“We’ve gone back into this kind of a foie-gras bubble environment. We’re all being force-fed risk assets. It’s an unpleasant experience when you’re playing goose to the central bank farmer.”

-James Montier, strategist at elite money manager, GMO

“Unless countries come together to take the right kind of policy measures, we could be facing years of slow and subpar growth.”

-Christine Lagarde, IMF Chief

Same time, this year. Almost everyone has heard the saying, “Fool me once, shame on you. Fool me twice, shame on me.” But what about, “Fool me four times”? It has been widely touted over each of the past four years that the global economy was about to achieve “sustainable acceleration,” “return to trend growth,” and “escape velocity,” or whatever other feel-good sound bite you care to use.

Unsurprisingly, those who have been wearing the economic “beer goggles” in recent years have tended to be the architects of, or apologists for, prevailing policies—a set of supposedly growth-stimulating measures so extreme that they might have caused John Maynard Keynes to blush. Yet, each year since 2010, the reality has been more of the same: Economic activity is moving as fast as the glacier on Mount Rainier.

2014, of course, was supposed to be different, especially in the US, where hopes have been running high for America to perform its typical role as the planet’s growth dynamo. This was believed to be the breakout year and, since it is still early, it could be. Undoubtedly, inclement weather has chilled activity in much of the country and, with spring in the air, a pickup seems probable. (It is ironic, though, that Europe’s latest sluggishness is being blamed by some on a mild winter that has restrained utility output and energy consumption.)

As expressed in last week’s EVA, the US has been growth-challenged for nearly 15 years. Europe has also experienced a recurring growth shortfall since the new millennium began, and in Japan the malaise is approaching a quarter of a century. Even emerging markets, which not long ago were supposed to keep the planet on a healthy expansion trajectory, have been looking like the Denver Broncos in the Super Bowl.

Additionally, inflation has been doing a vanishing act. Japan, as we all know, has been engaged in hand-to-hand combat with deflation for the past twenty years. Now that battle seems to be spreading to Europe, causing even inflation-phobic Germany to suddenly make noises about extreme counter-measures. And while deflation fears in the US are negligible, at least for now, overcapacity abroad and plunging foreign currencies have recently led to falling import prices even here.

If you think back to widely-held views of a few years ago, this is the precise opposite of what was supposed to happen, given the ultra-easy monetary policies by most of the world’s dominant central banks. Among the pessimistic back then, there was considerable hyperventilation about hyperinflation. For the optimists, rapid growth was just around the corner. But, despite zero or near-zero interest rates, countless trillions in deficit spending in most leading countries, and massive money creation in the US and Japan, inflation and growth remain largely MIA.

For true believers in the efficacy of the classic Keynesian remedies of incontinent fiscal and monetary policies, it is, and probably always will be, just a matter of time—no matter how many years go by. But, for the rest of us, it might be time to wonder if this isn’t the economic version of waiting for Godot. In case you don’t know, Godot was a no-show (as Mark Twain once wrote, “History doesn’t repeat, but it does rhyme!”).

A most unvirtuous circle. Veteran EVA readers know that for many years we have expressed the view that the missing link for both the inflation-paranoids and the growth-hopers was money velocity. As the rate at which money circulates through the economy crashed, it has become virtually impossible to trigger either a “normal” inflation rate or recovery (yes, I realize that “normal” is just a setting on your dryer but you get the idea). Figure 1 on the next page vividly illustrates that velocity has been declining and continues merrily on its downward path—a trend that is anything but normal. (However, as you will read later, this may be poised to change.) (See Figure 1 below)

Regular readers also won’t be surprised to learn that GaveKal’s co-founder, Charles Gave, has done some of the more ground-breaking and controversial work on this topic. Several months ago, we discussed his theory that velocity should be split in two: One part measuring what he calls “financial velocity,” and another that tracks “economic velocity.”

His key point, one we believe to be very valid, is that when central banks are bombarding the system with trillions of synthetic money, and anchoring interest rates close to zero, financial assets go bonkers. Money flows into the capital markets (like stocks) rather than capital assets (like new factories); hence, the result is high frequency financial velocity and low frequency economic velocity.

Since capital expenditures are essential for long-term economic vitality, the net result is bubbly financial markets—at least for awhile—and an underachieving economy. As you may have noticed, this is essentially the scenario that has played out over the last five years, and particularly the last two or three when QEs have been in full force. In fact, this has largely been the case for the last fifteen years. Accordingly, inflation has shown up primarily in asset, not consumer, prices.

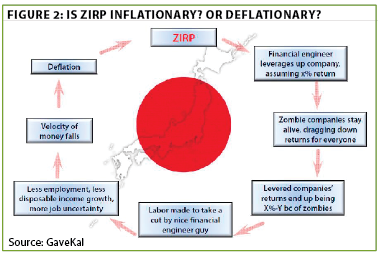

You may be wondering why this has been the case. Why is it that the two favorite acronyms of leading central bankers, QE (quantitative easing, commonly known as money printing) and ZIRP (zero interest rate policy) have failed to bring home the economic mail? One of the better answers I’ve seen comes from this simple chart GaveKal included in a recent presentation. (See Figure 2)

Basically, this illustrates that when interest rates are artificially low, companies that normally should fail due to excessive leverage and inferior profitability, linger aimlessly around (the zombie effect), luring earnings and returns away from healthy firms. Thus, capitalism’s essential function of creative destruction is inhibited, resulting in overall stagnation.

Additionally, very low interest rates encourage companies to leverage up and buy back their own stock (or buy out competitors) rather than invest in new plant and equipment (i.e., capital spending), per Charles’ theory. One of the two drivers of growth (along with population increases) is productivity, and it withers without capital investments. Thus, it should be no surprise that productivity has also been anemic in recent years, as discussed in last week’s EVA.

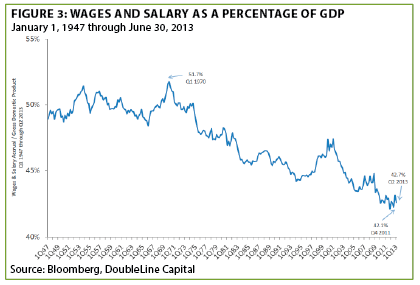

While this chart describes what has played out in Japan since their gargantuan asset price crash occurred over twenty-five years ago, it has also unfolded to a large degree in the US after our own home-grown (literally) bubble went kaput six years ago. The daisy-chain shown above may also be a prime reason why US workers have seen their share of the proverbial pie get cut down to super-model size (i.e., a tiny sliver). As you can see below, this trend has been in place since the early 1970s, but it accelerated after 2000, when we first began to see excessively easy Fed policies (first to combat the tech bubble bust and then the housing meltdown). (See Figure 3)

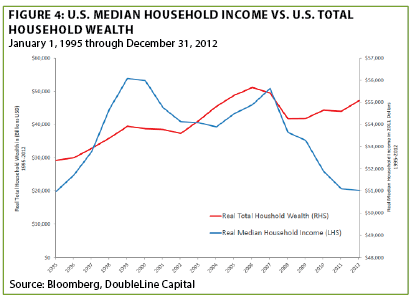

Similarly, it could be just a coincidence that real household earnings peaked around 2000, when the Fed went into extreme “stimulation” mode (with a brief hiatus from 2005 to 2007), and have been in a bear market ever since. (See Figure 4)

It could be, but much like Sherlock Holmes, we’re not big believers in coincidences.

Have we gone “ex-“ cap ex? One of the more interesting views we see from time to time comes from Paradarch Advisors in their provocatively titled, Sex, Drugs, and Debt (who knew those three were connected!?!). In their most recent missive, they included some commentary that I thought was so good I should just relay it as is:

“The entire edifice of the 2009-2013 economic recovery has been built upon the foundation of wealth effects, i.e., higher stock prices. This was precisely the intent of the recovery’s bearded architect. The wealth created has certainly been enormous: Since bottom ticking 666 on March 6, 2009, the S&P 500 is now up roughly 208%. But like all spectacular bubbles, behind all of that newly created paper wealth stands a mountain of debt.

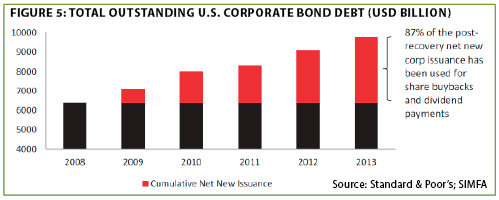

Since the beginning of 2009, total outstanding US corporate debt has increased by $3.376 trillion to a total of $9.766 trillion at year-end 2013. Of that $3.376 trillion increase in net issuance, nearly 87% has been used to fund share buybacks and dividend payments. In other words, the last five years have been one massive, market-wide leveraged buyout/dividend recapitalization.” (See Figure 5)

Paradarch further notes: “This situation has the potential to devolve into something extraordinarily dangerous…very little of the post-recovery corporate debt issuance has gone into either the building or purchase of productive assets, meaning a deeper long-term economic contraction is more likely whenever the (bear market) comes. The current situation seems perversely worse than the housing bubble, because at least after that iteration of the credit mania we were left with something tangible (i.e., cheaper houses).“

Lest you think this is an off-the-wall, renegade view, the iconic Jeremy Grantham was just interviewed in Fortune, where he echoed this same sentiment. Given that Mr. Grantham previously issued early warnings on both the tech-wreck and the housing-hosing, it’s wise to heed his words. (By the way, he feels the S&P 500 could rise another 25% before reprising those earlier obliterations.)

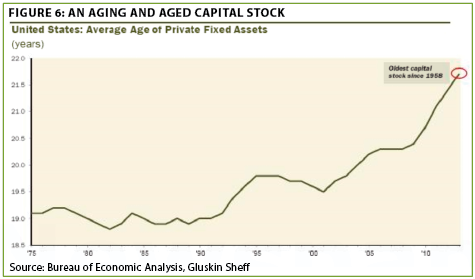

As with Charles Gave and Paradarch, Grantham wants to know where all of the long-term investing has gone, per this line from his Fortune interview: “The theory is that lower interest rates are supposed to spur capital spending, right? Then why is capital spending so weak at this stage of the cycle?” As you can see from the chart below, it’s hard to argue that over the last 15 years that we’ve been adequately investing in productive assets. (See Figure 6)

Could it be that by letting ourselves get caught up in a series of bubbles we’ve been engaging in a societal version of what the Austrian school of economics calls malinvestment? If the answer is yes, we should all be doing some serious thinking about future implications.

The Fatted Goose. Returning to this EVA’s opening theme about the close-but-never-quite-here-recovery, there are some very bright people who believe that we are on the cusp of the real deal. In at least one way, we think they may be right. There does seem to be growing evidence, as previously relayed in recent EVAs, that the labor market is tightening for the best workers. Yet, this raises another nettlesome question.

If the tens of millions of unemployed aren’t truly employable, is the Fed making a huge mistake by trying to force the jobless rate down from here? There is already evidence of wages rising in many sectors of the economy. It just may be that most of the workers companies want to hire are already on the job. Thus, as the Fed continues its long-running rendition of The Big Easy, it is also elevating the risk of creating the next asset bubble (and we would agree with Paradarch and Grantham that they already have) with little benefit to employment. If this logic is right, the Fed is basically trying to force a round peg into a square hole (or stuffing even more fat-soaked corn into an already gagging bird).

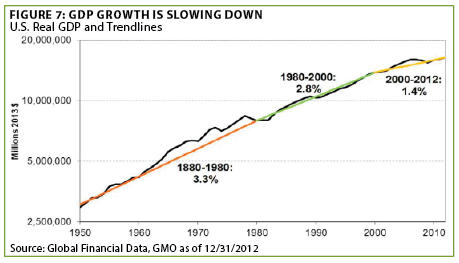

An EVA prediction from last summer and fall was that this would be the year of the taper. That is turning out to be the case, and it is likely to continue barring some catastrophe. But that doesn’t mean the Fed is inclined to alter its Zero Interest Rate Policy. In fact, Janet Yellen went out of her way earlier this week to assure markets that it won’t zap ZIRP anytime soon. The stock market predictably celebrated, but should those of us who would like to see America finally return to its former 3% growth rate feel the same way? (See Figure 7)

If the past 15 years in Europe and the US, and the last twenty-five in Japan, are any guide, the answer is a resounding no. The odds are high that our economy will remain burdened by growth-inhibiting monetary policies. In addition, it will continue to be negatively impacted by various other impediments, including a populace that is increasingly under-employed, an unwieldy and inscrutable tax code, a Rube Goldberg-like healthcare system, an increasingly ossified infrastructure, and a regulatory apparatus that congests the lungs of our economy, small businesses.

Consequently, the still-dominant consensus view that America’s economy is poised to single-handedly yank the world out of its lethargy is likely to be disappointed once again. We say this realizing there is some evidence that loan and money supply growth in the US are decisively turning up. This is a development we will watch very closely as it would almost certainly lead to money velocity acceleration in fairly short order. If so, the Fed won’t just need to tap the brakes but slam them on, and put out the drag chute as well.

While many would welcome a surge in velocity, we don’t think financial markets should be among the celebrants.They’ve benefited mightily from the paradigm of collapsing money turnover and constant liquidity injections. Even though sharply higher interest rates, at least on the shorter-term end, are what the economy needs to return to some kind of normal capitalism—and capital formation—weaning the stock market off of casino capitalism promises to be anything but pain-free. But did any responsible adult really believe there would be no pay-back for all these years of the Fed’s force-fed gains? If you do, you probably also believe foie gras grows on trees.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.