“The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore, all progress depends on the unreasonable man.”

-GEORGE BERNARD SHAW, playwright

Conform or reform? In human terms, 500 years is a very long time. Yet, that’s how far back one of the most renowned Fed watchers is taking us in this edition of our Guest Evergreen Virtual Advisor (EVA). Danielle DiMartino Booth has previously been highlighted in these pages and she graciously gave us permission to run her recent missive: “Destination Reformation: The Dawn of a New Era in Central Banking”.

If Danielle’s movie star-like visage looks familiar, it’s because she has become a regular on CNBC, and numerous other financial mediums, over the last couple years. One reason her media star has rocketed skyward is due to the fact that for nine years she had a privileged view into the inner workings of the Federal Reserve as advisor to former Dallas Fed President Dick Fisher. Their tenure coincided with the era when Ben Bernanke was launching his series of QEs into the turbulent seas of the financial markets in the immediate post-crisis years.

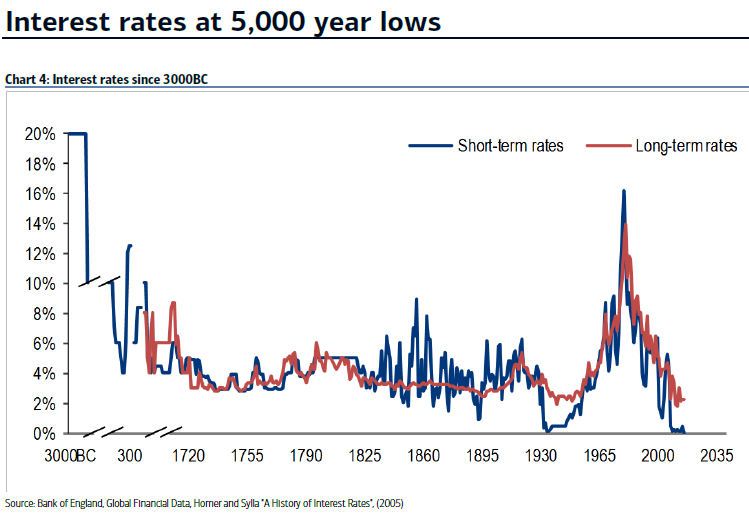

But what really caused the financial media to embrace Danielle was her best-selling book, Fed Up: An Insider’s Take on Why the Federal Reserve is Bad for America. However, as we are well aware, the Fed is far from alone in its multi-year pursuit of monetary extremism. All of the developed world’s central banks have engaged in unprecedented efforts to force interest rates down to the lowest point in 5000 years. Even my crude math skills tell me that’s 10 times longer than 500 years.

In this week’s piece, Danielle directly addresses one of the themes we’ve harped on in multiple EVAs this year: the changing of the guard at the Fed and what that likely means for monetary policy as well as financial markets. Her point about the influence of the various Fed chairmen and women over the last thirty-seven years is a key one, in my view. She points out how, back in the 1980s, the Fed’s tone morphed from the non-academic bluntness of Paul Volcker to the intentionally obfuscating verbal style of Alan Greenspan. It was also under the former “maestro” that the Fed abandoned its willingness to allow financial markets to find their own level and became obsessed with attempting to prevent market downside. (It’s ironic that the two worst market declines since the 1930s occurred in this “Fed put” era.)

As Danielle notes, we are now moving out of the Bernanke/Yellen regime. They were widely viewed as near clones of each other and intellectual soul mates of Mr. Greenspan. Their successor, Jeremy Powell, is seen by many as another virtual replicant. But Danielle disagrees, observing that Mr. Powell has expressed remorse for supporting QE III. Danielle feels Mr. Powell, like Martin Luther 500 years ago, has what it takes to reform an institution that has suffered from an extreme case of hubris in high places.

It’s my fervent hope she is right. Mr. Powell may be taking on America’s toughest leadership position—harder even than what John Flannery has stepped into at General Sclerotic Electric. But we do agree with her that the Fed is clearly becoming much more focused on asset price inflation instead of just consumer price inflation. Its new Underlying Inflation Gauge (UIG) is encouraging in that regard, as she explains.

It’s important to note that Danielle, like me, believes the Fed was totally justified in implementing QE I during the worst of the 2008/2009 panic. But, also consistent with my views, she is convinced the repetitive iterations since then only served to create a string of dangerous bubbles, with the present low volatility seen in the US stock market representing “a ticking time bomb”.

It’s time to turn it over to Danielle but, before I do, I would like to re-recommend her book, Fed Up: An Insider’s Take on Why the Federal Reserve is Bad for America. Additionally, her Money Strong weekly newsletter is one of my must-reads and I think it should be for other professional investors, as well.

In the meantime, Godspeed Mr. Powell!

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DESTINATION REFORMATION: THE DAWN OF A NEW ERA IN CENTRAL BANKING

By Danielle DiMartino Booth

Combine contraband coffee, paralytic guilt and a gift for translating Greek and you too can change the world. Such was the case with a young, deeply devout Catholic by the name of Martin Luther in the year 1516. A decade after he traded academia for the priesthood, Luther found himself disturbed by the quid pro quo nature of Catholicism. Sin expunged via penance in increasingly pecuniary form struck Luther as graceless at best. A field trip to Rome only served to dial up his unease as the ornateness on vivid display communicated dishonesty and even vice. That this epiphany coincided with the first trickles of coffee into Germany was fitting given what was to come.

And so, it was that contrition and caffeine contrived to compel Luther to seek the ultimate truth in sleep-depriving, time-consuming translation. Legend has it that the culmination of his first body of work arrived with his 95 Theses being hammered onto the grand doors of the Castle Church of Wittenberg, Germany on October 31, 1517. Five hundred years later, the Christian world continues to celebrate what was contorted by the corruption of Latin-speaking priests. The word “repent” in the Latin Vulgate should never have been translated as paenitentiam agite, or “Go, and do penance.” The original Greek text for repentance was rather metanoia, or making a decision to turn around, to face a new direction. In the case of the New Testament, metanoia translated into a lifetime of repentance, of turning from sin and trusting that to be saved is not a once in a lifetime initiation, but rather the daily sustenance of Christianity itself. Imagine, that magnificence was captured in his first thesis alone; 94 more followed.

One man. One selfless goal. One moment in time.

Sometimes that’s all it takes to transport the masses from the dark shadows into the light of day. That is what Martin Luther achieved by turning from the insularity of academia to the true meaning of the priesthood, which translated from Greek, once again, means to sacrifice in the name of God. Imagine if today’s central bankers had pivoted in the same spirit, if they had taken the riches of their studies and translated them into lifetimes of sacrifice to serve those they’ve committed to shepherd. How much more secure would our world be today if economics had not been elevated to the exclusion, but rather opened up to the inclusion, of every man and woman who mires in financial illiteracy?

History is a deeply personal concept. Eras to one are a continuation to others. In my case, the realization that central bankers were purposefully excluding even the educated masses arrived with Alan Greenspan and the advent of “Fedspeak.” In a 2007 60 Minutes interview the year after he left his post as Chairman of the Federal Reserve, Greenspan explained that he had employed, “a form of syntax destruction” to sound as if he was answering Congress’ questions. The true aim, though, as he offered, was to not answer the question. But he sure did sound brilliant.

Most agree that Paul Volcker is brilliant. At the same time, the man who preceded Greenspan’s coming into office on August 11, 1987 was no PhD and he redefined blunt. Mark the handoff between the two living legends as the commencement of a dark age in this nation’s history, one that would go on to achieve the opposite of an economics reformation. Some 30 years on, the plainspoken has been obfuscated back into agenda-driven Latin, or what we’ve come to know today as Fedspeak.

All of that can now change. For the first time since Greenspan breached the Fed’s threshold, a non-academic has been charged with safeguarding the wellbeing of our nation’s economy. Though the conventional wisdom insists Jay Powell is a calm continuation of the past three decades, a Yellen clone, the breadth of his life’s experiences gives hope that he is not as malleable as the markets would like to believe.

Every dawn begins a new day. Powell is known to have regretted voting for the Fed’s last-ditch effort to anesthetize the financial markets, otherwise known as the final round of quantitative easing. If it’s true that we learn the most from our failures, perhaps this is a good launch point for him to contemplate what he hopes to accomplish as the Fed’s new leader.

One man. One selfless goal. One moment in time.

With any hope Powell has no preset agenda. He once worked for a $1 salary to consult the Congress on the dangers of the United States defaulting on its debt.

Politically savvy as he no doubt is, Powell is wise to the fact that it’s the Fed’s second mandate, to maximize employment, that’s driven his predecessors to excessive easing these past 30 years. Ergo, he knows it would take an optically unpopular Act of Congress to reverse the 1977 mistake that put the second mandate in place and return the Fed to its rightful role as lender of last resort, as the entity charged solely with protecting the buying power of the U.S. dollar.

In that the current state of politics suggests ‘unpopular’ and ‘Act of Congress’ will never go hand in hand, Powell should instead work to formalize the Fed’s understood third mandate, that of financial stability. You may be thinking that’s what got us into this inescapable boom/bust cycle to begin with – Greenspan’s inviting the financial markets to dictate Fed policy.

Counterintuitive as it may seem, an effective formalization of financial stability reverses the impetus for the Fed to follow the markets. Even better, the Fed has a tool in hand, a first thesis, if you will, to accomplish this conversion.

Call it a hunch. But chances are the name Simon Potter may become familiar to you in the coming months. By all appearances, the current head of the New York Fed’s Markets Group has spearheaded a project of historic import at the Fed, which is saying something. You may note that Potter’s predecessor in Markets who went on to be president of the NY Fed, Bill Dudley, recently announced his early retirement.

Potter’s name is raised here to purposefully distinguish it from Dudley’s. Color me the skeptic, but I fail to see any semblance of coincidence in Potter’s work on an alternative inflation gauge that captures stock market pricing with Dudley’s post-election about-face to publicly proclaim the dangers of easy financial conditions as license to speed up the process of raising interest rates.

A digression. Recall this Dudley is one and the same with the Dudley who altered the order of the Fed’s exit years ago, adamant that the Fed could begin to normalize interest rates before reducing the Fed’s balance sheet. Though such weed trolling may seem trite, Bernanke would have failed to sell a handful of District bank presidents QE without the promise that the Fed’s balance sheet would shrink as a first step back to normality. Dudley’s coercing a continuation of reinvestments was no small matter. Ask anyone in the room at the time.

Time and again, Dudley carried the owls’ shield into battle. Hence the hypocrisy of his finding his inner hawk after the election had come and gone.

That dollop of background is essential to grasping the import of the Fed’s recent recognition of financial conditions in an inflation metric of their own device. The very disregard of those conditions rendered them blind in the years that the housing boom inflated into a bubble and subsequently collapsed and culminated in the Great Financial Crisis.

For the purpose of simplicity, think of ‘financial conditions’ as a reflection of asset price inflation. The hotter asset prices, the easier financial conditions that induce risk-taking, animal spirits, speculative behavior – take your pick.

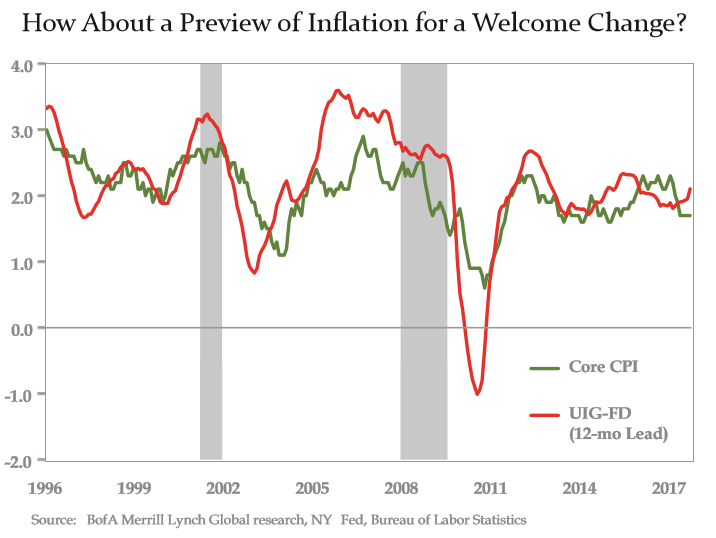

At the risk of waxing wonkish, the NY Fed’s Underlying Inflation Gauge (UIG) is a dynamic factor model. In English, that means that in endeavoring to capture the underlying inflation trend, the UIG incorporates an abundance of indicators to glean the commonality across time series. Conversely, ‘core’ and ‘trimmed mean’ metrics strip away the most volatile inputs to discern the persistence of what’s driving inflation.

Unlike the CPI and other traditional inflation measures that capture only measurable prices, the UIG ‘full data’ series incorporates labor, monetary and financial data. In addition, the UIG captures the persistence of price moves over a 12-month timeframe.

This from Bank of America Merrill Lynch: “The rationale is that monetary policy affects the medium to long run trend in inflation while moves in inflation at a horizon of one year or less are less likely to be related to the stance of monetary policy.” It is the case that monetary policy percolates through the economy with a lag, so this is a logical approach.

Patience please. Unemployment measures are the most lagging of economic indicators. They should thereby be the last to flash red, as in overheating. It stands to reason that of the 200 inputs tracked, labor market indicators are the most negatively correlated with the UIG. The caboose does not precede the engine. The flip side is that the of the top 10 positively correlated inputs, eight are financial market indicators that drive the inflation train into the station. Leading trumps lagging in any race to the finish line.

As financial markets make mincemeat of the prior day’s record close almost daily, it should come as no shock that the NY Fed’s UIG has been running hotter than the traditional inflation metrics which cannot possibly depict the same urgency to policymakers. BofA Merrill’s conclusion: “The UIG could be a more direct way of linking asset price inflation with consumer price inflation.”

Conveniently, for freshly minted central bankers not married to lagging indicators that only suggest where they might be headed, the UIG gives a nice 12-month preview of what lies ahead. The best news yet is that your eye doesn’t lie. The year-over-year change depicted in the chart below is all you need to see the forward-looking tendency of the UIG vs. the core CPI, which excludes food and energy.

With all due respect to every economist who’s ever had a rule named after them, the idea that any one metric should be used to create monetary policy for the world’s largest economy is hazardous. Recall that it was liquidity that seized up in the early days of the financial crisis. Make no mistake, it was the panoply of emergency liquidity programs paraded out by the NY Fed that eventually stemmed the tide and prevented systemic risk from taking hold.

And this is the critical distinction: It was not the level of interest rates, as in the price of credit, or the size of the Fed’s balance sheet, that saved the markets, but rather the reintroduction of liquidity where it had dried up rendering no price relevant to execute a trade. The liquidity facilities were the white knight writ large.

With that as the stark background, the next generation of central bankers must ask hard questions of themselves in the here and now. Could another liquidity freeze of 2008’s magnitude manifest today?

The short answer is how on earth could it not? Ill-designed post crisis regulations will deprive capital markets of their lifeblood of liquidity at combustion points. And this is something we know as fact today. Brokerage firms’ stores of bond inventories have plummeted even as issuance has set records for seven consecutive years. How will this disconnect be rectified in the face of a liquidity freeze? It won’t be. The backstops are gone.

That begs the next question. What to do? As dissatisfying a menu choice as it might appear, the best thing to do might just be very little. With all due deference to the neo-hawkish contingency led by Bill Dudley, concerns that financial conditions are too easy are naïve. That’s not to say complacency is not ingrained at record levels. But rather that easy financial conditions, in and of themselves, present a clear and present danger to an economy that’s become wholly dependent on the staying power of a rally in risky assets.

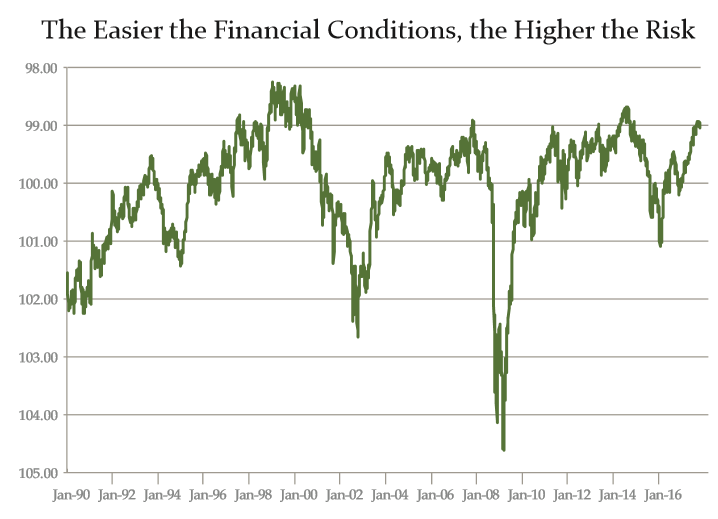

If the new orthodoxy is one that comprehends that the fallout from financial instability will always fall under the Fed’s purview, then it might be high time someone stood the whole idea of financial conditions on its head. Easy today is tomorrow’s percolating risk. Tighten into such treacherous territory at your peril.

What you see in the chart below these words is the Goldman Sachs Financial Conditions Index, but inverted. Don’t envision easy financial conditions as indicative of an overabundance of animal spirits, even if that is indeed the case. Be mature about the precarious environment and understand that the mirror image of complacency, of record low volatility, is a ticking time bomb of rising financial instability. Overtighten into this seeming calm, and detonate that bomb at will.

If the last bastion of the old guard at the Fed continues in its current thinking, it will follow easy financial conditions and natural-disaster-exacerbated inflation into the abyss, forcing the economy into recession just as they make their way for their own exit.

As things stand, the market is pricing in one rate hike in December and one next year. Is that reasonable? To borrow a central banking term, evidence is mounting that ‘transitory’ factors will juice GDP growth over the next six months. This flash of growth will push the unemployment rate down further while at the same time show up in pockets of wage growth. The Fed could well chase these indicators, despite the underlying fragility of the economy, and in doing so, invert the yield curve.

With a scant 69 hundredths of a percentage point between the two-year and 10-year Treasury yield, the bond market is communicating the economy can handle two rate hikes at the most. As distasteful as the prospect may be, pay heed to Fedspeak in the weeks to come. At the first hint that policymakers are selling the case for a more rapid tightening ramp-up, make a sprint to short the two-year and buy the 10-year. Ride that curve.

December 1996 was a wasted watershed moment in U.S. central banking history. Alan Greenspan knew the stock market was overheating. He even called investors’ “irrational exuberance” to the carpet. And then…he did nothing. He didn’t raise margin requirements but sat back and watched the bubble grow to such magnificent proportions it imploded under its own weight. And then he and his moral hazard henchmen rode to the rescue.

Greenspan would not learn a thing from his failures. In the years following the dotcom bust, he repeated his sins of the past, but in grander form, insistent that the role of the central bank was that of the clean-up crew, only and ever after the fact. What the country received in return was the worst housing and financial crises since the Great Depression. Pay the price we did.

All the while, savers lost billions upon billions in interest income, a predicament that landed them in increasingly desperate straits, chasing yield into their twilight years as so many fireflies in the night.

The onus is thus on Jay Powell to do as Martin Luther did all those years ago. Recognize the err of his predecessors’ ways, tradition be damned. Break the Fed’s penance habit, acknowledging that there are actions that can be taken as a bubble is forming to mitigate its eventual damage. Live by no tried and true rule of thumb. Question the orthodoxy every step of the way. And finally, take back the Fed’s independence by never again allowing the markets to make monetary policy. When in doubt, lean against the wind and in doing so, restore integrity to the Federal Reserve.

No doubt, those are tall orders. It would be disingenuous to suggest Powell can stand on principle from day one. The next recession and multiple market corrections will exert tremendous pressure to slash interest rates right back to the zero bound, where they never belonged. Perhaps a viewing of General Electric’s new CEO’s interviews would bolster Powell’s convictions. Rarely has a public figure done such a gracious job of citing his predecessors’ failings for his firm’s woes. But that very task awaits Powell.

The good news is there is grace to be had. Zero interest rate policy has failed miserably, a fact increasingly on vivid display. Meanwhile, the Fed’s own staff papers concluded that QE was, shall we say, inefficacious. While we’re bandying about fancy economists’ terms, take one last page out of Martin Luther’s play book and translate the arcane into the articulate, the universally attainable.

To prepare for the monumental challenges that lie ahead, perhaps a deep study of William McChesney Martin over the holidays is also in order. For starters, it will help Powell manage the monstrous organization of academics housed at the Fed, to say nothing of priming himself to resist any encroachment on the Fed’s independence from the Congress or the White House.

McChesney Martin, the longest serving Fed chairman in its history, is most famous for testifying to Congress that it’s the Fed’s job to take away the punch bowl just as the party gets going. While no doubt one of the greatest punch lines of all time, my time on the inside left me enamored with his other, wise warning -- that it was essential to keep the PhDs at the Fed on tap, but never on top.

One man. One selfless goal. One moment in time.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.