“We may well be in a recession. But I would point to the difference between this and a normal recession. There is nothing fundamentally wrong with our economy. Quite the contrary. We are starting from a very strong position…The Federal Reserve is working hard to support you now. Our policies will be very important when the recovery does come, to make that recovery as strong as possible.”

– Jerome Powell, Fed Chairman

At the end of last week, David Hay outlined his case that the Fed should – and would – buy enormous amounts of corporate bonds. He also suggested that the US Treasury might resurrect TARP (also known as the Troubled Asset Relief Program) to stabilize the economy. Evidently Fed-head Jerome Powell is a close follower of Evergreen’s newsletter! On Monday, the Federal Reserve pulled out its big gun—more like a howitzer than a bazooka in its impact on the bond market! The Fed stated it is poised to buy enough investment-grade corporate debt to bring down credit spreads in a major way. It has moved swiftly and aggressively to stabilize the municipal bond market, as well.

These promising moves by the Fed additionally relaxed accounting rules for banks while launching a suite of programs designed to take risk off companies’ balance sheets. Notably, the Fed has been able to push prices up, and yields/spreads down (and the Fed may not have even started buying bonds yet!) This is critical because the recent fire sale has driven up corporate capital costs steeply, further pressuring an already beleaguered private sector.

Unfortunately, as many who keep an eagle-eye on the stock market are likely aware, the Fed’s decision did little to comfort markets on Monday, as the S&P 500 ended the session down -2.9%. This marked the third time in as many weeks that the Fed’s actions failed to sooth investors’ confidence. (Its decision to step-down interest rates to 0.0-0.25% over the last couple of weeks also rattled – rather than reassured – markets.) However, the next three days were entirely different story. In fact, on Tuesday US equity markets registered the strongest one-day rebound in history, a rally that continued onto Wednesday and Thursday. To attribute the snapback entirely to the Fed’s move would be disingenuous, as a $2 trillion stimulus package– yet another heavy gun in the USA’s economic artillery—began to be priced in.

What remains unclear is if launching these cannons simultaneously will create a permanent backstop for what had become a painfully sharp asset price crash due to the unprecedented COVID-19 crisis. If the impact of the novel coronavirus continues to derail the global economy for an extended period of time, it’s very feasible that we could revisit stock market lows over the coming weeks and months. (Which, as a side-note, is a key reason why we believe all readers should have a strong money manager at this time to help navigate you through volatile markets. If you, your loved ones, or friends, need a trusted money manager, please reach out to us.)

In this week’s EVA, we are presenting an article from our partner, Louis-Vincent Gave, on themes that investors with a long-term investment horizon should consider. (As another side note, we believe that every investor should be making investment decisions with a long-term mindset right now, especially given the extreme price swings). Many of the ideas Louis presents are also echoed in our accompanying “Likes/Dislikes” section. One theme that Louis fails to mention but that we believe should be vital tools in every investor’s toolkit are gold and gold-mining stocks. For those who want to hear more from Louis, we will be running a Special Edition EVA next week, where Louis-Vincent Gave and Tyler Hay, Evergreen’s CEO, sit down for an interesting discussion on all that’s happening in the markets. Until then, please stay safe and healthy.

As they survey the shattered remnants of the past decade’s bull market, investors are inevitably asking: what happens next? Not next week, and not next month, but what happens for the coming years? Specifically, did this bear market mark the end of an era and, in time, the start of a new one? Or do we still live in a MAGA (Microsoft, Apple, Google, Amazon) era?

In a recent paper, Charles* argued that the Covid-19 outbreak is paving the way for a universal basic income funded by MMT (aka the magic money tree) and that these two profound changes will upend the investment environment. This view leads me back to the most trusty Gavekal framework for linking the macro environment to the investment landscape, namely the Four Quadrants.

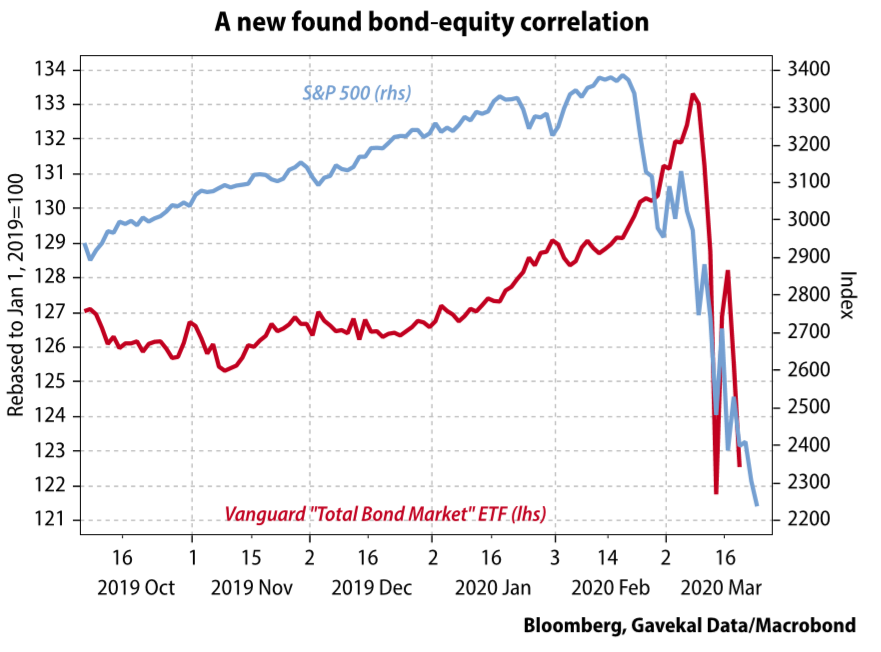

For the past 30 years or so, the world has basically alternated between disinflationary booms and busts, which makes inherent sense as the dominant force of capitalism is deflation. Every entrepreneur, everywhere around the world, is always trying to produce more with less. And in a disinflationary world, asset allocation is a breeze: one needs to own government bonds (to hedge the risk of a deflationary bust) and equities (to participate in any deflationary boom). And best yet: in a disinflationary world, not only do bonds and equities both have the wind at their back, but the two main asset classes have in bad times been negatively correlated. So, happiness all around.

In recent weeks, of course, there has been little happiness. Instead of having the wind at their back, both bonds and equities have faced massive headwinds. And instead of being negatively correlated, it seems that, all of a sudden, bonds and equities have become positively correlated, thereby wreaking havoc for risk-parity funds whose starting assumption is a negative correlation between the two main asset classes.

This brings me back to the question of whether the winners on the other side of this bear market will be different from those in the previous bull market? Or whether this bear market, like so many of its predecessors, actually marks the start of a new investment environment, and thus new leadership?

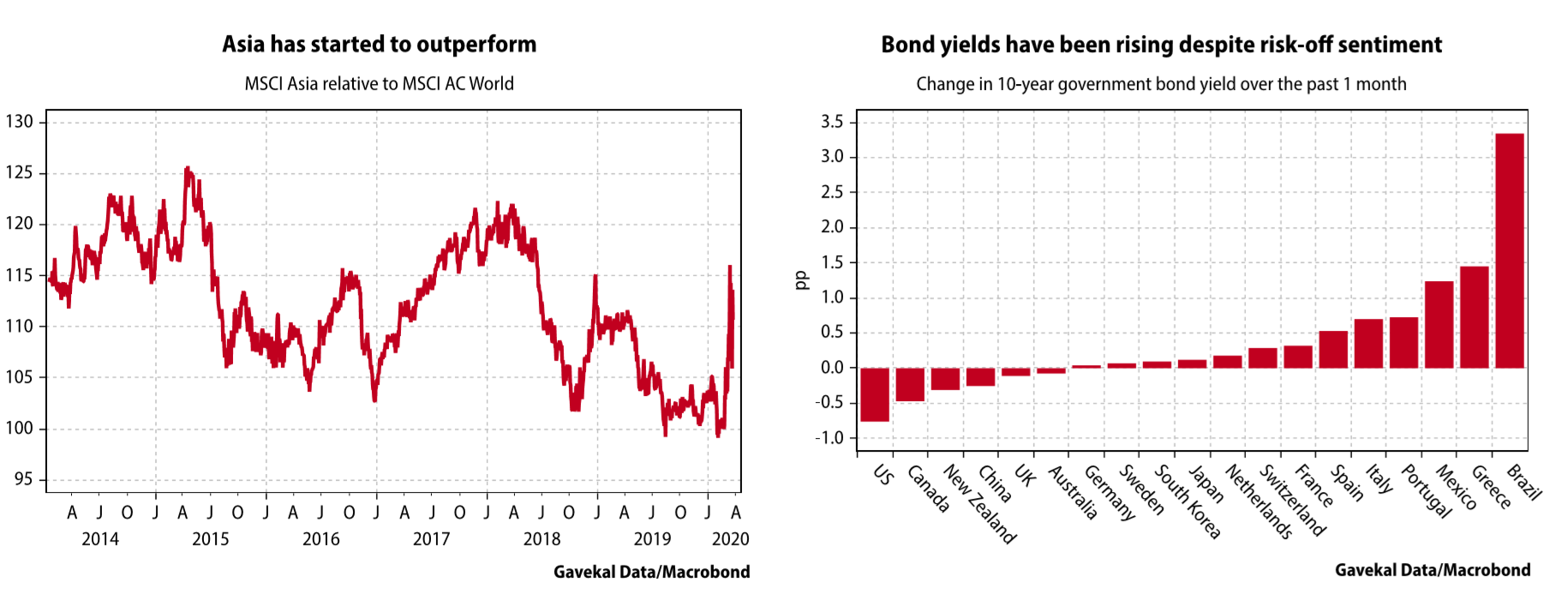

Now talking of leadership, it seems that the world can be split roughly into two zones. The first is Asia, where Covid-19 emerged. There, policymakers responded to the disease fairly early and successfully by closing schools, universities and gathering places, and even quarantining entire regions. Economies have been negatively impacted but not brought to a halt. In cities like Hong Kong, the situation was eased by a high share of the population— even lower middle-class office workers—employing domestic helpers; schools could be shut yet parents could still work. To date, the fiscal and monetary stimulus in Asia has been fairly modest.

In Europe and North America, by contrast, the disease was imported and allowed to spread until panicked policymakers decided to basically shut down their economies. Having undertaken these measures, European and North American governments have been forced to embrace versions of the universal basic income and MMT described by Charles.

So, it has been a case of different policy responses, with different outcomes. Unsurprisingly, the market seems to like the Asian way more than the Western approach, as shown in the left-hand chart below. And it’s not just Asian equities that have lately been outperforming. Through this crisis, the few ports in the storm for investors have included US treasuries and bonds issued by the Chinese government and high quality corporates in that country (see right-hand chart below). Almost any other asset has delivered negative returns over the past month for a US dollar-based investor.

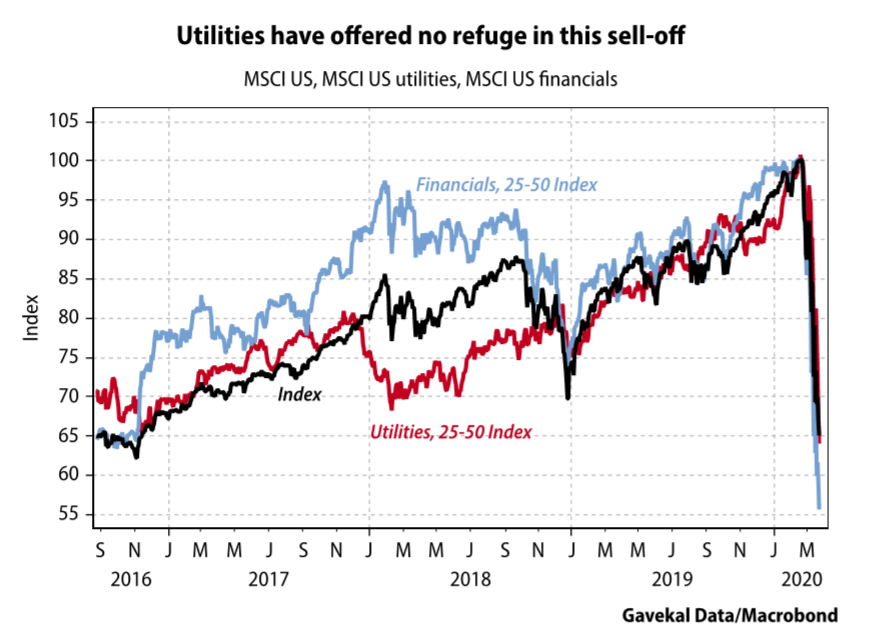

Even traditional safe-havens like US utilities have been complete duds in this sell-off, faring almost as poorly as the broader benchmark.

This pullback in utilities wrong-footed me as I entered the crisis with decent exposure, thinking they would provide shelter from the storm and an offset to financials. I.e. if yields rose, financials would do well, and if yields fell, utilities would do well; a value-oriented, risk-parity strategy of sorts. Instead, yields went all over the place and both utilities and financials have cratered!

But with hindsight, this may all make sense. If the end result is, as Charles believes, a universal basic income and MMT in Western economies, which in turn leads to currency debasement and inflation, then US utilities are probably a bad place for shelter: a likely rise in long rates will compress earnings multiples for stocks that offer limited, but predictable, profit growth. And if inflation is around the corner, regulated sectors like utilities are vulnerable as governments will use regulatory power to limit the pass-through of costs as general prices start to rise.

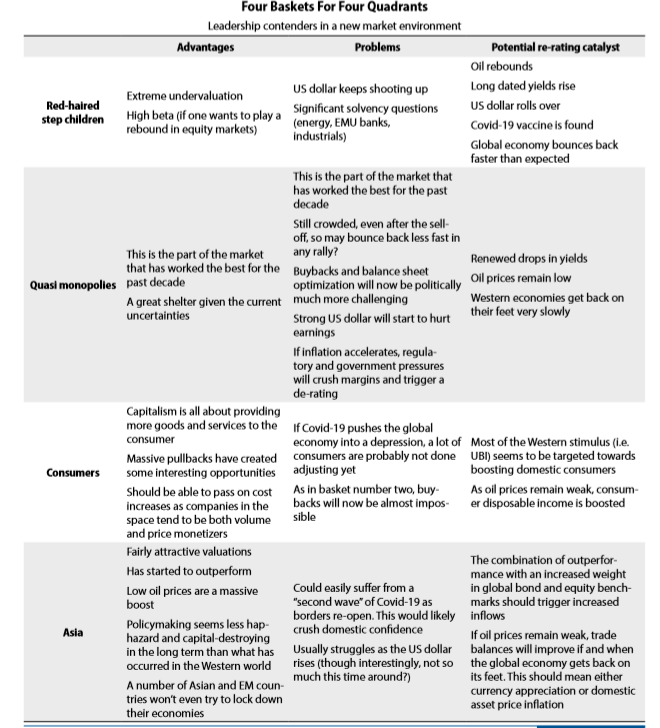

This brings me back to the ruin of global equity markets. At some point (perhaps as soon as this quarter’s end), institutions will rebalance from bonds and toward equities in part because of the extreme divergence between the two. This exercise may be given more impetus by Western countries’ bonds no longer doing the job they are paid to do (make no mistake, in a number of markets, investors do pay for the privilege!) Unless regulations prevent it, workers/assets who don’t do their job usually get fired. Today, the bonds of Western governments are in this camp. As such potential portfolio replacements can be split into four “investable” baskets.

Basket #1: The “beaten like a red-haired stepchild” basket

This basket is made up of energy, materials, industrials and financials. It is the basket I advocated overweighting in recent months on the premise that the monetary and fiscal stimulus of the past six months would lead to a pick-up in both global growth and inflation. Needless to say, it has not worked out. Instead, the combination of Covid-19, the oil meltdown and a liquidity crisis has ensured that already cheap stocks in this basket have gotten cheaper. In essence, this basket is the “inflationary boom” basket for the constituent companies are, to use Gavekal lingo, the ultimate “price monetizers”.

Basket #2: The monopoly basket

Buying monopolies, or quasi-monopolies, has been an investor favorite for the past decade, whether in tech, health care, communications, utilities, or financial technology (the likes of Visa, Mastercard and Paypal). The re-rating of such stocks made good sense in a structurally deflationary environment as highly visible income is more valuable than fairy dust. Monopolies work well in both deflationary booms and busts (at least in relative terms) for they tend to be first and foremost “volume monetizers”. After all, monopolies which raise their prices tend to incur the wrath of regulators and governments.

Basket #3: The quality consumer basket

It is rare for consumer cyclicals or staples to benefit from the perception of being monopolies, even if their performance drivers are similar to those in basket #2. Indeed, consumer stocks usually do well in times when energy prices fall and inflation and wages are stable. In essence, they are the ultimate deflationary boom stocks. However, because they do not benefit from the perception of having secured a monopoly rent, the deflationary bust scenario can be more problematic for basket #3 than for basket #2.

Basket #4: The Asia/China basket

Chinese fixed income was one of the few asset classes that did its job in the past month. As many investors will have paid little attention to the asset class, this performance could yet spur a shift in assets from Western to Asian bond markets. Such a shift could be justified by the increased divergence in policymaking between the two regions—in the West, domestic economic collapse followed by universal basic income and MMT; for the East, rapid detection and quarantine with limited monetary and fiscal stimulus. Along with fixed income, Asian equities may also warrant a look. Here again, we have in the past month started to witness outperformance from Asia which is unusual as in broad sell-offs, Asian equities tend to deliver worse returns than developed market equities. In big equity market downturns, Asia has been the “high beta” play; never the “low beta” play. Historically, the region has been a “price monetizer” and tended to thrive during inflationary booms (just like the red-haired step-children of basket #1). This makes Asia’s recent outperformance all the more interesting.

Needless to say, each basket has its own attractions, pitfalls and possible catalysts. But the end question remains the same: is the current bear market a dip in a broader deflationary boom trend, and thus an opportunity to buy back the shares that have done so well in the past decade? Or, alternatively, is this bear market repeating patterns of the past by facilitating the transition of leadership from one group of assets to another? There is good reason to think that it is the latter and future leadership may come from Asia.

*Note: another Gave and co-founder of Gavekal Research.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.