“A $100 bill would buy less in 1998 than a $20 bill would buy in the 1960s. This means that anyone who kept his money in a safe over those years would have lost 80 percent of its value, because no safe can keep your money safe from politicians who control the printing presses.”

– Thomas Sowell

______________________________________________________________________________________________________

Introduction

At the end of 2017, Evergreen initiated a special-edition EVA series with excerpts from David Hay’s upcoming book titled “Bubble 3.0: How Central Banks Created the Next Financial Crisis.” The EVA series ended in May 2020, when David finally unveiled his long-running thesis about the Fed’s “End Game”.

Over the past 15 months, David has been working to prep his book for print and has decided to share one chapter ahead of its release titled “The Anti-Bubble Years.” Last week, we ran the first part of this chapter which can be found here. Please enjoy the conclusion to this chapter and be on the lookout for more information about David Hay’s upcoming book launch!

Summary

The Anti-Bubble Years (Part II) by David Hay

Continued from last week…

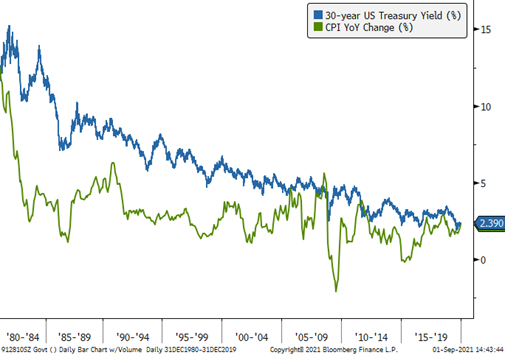

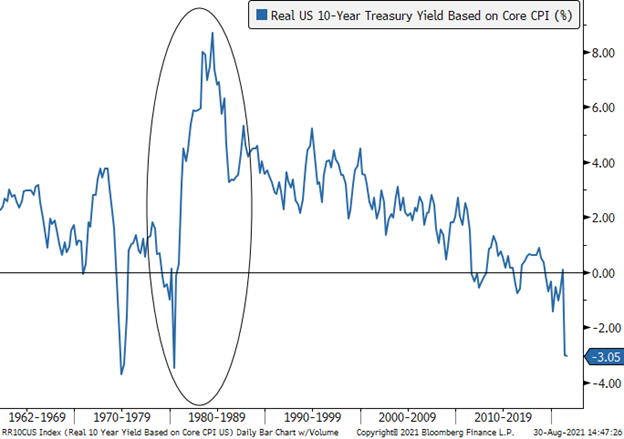

Returning back to the question that opened last week’s EVA, why, for nearly 40 years, was I almost always bullish to very bullish on bonds? The cut-to-the-chase reason was that interest rates were largely positive even after inflation for most of that timeframe. As you can see below, there were very few instances during this era, at least until the post-financial crisis timeframe, when real interest rates (i.e., net of inflation) were not reasonably positive. Consequently, as a bond holder you actually got paid to hold them, a refreshingly quaint, but also increasingly rare, notion.

Source: Bloomberg, Evergreen Gavekal

Additionally, and similarly, inflation was under constant downward pressure. There were a multitude of factors through this four-decade period that kept it in check, if not even push it lower, and I was a believer in their sustainability.

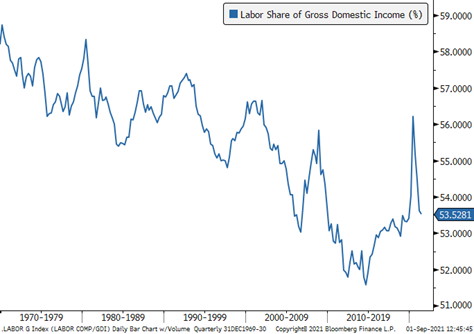

This is a major topic and it would take an entire book to do it justice but I will try to summarize what I believe were among the major disinflationary forces. First up, was the decline of collective bargaining. Union membership for the overall US workforce fell from 29% in the 1970s to 11% today. It’s hard to argue this wasn’t behind a shift in the revenue split between businesses and labor.

Source: Bloomberg, Evergreen Gavekal

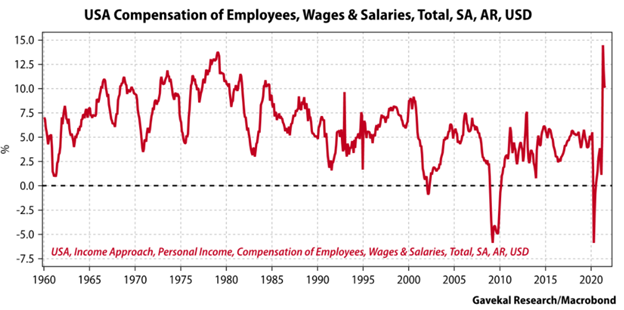

As you can see in the next chart, wage increases have erupted at an unprecedented rate coming out of the Covid recession. Nearly all business owners will tell you that there aren’t many costs that are as hard to cut as wages, other than by layoffs—and right now companies need every worker they can get. With a remarkable 2 ½ million more job openings nationally than total unemployed, that is likely to be the case for a very long time. (It is probable there is an overstatement of unfilled positions occurring right now, possibly because businesses realize that if they need 10 new hires, they better put out a request for 20.)

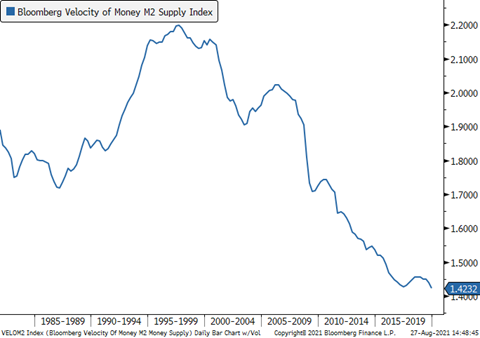

Second, was the long-term erosion in the velocity of money.* With its turnover rate in a persistent slide, it made a serious burst of inflation highly unlikely, at least of a lasting nature. (It is worth noting that money velocity has stopped falling for most of 2021 despite an enormous increase in the money supply; in my mind, this implies an important sea change may be underway.)

Source: Bloomberg, Evergreen Gavekal

Another exceedingly powerful factor in keeping the CPI muted was the ascent of China as a global export tour de force. The shift of production of almost everything to its shores and the related emergence of what became known as “the China price” resulted in actual deflation for many goods. This was heaven for US consumers but often hell for US producers. Entire industries were relocated from the American heartland to the Chinese mainland.

This was allowed by US policymakers to unfold over decades, resulting in massive trade deficits and the loss of millions of high-paying jobs. But it for sure lowered consumer prices in the US. (The ramifications of that laissez-faire attitude toward globalization, China-style, obviously came to a head under Donald Trump and are continuing with the Biden administration. There is little question that the model of having supply chains halfway around the world in ultra-low-cost venues is under siege. As others have noted, the world is moving from just-in-time to just-in-case inventories.)

*Money velocity is a technical concept per the below but a rising reading implies higher inflation, assuming a constant or rising money supply, and vice versa in the case of falling velocity.

Demographics also played a starring role in the taming of inflation saga. As tens of millions of Baby Boomers have aged, we’ve tended to spend less and save more (I’m smack dab in the middle of the Boomer generation, hence the “we”). Going forward, though, it’s possible the $35 trillion that Americans over 70 are estimated to collectively hold will be partially spent down in coming years, reversing this trend, as well.

Two oil busts in the last decade also exerted downward pressure on the CPI, as did the crude crash in the mid-1980s. Based on how pervasive energy is throughout the global economy, this has been a significant disinflationary—and, at times, deflationary—force. Now, though, years of reduced exploration activities, along with recovering demand, are pushing up both oil and natural gas prices. This upward trend is likely to persist for many years in no small part due to governmental hostility toward the domestic energy industry.

Admittedly, this is a very short and simplistic summation of an extremely complex subject and they are all fairly mainstream views of the victory over high inflation that started under former Fed chairman Paul Volcker. The exception on the obvious front might be money velocity which is somewhat esoteric but quite crucial in my view. (Serious economists would point out that it is a dependent variable derived by dividing nominal GDP by the money supply; thus, it is not a driving force but a reactive one. However, regardless of the sequence, the outcome of falling velocity works against rising inflation. I told you it was esoteric!)

However, there was another explanation for the subjugation of inflation and it is one I haven’t read much about in years but it is—or, I should say was—a powerful one, in my view. This has to do with the thermostatic effect of interest rates, at least when they were allowed to be set by market forces (i.e., totally unlike today).

This concept views interest rates/bond yields as the thermostat; when the economy got too hot, the bond market would fall in price*, raising the economy-wide cost of money. Such a reaction would depress borrowing which had a cooling economic ripple effect. If the rate rise was severe enough, widespread bankruptcies often occurred, leading to recessions and, frequently, actual deflation in some goods and services. (Strangely, when the Fed has been on long tightening campaigns and rates have risen considerably, most bond investors are typically reluctant to extend “duration”, a fancy way of saying buying longer maturity debt to lock-in high returns for years to come.)

Such a drastic cool-down, to the point of freezing portions of the economy, can have a pronounced, even terrifying, impact. For example, consider what happened to housing in 2007 and 2008 when mortgage rates soared and home financing became nearly unavailable for a time. Financial ice-storms such as this caused the Fed to heat things back up by cutting short-term interest rates. Longer-term market driven rates would also plunge. Before long, the credit crunch, or crisis, eased and economic growth resumed. Inflation consistently fell, sometimes hard, during these glaciations. Even in the inflationary 1970s, the 1974 recession cut inflation down by almost 60%.

*Bond prices and yields are like a teeter-totter. When prices fall, yields rise and vice versa.

There is yet another, much more cynical, explanation of why inflation has been in such a prolonged dormant phase. This focuses on the way the US government measures the CPI. Starting in 1996, the official arbiter of inflation, the Bureau of Labor Statistics, changed its methodology to what is called chain-weighted.

What this non-descriptive term means in a practical sense is that consumers can switch to cheaper goods when prices for some items and services increase. Thus, when the price of filet mignon is rising rapidly, consumers can switch to something cheaper, like pork. (Another related example is that, in 2021, many consumers of modest means are being forced to shop at dollar stores versus traditional grocery stores due to soaring food prices.)

Most economists seem to have accepted the government’s contention that this is a more accurate way to measure inflation. However, others are much less certain. Perhaps a better name would be “the substitution effect”, or maybe “the trading down effect” but, regardless, when high prices cause consumers to make an inferior preference choice due to rising prices, that seems to me like a negative. And this leads to another way in which the government has controversially suppressed inflation—hedonics.

Hedonic adjustments attempt to take into account improved quality. Whether it’s air bags in cars or vastly improved cell phones, the idea is that if the price goes up but the quality improves even more, then the true cost has actually fallen. With technology, quality has often drastically improved while the cost of almost everything tech-related has crashed. Tech’s inherently deflationary nature has been another material, and totally legitimate, depressant on the overall CPI. (It is important to note this may be changing; the world’s most important chip manufacturer, Taiwan Semiconductor, just raised prices 20% on some of its products.)

Clearly, hedonic adjustments are tricky and subjective. Further, they seem the opposite of chain-weighted where there is debatably the need to create an adjustment for consumers moving down the quality chain. (There is a related stealth influence called “shrinkflation” of which we’ve all been the victim—same price but less quantity per package. I’m not sure government statisticians are fully on top of that ploy.)

One last critical inflation dampener has been housing, oddly enough—in fact, very oddly enough. As we all know, in most regions home prices have gone postal over the last twenty years, despite the 2008 -2009 crash. This has, in turn, priced millions of young people out of the housing market. It has also pushed up rents in a big way. Based on these realities, one would think that housing should have been an upside driver of the CPI. But not according to our infallible central bank.

The Fed’s preferred inflation measure—the PCE which stands for Personal Consumption Expenditures—attributes a much lower weighting to shelter costs than does the CPI. Moreover, it uses something it calls Owners’ Equivalent Rent (OER) which asks a sample set of homeowners how much they believe their home would rent for if they did lease it out. If you think that sounds less than precise, I’m right there with you.

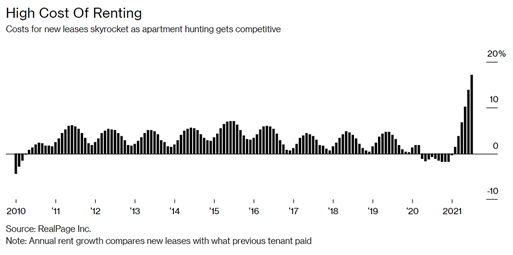

This methodology has almost certainly drastically understated housing cost inflation, particularly since 2000 when home price appreciation began to far exceed the CPI. Since shelter costs are around 40% of the CPI, this is highly significant. Post-Covid, the Fed’s methodology has created even more divergence versus reality, especially once rent abatements have begun to roll off. Rents are now rising at a record clip as you can see in the below chart, 17% above the prior lease rate overall.

Even the Dallas Fed is admitting this pending catch-up, per the venerable Fred Hickey in his typically insight-rich September 1st newsletter. To wit: “Our forecasting model shows that rent inflation and OER inflation are expected to increase materially in 2022 and 2023.” That doesn’t sound very transitory to me.

In summary, most of the factors that have kept inflation subdued for the last four decades appear to be either weakening or outright reversing. This paradigm shift is increasingly looking much more enduring than the Fed believes—or wants the markets to believe. Yet, long-term treasury bonds are trading at their most negative yields since the 1970s, implying investors are buying into the Fed’s transitory inflation meme.

Source: Bloomberg, Evergreen Gavekal

As a result, even though bond yields have soared from their 2020 lows (around 0.50% on the 10-year T-note), for the first time since 1981 I’m not a buyer on weakness. Even when the 10-year hit its recent peak of 1.75% this spring, it was hard to muster any enthusiasm for that puny yield; however, it did rise sharply in price, lowering the yield to 1.25% by late August of 2021. Accordingly, it was, as they say, a tradeable rally. But I have a hard time playing that game, especially when there are a myriad of inflationary winds beginning to blow, even howl.

As recently as late 2018, when the Fed had been raising rates for several years, the 10-year T-note yield moved about 1.2% higher than inflation—3% versus roughly 1.8% inflation. It was also possible to get close to a 5% yield on investment grade corporate debt, generating an even more positive real return. (My team and I once more used this bond sell-off to extend the maturities of our clients’ bond portfolios, something I have done in every bond bear market since the early 1980s. Now, however, I am beginning to wonder if I’ll ever get this opportunity again based on current Fed policies.)

As 2019 unfolded, the yield curve (the difference between short-term and long-term rates) became inverted; in other words, short rates moved above longer rates. This is an unusual occurrence but it does happen when the Fed has been tightening for an extended time and the bond market begins to sniff out a slowdown or, usually, a recession. In fact, an inverted yield curve is one of the best recession predictors around—infinitely better than the Fed, which, as I’ve often written, has failed to warn of a single economic contraction.

Since WWII, there have been nine yield curve inversions and eight of these were followed by recessions in relatively short order. Thus, the yield curve’s batting average has been .889 versus the Fed’s at .000. (Similar to when interest rates have risen materially, many retail investors, and even some institutions, shy away from buying longer-term bonds during inversions. A common—and costly—attitude is “why should I accept a lower yield for a longer maturity?” Answer: Because of the yield curve’s aforementioned recession forecasting track record combined with the reality that economic downturns always lead to lower interest rates.)

This warning signal worked in 2019 and 2020, as well; however, it is impossible to know for sure whether the US would have entered a full-blown recession in the absence of the pandemic. The broadest measure of corporate profits (the National Income and Products Account or NIPA) was already shrinking in 2019 in real terms. Moreover, the manufacturing side of the economy was contracting even though pre-Covid although retail sales were healthy.

Unquestionably, Covid turned what was likely a mild contraction into one of the deepest ever. However, it was also the shortest with the recession ending in April of last year, a mere two months after the official peak of the last expansion.* This coincided with the briefest bear market in stocks ever seen.

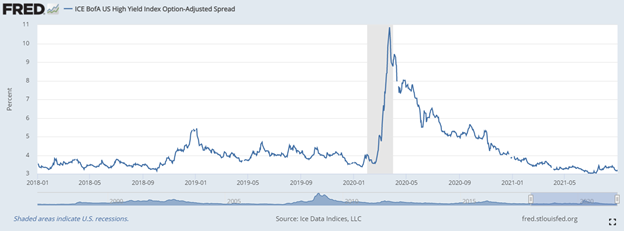

It was the Fed’s announcement in late March of 2020 that it would buy corporate debt which triggered the furious bull market and ended the Covid recession, despite the on-going lockdowns. As I’ve mentioned in prior EVAs (naturally, since it was among my best calls!), this fulfilled one of my wildest predictions: That the Fed would bring down credit spreads during the next crisis. (However, it also stated it would buy junk bonds which I didn’t expect.)

Ironically, and also as I speculated as far back as 2008, it actually didn’t need to purchase large quantities of corporate bonds to cause credit spreads to collapse. By the time the program was closed down by the Treasury Department at the end of 2020—over the Fed’s objections—a mere $14 billion was actually acquired. This is in contrast to the $4 trillion the Fed has bought via its Magical Money Machine of US treasuries and mortgage-backed securities since the pandemic hit. Just the idea that the Fed had the corporate bond market’s back was enough to produce the credit spread plunge seen below. (Falling corporate spreads mean that private-sector bond prices are rising relative to Treasuries; this process has had an extremely powerful and beneficial impact on asset prices, as well as borrowing conditions.)

*It’s fair to note that if government deficit spending hadn’t blown out to 20% of GDP, a deep and much longer-lasting recession would have occurred. Deficit spending always rises during recessions but never before to anything close to this level.

Consequently, in the late summer of 2021, a bond investor is faced with a situation 180 degrees removed from the time in 1981 when I became a bull on bonds. Instead of a real rate of return far above inflation, we’re facing yields that lose money each and every year even if the Fed’s 2% inflation target can be maintained. If I’m right, and we’re facing much higher consumer price increases than that, bonds will be certificates of confiscation to a degree they haven’t been since the 1970s.

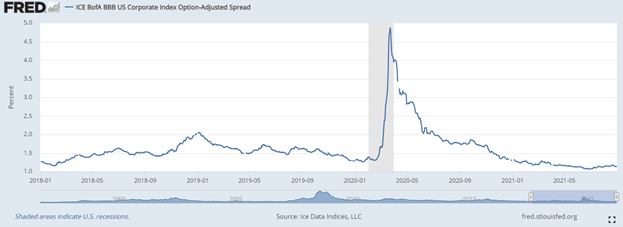

Similarly, corporate spreads are down to levels that offer little compensation for default risk. This is particularly true with junk bonds which now, for the first time in history, also have negative real yields. (Obviously, junk bonds have far greater default risk than investment grade debt but even the latter sometimes go belly-up.)

My love affair with the bond market has been a long and blissful one. There were times when I would briefly jilt it, such as late in an economic expansion as inflation was heating up and the Fed was in the early stages of tightening. But this time is different—radically different, in my view. Those are always dangerous words to utter in the financial markets. But, then again, when was there a time, outside of war, when the US government was engaged in Modern Monetary Theory?*

In a subsequent EVA, we will examine an inflationary force that, in my mind, has the potential—in fact, I’d say probability—of being among the most potent, giving MMT a run for its money--literally. Moreover, it’s one that very few pundits and financial narrative-spinners are discussing.

In the meantime, if you are heavily exposed to longer term US bonds be afraid—very, very afraid—of the current fiscal and monetary policies being pursued in this country. And don’t get sucked in by the sucker’s rally that we’ve seen in the bond market in recent months. It’s likely to last about as long as the government’s next debt ceiling.

*Modern Monetary Theory (MMT) holds that a government, like the US, which issues debt in its own currency, can spend without regard to budgetary constraints, at least until inflation becomes uncomfortably high. It also asserts that should there not be enough willing lenders to the government, at acceptable interest rates, then the central bank (aka, the Fed) should buy treasury debt with fabricated funds. There is no doubt in this author’s mind that the US is currently engaging in MMT and, as I have described, inflation is already becoming problematic.

David Hay

Co-Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.