specific stocks can go even more exospheric than overall markets or sectors, even when they trade at essentially an infinite P/E as SHOP does presently.

*This was a technical aberration due to a lack of storage capacity, squeezing the longs—or futures contract owners—who wouldn’t, or couldn’t, take delivery. The June contract never went much below $10.

Source: Bloomberg, Evergreen Gavekal

Please observe that in each of the earlier bubbles, once the break happened it was a long, agonizing trip down the other side of the mountain. History is LCD clear that ALL bubbles turn out this way. It’s kind of like humans and mortality—the “success” rate is 100%.

Let me add that with anything caught up in a bona fide bubble, the three-year support rule isn’t going to do you much good, once the inevitable bursting happens. As alluded to earlier, you’ll be down so much by then the only thing you’ll be able to do to make yourself feel better is to send hate-mail to Jim Cramer (who is back in a bubble-blowing mode worthy of a Dale Chihuly apprentice). This is where paying attention to the good news/bad reaction might be a nest-egg saver. But even that might not work in time. My best advice to anyone reckless lucky enough to be sitting on massive gains in names like SHOP is to methodically sell them down. If they go up another 25%, sell one-quarter of what you have left and just keep doing that…no matter how much Jim Cramer loves the story.

One semi-final observation is that this process seems to be—and I could be wrong about this—working better than ever. With so much money pushed around by no-thinkers, why would that be? My best guess is that it could be due to the staggering sums now managed by shadowy algorithmic trading strategies. These use artificial intelligence and from what I know about them (which isn’t much) pattern recognition is a prime strength of the “algos”. Thus, the computers may be magnifying and accelerating the moves that securities are making after breakouts and break-downs. Even staid UPS, has been another case in point recently.

Source: Bloomberg, Evergreen Gavekal

One final chart to ponder relative to the main theme of this EVA is the recent break-out by gold to an all-time high. The many skeptics on the yellow metal may be wise to consider the emphatic message this image is conveying. Perhaps it’s time for all the anti-gold bugs out there to shift from being naysayers to yea-sayers.

Source: Bloomberg, Evergreen Gavekal

My truly final comment to those who ask why this might work is my feeble stab at a fundamental rationale. It’s long been my suspicion that to push a security out of a long established trading range means that something extremely material is unfolding – a development, or series of developments, of which the market may be only dimly aware, at least until more news comes out. At least that’s my story and I’m sticking to it…until the facts change and, then, so will my mind.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.