Dear Readers,

From everyone at Evergreen Gavekal, we want to wish you and your loved ones a very happy and healthy New Year. While 2020 was not easy, amid a once-in-a-century pandemic, neighbors checked on neighbors, many families got closer together, and health care workers got the applause they deserve. As we turn the page to 2021, we want to share a heartfelt thank you for your readership. If there's anything we can do to help you navigate the new year, please don't hesitate to reach out.

Happy New Year!

- The Evergreen Gavekal Team

______________________________________________________________________________________________________

“If This Isn’t A Bubble, There Ain’t No Such Thing.”

– Michael Lewitt, author of The Credit Strategist

“My belief is that people are once again ignoring what is staring them in the face – a gargantuan financial bubble that is going to explode in their faces.”

– Michael Lewitt, author of The Credit Strategist

“Investors have become uninterested in worrying about downside risk.”

– Tobias Levkovich, Citigroup’s chief US equity strategist.

______________________________________________________________________________________________________

Admittedly, that isn’t the snazziest EVA title I’ve ever created. But I wanted to accomplish two things with it: First, save time for those who want essentially a Twitter message in terms of brevity and, second, to underscore the basic message.

Now, for all those who are wondering “But Why?” I will proceed to make my case for raising cash, asap, if not sooner. But before I do, remember the similarly blunt message conveyed in these pages back during the March market meltdown in “Bring Out the Bazookas!” to buy stocks aggressively.

Before we get into the market’s current extreme valuation level—which, candidly, many pundits dismiss as irrelevant these days—let’s focus on an area that is extremely dangerous for perma-bulls to blow off: insider trading activity. No, I’m not talking about the kind that our precious political leaders blithely engage in, capitalizing on privileged and, therefore, what should be unactionable information, but the truly legal kind. These are the publicly reported buys and sells made by corporate senior management types within the SEC-permitted windows after critical news has been released.

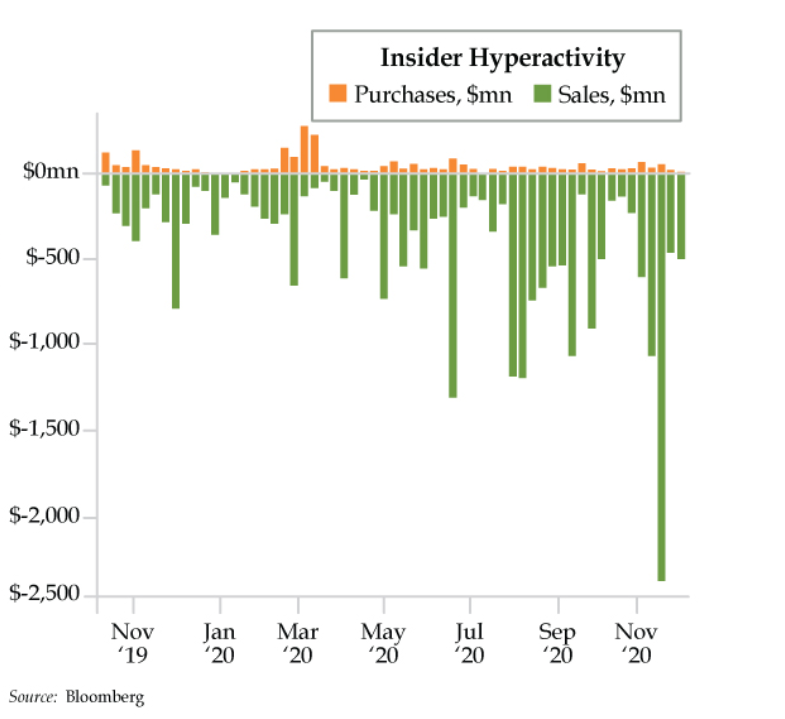

The normal tendency is for insider selling to be greater than buying for a variety of reasons, including that corporate insiders usually have considerable exposure to their own company’s stock (often through the management enrichment device known as stock options). When the ratio is around 10 to 1 (10 sales to one buy), this is considered bullish. On the other hand, when it rises to 20 to 1 that’s viewed as a warning flag. According to Canada’s most famous economist, David Rosenberg, this ratio recently hit 58! For those who would like a visual representation of how skewed insider activity is to the “get me out” side, please see this image from my friend Danielle DiMartino Booth.

If you look closely, you can also see that during the March Madness (stock market, not NCAA, variety) purchases by those in the know substantially outweighed sells (though some of that appeared to have carried over into April). One of my favorite Warren Buffett sayings, that has often been repeated in these pages, is to be fearful when others are greedy and greedy when others are fearful. Obviously, though, when it comes to insiders, you want to be greedy when they are greedy and fearful when they are fearful. That kind of makes sense, don’t you think—unlike so many current market happenings. But much more on that last part in a bit. (But, again, for a quick takeaway, re-read the first quote.)

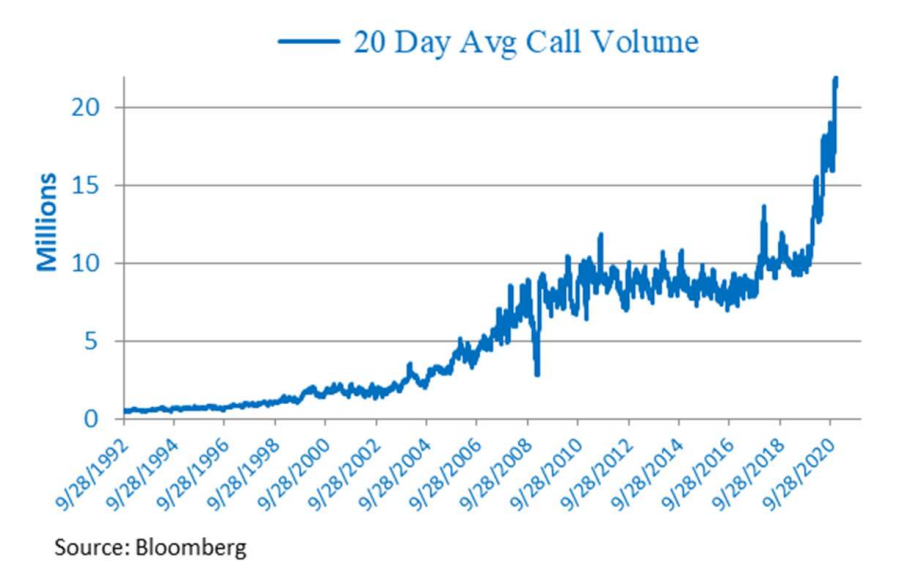

There isn’t a direct method of measuring what “outsiders” are doing with their money; however, there are a plethora of indirect markers that can give rational contrarians some powerful clues. In that regard, let’s sneak a peak at what’s happening in that ultimate market playground of the reckless and ill-informed—the options market.

Courtesy of another friend of mine, Mike O’Rourke, Chief Market Strategist at JonesTrading, recent call (i.e., bullish) option activity has recently gone postal to a degree unlike anything seen in nearly 30 years. Note, that this encapsulates the 1995 to early 2000 timeframe, the biggest stock market bubble in US history. Further, overall option volume is the highest ever.

Along similar lines, per the Sentiment Trader service, December saw twice as many calls as puts (bearish bets) purchased. A ratio this skewed hasn’t been seen since 2000.

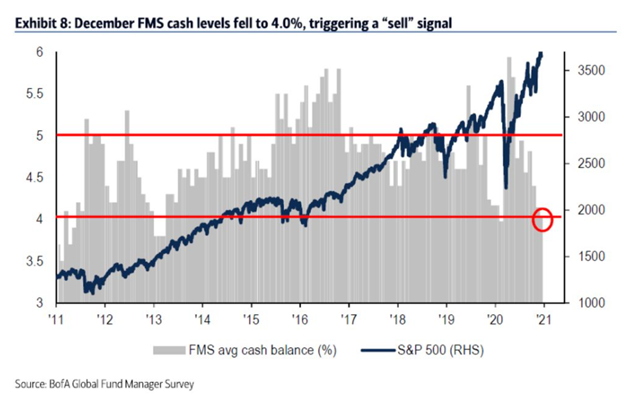

Shifting to sentiment readings, and/or how traders and speculators are positioned, tells a carbon copy (remember those?) story. Jim Cramer, perhaps the most emotional market “expert” known to woman and man, has been screaming on CNBC lately that he’s bullish because there are still so many bears. His main basis for that assertion is that there is $4 trillion in cash on the sidelines (we’ll take a closer look at the reality of that stat shortly).

From purely an attitudinal standpoint, Jim “Cramerica”, as he likes to call himself, couldn’t be further from the truth. The Investors Intelligence poll hit almost 65% bulls to a miniscule 17% bears—and that was in early December. Given market action since then, the numbers have likely shifted even more to the ultra-bullish side…and 65% vs 17% was already an exceedingly euphoric reading.

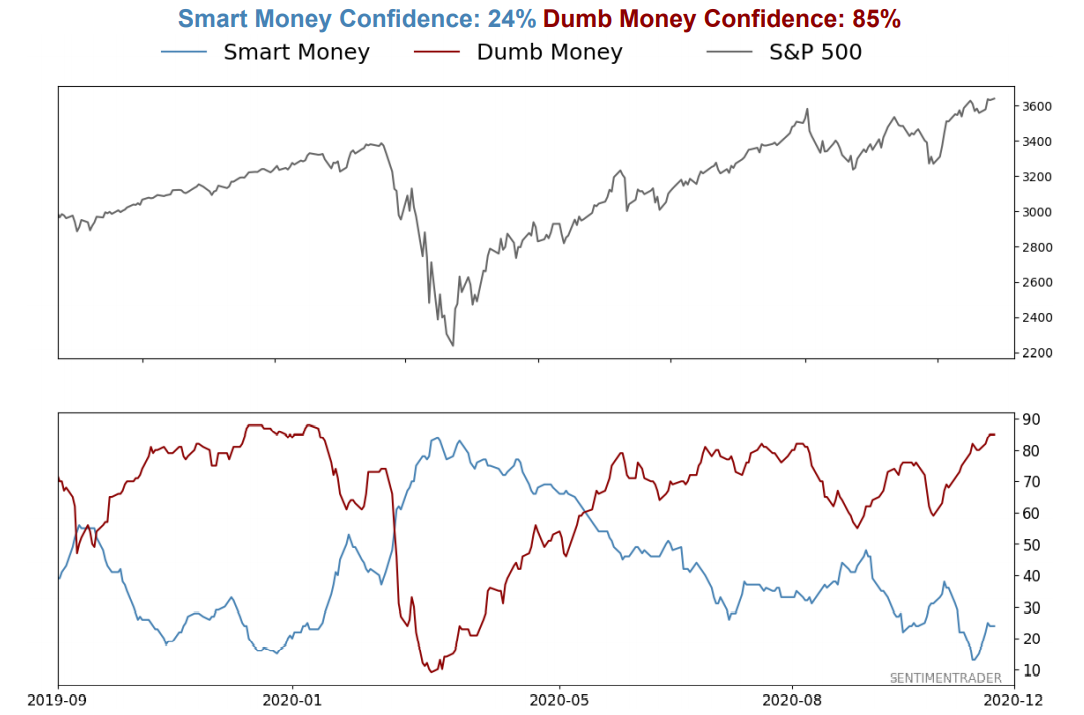

The CNN Fear-Greed Index is at a dizzying 89 (historically, it is only at this extreme reading 10% of the time and the market generates negative future returns, on average, when it is). Meanwhile, median short interest has crashed to a 17-year low. Similarly, “smart money” confidence is very subdued while “dumb money confidence” is extremely elevated (note that, like insider buying/selling, it was the opposite during last spring’s market seizure).

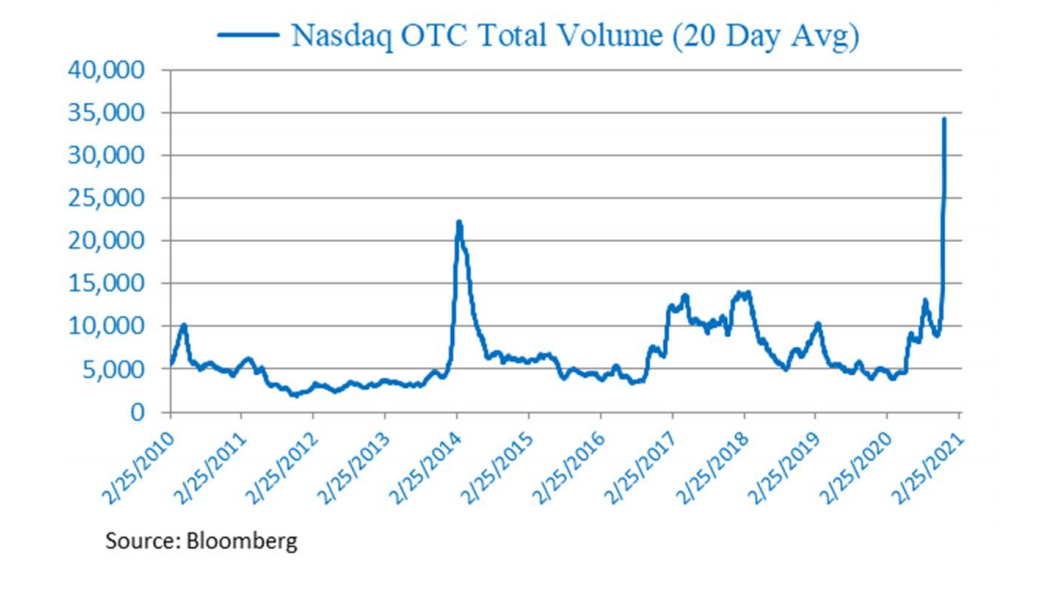

Finishing off the sentiment/positioning section, NASDAQ OTC (over-the-counter) volume has recently done a moonshot worthy of Bitcoin. The below graphic is again courtesy of the highly perceptive—and bubble wary—Mike O’Rourke.

But perhaps the most telling reflection of the prevailing level of mass insanity speculation is market conditions for IPOs and SPACs. (Quick definitions: IPOs are Initial Public Offerings, or new issues, while SPACs are Special Purpose Acquisition Companies.) A quick image from a recent Barron’s cover story gives a hint as to the super-heated nature of IPOs as the heart-breaking – but, incredibly, wealth-inflating – year of 2020 winds down.

Per the above graphic, note the “Shades of 1999” sub-title and the following comment that “today’s new companies are stronger” than in 1999 during the dotcom mania. That sounds comforting but I don’t think it’s totally, or even mostly, accurate. Consider the IPO right before Christmas of QuantumScape, an aspiring electric vehicle (EV) battery maker. Despite an absence of revenues, the market quickly accorded it a $50 billion valuation. This doesn’t strike me as an example of a strong new company even though it is obviously hoping to be a player in one of the market’s hottest sector—green energy.

Notwithstanding its revenue-free condition, QuantumScape’s instantaneous market valuation was more than double that of the venerable Japanese electronics company, Panasonic, which is the main battery supplier to Tesla. Panasonic also has a number of profitable divisions, unlike its EV battery unit that has consistently lost money over the years. Caveat disruptor, QuantumScape—EVs are a tough business where profits have been elusive for long-established companies. Even $680 billion market cap Tesla has never generated operating earnings; its reported profits have strictly come from selling tax credits to competitors.

Another recent IPO shooting-star has been Snowflake. It has been accorded a market value of nearly $100 billion which amounts to 200 times—drum roll, please—sales, not earnings. Typically, stocks trading at more than 10 times sales are considered to be at bubble levels. Snowflake’s Himalayan-like pricing didn’t prevent Mr. Cramerica from boldly recommending it to a young caller as an ideal investment for someone with a long-range investment time horizon (presumably, approaching infinity). By the way, Snowflake’s CEO has been earning a cool $100 million per month due to his stock-based incentive package. This is roughly double its current monthly revenue run-rate. Of course, that rather generous sum needs to be paid by shareholders, one way or the other. But don’t let reality get in the way of a rousing bull market story.

Then there is the recent IPO of Airbnb. Despite being hammered by the virus crisis, just like most travel-related enterprises, Airbnb’s stock is walking on air…lots and lots of air. Its market value topped $100 billion shortly after it went public last month, far exceeding the market value of Fed Ex, which has prospered through this past year’s unparalleled economic dislocations. Moreover, Airbnb was a money-loser even before Covid hit and its business practices are becoming increasingly controversial. (See “No profits? No problem for red hot tech IPOs.”)

Bulls might take comfort in the fact that 2020’s IPO mania hasn’t become quite as maniacal as was the case in 1999. However, as the chart below indicates, courtesy of David Rosenberg, it’s become a horse race that might soon have a nose-to-nose finish.

In case you think the IPO market is about to run out of supply, there are some 500 other “unicorns” (private companies with assumed market valuations of $1 billion or more) that are prime candidates to go public. It’s hard to believe all of those, plus the hundreds that have already done IPOs, are going to be successful, much less industry leaders. If the late 1990s new-issue orgy is any guide, a multitude of these are doomed to mediocrity…if not bankruptcy.

Of course, Wall Street loves the IPO avalanche because of the immense underwriting fees they generate. But not everyone is drinking the Kool-aide. Jim Tierney, Alliance Bernstein’s chief investment officer of Concentrated US Growth (i.e., he’s a growth-stock pro) recently told The Financial Times that, referring to the IPO uber-euphoria, “We’ve all been around markets for enough time to know this doesn’t end well.” Perhaps all of Jim’s colleagues have been around long enough to realize that but clearly millions of Robin Hood type, do-it-yourself investors, and countless other inexperienced speculators, have not.

As far as SPACs go, these are basically “blank check” entities that have raised money from investors on the premise that they’ll find rewarding opportunities in…well…something. As Forbes recently summed up this latest craze: “What’s driving the SPAC mania on Wall Street? Not the billionaires and bankers making headlines daily, but a mob of little-known hedge fund investors, the ‘SPAC Mafia’, who are incentivized to gobble up these opaque public offerings with little concern over whether they ultimately succeed or fail.” Excuse me for wondering whether, based on this indifference to winning vs losing, there won’t be a lot more of the latter than the former.

More than 200 SPACs have gone public in 2020, raising $75 billion, greater than in the prior decade combined. For sure, $75 billion for 200 entities seems like a rounding error compared to merely one Snowflake or Airbnb. Yet, nonetheless, it’s another shrieking siren that animal spirits are out of control as the real world staggers out of 2020 and into 2021. Again, the contrast between outlandishly bullish financial markets and the conditions of America’s battered economy couldn’t be more glaring.

To that last point, let me join the chorus of commentators who believe this disparity is light-years removed from healthy. It is creating a concentration of wealth—and divergence of outcomes—that is alarming, if not terrifying.

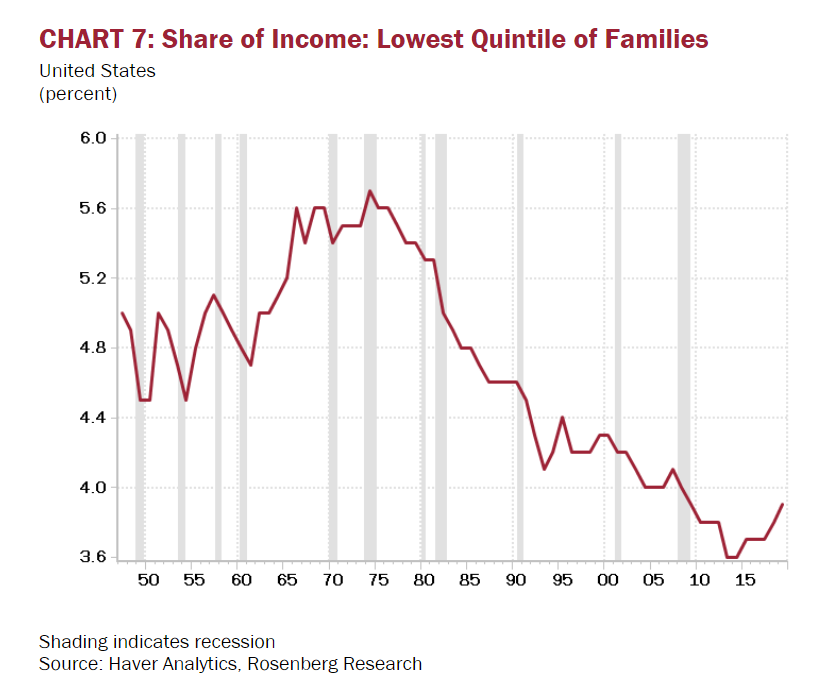

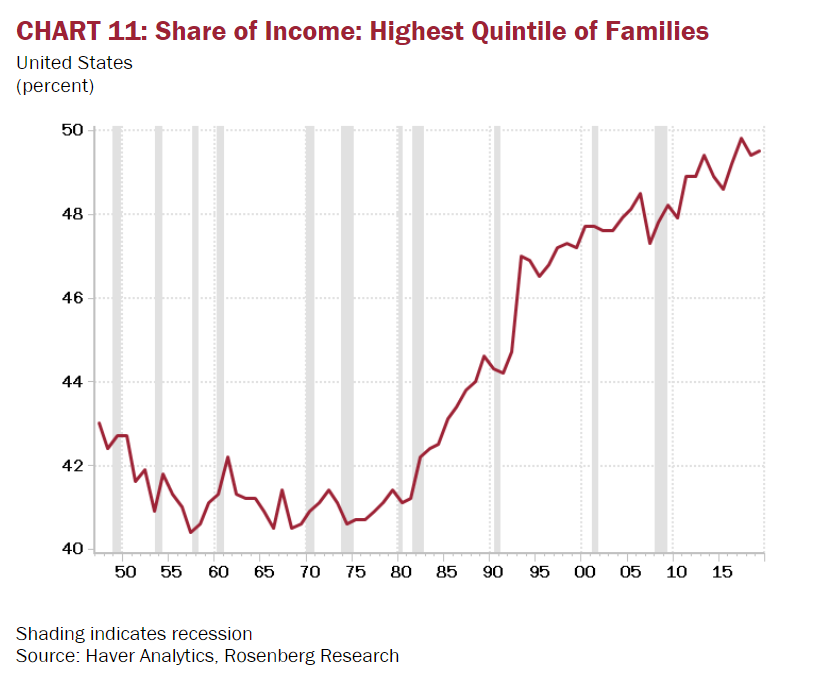

As David Rosenberg recently wrote, the vast majority of Americans have little to zippo exposure to the stock market. For most, it’s whatever she or he has in their 401(k), assuming they are lucky enough to have one. US households own about $40 trillion of stocks but the wealthiest 1% own 53% and the richest 10% hold 87%. This concentration has increased drastically over the last fifty years.

On an income basis, it’s essentially the same story. For the lowest quintile (20%) of income-earning families, their share of the pie has fallen sharply, despite a bounce a few years back (that has likely reversed since Covid). Conversely, the top quintile has seen its share of the total rise dramatically since the mid-1970s. (It’s fair to note that people move around a lot between quintiles; this author was in the lowest 20% in 1975 and now is in the highest--although immensely below the top 1/10th of 1%.)

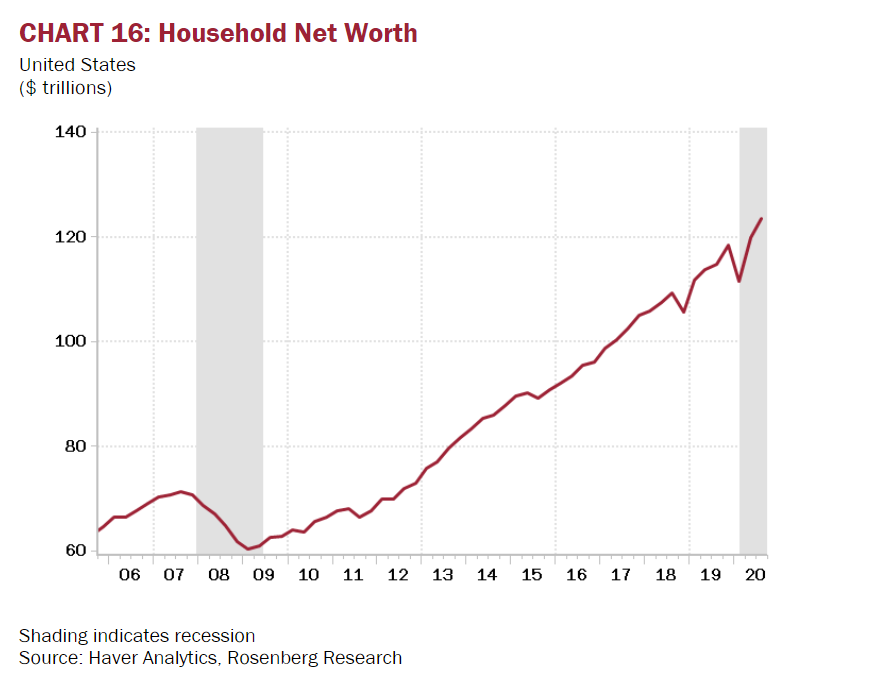

What could be the great, if not great fun, equalizer would be another wrenching bear market. These logically hit those with the biggest stock and real estate portfolios the hardest. Based on the latest Household Net Worth status, a considerable amount of equalization could be in the offing.

Concentration is also an issue in the stock market where the top 10 companies in the S&P 500 make up 28% of its value. The recent inclusion of Tesla is an interesting case study. Index-tracking funds, which directly and indirectly now control trillions, were forced to buy roughly a 2% position in the now nearly $700 billion market cap EV maker. Thus, from a negligible market cap to spitting distance of $700 billion indexers had zero in it but, last month, at an astronomical valuation, they are forced to own a massive position. Index funds are alleged to be an ideal way to capitalize on the inherent efficiency of markets. Again, maybe I’m clueless but this strikes me as the polar opposite of efficient markets.

As the always wittily ironic Jim Grant wrote last month, “Whether or not Elon Musk will ever deliver autonomous driving, we are drifting closer to autonomous investing.” A key tenet of the latter is that markets are always fairly valued by the collective wisdom of the investing crowd. So, let’s end this EVA with a quick overview of how wise that appraisal is right now.

There is actually a parallel between the aforementioned wealth concentration and the highly concentrated nature of today’s stock market where a handful of companies represent such a disproportionate share. As Goldman Sachs explained last month, the market cap weighted P/E is 29, not the 22 that is commonly cited (and is worrisome enough). The bulls would point out that it was 45 back in 1999 but I don’t find that comforting in the least. After all, 45 times earnings was the highest ever, leading to a disastrous bear market (despite much, much stronger US economic and financial conditions back then).

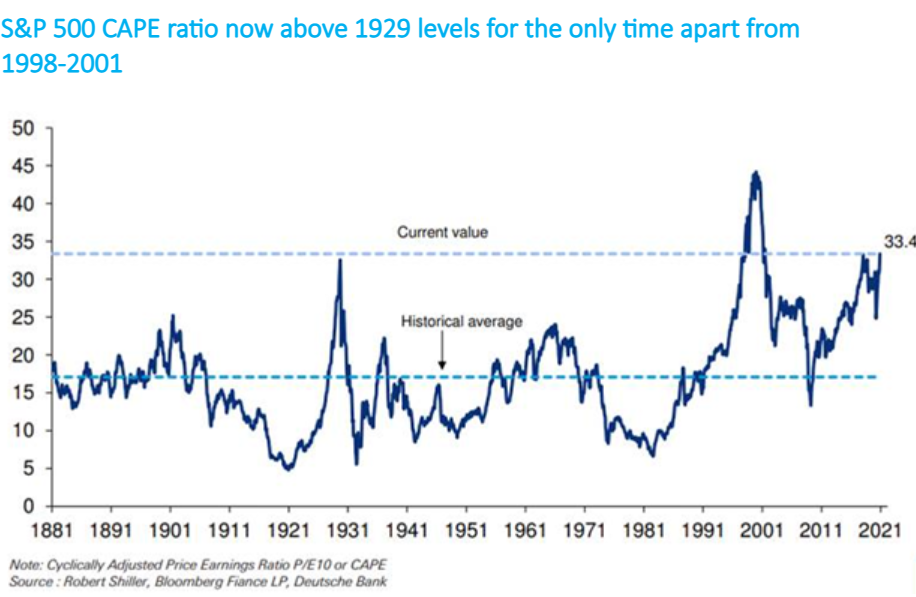

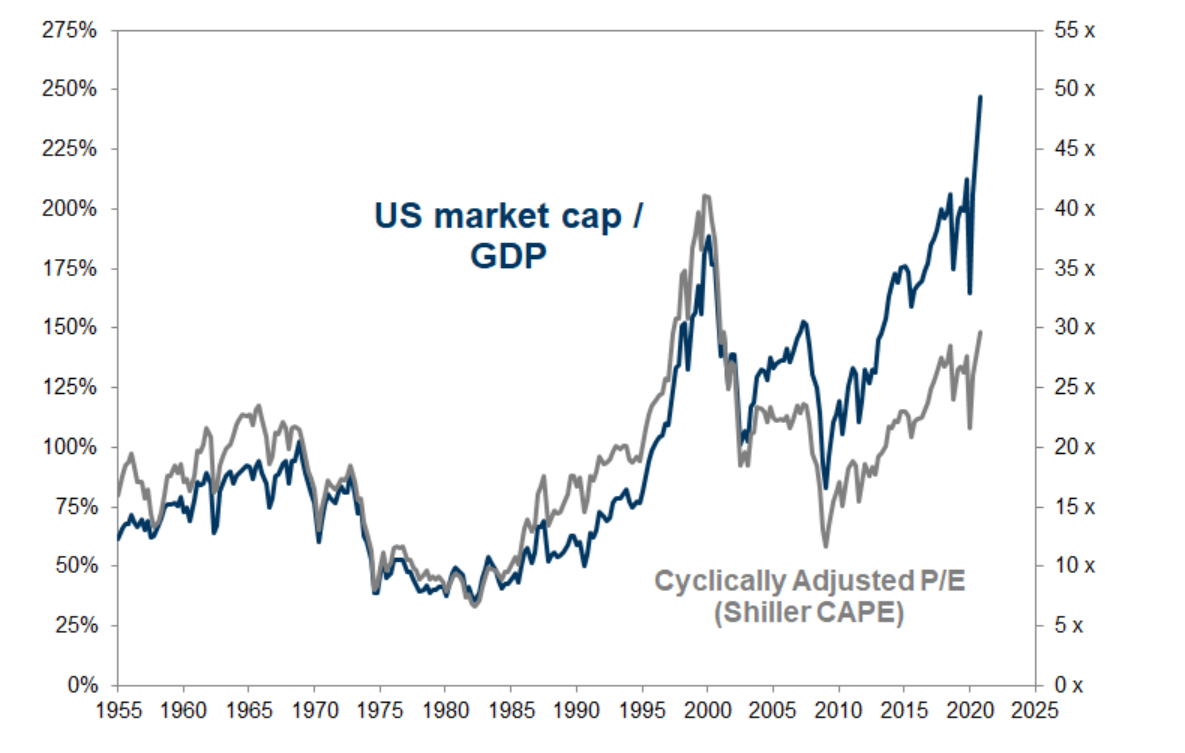

Using the Cyclically-Adjusted PE ratio (or CAPE), which seeks to normalize profits across 10-years in order to get a more accurate P/E, the S&P 500 is now at an equivalent level to 1929 (though still below the outrageous level seen in early 2000. However, using Warren Buffett’s favorite big-picture market over-/under-valuation metric—US market cap vs GDP (or the economy’s total revenues)—we are presently way beyond even 2000.

Then, let’s get back to that supposed towering pile of cash on the sidelines. Actually, institutional investors have one of their lowest cash allocations ever. More worrisome is the record level of margin debt, reflecting delirious bullishness on the part of retail “investors”. (By the way, other studies of cash reserves echo the results of this BofA Fund Manager (FMS) survey.)

Based on all of the forgoing, one has to be a trend-follower of the Jim Cramer persuasion not to concede this is an incredibly expensive, over-bought, and highly speculative market environment. Markets don’t typically go down for no reason, however. Unquestionably, perma-bulls take comfort in this and also the reality that most severe bear markets are preceded by Fed tightening. Without a doubt, a punchbowl – removing Fed is nowhere on the horizon.

Accordingly, one could reasonably conclude any downdraft will be a correction not an implosion. For now, I agree with that, but it doesn’t preclude a total bloodbath in the most hyperinflated parts of the market (where amateur investors are heavily exposed).

Two downside catalysts loom, one of which is a potential while the other is a likelihood. On the first, should the Georgia Senate run-offs both go to the Democratic candidates, giving their party control of all three chambers of government, the prospect of much higher taxes that might portend could be extremely upsetting to the market. While the odds favor the GOP retaining Senate control, they are sliding.

The second risk that investors are blithely ignoring is of portfolio rebalancing. Per our October 16th EVA by another friend of mine, Vincent Deluard, Target Date funds—a mainstay of retirement accounts—are now a market whale—make that a Moby Dick-on-steroids of a whale. Based on the tremendous market appreciation seen since November 1st, these are almost certain to be heavy sellers of stocks in the first couple of weeks of this month as they seek to restore their previous stock-to-bond mix. This may be amplified by myriad taxable investors selling appreciated positions they deferred into 2021.

Whatever the catalyst might be, let me end this EVA the way I started: Take profits—the sooner, the better—even though, or maybe precisely because, Jim Cramer is telling the world to do the exact opposite.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.