“An entire industry is nearly priced as though it will simply run off its existing assets. How can this be? We believe there are simply no buyers left.”

– Natural resource investing experts, Goehring and Rozencwajg

“Valuation, I find, is a useless tool. If you base your investment decisions on valuation, you are never going to make money.”

– Mark Schmehl, portfolio manager at Fidelity Canadian Growth Company fund

______________________________________________________________________________________________________

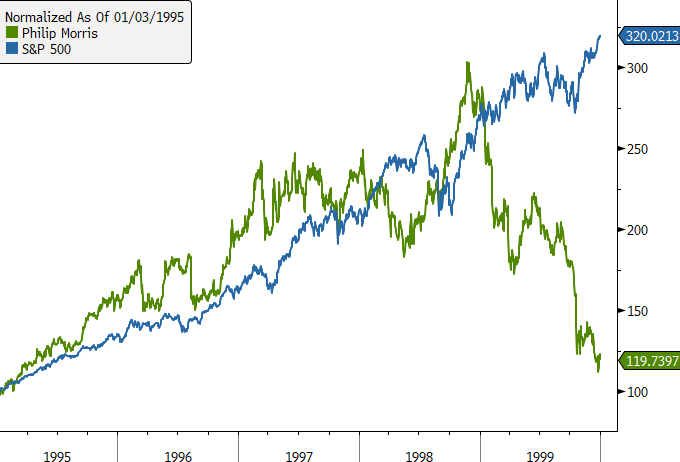

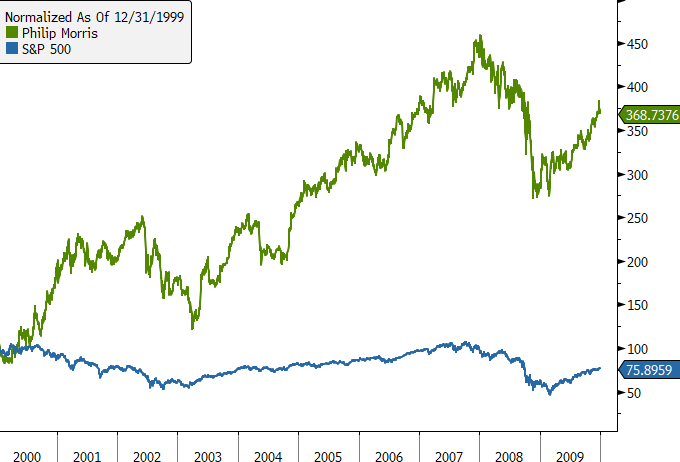

There may have been no more reviled corner of the stock market in its history than tobacco stocks were in the late 1990s. The industry was besieged by countless multi-billion lawsuits from almost every state in the union. It appeared destined to suffer the same fate as asbestos producers, most of which were driven into bankruptcy by crushing tort liability plaintiff awards.

Incredibly, however, companies like Philip Morris and R.J. Reynolds methodically settled their suits, providing a number of states with enormous future revenue streams from the settlement proceeds. Often, these states packaged their projected cash flows into bonds which were then sold to yield-hungry investors. Thus, a win-win was achieved…except for the users of the products who continued to die premature deaths. (On a personal note, I’ve lost a mother and two close friends to their smoking addictions.)

Even hardy contrarians, such as I, were reluctant to touch stocks like Philip Morris – putting aside our personal feelings about the lethality of their wares. The specter of never-ending litigation was impossible to quantify, at least in my mind as well as to many other portfolio managers, perhaps most.

Accordingly, their valuations were garage-sale cheap even as the tech bubble drove the S&P 500 to its highest valuation in history (yes, even more inflated than in 1929). Yet, seemingly against all odds, the planet’s leading tobacco company, Philip Morris not only stayed solvent, but it also went on to absolutely crush the stock market over the subsequent ten years.

Source: Bloomberg, Evergreen Gavekal

No one is attacking the tobacco industry these days despite that it continues to escort hundreds of thousands, if not millions, to an early grave. Today, the market’s new whipping boy is the energy industry, at least those based on fossil fuels.

Some thought leaders are going so far as to compare energy to tobacco. Even among the less strident, fossil fuel-based energy is becoming viewed as totally toxic and virtually un-investable. In reality, there is an element of the fossil fuel industry that actually has some parallels with tobacco.

Coal-based power generation does release enormous quantities of unhealthy particulates into the atmosphere, undoubtedly harming the health of hundreds of millions, possibly billions, of human beings. Fortunately, as noted in our “Apocalypse Not Now” EVA, published October 18, 2019, generating electricity from coal is on its way out in the US, though it does still possess a fast-dwindling 20% or so market share.

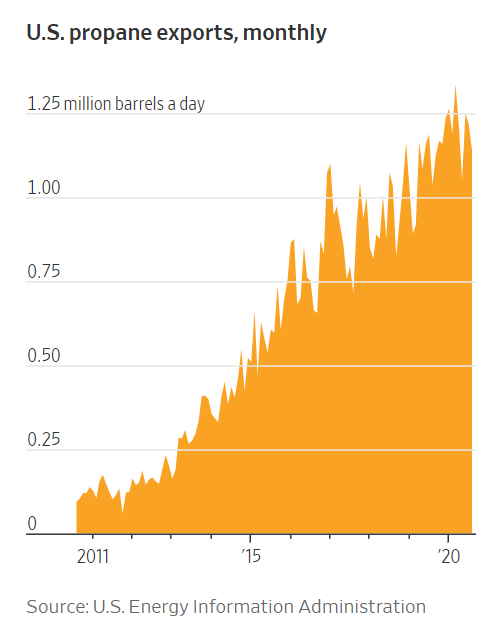

In the developing world, it’s also important for “First Worlders” to realize that the World Health Organization estimates roughly 3 million people die prematurely every year due to heating their homes by burning wood, charcoal, and even dung. The US energy sector is helping to address this humanitarian disaster through booming exports of clean-burning propane (LPG).

Since writing the “Apocalypse Not Now” EVA, I have read a couple of fascinating books on climate change. One of them is by a man I’ve admired since the 1980s, astrophysicist Hugh Ross, called “Weathering Climate Change”. Dr. Ross is no climate change denier and he actually suggested an explanation for a question that has long baffled me…but more on that later.

The relevant point with coal is his belief that black carbon soot, blowing over in the high atmosphere from China and the rest of Asia, is blanketing Northern Canada’s snow and ice fields. This makes them less reflective of the sun’s warmth, leading them to melt much faster than in the past.

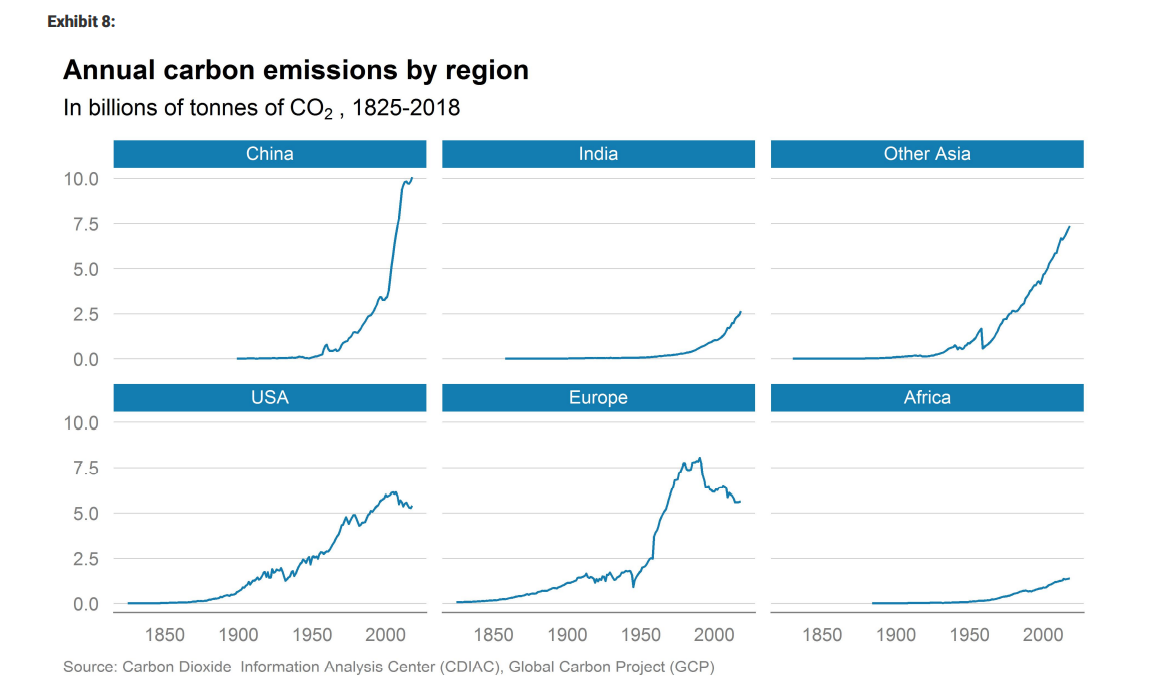

Despite China’s carbon reduction pledges, its actions tell a very different story. It is frantically constructing new coal-fired power plants, as is much of the rest of Asia. In fact, China has far more coal plants being built than are operating in the US today. As you can also see, India is no slouch in this regard.

It’s rational to wonder why there is enormous media support in the West for green energy, including electric vehicles (which, ironically are mostly indirectly powered by fossil fuels via the electrical grid) and yet pollution-gushing China attracts scant outcry. Showing the irony of the electric vehicle (EV) push, China is by far the largest market for EVs. Yet, since its grid is 60% powered by coal, this actually does far greater environmental damage than traditional internal combustion-fueled vehicles.

It seems to me that if the goal is really CO2 reduction—and, particularly, reducing the emissions of truly harmful molecules such as nitrous oxide (N20)*—there would be a global effort to tax countries that are the leading generators of CO2 and, even more so, actual effluents, like N20. (The European Union has proposed doing so but it has attracted little support thus far.)

However, even though CO2 is not a pollutant and is, in fact, vital for human, animal, and plant life, Dr. Ross did shed light on its role in climate change. To me, it has long seemed strange that such a benign substance, which has seen its atmospheric content rise from a mere 280 parts per million to 430 parts per million (i.e., from 0.00028 to 0.00043), could pose such an environmental threat. Yet, Dr. Ross’s book has compelling charts showing the linkage between the rise in CO2 levels and global temperatures. His explanation is that higher levels of CO2 increase water vapor in the atmosphere. You may not be aware of this but the most prevalent greenhouse gas (GHG) is water vapor.

*Some scientists contend that N2O is the primary ozone depleting emission. (See page 33, “Weathering Climate Change.”)

Before my climate-change skeptic EVA readers inundate me with emails about that last paragraph, let me readily concede that there are many other factors that could be behind the temperature rise such as solar activity, the shape of the Earth’s orbit around the sun, its inclination (axis tilt), and even plate tectonics. However, it seems more than coincidental that the surge in CO2 output over the last 70 years has aligned with the sharpest temperature increase of the past 2000 years. (Figure 2.5, “Weathering Climate Change”.)

Dr. Ross also answered a question I raised in the “Apocalypse Not Now” EVA on climate change we ran last fall that I alluded to earlier. The query I posed to EVA readers back then was why the carbonate/silicate cycle, which has kept the planet’s atmospheric CO2 content in rough balance since time immemorial, is no longer doing so.

Even though anthropogenic (man-caused) CO2 emissions amount to a comparatively small amount of total carbon output, it is apparently enough to throw off the normal balancing act that occurs as temperatures rise. Warmer temperatures cause more CO2 to be flushed out of the atmosphere and deposited into the oceans. This eventually gets absorbed into the Earth’s mantle. Colder atmospheric conditions cause CO2 levels to increase, creating warming conditions. This is the natural equilibrium process. But humanity does appear to be throwing a spanner into the works, as the Brits like to say.

Consequently, although CO2 is an innocuous byproduct (as even The NY Times recently referred to it) of burning fossil fuels, and it’s also a miniscule part of the Earth’s atmosphere, it appears to be a key factor in our planet’s warming trend of the last 70 years.

Of course, “key” doesn’t mean only. From a very big picture standpoint, the biggest challenge is the sun’s increasing luminosity or intensity. For eons, cooling events such as asteroid strikes and volcanic activity (which blocks out solar radiation), have offset the sun’s slowly rising radiation (the sun is now about 20% brighter than when life first appeared on earth). If human-generated emissions negate the cooling factors, thereby creating a double-warming effect, the future could be very toasty indeed. Dr. Ross also contends that the greatest warming has come from the population growth of farm animals, particularly cows, the domestication of rice and the conversions of forests into grassland and farms.)

Accordingly, I appreciate the desire to reduce atmospheric CO2 although I do believe cutting back on far more powerful and/or harmful emissions such as methane and N20 should be the main priorities. However, the unprecedented plunge in man-base emissions caused by the Covid pandemic has revealed some disturbing data that hasn’t received the attention I believe it deserves.

The International Energy Agency is projecting that this decade will see the slowest growth in energy demand since the 1930s, primarily because of this year’s demand collapse that will impact future years as well, even as global economies gradually return to normal activity. An October 15th, 2020, Financial Times article stated: “But despite the decline in emissions, scientists said it was unlikely to make a difference to long-term rising temperatures on the planet…”

The article went on to quote a climate scientist who said: “Unfortunately, the climate protection impact will be almost negligible.” In other words, the biggest negative shock to energy usage since the Great Depression barely moved the needle on improving carbon emissions. If that’s truly right, is the West pursuing the right climate change strategy by moving to EVs, along with solar and wind power?

Reinforcing this was a study by the UN and the US government based on the Model for the Assessment of Greenhouse Gasses Induced Climate Change (MAGICC). The model predicted that "the complete elimination of all fossil fuels in the US immediately would only restrict any increase in world temperature by less than one tenth of one degree Celsius by 2050, and by less than one fifth of one degree Celsius by 2100." Say again? If the world’s biggest carbon emitter on a per capita basis causes minimal improvement by going cold turkey on fossil fuels, are we making the right moves by allocating tens of trillions of dollars that we don’t have toward the currently in-vogue green energy solutions?

(While EVs are in the lead currently for taking market share from the internal combustion engine, hydrogen might win the long race. The Japanese automakers are making a major push with hydrogen-powered fuel cells and it has a number of advantages over charging EVs off the power grid, as well as disadvantages. One big positive is that hydrogen can be transported via the existing pipeline infrastructure. It continues to be my belief that transmission lines, and the fierce local opposition to their installation, is the Achilles heel of massive solar and wind farms, which themselves often trigger intense “Not In My Backyard”, aka NIMBY, reactions.)

I realize it is almost heresy, punishable by reputational death, to question the current green energy belief system these days but I’ve got some very influential company. The second epiphany-producing climate change-related book I’ve read lately is one with a coincidentally similar title to our EVA from last autumn: “Apocalypse Never” by Michael Shellenberger. Its subtitle is “Why Environmental Alarmism Hurts Us All”. What makes this book such a shocker is that Mr. Shellenberger is a life-long climate activist. In fact, he is a former Time Magazine hero of the environment.

It’s a book that I think anyone with a serious interest in climate change should read with an open mind. (For a sampler of the book, please click on this link to watch a speech Mr. Shellenberger delivered in November 2018.) In a nutshell, he believes the current focus on wind and solar power is badly misguided for a variety of reasons, including their lack of energy density versus fossil fuels, the vast amount of land and natural resources required to construct them, plus the negative impact on birds and other wildlife. (For those who say that cats kill more birds than windmills, as I often hear on CNBC, realize that eagles kill cats, not the other way around; but windmills kill eagles, condors, and other large birds, some of which are endangered species.)

It would take a full EVA to do justice to Mr. Shellenberger’s book but the bottom-line is that he’s excoriating the environmental movement he’s so long been a part of for demonizing (often with false facts and data) the nuclear power industry. He’s no fan of fossil fuels, though he does concede the many advantages they offer on a bang-for-the-buck basis over solar and wind. His overarching question is now that we know renewables can’t save the planet, are we going to allow them to destroy it? (Don’t flame-mail the messenger! Check out the video and/or the book. Moreover, brainiacs such as Matt Ridley and Bjorn Lomborg are making similar assertions.)

In Mr. Shellenberg’s view, reviving the global nuclear power industry is essential to lowering carbon output without inflicting severe environmental harm. Before you dismiss his views out of hand consider the dramatic divergence in France and Germany over the last two decades. Despite a frantic and extremely costly push toward renewables, Germany’s CO2 output is 88% higher than France’s today, up from 65% greater in 2000. Nuclear power provides 72% of French electricity generation versus just 12% in Germany. (Accordingly, EVs make a lot of sense in France.)

Similarly, on a per capita basis, US CO2 emissions are down nearly 30% over the past two decades. This has occurred despite the US moving away from nuclear power. In our case, the dramatic improvement has been due to switching away from burning coal to produce electricity and toward natural gas, as well as the recent rapid growth of solar and wind power. (However, non-hydro renewables remain a miniscule portion of primary fuel consumption, per Morgan Stanley.)

It’s hard to dispute the contention that unless the US suddenly develops a viable nuclear power industry again (as Bill Gates is attempting using new technologies), natural gas will be vital in further reducing our carbon emissions. With that as a segue, let me close this EVA with a relevant section.

A Tale of Two Stocks.

Returning to the opening theme of “totally toxic”, I want to contrast two outstanding companies and their stock market fortunes in recent years. One is Enterprise Products (EPD), the premier mid-stream energy infrastructure operator. The other is Paccar (PCAR), the most successful Class 8 (semi-tractor trailer) truck producer.

Since 2014, on the eve of two devastating energy bear markets, EPD’s profits are up by 63%; PCAR’s have shrunk by 5%. As previously mentioned, 2020 has seen the biggest decline in energy demand in 90 years and yet EPD’s earnings are projected to dip by a mere 1%. On the other hand, PCAR’s profits are forecast to swoon by 46%! Despite this, EPD’s unit price (equivalent to share price) is down 29% in 2020, notwithstanding a powerful rally over the last month. Conversely, PCAR’s stock is up 10% in 2020 despite its earnings collapse (including dividends/distributions, the comparative total returns have been -22% and +12%, respectively).

Looking back to 2014, when oil prices first crashed—putting almost all energy stocks in the penalty box—EPD is down 46% while PCAR is up 38%, with the latter recently making a new all-time high. This is despite the far better profits performance by EPD.

2020 Comparative Stock Price Performance: PCAR vs EPD

Since 2014 Comparative Stock Price Performance: PCAR vs EPD

Source: Bloomberg, Evergreen Gavekal

Based on the less than environmentally friendly nature of Class 8 trucks, and the diesel emissions they spew, one could argue that EPD, with its primary emphasis on natural gas transmission and processing, is more environmentally friendly than PCAR. Thus, in this age of socially responsible/ESG investing, EPD should be viewed as more compliant with those standards. But, clearly, that has not been an attribute, at least in market performance terms.

As an aside, I began gathering the research and creating the outline for this EVA over a month ago, before the robust rally in all things energy that has narrowed the gap vs companies such as PCAR; however, the valuation disparity remains yawning. EPD is currently yielding 9% and trades at 10 times this year’s forecast earnings. For PCAR, the numbers are 1 ½% and a 23 P/E. Which to you looks like a compelling value and which looks to be fully, possibly over-, priced?

Part of the reason I’m bringing this up is because recent months have seen the actualization of the “Great Rotation” that I, and many others, have long been anticipating. This refers to a revival of value type stocks, like EPD and PCAR, viz a viz the performance superstars of the last decade, growth names such as Microsoft, Apple, Tesla, Google, Facebook, and many others of that variety.

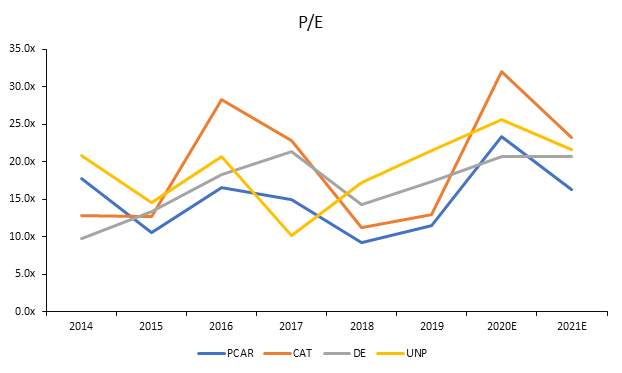

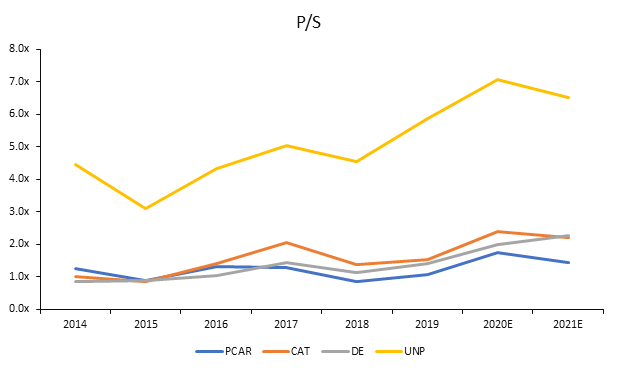

Since the election, the Great Rotation has intensified and looking back at the last few months, value has beaten growth by 6%. This value rally has been so powerful that many other typical value stocks, besides PCAR, that usually trade at modest multiples of earnings and sales (hence, their value designation) are now so pricey as to question that they still belong in the bargain category. To that point, please see the P/E and price-to-sales (P/S) charts for PCAR, Caterpillar (CAT), John Deere (DE), and Union Pacific (UNP) based on 2021 (i.e, post-Covid) estimates.

Consequently, investors need to be extremely discerning when it comes to which value stocks are actually still values. Energy clearly qualifies despite the intense fears about the impact a Biden administration will have on this sector. But just as tobacco stocks were the shockers of twenty years ago, defense stocks were similarly in the crosshairs twelve years ago as Barack Obama moved into the Oval Office. Many at the time, including yours truly, felt President Obama’s defense spending cuts would create a multi-year headwind for companies like General Dynamics. But here’s how it performed during Mr. Obama’s presidency (with a spike in late 2016 due to Donald Trump’s election):

Of course, history rhymes, not repeats and this time could be very different for energy stocks. But realize this sector has lagged the S&P by the greatest percentage in market history since 2014, despite its recent stunning rally. The “totally toxic” label affixed to it is no doubt why. But here’s a thought experiment: What would happen to the US economy if every oil and gas well stopped producing and every energy pipeline stopped flowing? You know the answer—a total shutdown that would make Covid look like a hiccup. Whereas, if the US totally banned cigarettes, the economy wouldn’t miss a beat (in fact, it might even improve due to the associated reduced healthcare costs).

So, if you are one of the few intrepid souls brave enough to still hold oil and gas securities, the next time you hear that energy is the new tobacco, just smile to yourself and think “I hope so”, at least from a market performance standpoint. And also remember that leading up to the election, you could count with a reckless bandsaw operator’s fingers how many people thought energy stocks would soar after all the votes were counted (and recounted). And that was about 30% ago.

Notwithstanding the opening quote, buyers have suddenly shown up in force, even if a lot of it has been short-covering. In fact, with energy infrastructure issues like EPD, an increasing number of investors may be soon asking themselves: “If they didn’t cut their payouts during 2020, when will they?” In other words, this might be a way to attain a rock-solid 9%, tax-advantaged cash flow. In our yield-starved world, the word for that might be nirvana and a partial antidote to our nerve-wracked times.

For now, though, speculative juices continue to gush. Per the second quote from page one, there is presently little, if any, regard to the outrageous prices being paid for securities with alluring stories (and, often, an absence of earnings). To my retro-mind—back to a time when markets were dominated by investors like Peter Lynch and Warren Buffett—it’s about as foolish to say valuation is a useless tool as it is to contend that gold is an ineffective portfolio diversification tool. When this latest monstrous speculative bubble in COPS* pops, the old “barbaric relic” is almost certain to prove itself anything but useless.

*Crazy Over-Priced Stocks

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.