Data on the health of the job market is one of the most important inputs for understanding the economy. It informs monetary policy, business confidence, consumer sentiment, and increasingly sits at the center of the debate about artificial intelligence: whether hiring is slowing, whether entry-level workers are being squeezed, and whether headline employment numbers are masking stress beneath the surface.

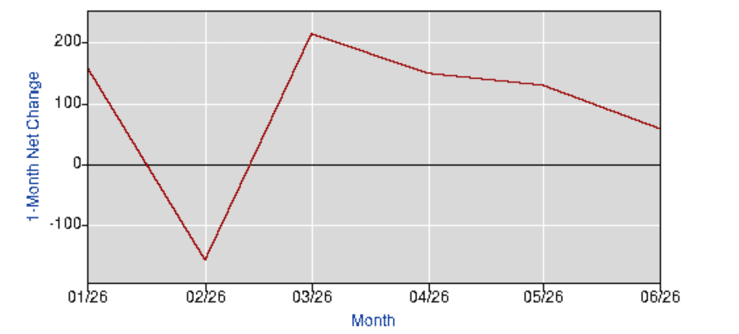

The June jobs report captured this tension. The U.S. economy added 57,000 nonfarm payroll jobs, and the unemployment rate ticked down to 4.2% from 4.3% in May. But the report was softer than the headlines suggested. Payroll growth came in below expectations of roughly 110,000 jobs, and April and May payroll gains were revised down by a combined 74,000. The household survey was also weaker: the labor force fell by 720,000, household employment fell by 507,000, and the number of people not in the labor force rose by 832,000. In other words, the unemployment rate improved partly because fewer people were counted in the labor force, not because employment surged.

Total Nonfarm Payroll Employment

The best description of the current market may be: low-hire, low-fire, high-anxiety. Job openings, hires, quits, and layoffs were all largely unchanged in the latest JOLTS report, and initial jobless claims remain low. This isn’t a labor market in distress. But it does look like one where finding a new job is becoming harder, especially for people who are unemployed, recently graduated, or trying to enter a new field.

The following five observations come from a narrower lens: actively hiring at high-growth technology businesses. This perspective is not representative of the entire workforce, but technology, AI, infrastructure, and growth companies are useful to watch because changes in productivity, hiring standards, compensation, and job design often show up there early.

Observation #1: Tech Workers are Worried

The anxiety in the technology sector is real. Workers are reading the same headlines as everyone else: layoffs, reorganizations, AI investment, cost discipline, and fewer obvious landing spots for people who leave or lose their roles.

Microsoft’s latest restructuring is one example. Reuters reported that Microsoft is cutting 4,800 jobs, including 3,200 roles tied to Xbox. Microsoft said the eliminated roles were not directly being replaced by AI, but it also acknowledged that AI is changing how work gets done.

Amazon provides another example. In January, the company said it would cut about 16,000 roles as part of an effort to reduce layers and remove bureaucracy. Separately, CEO Andy Jassy told employees that as Amazon rolls out more generative AI and agents, it will need fewer people for some jobs and more for others.

Are tech companies using AI as an excuse to reduce pandemic-era bloat, or is this the beginning of a structural shift in labor? The answer is probably both. Some cuts look like traditional operating discipline. But AI is also giving management teams a new way to rethink headcount. If one employee with AI tools can do work that previously required two or three people, the math on hiring changes.

Observation #2: AI is Driving Efficiencies, Not Replacement at Scale

AI is already changing work, but the evidence so far points more toward efficiency and role redesign than mass replacement across the economy.

The Census Bureau’s Business Trends and Outlook Survey shows that AI usage among U.S. businesses hovered between 17% and 20% from December 2025 through May 2026, with 20% to 23% expecting to use AI in the next six months. Adoption is much higher among larger firms: 37% of firms with at least 250 employees reported using AI.

That matches what many high-growth companies are seeing internally. AI helps people write, code, research, summarize, prospect, analyze, and automate repetitive workflows faster. The result is not always a layoff. Often, it is a higher output expectation. A lean team that previously needed an incremental headcount may now be expected to absorb more work with the same number of people.

This is the key distinction: AI is not replacing everyone at scale today, but it is changing the marginal hiring decision. They are likely to ask harder questions before adding headcount: Can this work be automated? Can an existing employee do it with AI tools? Can one person with AI do the work of a larger team?

Observation #3: Companies Want AI Experience

AI experience has quickly moved from “nice to have” to part of the basic hiring narrative in many roles. Hiring managers increasingly want to know whether a candidate can use AI tools to improve speed, quality, and output.

In practice, this means job seekers need an AI narrative. It is not enough to say, “I use ChatGPT.” Strong candidates must explain which tools they use, how those tools fit into their workflow, what outcomes improved, and where human judgment still matters.

Observation #4: Soft Skills Are Still in High Demand

One of the most overlooked effects of AI is that it may increase the value of human skills. As technical tasks become easier to automate or accelerate, the differentiator shifts toward judgment, communication, persuasion, taste, trust, and the ability to work well with others.

In hiring, this still matters enormously. Do people want to work with you? Can you sell an idea? Can you communicate clearly with executives, customers, and cross-functional partners? Can you handle ambiguity and build trust quickly? These are not secondary traits. They are increasingly becoming core differentiators.

Observation #5: For Many, Moonlighting Is Both a Necessity and a Viable Option

A constant theme among workers is that life is expensive. Even with wage gains, many households feel squeezed by housing, food, insurance, energy, childcare, and debt costs. The latest CPI report showed consumer prices up 4.2% over the 12 months ending in May, while average hourly earnings were up 3.5% over the year in June. Those are not perfectly matched real-wage measures, but they illustrate why many workers feel that nominal wage gains are not translating into financial comfort.

As a result, more workers are considering side income: consulting, advisory work, fractional roles, creator income, real estate, e-commerce, tutoring, contracting, or second jobs. AI makes this more viable by reducing the time required to draft, analyze, design, code, research, market, and administer small projects.

There is also a measurement issue worth acknowledging. The payroll survey counts jobs, not unique workers, so a person working two jobs can show up twice in nonfarm payroll employment. That can make job growth look somewhat stronger than the number of uniquely employed people would suggest. However, multiple jobholding does not appear to explain most of the current labor-market resilience. It is better understood as one example of the gap between headline labor data and the day-to-day experiences of workers in the economy.

The sustainability of this trend is unclear. AI may help workers maintain multiple income streams with less friction, making moonlighting more accepted and more productive. But it may also lead companies to adopt tighter productivity metrics, stricter conflict-of-interest rules, and more aggressive monitoring. AI could make side work easier in the short run while making employers more demanding over time.

Taken together, the job market appears stable, but slower and more uneven. AI does not seem to be replacing workers at scale in the aggregate data, but it is raising productivity expectations, changing hiring standards, and forcing companies to rethink headcount. For workers, the message is clear: AI fluency matters, but so dodoes judgment, communication, adaptability, and trust. The labor market is still healthy by many traditional measures, but beneath the surface, AI is changing how companies evaluate talent and productivity.

Disclosure: Evergreen Ventures is the alternative investment division of Evergreen Gavekal. Select Evergreen Ventures alternative investment vehicles have invested in certain RedBird Capital Partners-sponsored funds. This example is provided for illustrative purposes only and is not representative of all investments held by the Evergreen Ventures alternative investment vehicles. The views and opinions expressed in the interview are those of Gerry Cardinale and do not necessarily reflect the views of Evergreen or its affiliates. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed, and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.