“When the time comes to buy, you won’t want to.”

– Walter Deemer, renowned market technician

“The stock market is manic depressive.”

– Warren Buffett

“The investment-grade bond market is broken. This is as ugly as I can remember it.”

– BofA strategist, Hans Mikkelson

The fact of the matter is that the last half-dozen years have been exceedingly difficult for investors who like to buy assets, such as stocks, on sale. Instead, since at least 2014, it’s been a case of the US equity market jaggedly marching to higher and higher levels. The sell-offs were generally shallow and consistently very short-lived. To make good money during this period, a value-oriented investor needed to go against her or his basic investment DNA and mutate into a momentum player. In other words, the imperative was to go-with-the-flow—and, especially, buy aggressively into any dip—rather than patiently wait for a return to what was even a normal, much less underpriced, value for the stock market.

My wife likes to say that “normal” is only a setting on a washing machine. When it comes to assessing what that represents with stocks, her point is extremely well-taken. There are myriad ways to determine whether the market is cheap, dear, or in-between. You can almost always find one to justify your view - bullish, bearish, or neutral.

With that disclaimer, I do believe the bulk of market valuation measures were consistently indicating a very expensive S&P 500 for most of the past six years EXCEPT for those based on interest rates and/or projected (usually, too high) earnings. As I’m sure you heard or read as often as I did, the dominant bullish mindset since 2014 was that low rates meant stocks should trade at lofty valuations. And they certainly complied. The US stock market produced fabulous returns during most of this timeframe despite those who (like me) noted that the low rates were a function of poor economic growth prospects. It’s simply a fact that what was the longest-running bull market of all time coincided with the weakest economic expansion since WWII. It’s also nearly a fact that this extended but sub-par upcycle for the economy is now history. In other words, a recession is virtually certain in the US and for world at large.

In record-breaking time, financial markets have gone from sheer euphoria to utter despair. Bubble 3.0, which seemed like it would only constantly inflate, despite threats from multiple directions, finally met its pin prick—a once innocuous-seeming virus. It was an outbreak that the market did its very best to ignore until the economic damage became overwhelming and inescapable.

Now, with the S&P down nearly 32%, the Dow off 35.1% and small-caps (long an object of criticism in these pages) having crashed 40.5%, it is tempting to say that stocks are a screaming buy. To which I would add, sort of. Yes, I know that’s pretty wimpy but please allow me to explain.

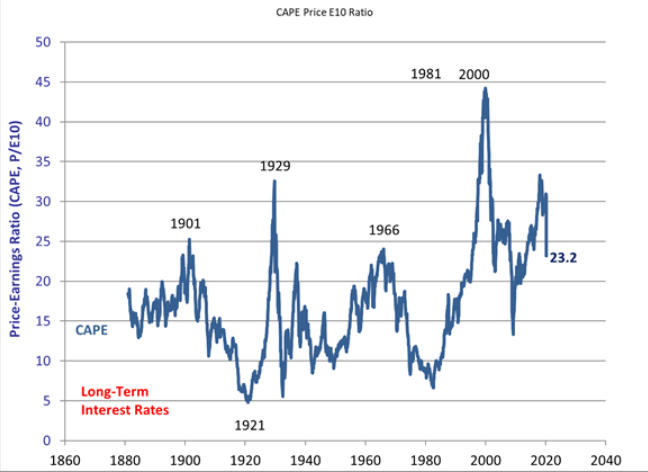

First of all, the S&P 500 itself remains on the pricey side despite the big mark-down. The Shiller P/E (also known as the Cyclically Adjusted P/E, or CAPE, shown below), smooths out earnings over a 10-year period to avoid distortions from either recessions or long expansions. On this basis (and many others, by the way, like price-to-sales) the US stock market is no screaming deal.

Source: Robert Shiller

Using an earnings normalization process is particularly important presently, because profits for almost all industries are in the process of falling off a cliff. Consequently, the P/E may spike even with prices down because the “E” in the P/E may go down faster than the “P”. One could realistically make the case that the Shiller P/E is actually too low (i.e., stocks are even more expensive because there is not a single recession picked up in the trailing 10 years for the first time ever). But, for sure, that is in the process of changing as a contraction finally takes hold.

Per numerous past EVAs, bear markets that coincide with recessions tend to be nasty affairs. We are seeing that play out right now. The excessive amount of leverage employed during the artificially pumped-up years, due to the Fed’s long war on interest rates, are now coming back to haunt investors with a vengeance. It’s been bad in the stock market, but actually much worse in the so-called “credit markets”.

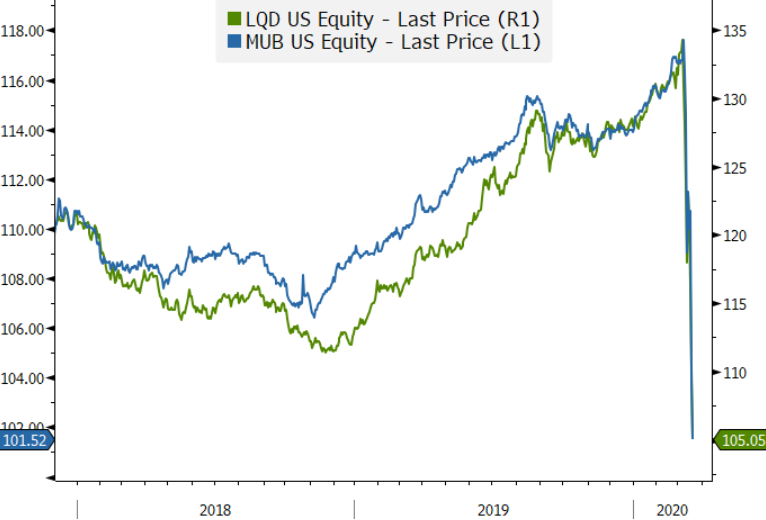

To prove this point, let’s look at some charts of securities which fall under the credit market category (credit instruments are basically bonds and related securities such as mortgages, preferred stocks and the funds that invest in them).

If you’re frustrated with how your blended stock/bond portfolio has been doing, these charts explain why. When even high-grade corporate and municipal bonds have produced losses of 17.5% and 10.5%, respectively, as they have this year, it makes balanced portfolio returns look pretty awful unless the bond component was strictly in US treasuries.

LQD = High-Grade Corporate Bond ETF and MUB = Municipal Bond ETF

Source: Bloomberg, Evergreen Gavekal

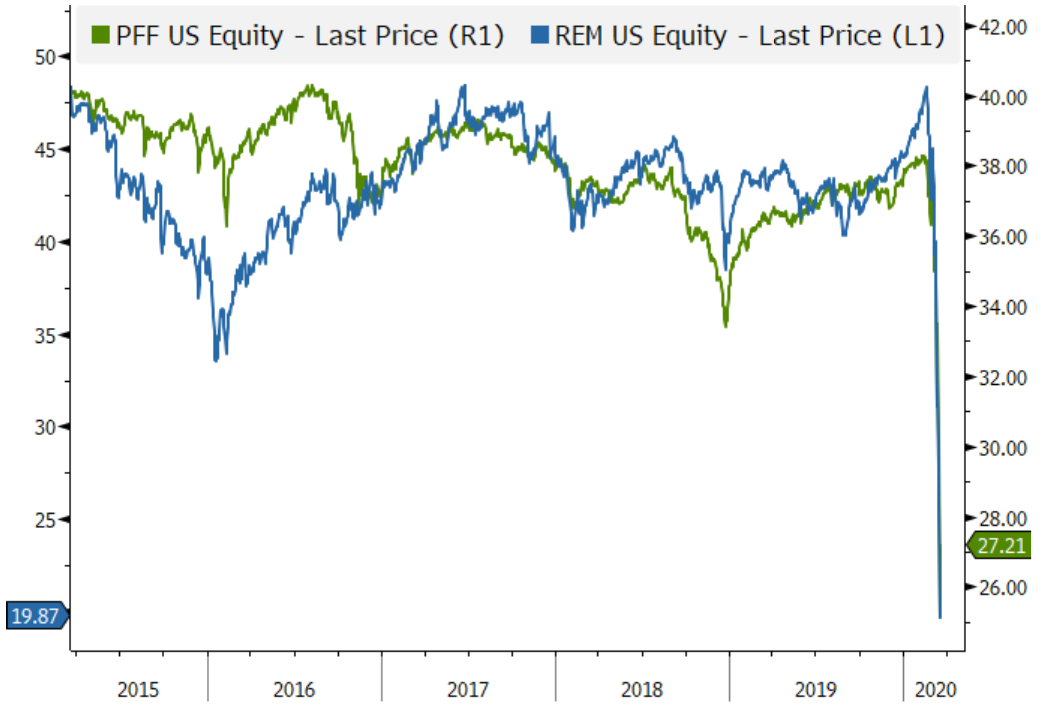

Then, let’s look at preferred stocks and funds that invest in those entities owning high-grade mortgages on a leveraged basis. As you can see, it’s been a total bloodbath.

PFF = Preferred Stock ETF and REM = Residential Mortgage Trust REIT

Source: Bloomberg, Evergreen Gavekal

Of course, if you really want to see carnage, MLPs, long favored by this newsletter (with caveats over the last six weeks due to our rising coronavirus concerns) will show you enough gore to qualify as a killing scene in a Tarantino movie. This is despite the powerful rally seen towards the end of this week.

AMJ = MLP ETF

Source: Bloomberg, Evergreen Gavekal

It’s also fair to note that many sectors in the US market have been nuked and now offer extraordinary recovery potential. These include pretty much any economically sensitive company and financials like banks and insurance companies. There is one large life insurer with an admirable earnings track record, selling at a P/E of 4.4 and yielding nearly 10%. The knock on any insurer is that with interest rates collapsing, they will be hard-pressed to earn anything on their critical bond portfolios. And that leads me to the big buy idea…

In a word, yield. Because of what I believe is a global margin call, where securities are being involuntarily sold en masse, the bargains in areas such as those mentioned above are a total flash-back to 2008. To be able to get a yield over 7% on preferred stocks, also selling at a discount from par value (providing capital gain potential) when treasury rates are around 1% is remarkable. Yields on the mortgage-backed security players included in the Mortgage Real Estate Trust ETF (REM) shown above are now in the upper teens. (Realize that although they own very safe securities, they also employ large amounts of leverage.)

The reason why I believe this entire class of yield securities has been mercilessly bludgeoned is that they are—or, at least, were—owned by heavily-levered hedge funds. Many of these have reportedly lost control of their own destiny and there are rumors of one or more of the big ones in this field doing a Titanic. As a result, there are massive sellers out there of almost every yield security, even, incredibly, federally-insured CDs.

Back in 2009, legendary money manager Jeremy Grantham penned a piece called “Reinvesting While Terrified”. It’s publication almost perfectly coincided with the March 2009 bottom. Interestingly, as we wrote extensively in those days, yield securities were far cheaper than even the battered stock market was back then. We are seeing the same thing today – though not to as great an extreme as in 2008 when it was briefly possible to get 13% even on high-grade preferred stocks and corporate bonds.

Could we be headed to those kinds of levels? In other words, could ETFs like LQD (investment-grade corporate bonds) and PFF (preferred stocks) soon be yielding in double digits? It’s certainly possible but I doubt it for the reasons to be articulated shortly. (This yield explosion gives banks and insurance companies a stellar opportunity to capture high cash flows for years to come…if they have the guts to buy into the selling tsunami.)

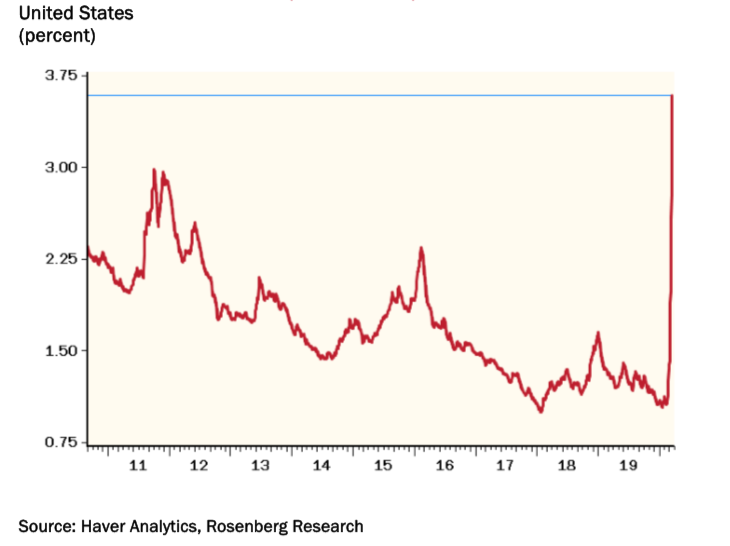

VERY long-time EVA readers may recall that this newsletter repeatedly urged the Fed and the Treasury to create both a TARP-type program in late 2008. My further vehement suggestion was that they should buy corporate bonds and non-government guaranteed mortgages in large enough quantities to bring down credit spreads (the difference between what Treasury and corporate bonds yield). As you can see below, spreads have again gone postal, reflecting the above referenced global margin call.

Corporate Junk Bond Spreads

Investment Grade Corporate Bond Spreads

This is an extremely dangerous development. It means that even US high-grade borrowers are being forced to pay exorbitant interest rates at a time when their revenues are often imploding. This may be why a long list of companies are frantically drawing down credit lines.

This needs to be stopped—NOW. Back in 2009, the government belatedly did TARP (more on that in a bit) but whiffed on the chance to buy corporate bonds. As I wrote at the time, this could have immediately stopped the meltdown in asset prices in those days. Instead, it did QE 1 and merely bought US government bonds. That move kind of worked but with a big lag and it didn’t produce another huge benefit—a tax-payer windfall.

Had the Fed stepped up in the fall of 2008 and bought into 1932-type pricing of corporate bonds and preferred stocks, they would have eventually realized monster profits for the US treasury. (Admittedly, the Fed would have had to come up with a novel scheme to get around restrictions on such an emergency response but that has never stopped it before—like by its de facto monetization* of US government deficits). Thus, it would both have arrested the panic and created enormous profits once spreads came back down (driving up the value of its fire-sale purchases).

But, sadly, it missed the chance. Now, though, it’s got another one. Many others, besides yours truly, are calling for the Fed to do exactly this, including the influential Paul McCulley, former CIO of Pimco and close confidant of Ben Bernanke, as well as other former senior Fed officials. In my opinion, it’s just a matter of time—and probably not much at that—before they fire this powerful bazooka. It is likely to be infinitely more effective than the Fed’s recent panicky rate cuts to near zero which provide little benefit and further punished savers.

But that’s not all: I also believe the government, likely the Treasury, is vectoring to launch a new version of TARP. In case you’ve forgotten, that stood for, in 2008, Troubled Asset Relief Program. It was beyond controversial—way, way beyond—when it was unveiled. As usual, I was in the minority at the time, pleading for this to be done and for the government to do again what it had done in the early 1980s when it rescued Chrysler. In that first clever move (I know, incredible for the government) it took warrants (basically, an equity stake in the borrowing entity) in addition to a high, but not punitive, interest rate. When Lee Iacocca’s company recovered, it repaid all of the loans and its stock exploded to the upside, earning the Treasury staggering profits at the time (back when a billion was a lot of money).

Fortunately, at least some senior Treasury officials remembered that shining success story when the entire US financial system was drain-circling in late-2008. To intense caterwauling, hundreds of billions were lent to banks and insurance companies at a lucrative interest rate AND with warrants attached. Because financial stocks were so annihilated at the time, the government received going-out of-business exercise prices (basically, the price it was able to buy at in the future). Once again, it made a killing. (Astute readers will realize this is often what Warren Buffett does: Make a big loan to a large but capital short company in return for a juicy interest rate and an equity kicker.)

The time is ripe for that today but across industries, not just with financials (the government also used this approach with the automakers in 2009, scoring another whopping profit). Airlines, restaurant chains, hotels, energy, and, of course, Boeing are in desperate need of emergency financing. Once again, their stock prices have been crushed, offering the Treasury vast upside during a recovery.

Taking an equity slice (the warrants) would also defuse the legitimate criticism being voiced today about bailing out companies that frittered away billions via over-priced buybacks. As almost every EVA reader knows, this has been my biggest pet peeve over the last five years, along with reckless central bank policies. The general public is finally waking up to what a scam it has been. Accordingly, this is a way to give taxpayers a windfall gain due to the foolishness and avarice of the management teams that leveraged up their companies to repurchase shares and, of course, enhance their stock options. (Claw-backs of prior executive windfalls from their option programs, should, in many cases, also be pursued.)

Unfortunately, there has been almost no discussion of resurrecting TARP—that is, until yesterday when President Trump’s senior economic adviser, Larry Kudlow, floated the idea of combining bail-out loans with an equity kicker for the Treasury. He’s just one voice but a very influential one. Do I think something like this is coming? Absolutely! Policymakers would be crazy not to do something along these lines and even I don’t think they are that insane.

In fact, I believe we will soon see the twin bazookas of the Fed buying enormous amounts of corporate bonds and TARP 2.0. The former effort is almost sure to materially bring down credit spreads (likely through some kind of deal with the Treasury to get around restrictions or perhaps with a special Congressional authorization) while the latter will save vital companies and industries from widespread bankruptcies, avoiding mass layoffs. Moreover, the government will be even better positioned (by firing both bazookas) to realize a gusher of profits once the worst of the coronavirus passes. This will help fund all the transfer payments to individuals and small businesses being proposed, some of which are desperately needed and some of which are silly (they can keep my $1,000, thank you very much).

To emphasize for clarity, this is the time to buy, especially those market segments exceedingly pummeled by the most intense bout of involuntary liquidation seen since the darkest days of the Global Financial Crisis. This is truly great news for millions of Boomers whose retirement, future or present tense, was imperiled by the systematic eradication of interest rate perpetrated by central banks over the last ten years. The yields available now are the kinds people can actually live on like 6% to 8%, or even higher.

As usual, the best laid plans of the planet’s central bankers blew up in their smug collective faces. And, as these pages have long warned, it was due to encouraging investors to leverage up and move into assets much riskier than they should have been playing with. But, it’s so cool that their latest blunder is actually a massive gift to investors willing to step in and capitalize on the carnage. It will be even cooler if taxpayers, most of whom are the same cohort, can also come out as big winners. So, lock-down your fears as tightly as Seattle is right now and be a buyer – or support your money-manager who is doing that for you…hopefully. (If not, contact Evergreen ASAP!)

This strategy assumes, of course, the current powers that be don’t let a liquidity crisis turn into a solvency crisis. I’m betting—a lot—they won’t, which is some much-needed good news for those brave enough to buy into the recent carnage.

Please allow me to conclude this important EVA by emphasizing the twin bazooka approach I’m advocating for is not what I wanted to see happen. It was the same in 2008. The half-dozen or so EVA readers who were recipients of this newsletter back in 2005, when it incepted, will recall how often I railed against the insanity during those years in the housing and mortgage markets. It was truly my overarching theme from mid-2005 until the home-loan crash began in the summer of 2007. It infuriated me that the Fed stood haplessly by as that bubble inflated to immense proportions. Former Fed-Head Alan Greenspan even encouraged homeowners to shift into adjustable rate mortgages which magnified their exposure to rising rates (he really said this and it was at a time when the Fed was hiking!).

It took over a year for the housing meltdown to bring the global economy and financial system to the brink of failure (unlike this time when the collapse has happened almost overnight). During that 15- month lag before the you-know-what hit the fan, the Fed was, once again, clueless. Mr. Greenspan’s successor, Ben Bernanke, even stated that the sub-prime lending crisis was contained in the summer of 2008, words that have lived in infamy.

Once major financial institutions began their serial collapse in the late summer of 2008, I began to plead to anyone who would read or listen (which by that time was maybe a few hundred souls, who felt as helpless as I did) that a TARP-time plan was needed. Some supported the idea but others told me I was crazy or, even worse, that I was a socialist. It was then that I also proposed the government borrow (not print) one trillion to buy into the collapsing credit markets. It revolted me to have to make these suggestions but then, as now, the objective is to save the system not to moralize. The fact that the Fed not only stood by but actively and repeatedly enabled Bubble 3.0 is irrelevant for now.

Speed is of the essence. For one thing, the longer the market panic goes on the more retail investors will panic and bail out at depressed prices, locking in losses they may never recover from. Financial institutions will be threated by the sudden plunge in the value of their assets and, of course, soaring bad loans. Big employers and the backbone of America, small businesses, are at grave risk of widespread failure. The chain reaction is already beginning to get to the critical mass point. But we’re not there yet and I’m encouraged that today the Fed announced they are also buying short-term municipal bonds.

Back in 2008, we followed a plan to basically “shake hands with the government”, as the former Bond King Bill Gross suggested. In other words, we went where the Feds were injecting hundreds of billions (these days it takes trillions) and bought the securities that would benefit from their stabilization efforts. We are doing the same thing today.

As we wrote during those equally fear-wracked days of late-2008 and early-2009, you either believe the system will survive and you invest accordingly or you put your wealth in cash and gold. It’s time for that kind of calculus again. We believe Winston’s Churchill’s wise observation about the US will be once more validated: “You can count on the Americans to do the right thing—once they’ve tried everything else.”

Technical note: While it seems somewhat silly to bring this up given what’s happening in the world these days, I was embarrassed to be told by our usual editor that I had made a dumb mistake in last week’s EVA. I referred to human-caused as “anthropomorphic”when I should have used the term “anthropogenic”. My only excuse is that, as I wrote last week, I had to revise that issue on a rush basis and didn’t have a chance to run it by our eagle-eyed editor. Please accept my apologies.

*Debt monetization’s occur when a central bank buys its own government’s bonds with fabricated money.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.