“The annual press focus on (the Social Security fund’s) insolvency dates has always been somewhat misplaced. What’s really important is the magnitude of the shortfalls and the difficulties of correcting them, which grows every year.” CHARLES BLAHOUS, former public trustee for the Social Security and Medicare programs, from a Wall Street Journal Op-Ed on June 8th, 2018

______________________________________________________________________________________________________________

Regular EVA readers are no strangers to Danielle DiMartino Booth, former senior adviser to Dallas Fed President Dick Fisher before and after the housing bust. Even sporadic viewers of CNBC are likely to have seen her repeatedly interviewed on nearly all things Fed-related. This month’s Guest EVA is a slightly condensed version of a recent issue of her main newsletter, Money Strong. (Per the June 8th EVA, Danielle has unveiled a new service, The Daily Feather. We had some technical glitches in linking to it earlier but please click on this link to check it out. It’s an exceptional value for just $25 per month.)

For those wanting the ultimate in a speed-read, I’d suggest perusing her underscored sections. However, if you do, you will likely want to slow down and thoughtfully review some—or all—of the rest. Here are a couple that particularly caught my eye: “The lower rates are, the more governments can live the lie that debt-driven prosperity comes at a negligible cost.” The other was: “Baby boomers are no longer an actuarial assumption to be fudged with corrupt accounting. They are now a cash flow reality.”

In case you think she is being hyperbolic with the latter line, please note that Social Security and Medicare have both admitted they are going cash flow negative years earlier than originally forecast. This means their cash outflows exceeds their inflows. As a result, Social Security now needs to tap into its “trust fund” for the first time since 1982, which is nothing more than a pool of US government IOUs.

Accordingly, the trustees for Social Security and Medicare are being forced to begin selling off their treasury holdings. On June 5th it was also disclosed that Medicare will become insolvent by 2026, three years earlier than expected. Social Security is poised to follow suit eight years later in 2034. This means the initial trickle of selling will gradually turning into a torrent. Effectively, this creates a triple-tightening with the Fed raising rates, selling down its multi-trillion treasury portfolio, and, now, Social Security and Medicare also in liquidation mode.

As Danielle points out, Social Security is far from the only retirement plan in trouble. It’s a global phenomenon as retirement funds have been collateral damage of central banks’ nearly decade long campaign to grind interest rates down to nothing (or less) and drive up asset prices.

Pension-type funds are always in chronic need of investment yield to off-set their future—and rapidly accruing—liabilities as baby boomers head into their “golden years” (which, sadly for many, are looking more like their “beholden years”). As a result of this global interest rate extermination (save for the Fed’s belated and speed-of-a-glacier hiking cycle), retirement plans are stretching for yield in all the wrong places—at least at this stage of what I’ve been calling Bubble 3.0.

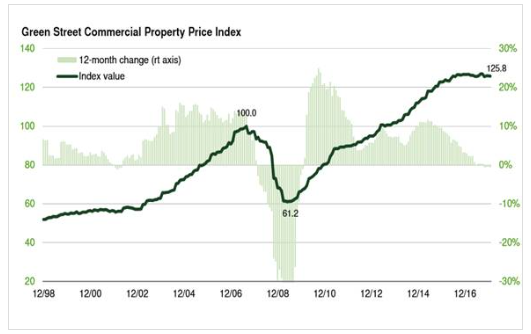

To wit, in a comprehensive recent survey of pension managers, 56% plan to add to their commercial real estate allocation. However, based on the following chart, their timing might be more than a tad inopportune. Prices are now above what was considered the mother of all property bubbles (adjusted for inflation, roughly back to those epic levels).

As Danielle further discusses, demographics are a massive problem for the increasingly aging developed world. This is a very big deal because economic growth is strictly a function of labor force growth plus improvement in productivity (for nerds, total factor productivity). In other words, aging societies need to generate exceptional efficiencies gains (more output per unit of labor and capital input) to offset the drag from a shrinking or stagnating work force. (The US is actually in better shape than many other countries thanks to the echo baby boom. By 2025, America is projected to have 33 old folks per 100 of working age—versus a 25/100 ratio now—but Germany will be 44/100 and Japan at 58/100. No wonder the latter is at the forefront of robotics!)

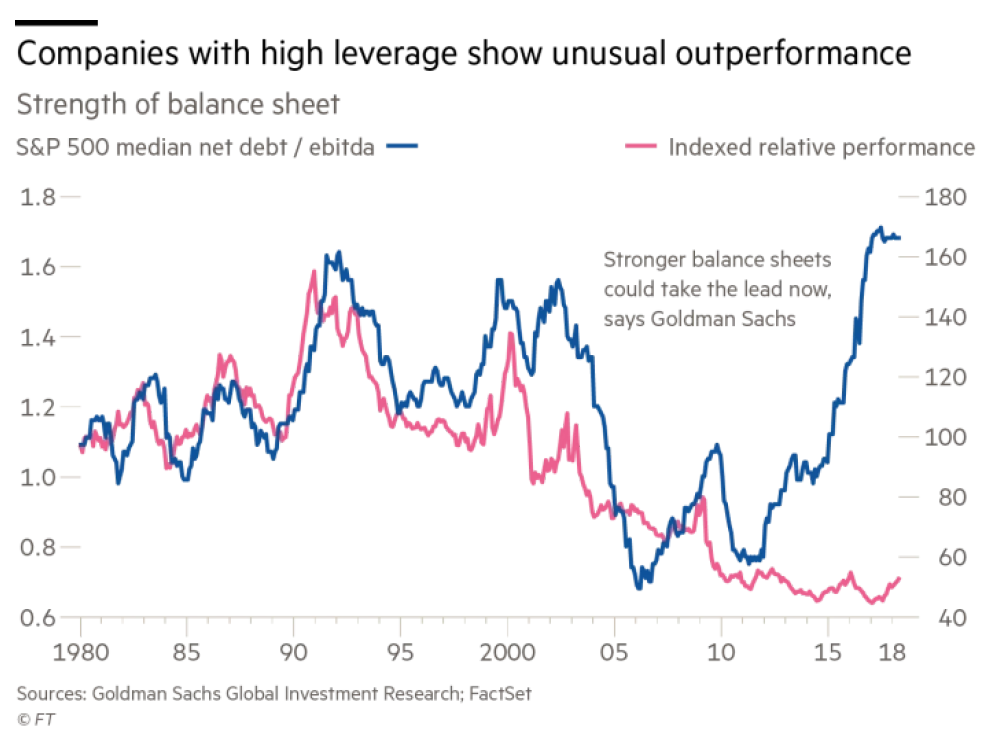

This is another downside of central bank money-for-nothing policies. Corporations, especially in the US, have used low-rate debt to leverage up their once pristine collective balance sheets to buy back trillions of their own increasingly overpriced shares at the expense of reinvesting in plant and equipment. This has been especially true outside of the tech sector.

*EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization and is synonymous with gross cash flow

Core capital spending has been flat for almost twenty years and that’s most definitely not a good thing. “Cap ex” is the essential ingredient for long-term productivity growth. If you’d care to see a short essay Danielle wrote on this topic two days ago, please click on this link.

As with so many serious long-term problems, the US stock market continues to be in a “no worries, mate” mode, fixated on admittedly strong but heavily tax-cut driven earnings. There’s absolutely no telling at what point that carefree mindset will undergo a sudden attitude adjustment. When it does change, however, investors will re-learn the painful truth that stocks go up on an escalator and down on an elevator—even though that elevator has been out of order for a very long time.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

______________________________________________________________________________________________________________

The Twisted Tie That Binds: The Globality of the Pension Crisis Entraps Central Bankers By Danielle DiMartino Booth

To say I’ve written extensively on the pension crisis here in the United States is an understatement. But what of retirees elsewhere who’ve also been affected by the very same monetary policy that’s spread like a contagion to the rest of the developed world?

A recent Tweet brought this question to mind even as I was still ruminating on my recent visit to Brussels. It was in response to a piece I’d published holding out hope that the Federal Reserve under Jay Powell would mark the first break in over three decades from the broken orthodoxy.

Consider these words from a young Englishman: “You mentioned Jerome Powell was the only hope, but who should I and other Millennials like myself in the U.K. blame for the extortionately overpriced properties which our generation cannot afford or the pensioners on my road who are struggling to survive?” My reaction was akin to being hit with a brick.

The just-released consumer price index tells us all we need know about rental inflation in the United States; At 3.6%, it’s near the cycle highs and outpaces wage and salary growth despite incomes hitting cycle highs. The most recent Employment Cost Index came in at 2.9%, the highest since mid-2008. Rental inflation applies to both demographics the Tweet mentions – the young and the old – as one cohort is just starting out and the other has begun to downsize.

Finding apples-to-apples comparisons is unrealistic because American, British and European housing and retirement systems differ so much. The data that do offer valid comparisons speak to what we shell out to put a roof over our heads. Europeans spend about a quarter of their incomes on housing while the average American household spends a third on housing.

While the advantage seems plain in numbers, bear in mind Europe has more extremely expensive cities vis-à-vis the U.S., especially if you include London in the mix. Commuters across the pond could give those of our most expensive cities a run for their money.

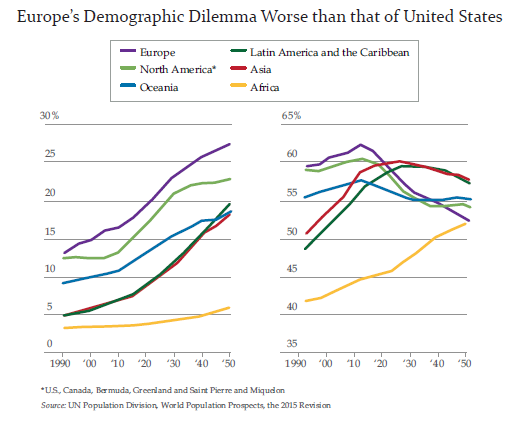

Comparing retirement systems is much more complicated. The best starting place is demographics at the highest level, which brings us to a Wall Street Journal article that came out two years back.

The United States has a demographics problem on its hands. That’s a known, known and has been for some time. As you can see, Europe is in much worse shape. In the coming decades, it will have more retirees (left-hand chart) and fewer workers entering the workforce (right-hand chart).

Curiously, if you look within Europe, this is not a productive north vs. profligate south story. It really does come down to two factors – one that can be easily defined and another that must be presupposed to a certain extent.

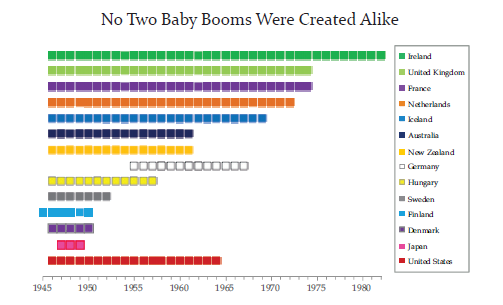

Americans can be guilty as charged in assuming that all Baby Boomers were created at the same time – 1946-1964. Vastly different levels of prosperity coming out of World War II, though, dictated the extent to which setting up millions of houses and homes to fill was feasible. As you can see, Germany’s birth surge was abbreviated and late out of the gate, which stands to reason. Japan’s was even shorter and ended just as abruptly. The Irish clearly had no need to get out more.

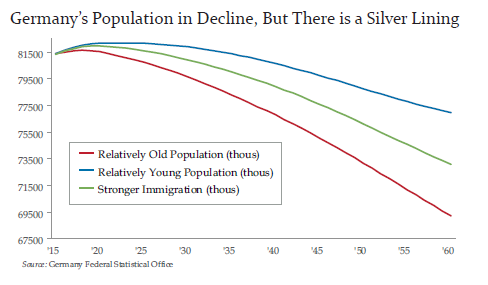

In fact, it is Germany that has some of the steepest demographic challenges ahead. At the root is a falling birth rate. Even with stronger immigration, the population of Germany looks to be in a long-term decline; its older population will dwindle while its young and immigrants struggle to replenish itself based on current projections. As has been the case across much of Europe, birthrates have fallen by 40% since the 1960s to 1.5 children per woman. In Germany, that rate is lower yet, at 1.4 children per woman.

The implications for the manufacturing juggernaut are a subject in and of themselves. As things stand, 1/8th of the German workforce is tied to the automobile industry. To maintain a dominant position on the world stage requires a robust workforce.

The flip side is German pension schemes will be appreciably less stressed compared to many of their Euro-neighbors. Call this the silver lining to the Baby Boom “Light” the country experienced. In stark contrast to Europe as a whole, fewer retirees to finance per worker will benefit the country’s fiscal position in the years to come*. Yes, that is an asterisk. Read on.

The just-released European Commission 2018 Pension Adequacy Report found 17.3 million, or 18.2 percent of those aged 65 and older in the EU, to be at risk of poverty or social exclusion, even though their ranks have dwindled by 1.9 million since 2008. Living too long appears to be part of the “problem.” The word ‘retiree’ should be replaced in the EU given the time they spend in retirement (51% of their lives) vs. the portion of their life they spend in the workforce (the 49% balance).

Inequality is an equally nasty scourge. In the three years through 2016, income inequality rose in 16 EU countries while it fell in nine. As the report warns, “older people at risk of poverty are now poorer.” The plight will be even worse for women: the EU gender gap in pensions is 37.2%.

*Of course, this math encompasses the whole of the EU as it stands today, including Great Britain. The U.K. is brewing a pension crisis that could rival that of the United States in scope. According to Mercer, the U.K. is perched atop an $8 trillion retirement funding gap when you tally all sources. This will balloon to $33 trillion in the next three decades.

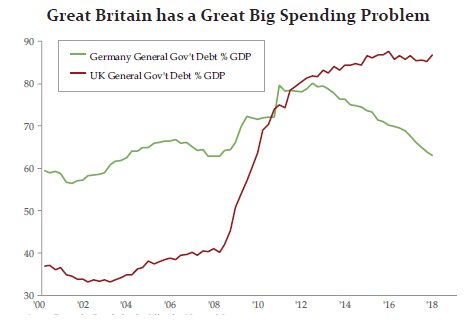

If that seems far off enough to dismiss, go back to the Baby Boom chart above. The Irish may have won the prize in the postwar baby-making department. But the U.K. (AND France) both placed a distant second. They will not have a dwindling older population that fiscally flatters their future pension obligations. And the U.K., like its across-the-Atlantic former colony, has a spending habit that hasn’t kept up with its revenues. As has been the case in the U.S., government debt as a percentage of GDP has spiraled upwards in recent years in contrast to that of Germany. To state the obvious, fiscal strains and pension underfunding are not good bedfellows.

Looking at that chart and the challenges already facing the eurozone on so many other levels, would a Brexit be such a bad thing for Germany’s fiscal health (Deutsche Bank and/or Italy come to mind)? More to the point, assuming the glue that holds the EU together withstands the test of time, Germany has more than enough on its hands dealing with the pension fallout that promises to debilitate the rest of the EU, excluding the U.K.

At the risk of painting Germany as benevolent, for all its hawkish bluster, the country has nevertheless sat back and borne witness to an easing campaign at its central bank sufficient to make Janet Yellen blush. The zero-bound was not low enough for the European Central Bank. The EU was sentenced to death by negative interest rates in addition to the bond-buying bonanza that blew up the ECB’s (European Central Bank) balance sheet. So now what?

The fact is over-easing will break something in the economy when the markets force a reversal in the United States and the EU. Pensions are a leading candidate to be that ‘something.’

ECB President Mario Draghi begged to differ with that eventuality in a speech in the Netherlands last May. In his view, pensions will benefit in the aftermath of the negative interest era. “We need to offset short-term negative effects against the positive effects for the long term,” said Draghi. On a separate occasion, Draghi went so far as to say that abandoning ultra-loose policy would do pensions a “disservice.”

Draghi’s words likely grated on the ears of the Dutch who define ‘short term’ in realistic terms. The ECB’s discount rate has not been above 1% since 2009. Demographics also plays an outsized role; their postwar baby boom was the fourth-most protracted. A study conducted last year estimated that the damage low rates have inflicted on the Dutch pension system was at least €60 billion and that accounted for the stock rally QE (Quantitative Easing) policy has driven.

In the event you’re rusty on your pensions math, the lower interest rates are, the more pensions must set aside to meet their obligations. By their very design, they are obligated to match future liabilities by investing in instruments that have a similar duration. Way back when that worked. Buy the requisite amount of 30-year bonds to match what you’ll be paying out in 30 years’ time. But interest rates have been falling for well over three decades.

Absent the means to pony up more money, pensions must get creative to ensure they have adequate future funds set aside. Picture a see-saw. The lower interest rates fall, the more pension fund managers allocate to assets that promise higher returns. These days, that seesaw is tilted at a dangerous angle. Bond allocations have been whittled down while pension funds have loaded up with higher-risk investments that threaten their solvency.

Despite the reach for yield and risk, liabilities have continued to grow at a faster pace than assets, leading to deeper and deeper levels of pension underfunding.

Wouldn’t the simplest solution be to raise interest rates, so pensions could get out of the business of blowing themselves up? Afraid that this thorny juncture is where the gravest sins of central bankers are exposed.

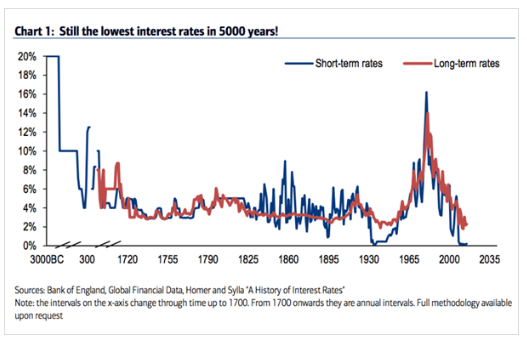

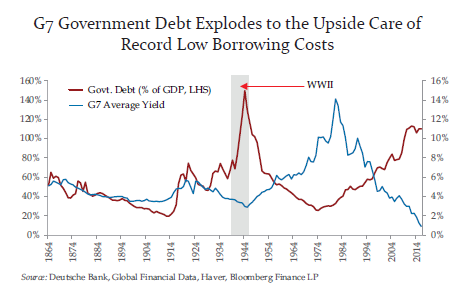

Governments worldwide have gorged themselves on debt which has done a splendid job of ensuring entire countries’ economies don’t blow themselves up. But it is solely by virtue of central bankers’ blessing that this approach has been feasible. Think of it as the mirror image of the effect low interest rates have had on pensions. The lower rates are, the more governments can live the lie that debt-driven prosperity comes at a negligible cost.

This chart does an excellent job of illustrating the quid pro quo relationship between unelected central bankers and the feckless politicians they keep in business. The upshot is central bankers are in a prison of their own making. Debt is now so high they can’t dare normalize interest rates.

Any aggression in the way of tightening will also shatter the other illusion central bankers have carefully crafted -- the stock market. For worse measure, it’s increasingly apparent that the Fed has the dangerous capacity to bring down the Emerging Markets complex.

Lest you think the U.S. had slipped my mind, Mercer took the same pencil to the same paper when it determined that the UK’s underfunding would balloon to a neat $33 trillion in 30 years (that’s 11 times UK GDP for any of you keeping score). According to Mercer, when you add up all the forms of retirement schemes in America, you arrive at $28 trillion. That lovely figure is set to jump to $137 trillion in 30 years (FYI, seven times GDP).

The beast in the math is social security which a recent government report found would be insolvent by 2034. The kindest thing to say about that bit of news is that social security is better off than Medicare which should run dry in eight years.

At least social security won’t melt any faster when the stock market corrects. But that doesn’t mean the country’s finances won’t be imperiled by insolvent public pensions. Whoever will be capable of bailing out, say, the state of Illinois, which by law cannot declare bankruptcy nor print its own currency to inflate its debts away. That’s Constitutional Law 101.

I must inject another recent Tweet here that offered up a solution to such an inevitability. How obtuse was I that I didn’t understand that the federal government need not bail out any state if the Fed QE’d the entire municipal bond market? Now why didn’t I think of that?

At least such a “solution” is conceivable in the U.S. Can you imagine how incensed Germans would be if called upon, as in their wallets as taxpayers, to bail out France’s pension system? Just an example, but you get the gist of the societal implications, to say nothing of the sanctity of the euro as a single currency.

As if we needed a twist to this sad tale, it’s increasingly likely that the kindling that sets pensions worldwide afire will come from the ECB. Draghi detests the idea of backing down on QE but the Germans seem determined to force him kicking and screaming down that path. Draghi will therefore do everything he can to slow the process by which the ECB exits its QE and negative interest rate regime. And therein lies the risk as inflation has arrived on Europe’s shores.

An overheated economy would prompt the hawkish Germans to rush to end the tapering of the ECB’s QE and hike rates into positive territory. There’s nothing overvalued risky asset prices hate more than abrupt moves. Any sudden moves to tighten would send a rate shockwave throughout the financial markets. Rates would be forced to reprice sharply and both equity and credit markets would correct in foul fashion.

Note to Draghi: Slow as she goes could backfire severely.

Of course, if markets misbehave, QE comes right back onto the table. At least that’s the working theory given the alternative. But that won’t save pensions given where we started – demographics. Baby Boomers are no longer an actuarial assumption to be fudged with corrupt accounting. They are a cash-flow reality. The next body blow pensions worldwide sustain will knock them down to the mat. In many cases, they won’t be able to stand by the count of ten.

What we’re dealing with here is a classic damned if you do, damned if you don’t scenario. Falling interest rates have forced liabilities and underfunding to record levels. Rising interest rates will annihilate the risky assets pensions have piled into playing defense against those falling interest rates. Either way, pensions are condemned. Crooked central banking policy has guaranteed the outcome.

As much as we’d prefer to look the other way, pensions still account for more than half of the retirement funds in the developed world. The world’s central bankers would prefer the pension crisis remained in the background, shrouded under the perception that stocks will never correct. But wishing tangible things away never works.

We’ve veered so far down the rabbit hole, the underfunding disaster cannot be rectified, the sums are simply too big. The societal implications cannot be dismissed. The guilty parties – avaricious unions, dishonest politicians and warped central bankers -- will be pursued. To the afflicted, pensioners and taxpayers, sorry will become a four-letter word.

First there was Alan Greenspan, The Maestro himself. Then Ben Bernanke had The Courage to Act. At least that’s how he saw fit to title his memoir. And finally, we have Super Mario who vowed to do, “whatever it takes.” Blest be the tie that binds the damned.

______________________________________________________________________________________________________________

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

** Due to recent weakness, certain BB issues look attractive.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.