“40 to 70% of the human population could potentially be infected by the virus if it becomes a pandemic. Not all of these people would get sick.”

– Marc Lipsitch, Epidemiologist, Harvard University, February 21st

“We should assume that this virus is very soon going to be spreading in communities here, if it isn’t already, and despite aggressive actions, we should be putting more efforts to mitigate impacts.”

– Jennifer Nuzzo, Epidemiologist, Johns Hopkins, Center for Health Security, February 21st

“Now we also face an immediate crisis. In the past week, Covid-19 has started behaving a lot like the once-in-a-century pathogen we’ve been worried about. I hope it’s not that bad, but we should assume it will be until we know otherwise.”

– Bill Gates on Friday

“The most useful model is the 1918 pandemic flu…with the cancelation of athletic events, theaters, and school closures. The more containment one imposes, one does reduce the amount of cases but spreads the number of cases over a much longer time.”

– Dr. Barry R. Bloom

The Virus Heard ‘Round the World

Let me begin this most unusual Guest EVA edition with both an observation and an admission. On the first part, the sudden market panic this week is precisely why Evergreen has been raising cash as we had noted the alarming news out of China and now other countries. It has been one of the reasons we have our clients so defensively positioned (along with extreme concerns about the highly inflated valuations of many currently popular stocks and sectors). To have a high cash position, as Evergreen does for all of its clients, is essential in a sudden panic like this. We have the luxury of buying when others are engaged in fear-stricken selling and we are doing so, albeit gradually.

Now the admission: It took me a while to appreciate how bad this was going to be. Of course, the “this” is the coronavirus, officially referred to as COVID -19. However, I prefer the simpler “CV” which I will use throughout the rest of this quasi-introduction. (It did hit me this morning that there are similarities with the housing implosion which I did anticipate but I also greatly underestimated the severity.)

The reason I refer to this as an “unusual” and “quasi” Guest EVA is that I personally have a fair amount I’d like to convey on the CV, perhaps making up for lost time. This is as opposed to the shorter introductions I usually create for our monthly Guest EVAs. Somewhat in my defense, our February 7th EVA, “The Long and Short of the Wuhan Flu”, did alert EVA readers that this was a dangerous development. We also provided numerous CV-related warnings in our February 14th Likes/Neutrals/Dislikes section.

A second come-clean concession is that I don’t have a ton of confidence in much of what I’m going to relay in my section. There is simply so much we don’t know about the CV. Yet, the suspicions that I will convey and, especially, the intel I’ve received from many people far more informed on this topic than me, have turned out to be far more accurate than the soothing coverage from popular media sources. As you may have noticed, until this week, media attention was woefully underestimating this rapidly evolving mega-crisis.

To that point, as late as last Friday, February 21st, there was not a single CV-related story on the front page of The NY Times (though there was a small window at the bottom, referencing an article on page A7). Similarly, last weekend’s Barron’s iconic “Up and Down Wall Street” column, long written by the late and very great Alan Abelson, was titled “It’s a Bull Market No Matter Where You Look”. The only article I could find related to the CV in that Barron’s issue was a short article that shared half of page 12. The lead sentence was, “Most economists and strategists assume that the coronavirus will be contained in coming weeks and that China will roll out a plan to cushion the blow.” (It did allow, though, that the fallout could be worse, possibly lopping off $1 trillion of the planet’s GDP.)

Calming words such as the Barron’s excerpt above have been the dominant mindset right up until last Monday. Remarkably the S&P 500 was actually up 3% on the year as of last Friday. Despite my belated epiphany to the severity of the risks, around the first week of February I began to have serious doubts this sanguine view was right, a concern I shared with Evergreen clients in numerous conversations. Undoubtedly, many were thinking “there he goes again, doing what he does best—worrying much about nothing”.

In the second part of this Guest EVA, I will share some of the emails and articles I read in recent weeks that began to change my mind. They are still relevant in my view because most of Wall Street believes (though with waning confidence) that this is a very short-term disruption. Again, I’m having deep reservations about that despite conceding there will be a time in the not-too-distant future when a vigorous rally likely occurs. However, my usual non-consensus view is that it will be a selling opportunity-- at least until we get closer to summer when a much more durable and powerful up-move is probable as flu season winds down. The most badly damaged virus victims, like energy and airlines, are likely to be the biggest winners at that point.

Last weekend, when I was astounded about the pervasive complacency, and when I was composing the outline for this EVA, I wrote: “We are about to find out what happens when one of the most speculatively out-of-control stock markets of all-time collides with the growing likelihood of a global pandemic.” Well, this week we found out and, for me, who vividly recalls the Crash of 1987, it has definitely brought back those painful memories. In fact, this has been the most rapid 15% drop from a market peak in the history of the stock market.

This shocking market air-pocket also recalls what happened after September, 11th, 2011. One reason that was such a brutal market environment was because stocks had become so inflated by the spring of 2000, at the end of the infamous tech bubble.

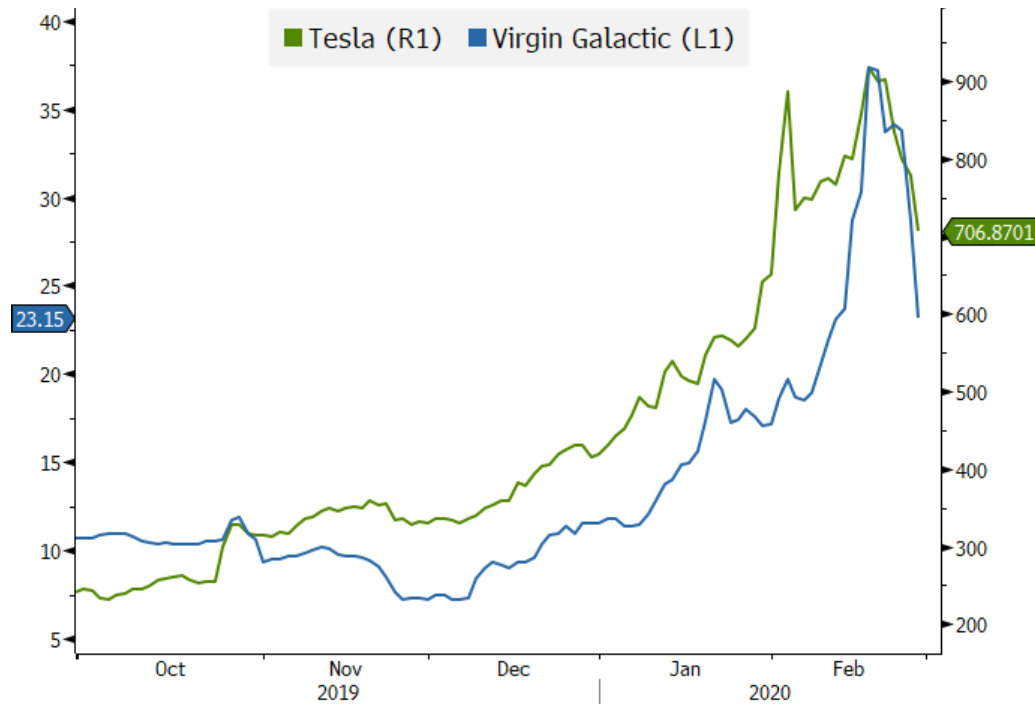

As was the case twenty years ago, over the last two years a plethora of US stocks were not caught up in this growth-at-any-price mindset. Many past EVAs have noted that it has long been a two-tier market, split between what I call the COPS (the Crazy Over-Priced Stocks) and the mostly out-of-favor rest of the market. (The same thing happened from 1998 to 2000, when a myriad of “old economy” stocks were pummeled even as the tech-heavy NASDAQ did a moon-shot.) In recent months, the COPS entered that straight-up phase that is the classic sign of a big bubble about to go pop. Tesla and Virgin Galactic are graphic cases in points (literally, as you can see from their graphs below). The latter hit 1000 times 2020 estimated sales and there is no P/E because, as with so many COPs, there is no E, as in earnings. (On Friday morning, as I edit this copy, Virgin Galactic has come crashing down to terra firma.)

Source: Bloomberg, Evergreen Gavekal

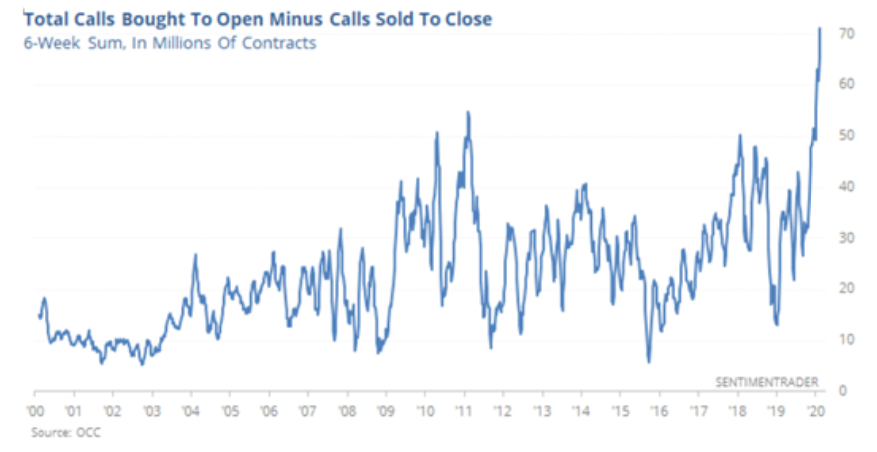

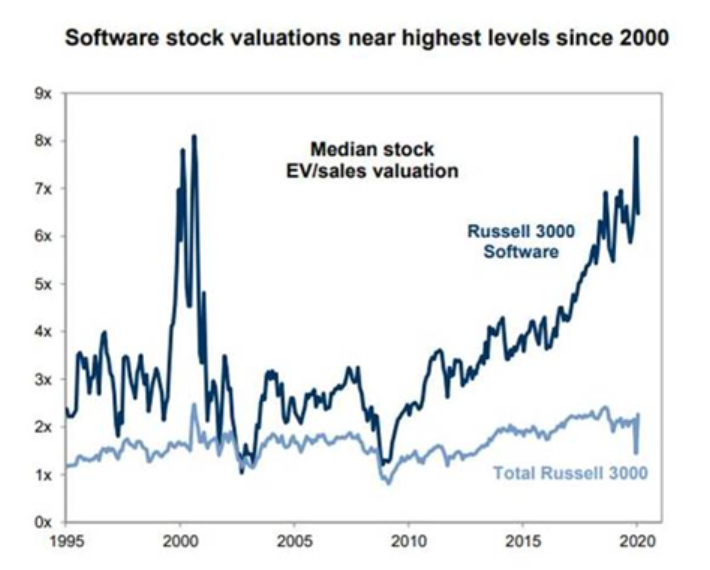

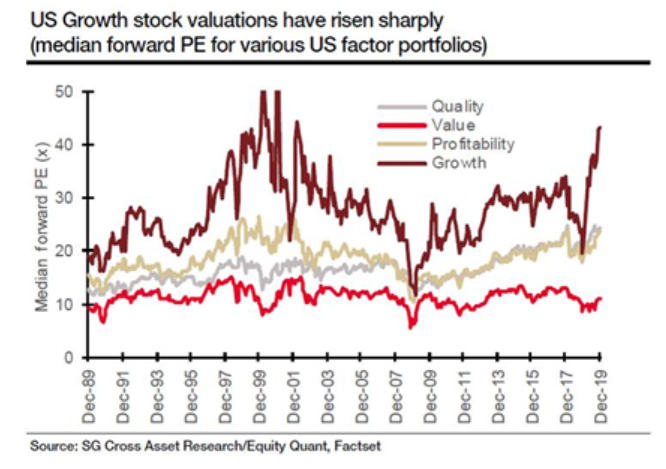

Yet, it was much more than those two COPS that were flashing a very bright shade of red lately. The ratio of calls bought vs calls sold, discount brokerage trading volumes, the Russell 3000 software stocks, and the P/E ratios of Growth vs Value stocks were all shrieking the same warning signal.

Additionally, other important markets, like bonds and gold, were telling a very different story, one that indicated mounting and intense fears. Many in the never-say-sell crowd hoped those were wrong while the S&P—and especially the vertiginous NASDAQ—were right. This week revealed it was very much the other way around.

The consensus view, even now, is that the CV is highly communicable but not very lethal, with mostly the elderly and frail at risk. In this week’s Guest EVA, that relaxed attitude is being questioned. The fact that the original 34-year old doctor, who first alerted the world to the CV, died after having briefly recovered from it, should raise some serious eyebrows. Then, last week, the death of 51-year old Liu Zhiming, one of the most senior healthcare officials in Wuhan, where the outbreak started, should also set off some smoke detectors. Supposedly, he expired despite frantic efforts to save his life. On Thursday, February 22, another physician, this one only 29, also succumbed. For a disease that is alleged to have a 2% fatality rate, or even lower, these are curious occurrences. (Two factoids that might get your attention is that China is the world’s largest producer of pharmaceutical active ingredients and that 97% of US anti-biotics are sourced there.)

As we should all know by now, it’s no longer fundamentally-oriented and research-driven money managers like Evergreen that move markets these days. Rather, 80% to 90% of trading is generated by computers and their infamous algorithms (algos, in the vernacular of the Street). It’s safe to say these auto-pilot programs have no way of incorporating a true Black Swan (this is, once more, Street-speak for an out-of-the-blue event with no precedent). Which is likely why they kept pumping out the buy orders even as evidence accumulated that the world was now facing what could be the medical equivalent of the Global Financial Crisis.

As you will read, one of the reasons I believe this virus is so pernicious is that more information is coming out indicating the CV was bioengineered. In other words, it’s a man-made virus. Many have rightly pointed out that Wuhan is where the Chinese military’s biological warfare lab is based. There is much more in the actual guest authors section on this thesis, so I won’t go into additional detail.

This is a good time to interject that my esteemed partner, Louis Gave, takes a much less dour view of the situation. In a call we did with our team this week, he dissented with my opinion that the CV already appears to be a global pandemic. He could certainly be right, and we should all hope and pray he is. Hedge fund rock star Ray Dalio has also opined that the market impact has been exaggerated and that the scare will be short-lived (though, curiously, he said that before the stock market had its crashette this week).

But let me conclude my section with a follow-on to the Bye-Bye Buyback EVA from two weeks ago. In it, I made as persuasive case as I could that the biggest helium pump in this great stock market bubble was buybacks, i.e companies repurchasing their own shares. My conclusion was that the longest bull run ever would be at-risk once Corporate America was compelled to hunker down and curtail these monstrous and seemingly never-ending buybacks. That compulsion may just have occurred.

Guest EVA section, with commentary from multiple sources.

The below are excerpts from a Financial Times article by Megan Greene, one of the few published last weekend that presciently anticipated what was to happen this week:

I recently asked some investment managers how they might immunize their portfolios against fallout from China’s coronavirus: “I wouldn’t” one scoffed, “the virus is temporary.”

Investors have been conditioned to believe that disturbances such as mad cow disease, SARS, and now the coronavirus are temporary blips.

Signs of complacency about the CV abound. According to BofA’s February global survey of fund managers, cash comprises only 4% of portfolios, the lowest since March, 2013. When investors are worried, they tend to hold more cash. Instead, they’ve been putting their money into global equities, which keep hitting record highs.

Investors appear to view the CV like a minor traffic jam: disruptive but, in economic and financial terms, something you get past quickly. They are making two assumptions. First, the CV will be contained shortly, pent-up demand will be released, and its impact is therefore transitory. Second, if the epidemic isn’t contained quickly, policymakers will step in to fix the mess with actions that send asset prices soaring. Either way, buy the dip.

But what if the CV fallout is more like sitting in traffic hours after an accident scene is cleared? Demand may recover quickly, but the supply side is much more problematic. Chinese firms are integrated into complex, global supply chains and the enthusiasm for “just in time” manufacturing, which involves thin inventories, leaves little buffer for disruptions.

Finally, there is a problem with relying on policymakers to clean up the mess. Their tools are designed to stimulate demand, not fix supply interruptions. “I’ve only been at the Fed for two years.” Richmond Fed Bank president Tom Barkin told me. “But to my mind, central banks can’t come up with vaccines.”

Most investors assume the CV will be contained by late March and that, as winter ends, so will the epidemic. But we cannot be sure the outbreak has a natural peak. If the virus becomes a full-blown global pandemic, growth and markets will be hit much harder than investors are assuming.”

Investors may be right that this will be temporary…But temporary can last a long time and get much worse before it gets better.

The following is an email exchange from early last week (i.e, before most of the world woke up to the seriousness of the threat) between two very bright friends who have provided me with some of the best intel I’ve received on the CV in recent weeks:

From Heinz B:

After reading a recent research paper discussed by Martenson in one of his videos, I am beginning to think the real horror is yet to come. In the first round of infections around 80% of cases tend to be mild and 20% tend to be severe, which is already a very bad ratio and a hint that the eventual death rate will be quite large. But the real problem rears its head when someone who recovered is infected a second time. Apparently once the body acquires the information it needs to manufacture antibodies against COVID-19, it goes haywire when it encounters the virus a second time, i.e. the antibody response becomes so extremely aggressive that re-infected patients are killed by their immune system response rather than the virus.

(Dave’s note: This is similar to what occurred with the Spanish flu after WWI.)

This problem was already described in 2003 when they were testing SARS vaccines on rats and mice (SARS is also a coronavirus). Indications are that COVID is similar in this respect, which obviously represents quite a big problem with respect to prospective vaccines.

The most recent surge in new cases in S. Korea and Japan indicates that the genie has now finally escaped the bottle. It looks ever more likely that the feared global pandemic is beginning to take hold. I personally think it can no longer be stopped, but that is just a hunch, I have no proof one way or the other. I believe this because over the past week or so several infection vectors have been discovered that cannot be traced back to visits to Hubei or any other contact with Chinese citizens - so it is already certain that there are outbreaks independent of what is happening in China.

Lastly, I would point out that containment in China may be temporary. Drastic measures have produced a certain degree of containment, but these measures will now be relaxed to permit resumption of economic activity. In the meantime, it has turned out that hundreds of people in Chinese prisons are infected as well. This is a new vector since visitors are presumably carriers now.

(Dave’s note: his point about the relapse situation sounds eerily like what happened to the 34-year old doctor in Wuhan who initially raised alarms about the CV. He reportedly recovered after his first bout with the virus but then, when it came back, he lived just two more days.)

From Tom R:

I agree with you Heinz. This is a long-tailed event, unfortunately. The CDC just issued a warning to avoid places with large crowds of people HERE IN THE US....so definitely the authorities know the genie is out of the bottle. The more I read about this virus the more convinced I become it is manufactured. But that is a discussion for another day.

(Dave’s note: Amazon has apparently just instructed all of its employees to avoid air travel.)

The fact the virus sends the immune system of a person who is infected a second time into overdrive is reminiscent of the Spanish Flu - it killed people in their prime, i.e. 18-40, and spared the very young and old, because they had weaker immune systems. Mortality rates were 20% back then and I wouldn't be surprised if it is something similar (or probably higher) for people who are re-infected, especially given the preferred demographic of the virus.

(Dave’s note: estimates are that 500 million were infected by the 1918 Spanish flu with deaths in the 40 to 100 million range; thus, the fatality rate of those infected likely was between 8% to 20%.)

China has no choice but to relax containment measures for obvious reasons. Pretty well every company has no visibility as to the effects even a month out on their operations - that is the picture I get from listening to and reading summaries of earnings conference calls. No one is able to quantify anything at this point which is a bad thing as it could lead to a sudden, negative surprise, especially in tech with regard to the (supply) chain.

Let's not forget that the survival of the regime in China depends on economic growth as the only legitimacy of the government lies in providing the populace opportunities for that. And Xi looked bad even before this virus outbreak, as his heavy regulatory hand has reduced economic opportunity, especially in tech. Should the virus resurge into March, we will be looking at a crash in markets, in my opinion.

(Dave’s note: Tom was prescient but the crash, or, as I call it, a crashette, has obviously already occurred as markets price in a probable global pandemic that continues into the spring.)

CDC alert on February 25th

“We expect we will see community spread in this country,” Nancy Messonnier, director of the CDC’s National Center for Immunization and Respiratory Diseases, said on a call with reporters Tuesday. “It is not a matter of if, but a question of when, this will exactly happen.”

The outbreak is “rapidly evolving and expanding,” she said.

National Economic Council Director Larry Kudlow later characterized the CDC’s warning as an emergency plan and said, “it doesn’t mean it’s going to go into effect.”

“We have contained this,” he said, describing the U.S. government’s prevention of the virus’s spread as “pretty close to air-tight.”

“I don’t think there’s going to be an economic tragedy at all,” he said. He dismissed concerns about supplies of pharmaceuticals and medical supplies such as face masks and said a vaccine for the coronavirus will be developed much faster than people realize.

“This is very tightly contained in the U.S.,” he said. “Elsewhere it’s a human disaster.”

(Dave’s note: Mr. Kudlow’s containment comments are uncomfortably reminiscent of what former Fed Chairman Ben Bernanke said about sub-prime mortgages in the summer of 2007.)

The wrath of Ben Hunt

Ben Hunt is a familiar name to EVA readers. His Epsilon Theory newsletter has become extremely popular among professional investors (yes, there are a few of those left, who still endeavor to think as opposed to just mimic overly popular stock indexes). Below are some searing excerpts from his two recent essays on the CV, the first titled “Body Count” and the second titled “The Fall of Wuhan”.

(Dave’s note: His opening paragraph is a bit “mathy” but his point is that the official Chinese statistics almost precisely—and improbably – fit the slope of a quadratic versus an exponential function; as you can see in the chart below from Ben’s “Body Count” letter, the latter begins to look like a hockey stick…or the graph of Tesla’s stock price in January!)

From Ben’s “Body Count” (To read the full issue click here):

The really damning part of modeling of the reported data with a quadratic formula is that this should be impossible. This is not how epidemics work.

All epidemics take the form of an exponential function, not a quadratic function.

All epidemics – before they are brought under control – take the form of a green line, an exponential function of some sort. It is impossible for them to take the form of a blue line, a quadratic formula of some sort. This is what the R-0 metric of basic reproduction rate means, and if – as the WHO* has been telling us from the outset – the nCov2019 R-0 is >2, then the propagation rate must be described by a pretty steep exponential curve. As the kids would say, it’s just math.

Now I don’t want to get into the weeds as to whether it’s possible to model this special data set with an exponential function (it probably is), and we’ll never have access to the detail of data we’d need to be certain about all this. And to be clear, at some point the original exponential spread of a disease becomes “sub-exponential” as containment and treatment measures kick in.

But I’ll say this … it’s pretty suspicious that a quadratic expression fits the reported data so very, very closely. In fact, I simply can’t imagine any real-world exponentially-propagating virus combined with real-world containment and treatment regimes that would fit a simple quadratic expression so beautifully.

I believe that the Chinese government is massively under-reporting infection data in the pandemic regions of Hubei and Zhejiang provinces. (Dave’s emphasis)

Just like the American government massively over-reported North Vietnamese casualty data in the Vietnam War.

It’s not only that I believe the numbers coming out of China are largely made up. More importantly, I also believe that Chinese epidemic-fighting policy – just like American War-fighting policy in the Vietnam War – is now being driven by the narrative requirement to find and count the “right number” of coronavirus casualties. nCov2019 is China’s Vietnam War.

*The World Health Organization

From Ben’s “Fall of Wuhan”(Click here for the complete letter):

What we’re seeing in South Korea, Iran and Italy is what exponential disease propagation looks like in the real world. Real world data is spiky. Real world data is messy. Real world exponential growth looks like nothing, nothing, nothing … then cluster, cluster, cluster … then BOOM! My rule of thumb: when a country reports a death from a local COVID-19 infection, then the disease is already endemic in that country. Implementing extreme quarantine measures after that first death – either within that country or by other governments to isolate that country – is closing the barn door after the horse is out … it’s too late. Doesn’t mean you shouldn’t do it for disease minimization or social distancing. But it does mean that a goal of containment is unrealistic.

What we’re seeing today in South Korea, Iran and Italy is the BOOM. Other countries will follow. The United States will follow.

And so now we must fight.

As individuals that means social distancing. As individuals that means doing what we can to stay healthy and prepare for a storm. As a nation that means a war-footing to build dedicated treatment wards before they’re required, to protect healthcare professionals before they get sick, to update our testing and diagnostic capabilities before they are swamped … to do everything possible to bolster our healthcare systems BEFORE the need overwhelms the capacity.

Above all, that means calling out our leaders for their corrupt political responses to date, and forcing them through our outcry to adopt an effective virus-fighting policy for OUR benefit, not theirs.

Because a city does not fall just because it is hit hard by a plague. A city falls when its healthcare system is overwhelmed. A city falls when its national government fails to prepare and support its doctors and nurses. A city falls when its government is more concerned with maintaining some bullshit narrative of “Yay, Calm and Competent Control!” than in doing what is politically embarrassing but socially necessary.

That’s EXACTLY what happened in Wuhan. More than 30% of doctors and nurses in Wuhan themselves fell victim to COVID-19, so that the healthcare system stopped being a source of healing but became a source of infection. At which point the Chinese government effectively abandoned the city, shut it off from the rest of the country, placed more than 9 million people under house arrest, and allowed the disease to essentially burn itself out.

And so, Wuhan fell.

The disaster that befell the citizens of Wuhan and so many other cities throughout China is not primarily a virus. The disaster is having a political regime that cares more about maintaining a self-serving narrative of control than it cares about saving the lives of its citizens.

We must prevent that from happening here. From happening anywhere. Yes, containment has failed. But that does NOT mean the war is lost. We can absolutely do better – SO MUCH BETTER – for our citizens than China did for theirs.

And so we must call out the Director-General of the World Health Organization for his corrupt political response to COVID-19, where by continuing to toe the (literal) party line, he sacrifices WHO’s authority and credibility on the altar of China “access”.

Conclusion

As I wrote at the beginning of this EVA, maybe I’m trying to make up for initially underestimating threats posed by the CV, even though I was more worried than almost everyone with whom I communicated on the subject. Consequently, I’ve tried to present a very non-mainstream and, frankly, extremely concerning overview of the situation. But before you accuse me of being a reckless alarmist, you might go to Amazon.com and try to order things like sanitary wipes, survival kits, surgical masks and hand-sanitizers. If you want any, it’s going to be a very long wait.

I’ll end this EVA by saying what we all know (though we may forget in the throes of a panic): this too shall pass. It might be as uncomfortable as passing a kidney stone, but humanity will recover from this threat and so will the financial markets. As noted earlier, late spring and early summer should bring significant relief and a rousing rally.

In the meantime, the outbreak may well trigger an actual bear market, something that hasn’t hit US stocks in over a decade. We have been way overdue and the CV, along with rising political uncertainty combined with what could be a precipitous decline in buybacks, all have the potential to end the postponement.

Evergreen has already begun to slowly purchase shares in companies that we believe will survive the CV threat and eventually thrive. We are funding these purchases with proceeds from the many sales we did earlier this year as our concerns about the CV escalated.

However, to reiterate a point from earlier in this missive, many investors are far out over their skis with those aforementioned Crazy Over-Priced Stocks. They have made huge gains in these issues, many with glamorous stories but little, if any, in the way of earnings. The valuations of these, including some stodgy issues that have become darling stocks for some reason (including the maker of a mundane household product that was recently trading at 45 times earnings) are simply absurd. That part of the market is where truly shocking losses are likely to be realized. And unlike some of the blue-chip names that are presently being punished because of exposure to the global economy and its supply chain, most of those might never come back up to where they were trading last week.

There’s temporary risk that hurts near-term market values but ultimately fades. Then there’s lasting risk that leads to permanent loss of capital. Just ask all those folks who were as crazy about dot.com stocks 20 years ago as they have been about the COPS lately.

But for quality companies with a history of strong profitability, we could soon be looking at the best buying opportunity since 2009—at least for those who have the substantial cash reserves to pounce on the bargains. For the fully-invested, momentum-chasing investor—of which there seems to be millions these days—they will be doing well simply to hang on and hope the medical experts quoted at the top of this letter are greatly exaggerating the threat. My money is on the pros—both in medicine and the markets.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.