“As the world emerges from this enforced hibernation, investors have to choose between one of three potential outcomes.”

– Louis-Vincent Gave on May 14th

As the World Turns was one of the longest-running shows in television history. The soap opera aired for 54 years and compiled 61 Daytime Emmy Awards before ending its illustrious run in 2010. Several Tinseltown staples, including Meg Ryan, Julianne Moore, James Earl Jones, and William Fichtner, even had early-career roles on the program.

As with any good TV drama, conflict was central to the premise of the show. It doesn’t take much of a leap to draw parallels between what’s happening around the world and a daytime television drama. The emergence and spread of Covid-19 has been a central figure in the world’s dramatic narrative since early 2020. But there have been several other sub-plots as well, including protests in the United States and Hong Kong, worsening relations between the United States and China, unbridled stimulus by the US government, and a very dramatic rebound in the stock market.

This week, we are presenting an article from Evergreen Gavekal’s partner, Louis-Vincent Gave, on what’s in store for markets as the world reopens. The article was originally published on June 1st and at the time, Louis advocated that markets were moving towards what he dubbed “scenario #3.” Based on what’s happened since the article was published—a crescendo of intense speculation in the riskiest stocks with activity dominated by home-bound day traders—Louis has become increasingly cautious about the market on a near-term basis. (His concerns were reiterated and amplified during an internal research call with the joint Evergreen/Gavekal research team on Monday before markets swooned over the last two days.) With so much still unknown, the below provides a concise overview of three potential outcomes as the world (or at least the Northern Hemisphere) moves from forced hibernation into the summer.

A few weeks ago, I outlined three scenarios that could unfold as the world reopened for business. In scenario #1, the end of lockdowns was marked by a sharp rise in death rates and a rapid move back into confinement; my advice here was to sell everything except physical gold and gold mining stocks. In scenario #2, activity picked up but global growth was soft and inflation non-existent; for this, I advised owning US treasuries and US growth stocks. In scenario #3, the world economy ripped and inflation rose on a mix of pent-up demand, record-high budget deficits, low oil prices and unprecedented money printing; in this event, my advice was to buy cyclicals, financials and emerging markets, while underweighting the US dollar and US growth stocks.

At the time, markets pointed to scenario #2. Treasury inflation-protected securities, aka TIPS, were pricing in less than 1% annual US inflation for the next decade, US growth stocks such as tech and health care were making new highs, and despite massive issuance and money printing, 10-year treasuries were stuck in a tight trading range around 0.6%. Yet in the last few weeks, we have seen financials, materials and even that perennial three-legged donkey with fleas, energy, start to outperform. At the same time, beaten-up currencies like the Brazilian real, Mexican peso and even the Canadian dollar have recovered despite continued bad news (in Brazil, the pandemic seems to be spurring a political crisis). In short, it looks like the market is starting to tentatively position for scenario #3. This makes sense, but the rotation may soon face a number of challenges, namely:

Putting it all together, it seems likely that, at least until the election, China-bashing does not give rise to meaningful measures.

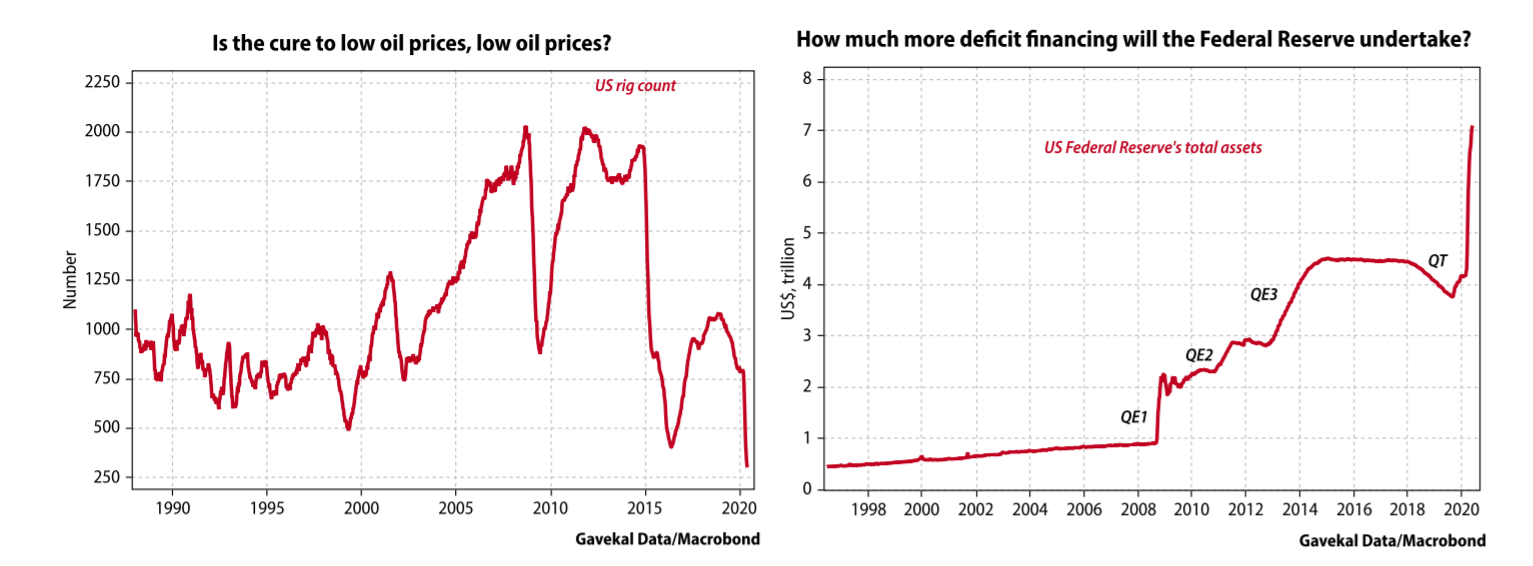

It seems that once again oil prices have shown themselves slave to the old adage that “the cure to a high oil price is a high oil price, just as the cure to a low oil price is a low oil price”. And obviously, if oil prices continue to rise, this could cause a profound shift in the investment environment.

Putting it all together, the markets are starting to shift from scenario #2 to scenario #3. Absent three disruptive developments—a fresh euro crisis (possible), a sharp worsening in US-China relations (also possible), a renewed collapse in oil prices (unlikely given production constraints) or a Fed that starts to taper its asset purchases much earlier than anyone expects (unlikely)—this movement makes sense.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.