“Consider the subtleness of the sea; how its most dreaded creatures glide under water, unapparent for the most part, and treacherously hidden beneath the loveliest tints of azure.”

– H. Melville, Moby Dick or the Whale, 1851

“Vincent Deluard…is well worth following.”

– Louis Gave in his recent “Nine Guiding Principles” essay

_____________________________________________________________________________________________________________________

Even hard-core EVA fans are probably tired of reading about how much I read. But believe me, you’re not as tired of reading it as I am of doing it! Occasionally, though, I come across something so unique and interesting that it makes it worth ploughing through the 1,000 or so pages I read per week that are for the most part kind of, well, meh. (Naturally, this excludes Louis Gave and the rest of the stiletto-sharp minds at Gavekal!)

The main reason for my typical shoulder-shrugs is not that my reading material is lacking in quality; rather, it’s that I’ve seen much of it before, often multiple times. But thanks once again to my friend Vincent Deluard, Director of Global Macro Strategy at INTL FC Stone, my shoulders snapped to attention when I read his September, Flow Report, titled “SWIMMING WITH THE TARGET-DATE WHALE; SHORT FOR HALLOWEEN, LONG FOR CHRISTMAS?”

It’s my belief that his discovery about the impact of target-date funds on the broad market will be new and eye-opening information for you, as it was for me…which is why I chose it for this edition of our monthly Guest EVA. It certainly caught the attention of the aforementioned Louis Gave, who is even harder to impress and intrigue than am I. But, just as in my case, Vincent’s note did exactly that, reinforcing my belief that this is special material to share with all of you. (A thousand thanks to Vincent—merci mille fois, in his native language—and to his firm for their permission to do so.)

If you have limited knowledge about the modus operandi of those mysterious target-date funds—and particularly if you are heavily invested in them in your retirement plan—you should definitely keep reading. My suspicion is that you are, like many, unaware of how concentrated and mechanical these vehicles have become. It’s not my intent to “scoop” Vincent’s main message; thus, I’m going to keep this introduction quite brief…always a crowd-pleaser.

However, I will say that paying attention to the phenomenon Vincent describes might prove highly lucrative to those investors who are willing to be less buy-and-hold and more tactical. If so, Vincent might be giving you one whale of a Christmas present!

Moby Dick is rich with profound spiritual, religious, and psychological themes – and very practical advice: when men fight a giant sperm whale on a tiny boat, the whale usually wins. Giant whales also hide below the calm surface of markets and experienced traders know better than to fight them: when a whale is hungry, it will feed, whether we like it or not.

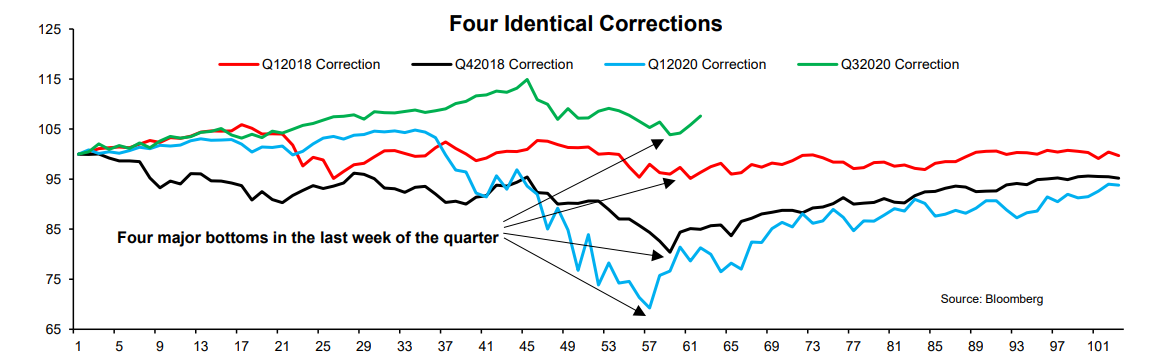

This report will start with a statistical oddity: the four most recent corrections ended in the last week of the quarter, and three of them ended on the same day - the 23rd.

The second part will discover “the whale”: the target-date fund industry, which collects 5 to 10% of most Americans’ paychecks and invests them formulaically into a handful of low-cost index funds with assets of $2.3 trillion. Target-date funds, or any strategy with a pre-set asset allocation, must rebalance against the market, i.e., sell the assets which go up in price and buy the ones which go down.

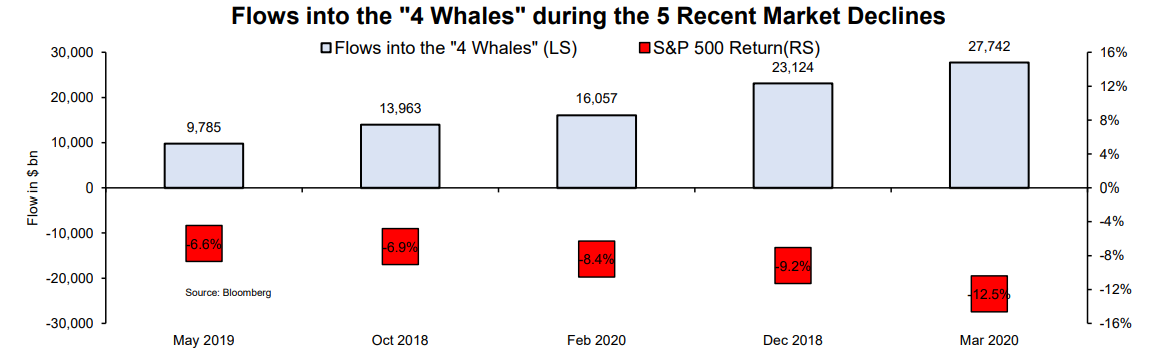

For example, Vanguard’s four equity whales took in an insane $43 billion during the Covid-19 bear market of Q1 2020 and $23 billion during the Christmas massacre of 2018. No wonder that stocks posted neat “V-shaped” bottoms and never re-tested their lows!

Stocks’ torrid rally this summer forced target-date funds to rebalance out of equity funds in September, which drove the 10% correction from September 2 to September 23 (that magic number again!).

If these dynamics play out again in the fourth quarter, I expect stocks to drop rapidly in October and November due to poor liquidity, electoral risks, and record valuations, before the target-date whale shows up to save everyone for Christmas.

It Is a Statistical Miracle!

March 23, 2018. December 24, 2018. March 23, 2020. September 23, 2020. The past four bear markets or corrections all ended with a V-shaped bottom in the last week of the quarter. Three of these bottoms took place on the exact same day of the month* – the 23rd.

Statisticians can calculate the exact probability of such a remarkable coincidence, but experienced investors already know that this cannot be a fluke and should instead focus on understanding why a seemingly occult hand keeps rescuing markets at almost the same date every quarter.

*December 23 was a Sunday, so the market bottomed on the following day, on Christmas Eve. Also, the S&P 500 index had a second bottom on April 2, 2018, following the March 23, 2018 bottom.

As usual, the #fintwit community has been quick to offer an explanation, which follows the first rule of market punditry: “when in doubt, blame the Fed”. I enjoy Fed-bashing as much as the next guy, but I trust that S. Mnuchin would be smart enough not to instruct the New York Fed to buy S&P 500 index futures in secret on the same day of every quarter.

How about target date funds (investment funds that invest in a mix of assets that shift from higher-risk to lower-risk investments over a pre-established glidepath)? The industry manages $2.3 trillion in retirement assets across mutual funds, collective investment trusts, and separate accounts, and received close to 80% of all 401-K contributions this year.

Surely, receiving 5 to 10% of most Americans’ paychecks every month and investing according to a pre-set asset allocation, must result in “whale-like” trading flow, which can rock markets. How target-date funds trade is the object of the next section.

Understanding Target Date Funds Demand

The target-date fund industry is remarkably concentrated: three companies, Vanguard, Fidelity and T. Rowe Price, account for more than two thirds of the market. This study will concentrate on Vanguard for two reasons.

First, Vanguard is by far the largest player with $862 billion (38% of the industry) in target-date assets at the end of the 2019, a trend which will likely accelerate as a result of the Department Of Labor’s guidance on “qualified default investment alternatives” which cements the domination of low-fee index funds.

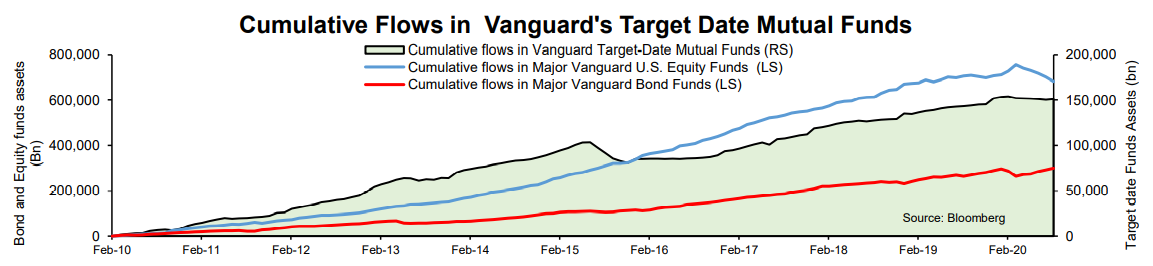

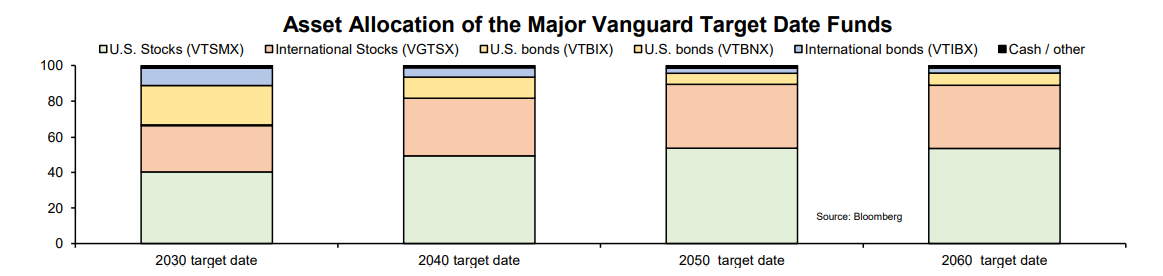

Second, Vanguard’s public offering is remarkably simple: 12 mutual funds offer retirement solutions based on the expected retirement date, from 2020 to 2065. These funds, which have collected $167 billion since 2009, are solely invested in Vanguard’s six behemoths (VTSMX, VFINX, VGTSX, VINIX, VBITX, and VTBIX), which manage $2.3 trillion (with a “T”). These six whales have received about $1 trillion (again, with “T”) in the past decade, making them the single greatest buyers of stocks by far.

The retirement contributions into target funds are distributed across Vanguard’s index funds according to a formulaic allocation key: the older the expected retirement date, the higher the allocation to stocks. For example, the 2050 target date fund (VFIFX) has a 90% allocation to stocks**

**For what it is worth, these weights seem aggressive for workers in their mid-30s based on the old heuristic that the allocation to stocks should be 100 minus your age and the fact that the S&P 500 index trades for a record 26 times forward earnings. But in Vanguard’s actuarial and capital markets assumptions we trust – and if we don’t, the DOL's rules do not give us much of a choice anyway.

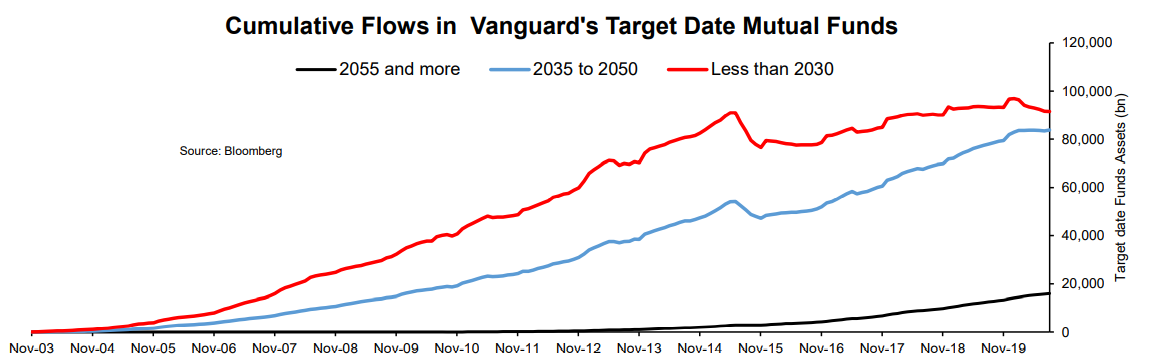

Although this report focuses on overall target-date fund flows, investors should be aware that flows are not equally distributed among age groups. In general, long maturity target-date funds have been gathering the most assets as Millennials and Gen Z-ers rely exclusively on 401(k) accounts for their retirement. Conversely, funds with a target date of less than 2030 have lost assets as older workers started to retire. All else equal, these trends result in greater flows into stock funds.

Target-date funds, or any strategy with a pre-set asset allocation, must rebalance against the market, i.e., sell the assets which go up in price and buy the ones which go down. The chart below shows the trailing two-year correlation between Vanguard’s four equity whales and the monthly returns of the S&P 500 index. The correlation has dropped to a record negative 74% in August, which suggests that:

The counter-cyclical demand from Vanguard’s equity index funds is especially remarkable during extreme market events. These four funds took in an insane $43 billion in February and March 2020 when everyone else was liquidating stocks. Flows around the Christmas massacre of December 2018 soared to $23 billion. No wonder that stocks posted neat “V-shaped” bottoms and never re-tested their lows.

A Flow Perspective on the September Correction

This pattern can help us understand the sharp correction of early September, and the now-customary “last week of the quarter” rally. Vanguard’s rebalancing policy states that “most of the time, the target retirement products are rebalanced within fairly tight guardrails by using the regular cash flows they receive, primarily from payroll deferrals. Occasionally, when payroll deferrals are not enough to accomplish this, the portfolio managers buy and sell two or more of the underlying funds to bring the target retirement products back into balance”.

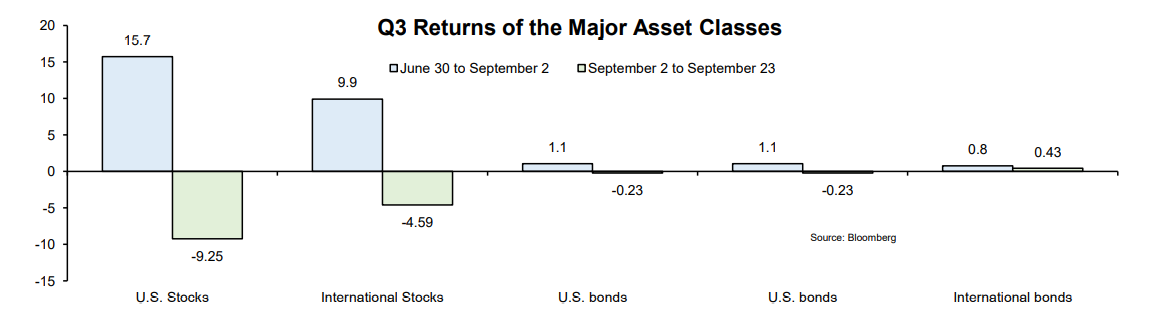

At the September 2 market peak, U.S. equities had gained 15.7% for the quarter, while bonds were essentially flat. The gap was too large to be filled with regular 401(k) contributions: target-date funds had to actively sell stock funds and buy bond funds to get back to their target weights by the end of the quarter.

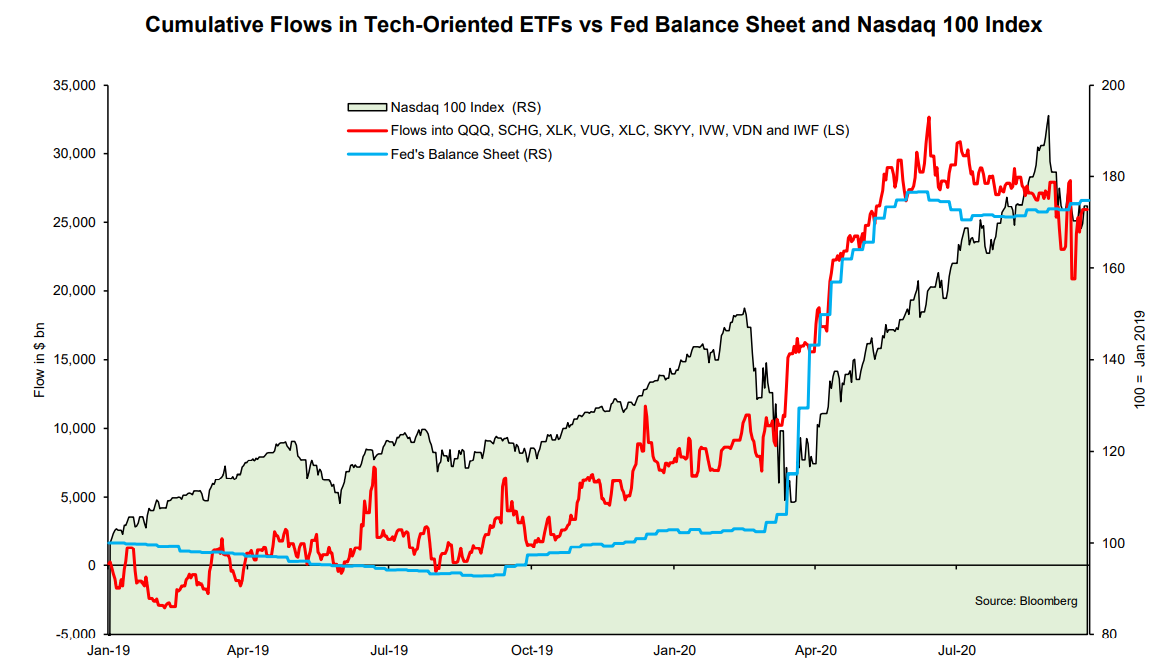

In addition, this rebalancing dynamic was compounded by unusual outflows from tech-oriented ETFs: the nine major tech/growth-oriented ETFs lost $12 billion between June 18 and September 18. Interestingly, and perhaps not coincidentally, these outflows coincided to a small reduction of the Fed’s balance sheet, just as the heavy inflows into tech ETFs from April to June coincided with the explosion in the Fed’s assets.

The combination of target-date funds selling stocks, ETF investors bailing out of large growth funds, and a small reduction in the Fed’s balance sheet led to the rapid market losses in the first two weeks of September.

But the 10% correction between September 2 and September 23 was so rapid that it effectively rebalanced target-date funds’ allocations to their intended weights. Funds which had actively sold equities in the first weeks of September likely became underweight stocks, leading to the now-customary “last-week-of-the-quarter” scramble to get back into stocks. The big rebounds on Friday and Monday lifted almost all stocks, which is an indication that they were driven by heavy inflows into index funds.

How will these dynamics play out in the fourth quarter? To which we shall now turn.

Halloween Scare, and then Christmas Rally?

As I explained in “From a Summer Storm to a Secular Bear Market”, a perfect supply and demand storm should hit markets in October and November.

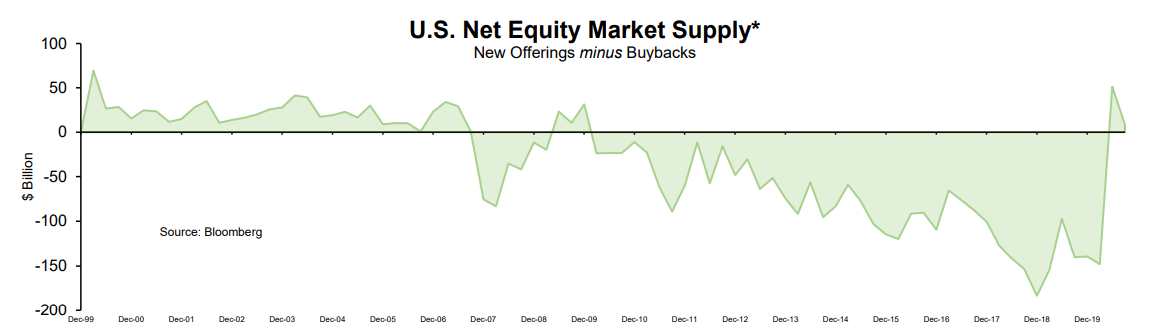

First, the net supply of stocks has turned positive for the first time since the Great Financial Crisis as new equity offerings exceed buybacks. In other words, equity markets will need net new investor flow just to remain at their current levels.

Second, active investors will likely remain nervous ahead of the Presidential election, which I do not expect to be decided on the night of November 3. As both sides have already promised a protracted legal battle should they lose, violence could easily spill into the streets, especially as the replacement of Ruth Bader Ginsburg has further escalated tensions.

It is not clear that the Federal Reserve would come to the rescue as quickly as in prior corrections. Bank of America pointed that the Fed’s purchases of bond ETFs have slowed to a trickle in September. In addition, the Fed may not want to be seen as helping or hurting any candidate before the election.

Furthermore, recent communications by the Federal Reserve have stressed the importance of fiscal policy and the notion that monetary policy has already done its part. J. Powell’s subliminal message to Congress is that politicians should not expect the Federal Reserve to bail out the market if they cannot agree on another fiscal package before the election (which is now a near-certainty).

This Mexican standoff between monetary and fiscal authorities happened repeatedly in Europe during the sovereign debt crisis and led to sharp corrections in asset prices.

Unprecedented Treasury issuance is another risk factor in the fall of 2020. An unprecedented $5 trillion of federal and local debt must be rolled over in the next three months. Without a budget deal, the Treasury will have no choice but to draw from its massive cash hoard at the Federal Reserve, which is currently lent out in the repo market. Liquidity will likely tighten as a result, which would be another headwind for stocks.

These factors could easily lead to another double-digit correction in stock prices in the next two months, which should, in time, lead to counter-cyclical rebalancing flows from target-date funds. However, target-date fund rebalancing will not save the market right away. As of Monday, U.S. equities were up 7% for the quarter versus a gain of just 65 basis points for the Barclays U.S. Aggregate Bond Index. In other words, the target date funds which have not actively rebalanced their portfolios will start the new quarter with an excessive allocation to stocks: they would likely be sellers in October.

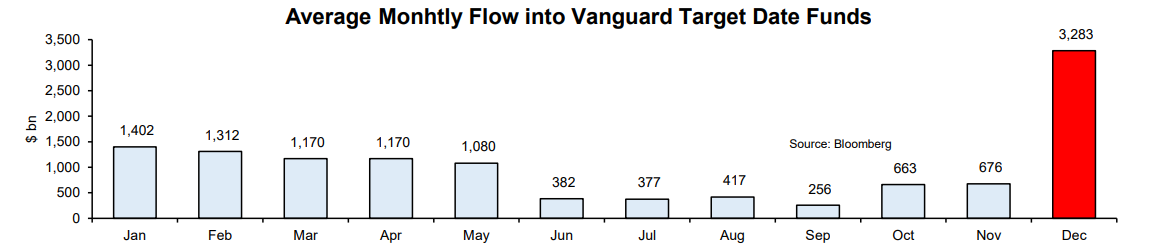

This math would change if stocks were to drop by more than 10%: target date funds would need to sell bonds and buy stocks. Based on historical precedents, this should happen in December, which is usually the best month for target-date fund flows, as year-end commissions and bonuses result in abnormally large contributions to 401(k) accounts. Investors who prefer to swim with the whale rather than against it should be short in October and November, neutral in the first weeks December, and long for the customary Christmas rally.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.