Early in my investment career, one of my roles at the firm was in business development. Admittedly, I was young for the role and found myself seeking advice from anyone and everyone in the industry attempting to fast track my learning curve. One conversation I had with an exceptionally successful individual in our industry centered around a philosophical paradox. I asked this person, “Do you want to speak to a prospective client about financial concepts in a way that they can easily digest, or do you want to use industry jargon and complicated terminology so that you sound smart?” The guy thought for a minute and then said, “probably the latter.”

Reflecting on his advice, it was probably right for me at that point in my career. Being relatively young was a material handicap when trying to convince people they should trust Evergreen with their life savings. After 22 years in this industry, I am no longer under the yoke of inexperience. In addition, my 11- and 14-year sons are interested in what I do for a living and are constantly asking me to explain investing concepts to them. Frankly, our industry remains committed to the mantra that if you use big words, people will assume you know what you’re doing.

For this piece, I asked ChatGPT to find the financial jargon most commonly used by the media when talking about private and public market investing. Below, I will put my financial translation skills to the test as I try to explain, in my own words, the term or concept into lay terms. In addition, I will also attempt to explain why these terms matter to investors.

Internal Rate of Return (IRR)

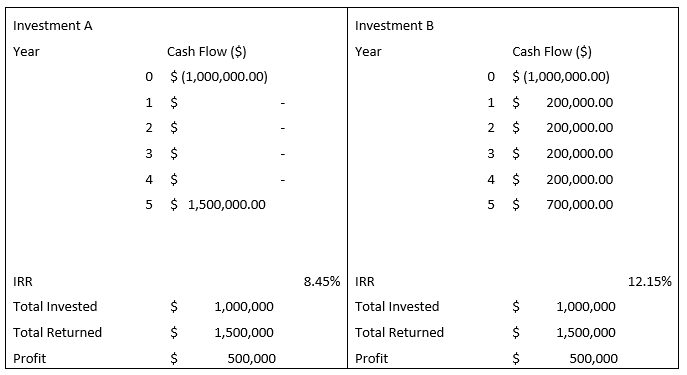

This is a way to measure the return you’ve earned on a specific investment. IRR calculations appear more frequently in the Venture Capital or Private Equity universe and are significantly impacted by the timing of when you receive the cash flow. Look at the below example…

In both examples you invested $1 million in year 0 and by year 5 you had received $1.5 million, a $500k profit. However, as you can see, Investment A and Investment B have much different IRRs. Even though the final profit is identical, Investment B produces a substantially higher IRR. The reason is simple: receiving cash earlier allows you to reinvest that money somewhere else, which improves the overall efficiency of your capital.

Another problem with IRR, albeit more subtle, is that it’s only calculated on the money invested, not the totality of money you commit. Imagine, you commit to investing $1 million in a venture capital firm. While you have committed $1 million, they are not obligated to invest your entire $1 million. They may only invest $500k out of your total committed amount of $1 million. While this might not sound like an issue at first glance, it means that 50% of your capital is never put to work and sits idle for the entirety of the fund’s lifetime. They could earn a strong IRR on the $500k they invest, but IRR does not account for the fact that half your money was never put to work.

Risk Adjusted Return

Let’s assume you’re a pioneer heading west along the legendary Oregon trail and you reach the Rocky Mountains. Your guide offers you the following two routes. You can go directly over the mountains via a dangerous mountain pass. If you survive the journey you will arrive on the other side in 3 days. Alternatively, there’s a much longer route that goes around the dangerous pass, but it takes you 3 weeks. This is quite similar to investing in the sense that if you’re trying to grow your money more quickly, you are likely to accept much higher risk. Conversely, the “slow and steady wins the race” approach reduces risk but also limits your return potential.

Part of what we do as professional investors is constantly weighing risks, probabilities, and rewards of different investment options, much like a pioneer would have done when considering their Rocky Mountain route. We are always trying to handicap if taking on more risk will bring with it an adequate increase in return for that risk. Taking on more risk is not necessarily a bad thing, but what’s imprudent is taking on more risk without the benefit of higher returns.

Liquidity Premium

Most investors typically invest primarily or even exclusively in public markets, i.e. stocks and bonds versus private funds. The reason is simple; investors embrace the fact that they can cash out of stocks and bonds at any time. Conversely, when you’re invested into a fund with a 10-year lifetime, your money is tied up for the lifetime of the fund. Historically, however, public markets have returned less than their private market counterparts. This means many investors often forego earning better returns for the sake of immediate access to their capital. For some investors, this is a necessity. They need full access to their money and cannot afford to have it tied up in longer commitment investments. Other investors, however, can and often should allocate a portion of their portfolios into investments with longer life cycles, to capture greater return potential.

Institutional Investors

This is a fancy term for large entities that invest large pools of money. The simplest example would be a college endowment. Harvard’s endowment manages over $50 billion in assets. Typically, these institutions have large in-house teams of dedicated investment professionals who have different areas of expertise. Another example of an institution or “professional investor” would be a mutual fund. The institutional investors are sometimes referred to as “smart money.” Perhaps, it’s time to drop that moniker as only 10% of mutual fund managers beat the stock market over a 10-year time horizon. These institutional investors have a handicap that individual investors are not burdened with. They are forced to stay within rigid investment guidelines when they are investing. Most, if not all, of these large college endowments investment decisions are governed by certain investment policy statements. Possible examples of this are a guideline that states that they can only invest in ultra-safe bonds or that they must allocate a certain amount of the endowment to green energy initiatives. Mutual fund managers who run a technology fund cannot suddenly decide to invest in energy companies, no matter how attractive the investment appears to be. Investors who are unconstrained by these limitations can pivot and adapt their portfolios based on purely on market opportunities instead of pre-determined guidelines.

Duration

This is a concept that relates to how short-term and long-term bonds are impacted by changes in interest rates. A way to think about this concept is to imagine two identical apartments buildings in the same city. One building is comprised completely of tenants that have 1-year leases. In the second building, all tenants have signed 20-year leases. Now, let’s imagine the economy goes into a severe and prolonged recession. Which building would you rather own? The answer is the building where tenants have signed 20-year leases. The rents these tenants are paying are locked in for a very long time. Conversely, the building with all 1-year tenants is going to suffer as the 1-year rents expire. The owner will likely have to drop rents significantly in response to the economic recession to attract tenants.

Consider the inverse scenario. Instead of an economic downturn imagine the economy is surging. Which building would you want to own now? The answer is the building with all 1-year tenants, and the reason is you will be able to greatly increase the rents you charge as the 1-year tenant’s lease expires. The building with 20-year tenants cannot change its’ tenant’s rent as they are locked into long-term leases. This analogy is essentially how bond prices behave. Short-term bonds are like buildings with short leases—they can adjust quickly when interest rates change. Long-term bonds are like buildings with long leases—the income is locked in, which makes them more sensitive when the interest-rate environment shifts.

J-Curve

This is a term commonly used when discussing the lifecycle and performance of venture capital investments in start-ups. Imagine you spot a house that’s a “fixer-upper” and decide to buy it, improve it, and then sell it. In terms of cash flow, you will have an initial outlay to purchase the home. Then you will have additional costs for materials and labor to make the improvements. In the early stages of the project, when the house is taken down to the studs and being ripped apart, the investment is likely worth less than what you paid for it. However, if things go according to plan, and you successfully complete the improvements, you stand to sell the house at a handsome profit.

This initial decline in value followed by longer-term appreciation is the concept of the J-curve. In the world of venture capital, most companies will decline in the early years of a funds lifecycle as they increase their spending to fund what they hope will be substantial future profits.

Volatility

The word volatility is often mistakenly interpreted to mean risk. This is not wholly accurate as risk implies loss or negative returns. Some stocks that have been very good over the long run have been very volatile; it just turns out the cumulative turbulence has been more positive volatility than negative.

Investors should also think about volatility as a relative term; meaning, what are you comparing something to when assessing its volatility? If you compare the daily fluctuation of a bond account to a stock account, you’re going to conclude stocks are volatile. This is neither bad nor good. It simply states that the range of outcomes in one scenario is wider for certain investments than others.

Investors are quite fond of investments that display positive volatility (going up rapidly compared to peers) but are rapidly discouraged as the investment enters the realm of negative volatility. Said another way, investors frequently find it very difficult to endure the wild swings of a volatile investment, both up and down, even if the net long term outcome is still very positive.

Alpha

Simply put, if your portfolio returns 13% and the stock market itself returns 10% you have produced 3% of alpha. Think of it as excess return where investors do better than the market itself. One tricky question when evaluating alpha is whether alpha was driven by skill or luck? Investors who consistently produce better returns than the market possess strategic or tactical skill. Knowing whether a manager made a lucky investment or has a repeatable process for producing superior returns is a challenging exercise even for investment professionals.

Alpha is harder to find in areas of the market that are crowded and well understood. Finding the next Amazon, Nvidia, or Microsoft is extremely difficult. It’s like an easter egg hunt with too many kids; the eggs get scooped up quickly. Other less mainstream investments are often better areas to find alpha.

Beta

I heard an analogy once that Beta is like the force of the wind pushing a sailboat, while alpha is the skill of the sailor in the sailboat.

A more quantitative description says that a stock with a beta of “1” moves in unison with the stock market. A stock can have a beta of >1 or <1. Stocks with a beta >1 have more volatility than the stock market, while stocks with a beta <1 has less volatility than the overall market.

Spreads

This term relates to how bonds of differing credit trade relative to each other. Imagine you have two friends, one who is very responsible and has a stable job and another friend who can’t keep a job and struggles to pay their bills. If they both came to you for loan, it is unlikely you would charge them the same rate of interest, since your confidence in one of them is far higher than in the other. The same concept is true of bond investing. Bonds that are deemed safer pay lenders lower interest rates than loans that are deemed more risky. The difference in interest rates between the safer and risky borrowers is known as the spread. In times of economic prosperity, the spreads narrow as people are more cavalier about the loans they make. However, in worse economic times, the spread widens dramatically as investors must be financially enticed to take on additional risk.

Leverage

Financial leverage is the concept of borrowing money to make a larger investment than your own capital alone would allow. Most people are already familiar with leverage, even if they don’t think of it that way. A mortgage is simply leverage applied to real estate. Instead of paying cash for a home, you put down a portion of the purchase price and borrow the rest, allowing you to acquire a much larger asset.

If the value of the home rises, you benefit from the appreciation on the entire property, not just the portion you initially paid for it. In that sense, leverage can enhance returns because a relatively small amount of equity participates in the full value of the investment.

However, leverage cuts both ways. Just as it can amplify gains, it can also magnify losses if the investment declines in value. When borrowed money is involved, the obligation to repay that debt doesn’t go away simply because the investment performs poorly.

Leverage itself isn’t good or bad. It’s simply a tool. Used responsibly, it can enhance an investment outcome. Used improperly, it can accelerate and magnify financial loss. The key isn’t avoiding leverage altogether, but understanding when and how to use it wisely.

Summary

I hope that casual investors found this piece informative. While I elected to use my own content and language to decipher these terms, the presence of many AI-powered engines like ChatGPT or Gemini are fantastic resources for translating complicated terms or concepts into simple terms. Understanding these terms is a fantastic start for furthering investor acumen. And there are second and third order effects that accompanies these terms. To give an example, I explained the concept of volatility, but understanding the concept and determining what volatility you should accept as an investor is a far more complicated decision. It’s my hope that after reading this piece, investors can be better equipped to ask informed questions and make quality decisions regarding their finances.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.