“Who needs us (CNBC)? The roulette wheel pays off for black and red right now.”

– Jim Cramer, commenting on current market conditions as of 6/16/20

“The volume of fiscal largesse already in the system and to come alongside the gargantuan monetary accommodation means the total amount of policy stimulus this year alone will approach $10 trillion. (This) will swamp the hole in the economy caused by the pandemic…by a factor of five.”

– Famed economist David Rosenberg, referring to America’s unprecedented virus crisis response

______________________________________________________________________________________________________

Reputations are hard to shake, even those that are unfairly attributed. In my case, this was a function of my frequent warnings that stocks were overpriced for most of the second half of the former 10-year bull market. Another contributing factor in the perception that I was a perma-bear was my constant harping on the theme that the prosperity we saw in the most recent expansion was of the pseudo variety.

My contention was that the weakest expansion in the post-WWI era was only achieved through trillions of Fed-created money and, after Donald Trump’s election, the first trillion dollar deficits (or about 5% of GDP) during a growth cycle. As most of us know, deficits relative to GDP usually contract when the economy is growing. The sad fact of the matter is that never before in American history had the federal deficit exploded as it did during the first three years of the Trump administration, even as the economy grew at a slow but steady clip (with a fleeting spurt in 2017). The fact that I kept pointing out this reality in these pages no doubt further stereotyped me as a stopped-clock bear.

Hopefully, the qualified buy recommendations made by this newsletter in December, 2018, when the S&P nearly fell into an official bear market, and, more importantly, the strong buy urgings during the “March Madness” this year, have served to eradicate the perma-bear label. (Emphasis on “hopefully” due to the aforementioned tendency for many to perpetually pigeon-hole other individuals.) If not, perhaps this EVA edition will finally do the trick. As a sneak preview, I am optimistic for further gains, at least for certain market sectors, once the current euphoria recedes.

Candidly, my outlook has evolved from “buy almost everything” during the most intense panic phase of the 41-day-long bear market, to being concerned that the market had gotten ahead of itself by early May, to coming to believe a few weeks ago that there were great opportunities in what Evergreen has been calling the “Virus Victims”.

During much of May, my fear was that the looming liberation from hibernation was going to be problematic and that any infection spike would be pounced on by the usual apocalyptic media sources like Gloomberg Bloomberg. The deterioration in US/China relations, with the potential for a military skirmish between the two countries in the Eastern Pacific, was another mega-fear of mine. Then, there was the risk of an implosion of the always fragile European Union (EU). Finally, on my list of major worries, was the increasing possibility of a leftward lurch in US politics come November, with the recent shocking and nationwide civil unrest elevating those odds even further.

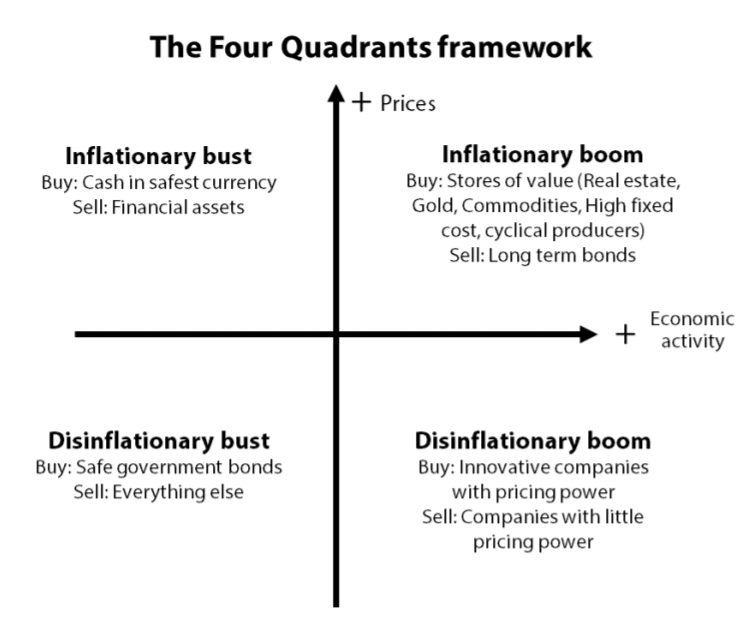

It’s clear from a number of recent client conversations that most investors are also mystified by a stock market that’s almost fully recovered from its nearly 40% crash during the 41-day bear market, the shortest, but certainly not mildest, bear market on record. My response to their bafflement has been largely a variation on a long-time Gavekal template that is the key aspect of this EVA and one that I will now describe. With apologies to those who are already familiar with this matrix, it basically divides the investment environment into four quadrants, as shown below.

Source: Gavekal

Obviously, this is a simplification of what is always an exceedingly complex market and economic eco-system. Yet, it serves a valuable purpose in at least roughly approximating the dominant conditions at a given point in the overall cycle.

Also, most obviously, we are currently in the southwestern, or lower left-hand, quadrant. In fact, it’s probable we’re virtually off the chart to the bottom left, in what is likely Deflationary, not just Disinflationary, Bust territory. Or at least we were way, way back in March from a market standpoint and, based on economic activity, if you can call it that, we still are. Prices for many goods and services have been falling at a terrifying rate, outside of the various sectors that are stay-at home winners, like food purveyors, cloud software companies, and PC vendors. This has caused a rare negative 2% reading even in core CPI (the most non-volatile) on an annualized basis over the past three months.

Certainly, from early-February to around March 23rd the basic investment strategy for this quadrant of buying government bonds and selling everything else was the only way to generate gains during the 41-day bear market. More importantly, it was nearly the only way not to lose money. As indicated in our March 20th EVA, even investment grade corporate bonds were down by 20% and preferred stocks had cratered by over 40% during the worst of the March Madness. This was a worldwide margin call, with almost nothing spared, as was also the case in 2008/2009, during the Global Financial Crisis.

Incredibly, the current bull market has already risen nearly 50% and, frankly, even the grumpiest perma-bears (those that never stopped growling even in March with stock and corporate bond prices in free-fall) have to concede a new bull has been born. It hasn’t come of age as fast as the six-week bear but it’s been, staying with mammal metaphors, one whale of a move in about 80 days.

Thus, what we’re seeing is an economy that is busting at a deeper and more rapid clip than the Great Depression and yet a stock market that is booming like few have in the past. As a result, there has been a complete divergence between the quadrants in which the economy and the S&P 500 presently reside. For sure, stock markets are forward-looking but, nonetheless, this is a startling dichotomy. So, again, what gives?

As usual, the answer lies in the Mariner Eccles building wherein also lies the Fed (far be it from me to imply from this word play that the Fed is deceitful—perhaps hypocritical and delusional but not really, truly deceitful). The Fed has moved with the speed of light in a perfect vacuum (or my wife heading into Nordstrom’s for their anniversary sale) to stop a health and economic disaster from cascading into a lasting market melt-down. What took it many months to do in 2008 and into 2009 happened in mere weeks this time.

The Fed’s unparalleled rescue measures – which includes our once-derided view that it would resort to buying corporate bonds with funds from its digital printing press – have unquestionably been the game-changer for stocks. The same has been true with credit spreads* which, as these pages have long noted, exert enormous influence on stock prices as well as, of course, on corporate bonds. Accordingly, as we anticipated years ago, credit spreads are too important to be left to market forces, at least in the ever-more interventionist mind of the Fed.

*Credit spreads are the difference between the yield on government and corporate bonds. When this spread widens dramatically, it is an extremely bearish event; conversely, big declines are very bullish.

Ironically, the Fed has actually bought very little in the way of corporate debt (though it did more this week). Rather, it’s mere promise to enter this market with its unlimited checkbook did the trick of bringing spreads down “bigly”. Frankly, it was a masterstroke of market manipulation, a gambit that I both admire and detest. As I’ve admitted before, I wish it hadn’t come to this but long ago I didn’t see any other way out of the next crisis which, of course, hit us this winter like a Category 5 hurricane.

On the other hand, when it comes to money printing to buy government bonds, the Fed has gone light-years beyond the posturing phase and right into hyper-drive. It has literally been matching, on almost a dollar-for-dollar basis, the three trillion or so of deficit spending the US government has been doing to keep the economy from totally shutting down, which would have left millions of Americans ruined and starving. Consequently, America’s money supply is doing a moon-shot that must make even Elon Musk jealous.

Although the surge in the S&P 500 from its 2237 low on March 23rd to around 2900 two months later was almost exclusively a Fed-driven event, to be fair, the next move from 2900 to over 3200 coincided with real-world developments. It was over the last month that it became clear the US economy was going to re-open and that it wouldn’t be a disaster as so many in the media, like Bloomberg, had predicted. Then, on June 5th, a stunningly positive jobs report was released showing millions of jobs created rather than shed, as had been forecasted. (Count me among those who feel the job gains were overstated but it was, regardless, a serious positive surprise.)

Consequently, we’ve got a blissful situation, at least for stocks, of a recovering economy, trillions of the Fed’s bogus bucks coursing through the system, and plenty of excess capacity that prevents an inflationary overheating. In other words, we are moving from the Deflationary Bust phase into the Disinflationary Boom stage. As nearly all serious students of stocks know, the market loves the latter condition, often known as the Goldilocks scenario; i.e, not too hot and not too cold. (Note, in the Gavekal schematic shown above, the sequence moves counter-clockwise.)

If history is any guide, this is the sweet spot for making money in stocks. The Fed feels no need to tighten and, actually, in these troubled times it is almost certain to continue to pump in additional trillions it conjures up from its magical money machine. The parts of the market that should be the biggest beneficiaries are those that were most seriously mauled by the 41-day bear market. These tend to be the more economically-sensitive sectors which also stand to enjoy the strongest snap-back from the economy climbing out of its bunker. This is exactly what we’ve seen in recent weeks with the hardest hit stocks – like energy companies, airlines, and cruise-line operators – leading the market charge.

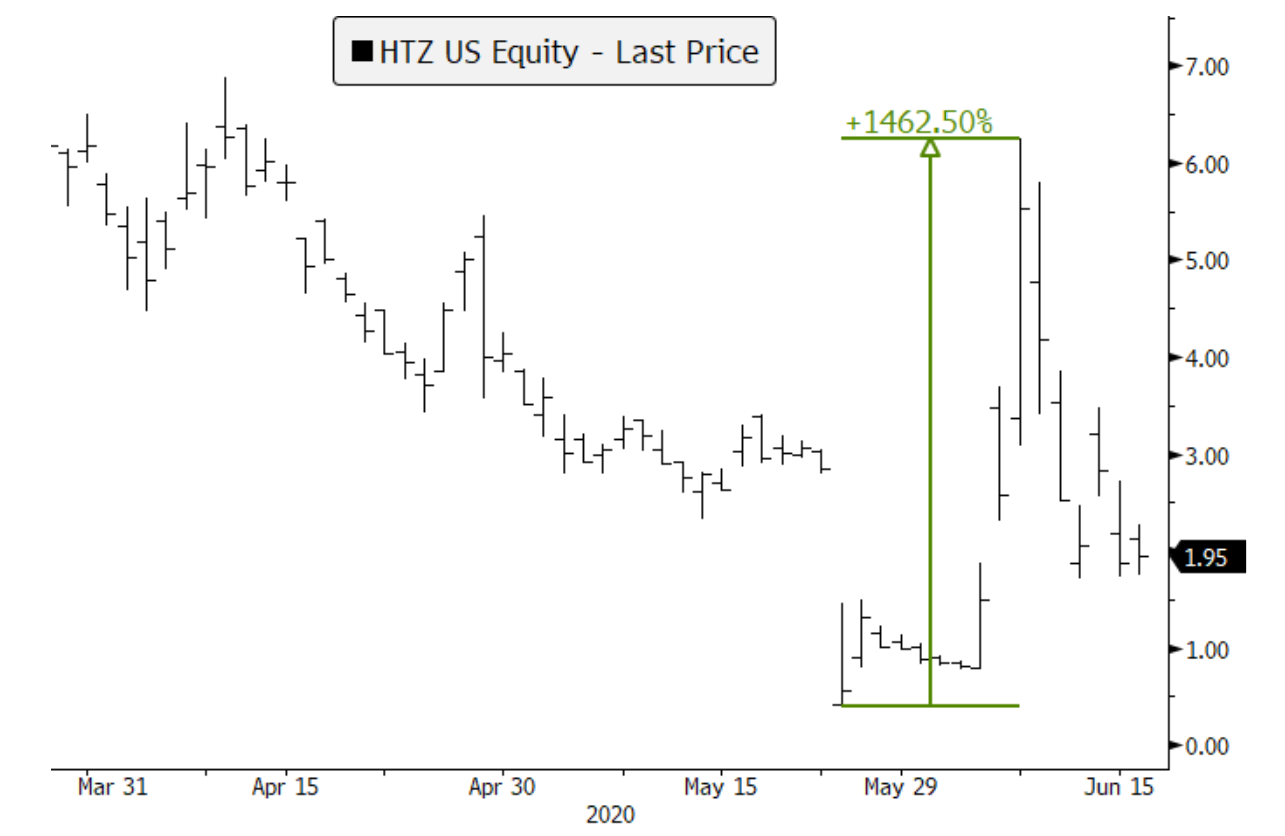

If you think I’m about ready to insert a caveat, you’re as prescient as my old friend Clair Voyant. There’s been no June-gloom this year when it comes to the riskiest stocks; in reality, it’s been a full-blown June-boom. Not only have the sexy story stocks like Tesla, Shopify, and Chipotle been en fuego, companies like Hertz, which has already filed for bankruptcy, have been on white-hot…or at least they were.

It’s clear the aforementioned stay-at-home day traders who have too much time on their hands and government stimulus checks burning a hole through the pockets of their gym shorts, are driving these ultra-risky names up at a sizzling rate. Hertz rose from 40 cents per share in late May (intraday low) to $6 by June 8th, for a cool 1462% gain in two weeks, before its return to reality plunge of 65% back down to a recent $1.95, showing how much it hurts to speculate in “securities” like Hertz. (Because companies that file for Chapter 11 protection typically end up wiping out equity holders, the probability is Hertz stock will find very durable support at zero, totally torching the amateurs playing with fire by investing in this name. Further, in an amazingly cynical ploy, the company actually attempted to sell up to $1 billion of its likely soon-to-be worthless shares this week. That the bankruptcy court allowed this flagrant rip-off of gullible investors to proceed is appalling. Fortunately, the SEC intervened.)

Source: Bloomberg, Evergreen Gavekal

Then came Thursday of last week. In one day, the S&P 500 fell 6% with the small cap index tumbling 7%, bringing the latter’s three-day swoon to 11.74%. Because I hate to rush the EVAs I write, I like to start creating them about two weeks before they are published. While that’s a lower stress way to go, it can lead to getting “scooped” by current events. On that point, I had written this section on Saturday, June 6th, six days before last week’s market face-plant (seriously!):

“To be concise, this market needs to cool off before it can mount its next advance. A correction of 5% to 10%, or even a bit more, seems highly probable, a pull-back that would stun and terrify all those stock flippers who’ve been earning easy money in recent weeks.”

Indeed, the playthings of the day traders were particularly crushed by Thursday’s crashette, as the above chart on Hertz illustrates. Yet, Friday brought a powerful early morning recovery, one that faded almost totally by mid-day before the S&P closed up a decent, but less than impressive, 1.31%. It’s doubtful that Thursday’s sudden reversal of fortune has fully absolved the investment world of its speculative sins. The hubris and greed have been far greater than a one-day shake-out can rectify.

If you think I’m exaggerating, consider these recent comments from Dave Portnoy, founder of the sports betting website Barstool Sports, aka, Davey Day Trader: “Stocks only go up, this is the easiest game I’ve been part of. It took me a while to figure out that the stock market isn’t connected to the economy. I tell people there are two rules to investing. Stocks go up, and if you have any problems, see rule Number 1.”

This is undoubtedly one of those quotes that is destined to go down in the annals of horrible investment calls, right up there with Irving Fisher’s 1929 proclamation that “stock prices have reached what looks like a permanently high plateau.” Unquestionably, Davey Day Trader (DDT) is several intellectual notches below Professor Fisher, who was one of America’s first and foremost economists, despite his defective market judgment. But DDT may prove as toxic to his legions of online followers as the famous DDT spray is to mosquitos. The exact number of those who follow his touts is murky (it is rumored to total around 1.5 million) but what is clear is that there are enough of them to move the busted stocks of bankrupt companies to massive percentage moves, squeezing the professional short-sellers in the process.

Equally obviously, his comment that stocks only go up is ludicrous, especially in light of what happened in March; yet, there are a couple of profound aspects to what he said. The first is the revelation of the casino atmosphere the Fed has created over the years with its huge bias toward easing every time the market hiccups. In a way, DDT isn’t totally wrong. He’s basically articulating a version of the Fed put theory – essentially, that our dear central bank won’t let stocks stay down for very long.

DDT’s not alone in having amnesia about the long grueling bear markets of yesteryear—like 2000 to early 2003—and is, instead, cognizant only of the quasi-flash-crashes that have happened since then. Even the gruesome bear market of 2008/2009 only lasted six months. And, as we’ve seen, the latest was less than a month-and-a-half.

His truly dead-on point, however, is when he said: “It took me a while to figure out the stock market isn’t connected to the economy.” Bingo! This is another condition the Fed has created. It’s one that ace economist David Rosenberg has been describing for years. That’s why the stock market returned almost 16% per year from February 27th, 2009, through February 28th, 2020, despite an economy that only grew at 2% per year. (Stock prices were depressed in early 2009 but not nearly as undervalued as at the bottom of most bear markets.) This a good segue back to the Gavekal Four Quadrants Framework.

Coincidentally, Charles Gave himself revisited this subject again last week as I was working on this EVA edition. One of his key points in that note was the concept that for the last 40 years, there has really only been a move between a disinflationary boom and a disinflationary bust; i.e., there have been no trips into the upper two quadrants of inflationary booms and busts. From a purely CPI standpoint, he’s right. Also, focus on the disinflation not deflation. The reality is that even right now, during a GDP crash that is right up there with the worst of the Great Depression, the CPI is only mildly, and likely fleetingly, dipping into deflation (the latest reading for May was -0.1%). But, in my opinion, realizing my own temerity, there are actually two GaveKal matrices.

The first is the one described above referring to inflation in consumer and wholesale prices (the PPI, or Producer Price Inflation). As Charles writes, that has merely oscillated between the lower quadrants for decades. But where we’ve gone full circle—or full square, in this case—is with asset inflation and deflation. Over the last dozen years, we’ve done at least two complete cycles through this matrix. Now, we appear to be starting a new one with the cursor already having moved from deflationary bust in March to deflationary boom now.

Admittedly, this is where there is some overlap between the two quadrant frameworks. It’s the extreme excess slack in the economy that is creating mild price deflation and the Goldilocks condition I described earlier. Thus, there is no threat of any Fed tightening a la 2017 and 2018 (which led to the brief but sharp correction at the end of the latter year). The only substantive knowable threats to stocks right now are excessive greed such as from the DDTs of the world (and the related Robinhooders*) and/or from a really nasty series of COVID infection spikes (putting aside, for now, any escalation of the US/China rift). There are times when markets correct hard just because prices are too high and I believe this is one of them, at least with what I’ve long called the COPS (the Crazy Over-Priced Stocks). Thanks to DDT, et all, this cohort is crazier than ever.

Consequently, one could argue that some parts of the market are already in the inflationary boom quadrant with an inflationary bust segment up next. But for the overall market, in my view, we’re not there yet. Once the inevitable flush-out of the flippers’ gross speculation occurs, the stage may well be set for the next up-leg, particularly in the “Virus Victim” market sectors. The upward pull of the Fed’s fabricated trillions and a recovering economy are almost certain to be a powerful bullish concoction.

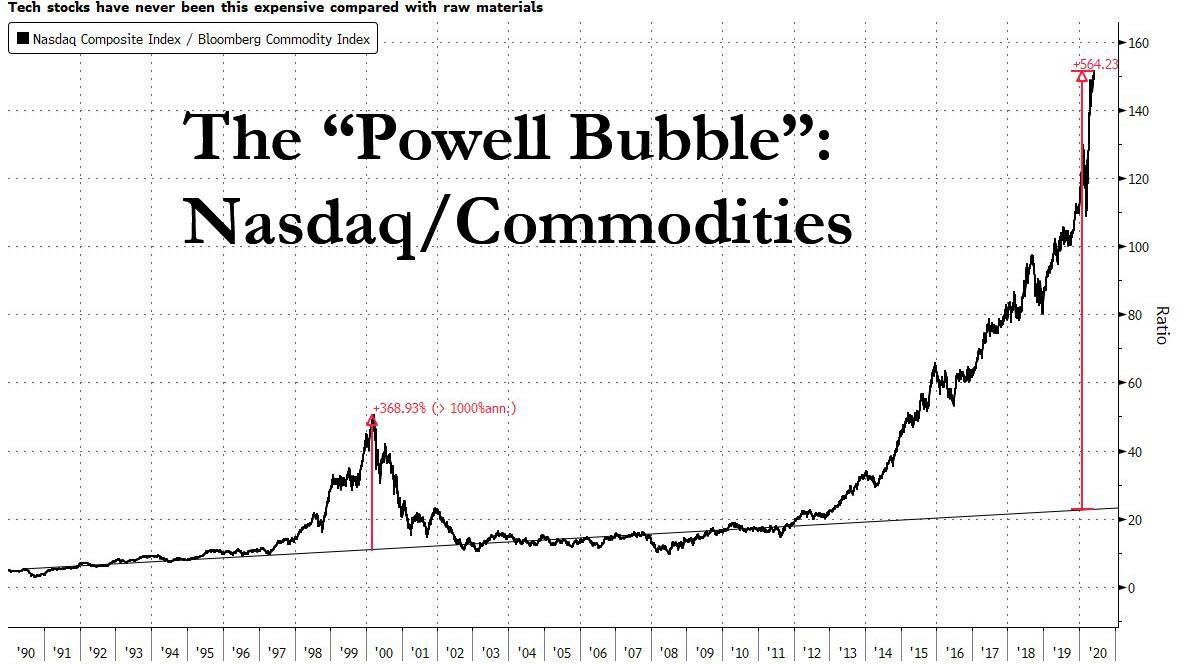

But Charles and I both believe the paradigm of the last 40 years—very little fluctuation in consumer prices combined with wild and upwardly trending swings in asset prices—is likely coming to an end. We also feel the era of stocks crushing commodities is similarly concluding. The chart below vividly illustrates this stunning (and highly likely to reverse) divergence.

*Robinhood is a trading app widely used by stock flippers.

Source: Zero Hedge

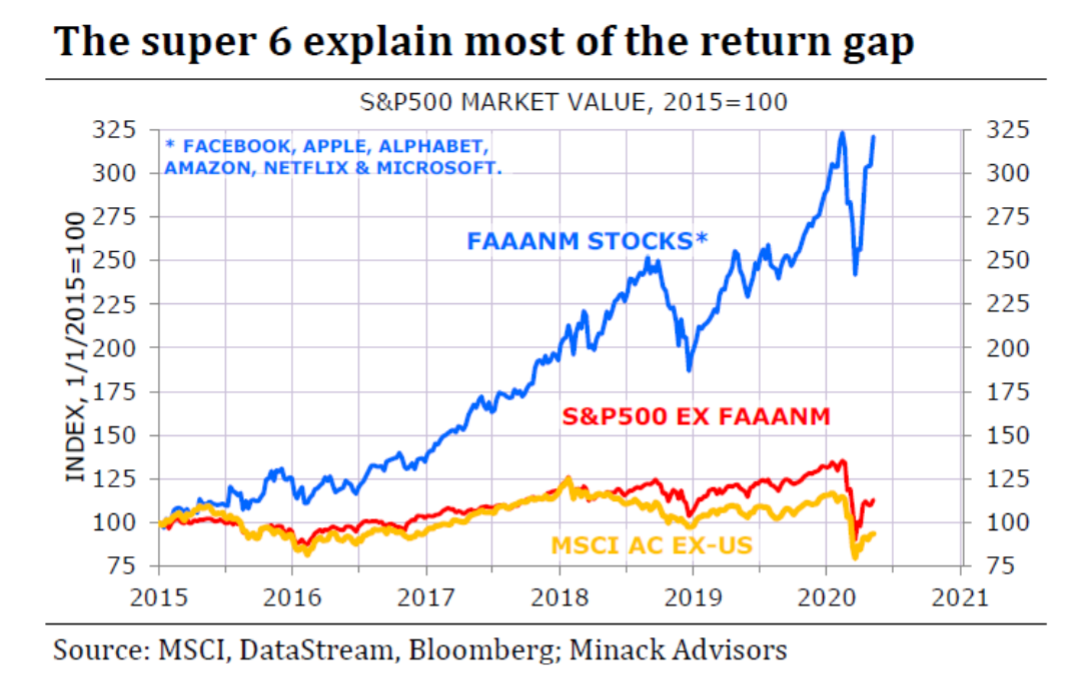

As we all know, the NASDAQ, heavily dominated by the FAAANM stocks – Facebook, Apple, Alphabet, Amazon, Netflix, and Microsoft—has been where market leadership has come from. Another chart underscores that reality.

Ergo, for the last 40 years, and especially the last ten, being heavily invested in tech—and lightly invested in commodities, if at all—has been the triumphant strategy. This was despite the first three rounds of quantitative easing (QE) through which the Fed created about three and half trillion dollars of fake digital money. During the early days of QEs I, II and III, many assumed that high consumer price inflation (i.e., not just stock and real estate inflation) was inevitable, as I’ve written in the past. Yet, as I’ve also previously observed, it didn’t happen in no small part due to the US government’s deficits tapering during the Obama years. Basically, monetary and fiscal policies were heading in opposite directions. Not so, today—in fact, it’s the polar opposite.

We’ve now got a multi-trillion dollar torrent of fake money and deficit spending happening simultaneously. This is very, very powerful stuff and its power is likely to be manifested as the economy gains momentum. The key to the latter is, of course, consumer spending which in America represents 70% of GDP. Based on the staggering growth in consumer savings—due to the government more than offsetting the income losses for most people and the limited ability to spend during the lock-down—the potential for a massive burst in consumer outlays as the year progresses is considerable.

Per earlier EVAs, what we’ve essentially got is a real-life application of Modern Monetary Theory or MMT. Some quibble that it isn’t precisely how its advocates have outlined it but when someone as prestigious and predictively accurate as Howard Marks is calling it out as such, that’s good enough for me. Further, based on what appears to be both a done-deal additional trillion dollar stimulus package (i.e. even more deficit spending) and a Fed intent on monetizing* that splurge, it’s going to be a case of MMMMT or Much More Modern Monetary Theory.

Presently, long-time believers that the US would continue to move only between the lower two quadrants of disinflationary booms and busts, such as David Rosenberg, concede that a few years from now we could be heading into the upper tier. However, like Charles, I believe it could happen much faster than that. For one thing, it’s vividly clear that the pace of bull and bear market cycles has drastically accelerated of late. For another, almost no one is prepared for such an outcome and, as Charles frequently points out, the markets love to surprise the consensus.

An even more compelling argument in favor of a not-too-distant venture into the two upper Gavekal quadrants is the history of past Modern Monetary Theories. Admittedly, they were never called by such a fancy name in the past but for all intents and purposes their essential characteristics were the same: in order to cope with some kind of existential shock—usually military wars but in this case a virus war—the government employing a MMT “solution” would spend unprecedented sums and its central bank would finance those with its equivalent of a printing press.

In the old days, it was usually done in the literal sense. Hence, the grainy newsreels of Germans in the Weimar Republic trying to buy bread with wheelbarrows of trillion “Papiermarks” after WWI. But a more apt example, because it was so convoluted (like everything the Fed does these days), and it involved both enormous amounts of debt and asset bubbles, was what happened in France in the early 1700s. (For more details on this event, please use this link to our “Can an Acronym Save the World” EVA from April 5, 2019.)

The good news is that we probably have more time in the sweet spot of the lower right-hand quadrant. There could be some very sweet profits indeed to be made in this phase. If so, recycling those into an increasing amount of hard assets to prepare for what could be a return to the 1970s-type decade, or worse, might be more than prudent—it just could be portfolio and lifestyle preserving.

In that regard, I thought it would be both fun and illuminating to end this issue with an email I recently received from Charles’ son and my great friend and partner, Louis Gave:

Talking of the US$6tr in additional deficit, here is a little quiz for your team:

Q1: How much did the Marshall Plan cost

A: US$12 billion (in 1946 money), or roughly US$130 billion in current dollars

Q2: How much did the Apollo program cost?

A: US$25 billion in 1973 US$, or US$150 billion today

Q3: How much did the Vietnam War cost?

A: US$168 billion in 1975 money or US$950 billion today

Q4: How much did the New Deal cost?

A: US$42 billion in 1933 money, or US$700 billion today

Q5: How much did the war in Afghanistan cost?

A: US$3 TRILLION (and counting…)

Q6: How much will COVID end up costing?

A: Probably around US$6 trillion

So, to put things in perspective, COVID will end up costing roughly 46x the Marshall Plan (which rebuilt Europe post WW2) in constant US$ terms.

Good thing there is no inflation!!!!

*A central bank engages in debt monetization when it buys its government’s bonds with funds it creates, either from a printing press or a computer, to finance deficit spending.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.