“The pharmaceutical industry is the biggest bunch of crooks in this country.” Senator Bernie Sanders

“All crises have involved debt that, in one fashion or another, has become dangerously out of scale in relation to the underlying means of payment.” John Kenneth Galbraith

“It is hard to imagine a more stupid or dangerous way of making decisions than by putting those decisions in the hands of people who pay no price for being wrong.” Thomas Sowel

The 1951 film, “The Day the Earth Stood Still”, helped usher in Hollywood’s Sci-Fi era. It starred Patricia Neal (“The Fountain Head”, “Hud”) and Michael Rennie (“The Robe”, “Les Miserables”) and was directed by Robert Wise (“West Side Story”, “The Sound of Music”). In other words, it was no “B” movie project. If you haven’t seen it, I’d highly recommend doing so (though I haven’t watched the 2008 remake starring Keanu Reeves, it received good reviews).

It’s no exaggeration to say that for most of the human race, 2020 seemed like a Sci-Fi movie, but without the fiction. And it certainly felt like day-to-day life came to a standstill. In this case, it wasn’t a suave alien (Rennie) who was accompanied by a lethal robot—which threatened to obliterate humanity if we couldn’t amend our war-like ways—but rather a pandemic of still controversial origin that brought life as we know it to a standstill.

Undoubtedly, 2020 was the planet’s most traumatic year since WWII ended. As with a war, at least for the losers, there was extreme economic carnage and the loss of countless lives. Yet, as was also true during WWII, the immense challenge brought forth remarkable innovation and adaptation. Technology came to the rescue in allowing most businesses to continue functioning. Additionally, thanks to the extraordinary R&D efforts of the oft-maligned US pharmaceutical industry, a vaccine was produced within months versus the years that many pundits initially felt probable. Critically, e-commerce and shipping companies such as Amazon, FedEx and UPS continued to literally deliver the goods.

However, for someone like me, who is a WWII history buff, the contrast with how rapidly and effectively the US government responded to the attack on Pearl Harbor and how ineptly it has reacted to Covid is both shocking and depressing. By the fall of 1942, America had already achieved resounding victories over the Japanese at Midway and Guadalcanal and launched a successful amphibious invasion of North Africa less than a year after the sneak attack on Pearl. (The final mop-up on Guadalcanal took until February 1943.)

Despite the government’s Covid response debacle (such as the inability to provide all teachers with N95 masks by the time school re-opened late last summer), the private sector showed its resourcefulness, as did millions of ordinary American citizens. The multitude of heroes who went to work every day at the local grocery stores, hospitals, urgent care clinics, and pharmacies particularly deserve our gratitude. As a result, the US economy only shrank by -3.5% last year despite the severity and length of the lockdowns.

Even more astounding was the rapid shift from stock market crash to boom conditions. Anyone who had been in a coma last year (as were so many government officials) and woke up to read the Wall Street Journal on Saturday, Jan 2nd, 2021, would have assumed that 2020 had been brimming with economic bliss.

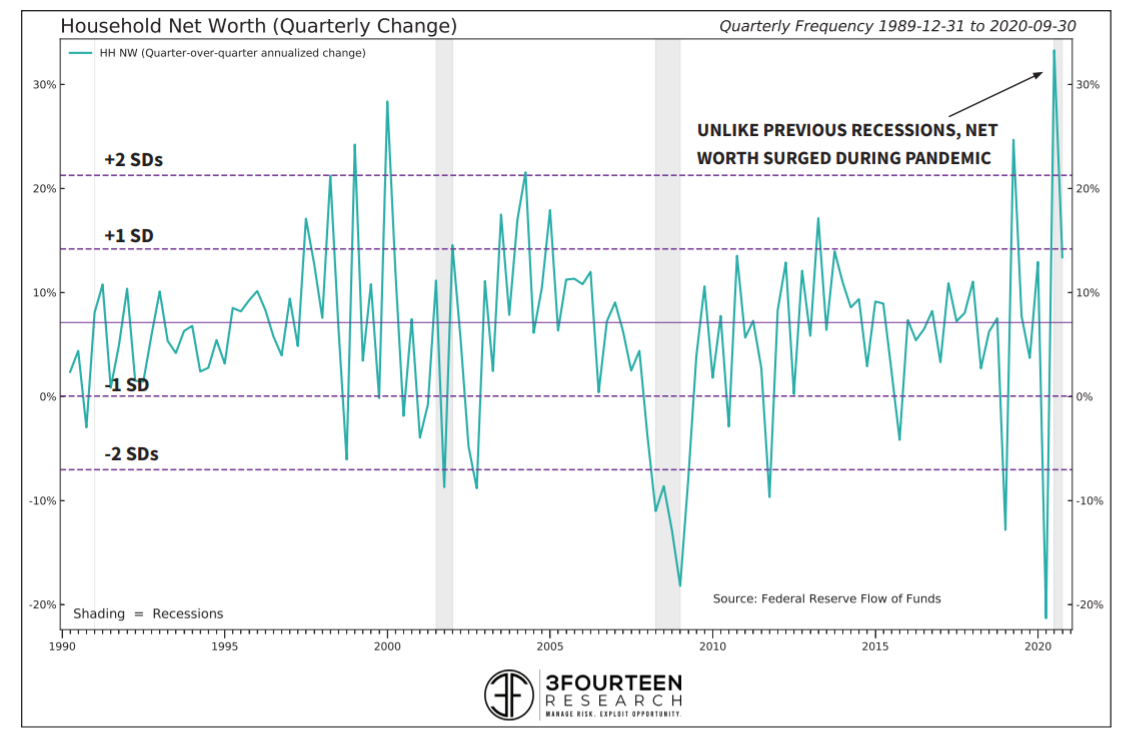

Obviously, a -3.5% GDP hit is brutal but it was much better than feared last spring. There was other good news as well. Thanks to the trillions of dollars of government stimulus and relief packages, consumer net worth rose last year. This is something that has never happened before in a recession.

Further on the good news front, the lockdowns led to a precipitous drop in greenhouse gas emissions. While this was obviously a temporary phenomenon, it did continue a trend that has been in place for the last 50 years, at least in the US. According to the EPA, America’s air pollution has declined by 75% since 1970, a remarkable achievement considering the enormous increase in the economy, as well as the number of planes and vehicles in use, since then. This is a positive that receives almost no mainstream media coverage.

Another below-the-radar piece of good news, at least in my view, is the emergence of a bipartisan political coalition known as “No Labels”. This is a group of 56 Congresswomen and -men, equally split between Republicans and Democrats. The co-chair of the sponsoring organization is the billionaire investor Howard Marks, often quoted in past EVAs. It has been in existence for 10 years but don’t feel bad if you weren’t aware of them; I wasn’t either until I read about “No Labels” in one of Mr. Marks’ celebrated newsletters (Warren Buffett is a big fan) and then was reminded of it recently by a client.

“No Labels” facilitated the creation of the Problem Solver Caucus now made up of the 56 elected officials (with hopefully more to join). Its main mission is to act as a counterweight to our nation’s current state of hyper-partisan politics which I believe is ripping America apart. While I plan to cover this encouraging development in more detail in a later EVA if you’d like to learn more about “No Labels” please follow this link.

There may be more good, even great, news this year as vaccines are finally broadly administered and the economy re-opens. The up-lift from millions of people returning to work, combined with trillions of government spending--and the $1.5 trillion of consumer savings that has accumulated during the lockdown--is highly likely to lead to a booming economy before long, perhaps as early as the late second quarter. It’s possible GDP gains will rival those seen in the 1980s and 1990s. In fact, I think we could have a quarter or two where the economy surges by as much as a 10% annualized rate. (Accordingly, Evergreen has been methodically accumulating shares in companies that are beneficiaries of a robust economy, particularly those that haven’t yet gone postal—for sure, a dwindling list.)

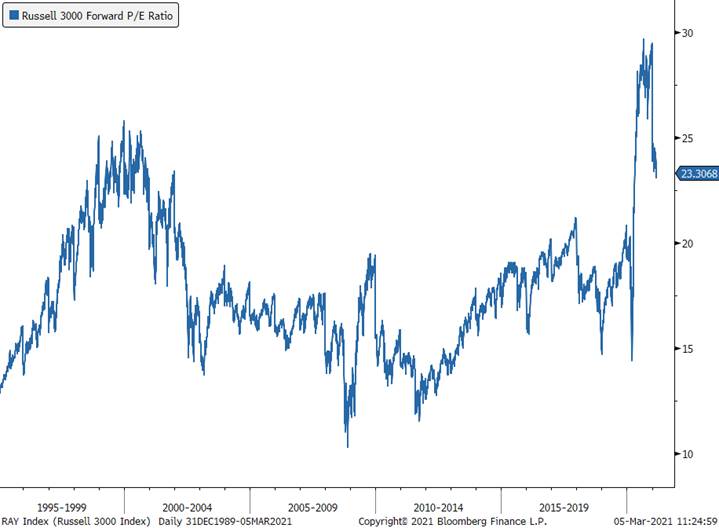

Is it all hunky-dory then? Hey, it wouldn’t be an EVA, at least one written by David Hay, if I didn’t question the sustainability of this probable boom. For one thing, it’s inarguable that US stock market valuations are among the highest ever, in some cases exceeding the late 1990s, the biggest equity bubble in American history. (You can see the impact of the recent correction on these charts.)

What’s surprising about these charts is that the two using forward earnings (which along with price is the P/E ratio), are as elevated as they are. These are based on optimistic analyst projections for this year’s profits. Based on the strength of the economy we should experience soon, they might be accurate--unlike the usual overestimation Wall Street usually does—but they clearly reflect a market bubble. Moreover, using my personal favorite valuation measure, the S&P 500’s price-to-sales ratio, the alarm bells are ringing even more loudly. (I prefer using sales versus earnings in the ratios because revenues are less volatile and they also are harder to fudge with creative accounting.)

However, there’s another mega-problem pending, besides nosebleed valuations, and it relates back to the relatively mild, considering the circumstances, GDP hit last year. -3.5% represents about a $700 billion dollar contraction in economic activity. That’s a significant number, for sure, but consider the offsets that have occurred. The US federal government deficit last year is likely to come in around $3 trillion, up by $2 trillion from what was already an inexcusably inflated level pre-Covid. And, of course, there is more “stim” on the way, though more moderate members of Congress (like the Problem Solvers Caucus) are pushing back against the $1.9 trillion additional package sought by the Biden administration. This is an amount roughly equal to the market cap of Apple, the world’s most valuable company, and while it’s being spun as a Covid relief bill, little of it is going to those who are still suffering economic distress due to the pandemic.

Additionally, the $900 billion stimulus bill passed in December, combined with what will still be a monster budget shortfall this year, means that the total deficit-spend between last year and this year will be in the neighborhood of $6 trillion, or more (as usual, when it comes to government largesse, I’ll take the over). Even the mathematically-challenged will appreciate that $6 trillion is a heck of a lot bigger than the $700 billion GDP hole. Can you say over-stimulus? Actually, it’s more like over-OVER-stimulus.

The Wall Street Journal’s Greg Ip recently noted that thanks to Federal assistance, aggregate wages and salaries actually rose last year by 2% and, with the additional aid package they might be up by 13% versus 2019. In 2020, prior to these last two stimulus extravaganzas, the average household in the lowest 20% of income-earners were the recipients of $45,000 in government aid. Moving up the earnings ladder, a working couple with three kids making $150,000 is poised to collect $10,000 from the upcoming stimulus payments. With the latest $1.9 trillion stimulus, $1400 checks are going to multi-millionaires and families making up to $400,000.

How is the government able to raise such immense sums? Unlike in the past, it’s not via the bond market. There isn’t enough private demand to fund the multi-trillion deficits, at least not without driving up interest rates to a level that would likely crash the stock market, leading to all sorts of disastrous after-shocks. Actually, that was the case even before Covid. The intense dislocations during September 2019, in the overnight bank lending (repo) market, revealed who the savior needed to be—the Fed, naturally.

The repo market problems forced the Fed to fabricate money at about a $700 billion annual pace before the pandemic struck. Since then, it has matched the $3 trillion or so of government deficit spending almost dollar for dollar. The net result has been an extraordinary boom in asset prices.

In numerous prior EVAs, I’ve noted that what the US is doing today is essentially Modern Monetary Theory (MMT). This economic “model” is based on the belief that since America borrows in its own monetary unit, which fortuitously happens to be the world’s reserve currency, it can deficit-spend to its heart’s content. And if, as now, there isn’t enough internal or external (foreign investor) funding, at acceptable interest rates, the Fed simply creates the funds from its Magical Money Machine (MMM). As I’ve written before, it’s MMT meets MMM—an exquisite marriage.

Another point I’ve made a few times is that MMT approaches have been tried before, among a long list of countries. The initial effect is an asset price boom such as we have today. Ultimately, though, what brings the party to an unhappy ending is inflation—not just in stocks—but in consumer prices. This is the mega-problem to which I referred earlier. In various prior EVAs, I’ve written about this mounting risk but now it is becoming top of mind for both stock and bond investors.

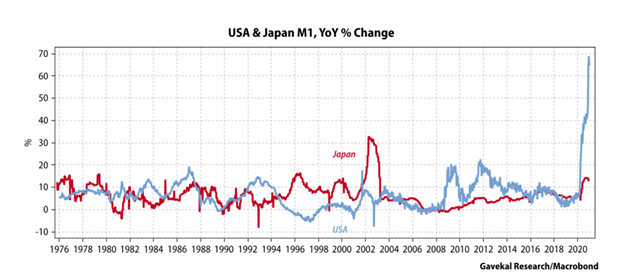

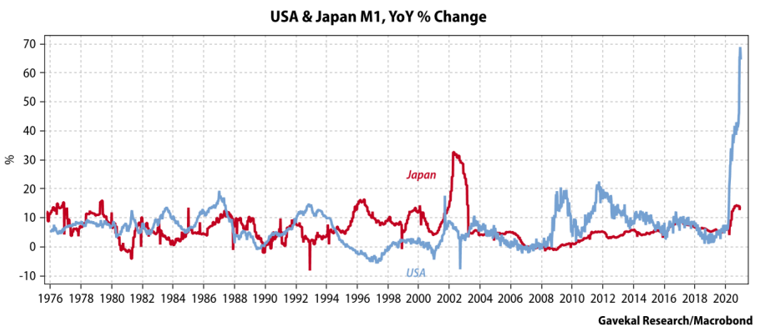

Many dismiss this concern by pointing to Japan which for three decades has tried massive monetary and fiscal stimulus, yet experienced more deflation than inflation. However, as our colleagues at Gavekal have illustrated per the below chart, Japan’s money supply (M1) never did the moonshot being seen in America today. The Fed is dropping hints that it wouldn’t have a problem if inflation rose to 3%. The assumption is that, should it rise above such a level, the Fed would bring it back down. And how might it do so? By reversing its latest binge printing (selling rather than buying treasury debt)? Or, perhaps, via raising interest rates? As the millennials like to abbreviate in their texts—ROFL (rolling on the floor, laughing).

Frankly, I don’t see how inflation of at least 3%--probably higher, possibly much--won’t result from a reopening economy in conjunction with the multi-trillion money fabrication and stimulus spending. This is not the QEs* from the last decade when deficit spending was decelerating, not exploding. Even the perennially upbeat Jeremy Siegel is warning that bondholders will suffer due to higher inflation.

In my view, the Fed is in a trap of its own making. Should inflation accelerate, it has no good options. It either lets price spiral up and the US dollar tank, or it tightens aggressively as it tries to play catch-up with the CPI. If you think an inflation problem is a low probability, I’d suggest you listen to a recent podcast my great friend Grant Williams recently did with Paul Singer of Elliott Capital Management on this topic. Mr. Singer is in the same net worth and investment-savvy league as Howard Marks; thus, his opinions are definitely worth considering. Both have made fortunes for themselves and their clients primarily through capitalizing on dislocations, ironically, in distressed debt. (They may soon have an opportunity to do so again—with US government debt!)

If you would like the ultra-Cliff Notes version, Mr. Singer believes the Fed is clueless about the gargantuan bubble it has allowed to form in almost all asset classes. He believes, as do I, the Fed’s going to get much more actual inflation than it is hoping for and that it will then be in a terrible bind.

Grant asked him if he thought this was intentional and Mr. Singer said that he believes it’s out of ignorance. His opinion is based on the released minutes from the Fed meetings fifteen years ago, as the housing mania of that time was in full swing and the Fed was utterly clueless to the dangers (such as Ben Bernanke’s infamous “contained in sub-prime mortgages” declaration).

Current Fed chairman Jay Powell is reprising this cavalier attitude by using language such as he did last month: “So valuations are high, but not at extremes”. He then went on to justify lofty stock prices because interest rates are low, neglecting to mention those minuscule yields are a function of both the sluggish growth of the last decade and the Fed’s multi-trillion buying binge of treasury debt.

Even more incredibly, Mr. Powell has also recently said: “The connection between low interest rates and asset values is probably something that’s not as tight as people think.” So, Jay, which is it? Is there a connection or is there not?

This leads me back to the main theme of this EVA: the increasing encroachment by the Federal government (and some state governments) into the economy’s ecosystem and, also, our daily lives. Based on the growing affinity for socialism in America and, critically, the aforementioned de facto implementation of Bernie Sanders’s economic model, Modern Monetary Theory, I feel this may be the most pressing issue of our time.

*QE stands for Quantitative Easing, which is the Fed’s fancy term for new-age money printing. The trillions, now approaching eight, that have been fabricated in this way have mostly been used to buy government bonds and mortgages, driving interest rates down to previously unseen levels.

Clearly, the Fed’s role in the economy and financial markets has expanded enormously in the wake of the housing bubble-induced Global Financial Crisis. The irony of this is acute considering that the Fed created and even egged-on the mortgage mania from 2003 to 2008. Former Fed Chairman Alan Greenspan encouraged consumers to take out adjustable-rate mortgages, a device that blew even more helium into the housing blimp. Thus, the Fed did a terrible job of bubble interdiction and yet it has been rewarded with ever greater powers.

Its mission statement has now been expanded beyond the already very challenging, and often conflicting, dual mandate of containing inflation and maintaining full employment. Now it is also charged with rectifying climate change and racial injustice. This is the Peter Principle on steroids.

Over the last 25 years, the Fed has repeatedly allowed enormous bubbles to form without once raising margin requirements and, over the last decade, only meekly hiking interest rates. At a late January press conference, Jay Powell was attempting to defend the Fed’s inaction during the mania in GameStop and the other WallStreetBets playthings. Quoting my friend Danielle Di Martino Booth: “One intrepid reporter, Bloomberg’s Michael McKee, even forced (Jay) Powell to repeat the sins of Irrational Exuberance of days gone by, pressing Powell by asking: ‘Have you discussed raising margin requirements under Regulation T and if not, why not?’ To this, a shell-shocked Powell replied: ‘No, we haven’t done that. Remember, we’re focused on maximum employment, price stability, financial stability as I define it, the broad financial sector’.”

The history of the past two and a half decades has shown us the fallacy of this see-no-bubble approach. Once these manias implode—be they tech stocks or housing—the real economy tanks, mass layoffs ensue, deflation fears erupt, and the Fed is forced to resort to ever-more radical policies to prevent a systemic collapse. In other words, its bubble-blind policies produce the exact opposite of the type of price and financial stability the Fed purports to pursue.

The Fed has been begging the Federal government in recent years to “go big or go home” with deficit spending. As mentioned above, it’s going to get its wish—and much, much more. Even Jay Powell seems to suddenly realize the risk of an overstimulated economy is growing should the next $1.9 spending blitz happen, a concern expressed by stalwart Democratic economic advisers like Larry Summers. (There is now an effort underway in Congress to add on a $4 trillion infrastructure bill. God help us!)

As a result of this fiscal insanity, over the last few weeks, the long-slumbering bond market vigilantes have suddenly woken up. With consumer inflation expectations already at 3%, a six-year high, they may become ever more cantankerous. As you can see, the rate rise is getting serious, with the downtrend in yields post-Covid now clearly broken, as we also showed last week.

Additionally, stocks have begun to feel the bond market’s pain. What seemed a one-way market—as in straight up— now looks increasingly vulnerable. Our partner firm, GaveKal, has done extensive research on stock market performance during Keynesian (i.e. big deficit-spending) episodes and those with moderate government stimulus. Stocks perform far better in the long run during the lower government-spending eras. And, of course, this is the mother of all Keynesian experiments with MMT taking this to a drastically higher level.

Yet, it’s far more than just the Fed taking on much more than it can handle—after consistently proving it couldn’t cope with its previous burdens. Due to the pandemic, the US government has intervened into the private sector to an unparalleled degree, as have most state and local governments. Tremendous economic devastation resulted. Was it necessary? That’s a question I believe will be debated for decades, if not longer.

Certainly, the experience of non-Western governments indicates that our policymakers handled the challenge very poorly, likely underreacting at first and then overreacting. Check out the deaths per million rates in several Asian/Pacific Rim countries with those in America and, especially, New York state.

Deaths per million by Country/State

The Empire State’s governor Mario Cuomo has positioned himself as an intrepid Covid warrior but the results tell a very different story, as do the recent revelations of how his administration understated nursing home Covid deaths. It was Mr. Cuomo’s decision early on to place Covid patients in retirement facilities and then to cover up the appalling death rate stats that resulted. This has caused even his own party to turn on him.

Neither Mr. Cuomo nor the Democrats have a monopoly on Covid ineptitude and deception. Former President Donald Trump excelled at both of those, as well. Many states, both red and blue, have also bungled the vaccine rollout, with countless precious but unadministered doses being thrown out. As all Americans are sadly aware, even for those 65 and older, obtaining a vaccine has been totally confusing and utterly frustrating, despite recent improvements. As the Wall Street Journal’s Daniel Henninger rightfully asked in a January 21st Op-Ed, “If governments can’t do something this straightforward—two injections—what can it do?”

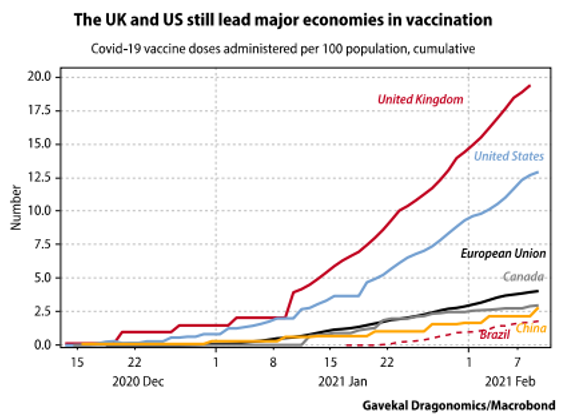

The most successful states diverged from overly stringent federal government guidelines and rapidly deployed vaccines to the elderly and essential workers. States that did so--like North and South Dakota, Alaska, and West Virginia--left those such as California in the dust. This once again illustrates that smaller, more nimble government is preferrable to a lumbering bureaucracy. The experience in even more sclerotic and bureaucratic Europe, where vaccine rollouts have made the US look like a well-oiled machine, underscore this point. (The UK shifted in late December to a rapid-deployment, looser-restriction model similar to US states like West Virginia.)

It also didn’t help to have politicians of both parties initially blow off the severity of the pandemic and encourage life-as-normal. Even the now-lionized Anthony Fauci said in late January of last year “I can’t imagine shutting down New York or Los Angeles…historically, when you shut things down it doesn’t have a major effect.” But maybe he was right after all, even though shortly after uttering those words, he became a lock-down proponent. The death rate per million in California (1190), which did lock-down hard after an initial delay, and Florida (1339) are remarkably similar. (Florida’s slightly worse performance vs California is almost certainly due to the former’s far greater percentage of senior citizens.)

Hindsight is always an unfair advantage but it’s now clear, based on the experience of myriad countries and states, that social-distancing, masking, and protecting the elderly were all wise and appropriate moves. Draconian and long-lasting lockdowns, however, are likely, in my view, to be harshly viewed in the fullness of time. Regardless, it’s hard to argue that most western governments, including the US, covered themselves in glory through this disaster. In America, the failure to much more extensively outsource the distribution and administration of vaccines to companies like Amazon, McKesson, CVS, Walmart, and Walgreen’s, and a long list of others, strikes me as inexcusably inept.

Another illustration of the superior response to the Covid crisis by the private sector is with education. Unquestionably, some of the greatest hardships of the pandemic have been borne by America’s children and their parents. Again, it boggles my mind that the federal government, working with state and local governments, couldn’t get a supply of N95 masks to every teacher in America before last September. There are now companies sitting on tens of millions of N95 masks that remain undistributed. And why weren’t teachers considered essential so that they could get vaccinated early on?

Despite these policy blunders, private schools have largely re-opened unless they were prevented from doing so by local authorities. On the other hand, public schools have mostly stayed closed, at least in the heavily populated coastal regions (excluding the southeast). It’s my belief most teachers would like to be back in the classrooms, with proper protection, but their unions are generally vehemently opposed to re-openings. It will be interesting to see how these union mandarins react once vaccines are widely available and there is little basis for continuing the lockdowns which have exasperated even many Democratic party officials.

Returning to the overarching theme of this EVA, yes, the Planet Earth still stands after the year the Earth stood still. Yet, looking at the big picture objectively, how well has the public sector done in coping with the Covid crisis compared to the private sector? In my opinion, it’s not even close. And yet—leading into next week’s EVA, the second installment on this topic which I believe is so vitally important—we are now trusting the federal government, along with state and local governments, to bring to satisfactory fruition one of the most radical transformations the world has ever seen. Until next week…

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.