"That men do not learn very much from the lessons of history is the most important of all lessons that history has to teach."

-ALDOUS HUXLEY

A recurring theme in various EVAs over the years is the importance of the yield curve. Sorry, I know a term like that can literally throw non-professional investors—i.e., those with a real life—for a curve. But, unlike with so many human relationships, it’s NOT complicated.

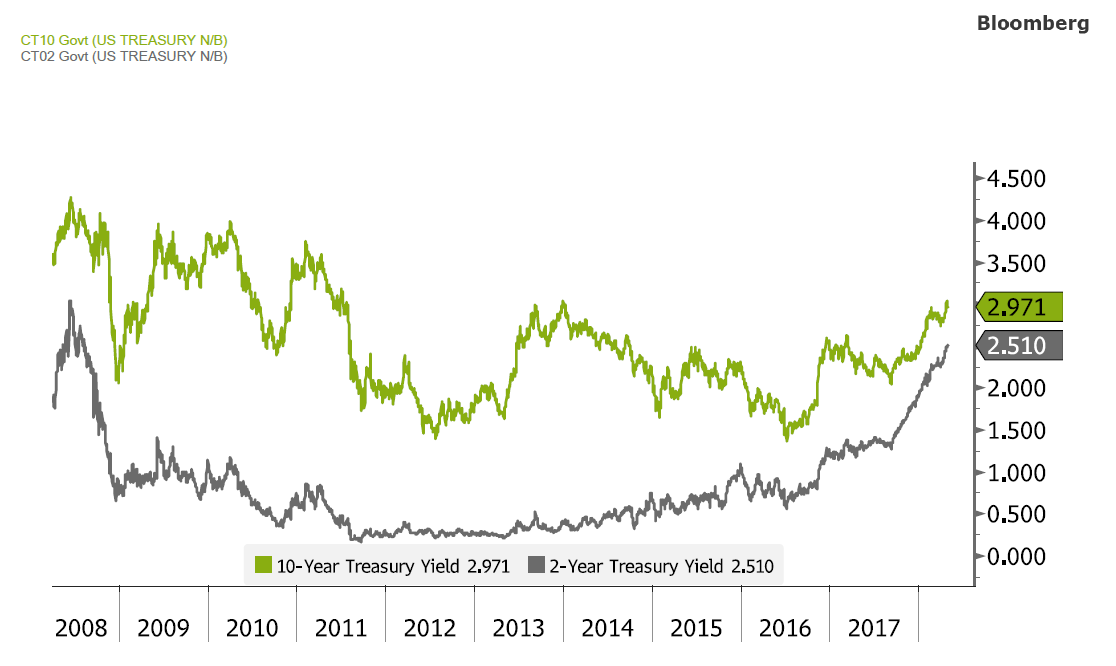

The yield curve is simply the difference between the yield on short-term bonds and those further out on the maturity curve—hence the name. For example, right now a two-year treasury note yields 2.51% while a ten-year note produces 2.97%. Thus, the difference is about 0.46% (46 basis points) which is still positive. (If it was 3.5% vs 3%, the yield curve would be considered negative, or, that dreaded term, inverted.)

However, the current differential is unusually tight, certainly by the standards of the post-financial crisis world and it has been narrowing rapidly. Should the Fed deliver on its plan to continue hiking through this year and into next, it’s not a flight of fancy to envision an inverted yield curve in the not-too-distant future.

Source: Bloomberg, Evergreen Gavekal (as of 5/2/2018)

Source: Bloomberg, Evergreen Gavekal (as of 5/2/2018)

This month’s Gavekal EVA describes a unique view of the yield curve courtesy of my friend, partner, and all-around hero in life, Charles Gave. As you will read, Charles is using two non-government interest rates to determine if the yield curve is generating any kind of warning impulse. His logic for using the two he has chosen—the prime rate and BBB-rated (also, known as Baa-rated) corporate bonds—is that central banks have radically distorted the yields on government bonds around the world. (FYI, roughly half of investment grade debt is rated BBB/Baa these days.)

It’s certainly fair to note central bank fabrication of trillions in digital reserves that they’ve used to buy government debt has distorted all interest rates, including those from corporate bonds. However, it’s reasonable to believe that non-government yields are less manipulated. And in the US, at least rates have risen back to something measurable instead of the still mostly non-existent yields seen in much of the developed world (with some $8 trillion of debt remaining at negative interest rates).

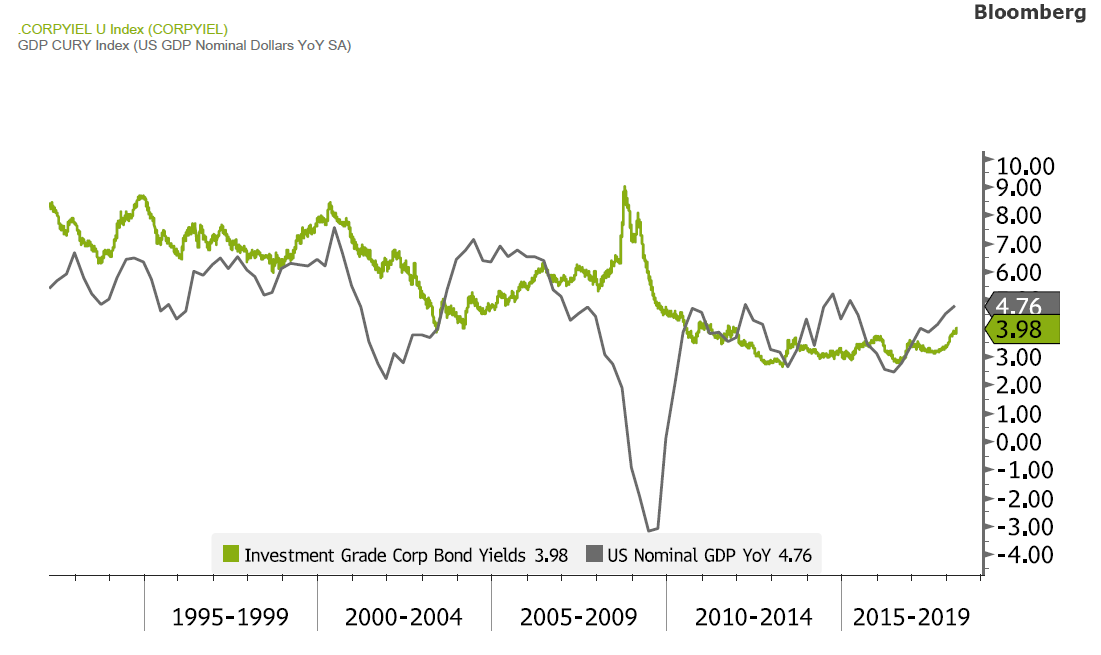

Charles is further making an interesting, but defensible, assertion that longer-term BBB rates typically offer yields around the GDP trend-line including inflation (i.e., nominal). He further notes that corporate profits are closely tied over time to GDP growth. If you think about it, those make sense and history has proven that to be the case (though there are times when there is some deviation).

For those who have read Charles over the years, you are aware that he is a big believer in the theories of the long-deceased Swedish economist, Knut Wicksell. The latter contended that when the market rate rises above the natural rate of interest (basically, the economy’s intrinsic growth rate), bad things happen. That’s certainly been the case with inverted yield curves over many decades.

Accordingly, a key aspect is that short-rates are market rates while longer yields roughly correspond to the natural rate. As Charles postulates, the prime rate is a decent proxy for market rates while BBB/Baa yields have long been closely linked to the economy’s inherent growth rate and, therefore, to the “natural” rate. Per the following chart, you can see that BBB/Baa bond yields have indeed generally closely tracked nominal GDP.*

Source: Bloomberg, Evergreen Gavekal (as of 5/3/2018)

Source: Bloomberg, Evergreen Gavekal (as of 5/3/2018)

The huge, though temporary, divergence was in 2009 when corporate bond yields soared even as the economy collapse due to ultimately unfounded fears of widespread defaults. (As very long-time EVA readers recall, this newsletter was repeatedly urging investors to buy corporate yield securities during that panic.)

The bottom-line is that based on this approach, a yield curve inversion is near at hand. At this point, this measure isn’t in the danger-zone, but it is definitely a concerning development and Charles provides a few reasons why this is the case. (By the way, his “zombie” company comment refers to those highly leveraged entities that would likely fail if interest rates weren’t artificially depressed.)

As is the case with a number of key financial indicators, the warning bells will start clanging much louder should the Fed deliver on its commitment to continue hiking short-term (i.e., market) rates. Based on its meeting this week, that looks highly likely despite the market turbulence that rate rises are creating. Unfortunately, with inflation on the rise, the Fed doesn’t have much choice. But, as those who have studied financial cycles are well aware, this is how all expansions—and bull markets—meet their maker.

*The GDP we are accustomed to hearing and reading about is “real” GDP, which is net of inflation. Thus, if nominal GDP, inclusive of inflation, was 5% and the CPI was 2%, then real GDP would be 3%.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

WHY A CURVE INVERSION MATTERS

By Charles Gave

Investors are increasingly obsessed about the flattening of the US yield curve, leading to talk of the dreaded “I” word. This is not surprising as inversions have usually been followed by a US recession and attendant equity bear market. However, I have always found standard explanations of how and why this shift plays out to be unsatisfactory. A more persuasive argument comes from Wicksellian theory, as an inverted yield curve signifies that the “market rate of interest” has exceeded the “natural rate of interest”.

For Knut Wicksell, the late 19th century Swedish economist, economic cycles stem from the interaction between these two key interest rates:

Wicksell contended that when the market rate moves above the natural rate, it no longer makes sense to borrow. This is because the cost of capital has exceeded the structural growth rate of earnings. At such points, firms tend to repay debt and a recession usually becomes unavoidable. If short rates are taken as a proxy for the market rate, and long rates as a proxy for the natural rate, then it quickly becomes clear why a yield curve inversion is so worrying.

It makes sense to use these proxies if you assume that an economy with an open capital account sees, over the long run, a convergence of long-rates and the nominal growth rate. And since the structural growth of GDP can be assumed to match the structural growth of corporate profits, it follows that when long-rates are below the market rate, they must also be below the structural growth rate of corporate profits (i.e. the Wicksellian condition for a recession to unfold).

The problem with this approach is the quality of the proxy relationships, as the classical yield curve’s two key interest rates are not ideal stand-ins for the Wicksellian natural rate and market rate. For example, recent recessions in Japan occurred without the official yield curve ever inverting. This was because in deflationary Japan, the very low market rate was always above the natural rate due to nominal GDP declining (this is no longer the case).

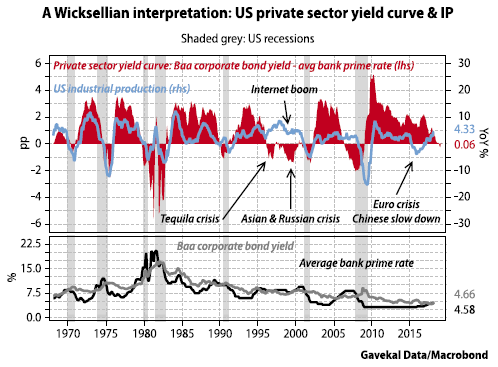

Hence, as a Wicksellian, I’d argue that what matters is not the public sector’s yield curve (the government can always borrow), but that of the private sector. Hence, for simplicity’s sake, let’s assume that the US economy’s natural rate is represented by the yield of a long-dated, seasoned industrial bond rated Baa by Moody’s. The market rate can be taken as the prime lending rate charged by US banks. The result is shown in the chart below.

Now things become clearer. Each time the private sector yield curve has inverted (red shaded area below zero), it can be seen then either a US recession has occurred within a year, or a financial accident has afflicted economies which run fixed currency links with the US dollar.

Consider a set of behaviors that firms will likely adopt in the event that the prime rate charged by banks is below the Baa bond rate.

As a result, in such periods banks will be able to earn a lot of “artificial” money. Yet in the event that the prime rate moves above the Baa rate, all bets should be taken off. Today, the private sector yield curve reading stands at zero, or right on the threshold where trouble can be expected to begin.

Should this spread move into negative territory, I would expect a financial accident to occur outside of the US, a US recession, or possibly both. In the latter two scenarios, US firms will no longer want to borrow and financial engineering will start to unravel. Zombie companies will fail and capital spending will be cut, as firms move to service debt and repay principal. Workers will get laid off and the economy will move into recession.

In such periods, US commercial and industrial bank loans usually plummet, and indeed that is the case right now. For this reason, I would advise investors to keep a beady eye on the spread between the Baa bond rate and the prime lending rate. If the spread does turn negative in the next few weeks or months with the Federal Reserve raising short rates, then some kind of economic or financial accident is almost certain in the following 12 months.

We are entering dangerous territory.

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.