“Whenever you are about to find fault with someone, ask yourself the following question: What fault of mine most nearly resembles the one I am about to criticize?”

-MARCUS AURELIUS in Meditations (written in 180 AD—when interest rates were higher than they are now!)

As I’ve expressed in previous EVAs, Anatole Kaletsky is one of the smartest people I’ve ever met. While he’s not well known in the US, his star shines brightly in Europe where government and financial leaders seek out his guidance. He’s also the “kal” in our partner firm, Gavekal, which was recently the subject of a glowing article in Barron’s, interviewing one of my closest friends, Louis Gave.

Gavekal is well-regarded by its clients not only for its extensive and intensive research but also because of the openness with which it conveys its internal disagreements. Rather than projecting the consensus firm view, as many of its competitors do, Gavekal provides clients with starkly contrasting perspectives. Regular readers of their research—or even our monthly Gavekal EVAs—realize that Anatole and another of Gavekal’s co-founders, Charles Gave, are often diametrically opposed in their outlooks.

In that spirit, I felt that the former’s recent piece, “This Is (Still) Not a Peak: It’s a Global Bull Market”, was ideal for this month’s Gavekal EVA. My reasoning is that, in this note, Anatole offers a bullish appraisal of future stock market returns, which is pretty much 180 degrees opposite of mine--at least when it comes to US shares. As I’ve conceded before, Anatole has been far more on target in recent years in that regard than I have and for that I give him full credit. If you sense a “however”, you are close; I’ve actually got several “howevers” that I’d like to offer up to readers, realizing that it’s human nature to side with the hot hand—and that would be Anatole.

First among my push-backs is that he also said this summer that oil prices would be subject to a permanent ceiling of $50. As you may have noticed, oil has been trading more like $50 is a floor, not a ceiling, of late. But far be it from me to say that it’s a permanent floor. (In fact, I’ve made a personal resolution to never use the term “permanent” with any of my forecasts, per our Never Say Never EVA, courtesy of Grant Williams.) My point in this regard is that, as smart as Anatole is, he’s not always right.

Further, when he made his call for a new long-term bull market back in 2013, I brought up our “twin margins” concerns at the time—the reality that US corporate profit margins were at record highs and likely to recede, as well as the lofty level of margin debt, even back then. His reply was that they didn’t matter because sales growth was poised to accelerate so dramatically.

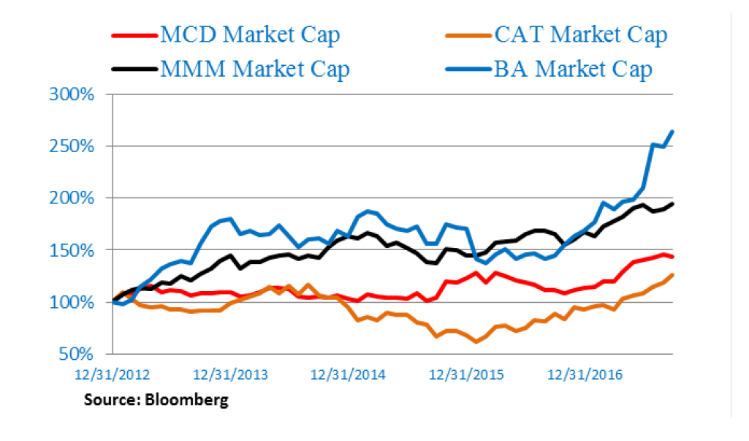

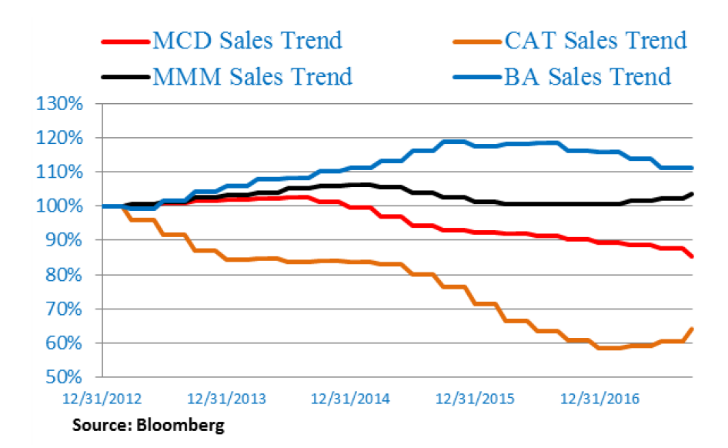

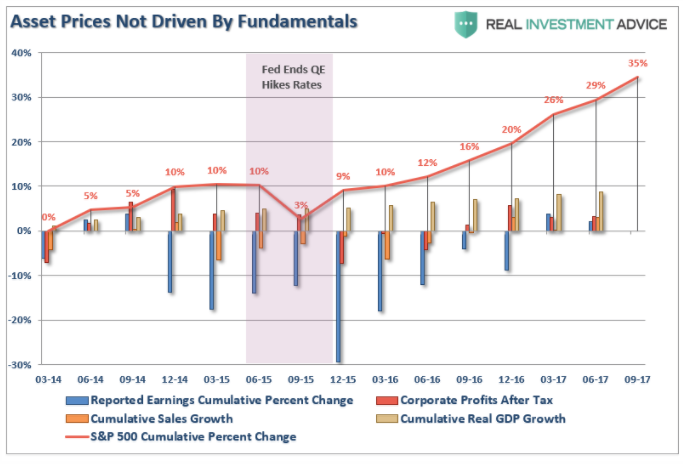

In reality, US profit margins topped out in 2014 and Corporate America entered a five to seven quarter (depending on the source) earnings recession. Meanwhile, sales stagnated rather than took off. This didn’t stop the market’s continuing rise, indicating it wasn’t driven by sales or profits. The charts from Jones Trading’s savvy strategist, Mike O’Rourke, makes this point with some of the biggest market darlings of recent years. The chart below it, courtesy of David Stockman, Ronald Reagan’s former budgetary whiz kid, conveys the same message.

*MCD: McDonald’s Corporation, MMM: 3M Company, CAT: Caterpillar Inc., BA: Boeing

*MCD: McDonald’s Corporation, MMM: 3M Company, CAT: Caterpillar Inc., BA: Boeing

Additionally, margin debt has continued to rise to the highest percentage of GDP ever. That’s obviously been great for past market gains but it also poses a grave threat to the future.

Therefore, it’s somewhat analogous to getting the right answer on a calculus exam but doing so using the wrong formula. Now, I’m the first to say I’d rather be lucky than good but the relevance is that in his essay, Anatole dismisses the notion that it has been central bank money creation which has driven the bull market. His logic is that the bull has kept running even after the Fed stopped its three-stage quantitative easing (QE) programs.

Yet, what he neglects to mention is that after the Fed quit “QEing”, its overseas counterparts more than picked up the slack. As prior EVAs have noted, global QEs were annualizing at the fastest rate in the post-crisis era in the first half of this year. And, as has also been mentioned in these pages, the Swiss National Bank is now one of the largest holders of US blue chip stocks—all bought with magic wand (digital printing press) money. How such efforts could not have been behind much of the last half of this bull market truly defies logic, in my opinion.

Anatole also asserts, “the lesson is that QE and ZIRP (zero interest rate policies) helped to create a genuine, sustainable economic recovery and not just a temporary ‘narcotic high’…”. Yet, this overlooks the fact that there have been two global economic downturns since 2010 and the weakest US expansion on record. This is despite interest rates being driven actually below zero in many countries and all the trillions in QEs. Additionally, many more trillions in government deficits throughout the developed world (ex-Canada) have also been needed to produce the weakest growth the world has seen in many decades. In fact, over the last six years the US has added $5.7 trillion to its cumulative national debt despite the fact we have been in a steady, if anemic, expansion. (Please click here to access David Stockman’s searing indictment of our addiction to debt.)

My other major quibble would be that we really need to see how this all turns out, especially once the central bank liquidity fire hose turns off. If we experience yet another bubble bust (as I warned in the late 1990s because of the insanity in tech stocks and again with the housing mania 10 years ago), then it will have been highly premature to call the policy prescriptions of recent years a success. In other words, the next few years could bring about a total role reversal in terms of outcome accuracy.

To add a however on top of a however, I do agree very much with his point that for investors who want to bet on a continuation of the global bull market—which could last well into next year—the best way to play it is with overseas markets. As regular EVA readers know, this is a theme we’ve endorsed over the past year—even when it was unfashionable after Mr. Trump’s election and all of the “America first” hype.

Anatole’s warnings about the frenzied trading and nonsensical valuations in what he calls the “cyber currencies” also rings true to me (but more on that next week), as do his warnings about valuations with some US tech stocks. Given that the median price-to-sales ratio of the S&P 500 is far higher that it was even during the daffiest days of the late ‘90s market mania, it indicates to me that bubble conditions are far more prevalent, at least in the US, than Anatole allows.

One final “but”: But you be the judge. Perhaps Anatole’s arguments are more persuasive than mine in those areas where we disagree. Of course, none of us will know for sure until this particular stock market tide goes out, as it will inevitably do—no matter how many smart folks say otherwise.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

THIS IS (STILL) NOT A PEAK: IT'S A GLOBAL BULL MARKET

By Anatole Kaletsky

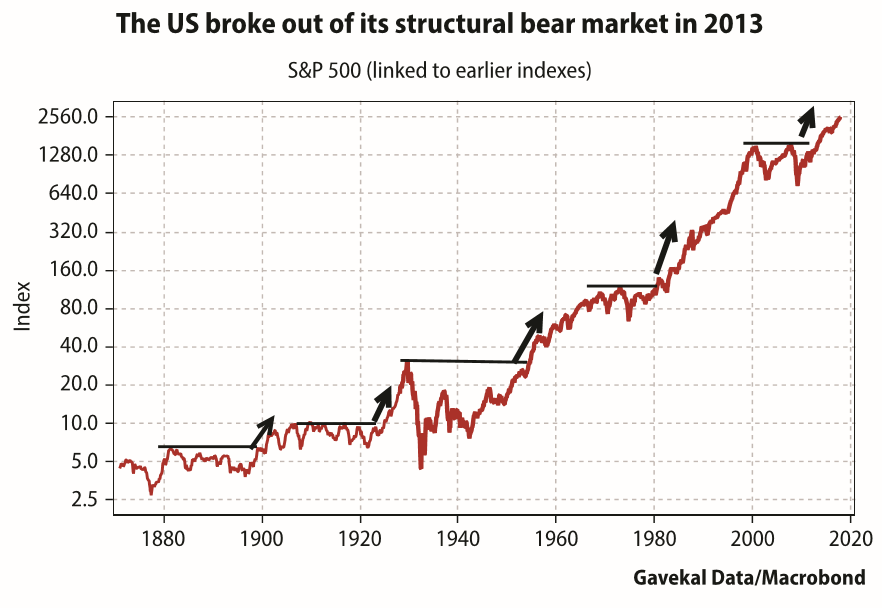

Near the end of a year that has seen equity markets set records on a near daily basis, it is tempting to turn contrarian and argue that the bull market is almost over. But after spending much of 2017 spreading a bullish message about equities and global growth in hundreds of meetings with Gavekal clients, I am convinced that fear, not greed, is still the dominant emotion in markets. Many investors still see recent asset price gains as a bubble, pumped up by monetary stimulus. The truly contrarian argument is one I have made since March 2013, when the US broke out of its 13-year trading range.

What many investors considered an unsustainable “dead cat bounce” after the financial crisis, has gradually matured into a structural expansion of economic activity, profits and equity valuations, which probably has many more years to run.

In this article I will summarize the main reasons for maximizing equity exposure, especially in Europe and emerging markets. In future articles, I will consider key risks to this benign investment outlook. When this bull market dies it will not be killed, in my view, by recession, secular stagnation or liquidity tightening, but by inflation and excessive stimulus applied to economies already near full employment.

For most of the world economy, that danger is many years away. In the meantime, there are at least five reasons why the global equity bull market has a long way to run:

Reason #1: The world economy is firing on all cylinders. For the first time since 2008, the US, Europe, China and most other big emerging markets are experiencing decently strong economic growth without threats to financial stability. Eventually, these coordinated expansions will either produce over-heating and inflation, or a severe monetary tightening. But given high levels of unemployment and low capacity-utilization in many big economies, and the powerful deflationary pressures exerted by technology and global competition, the dangers of over-heating are years away. Until there is hard evidence of excessive and sustained inflation, central bankers will risk over-stimulus over premature monetary tightening. This means that a return to “normal” interest rates— the Fed Funds, for example reverting to its pre-2008 average of 1.8% in real terms or about 4% in nominal terms—is almost inconceivable in any major economy, at least until the end of the decade.

Reason #2: The financial consequences of extremely loose monetary policies are now much better understood than when the unprecedented experiments with quantitative easing and zero interest rates started in 2009. In the first few years of these experiments, investors quite reasonably worried that the economic recovery and rising asset prices were temporary and unsustainable effects of ever-larger doses of monetary stimulus—and when the stimulus was reduced, economic activity and asset prices would collapse like an athlete addicted to ever larger injections of steroids.

This worry, which is still widely held, became less reasonable after May 2013, when Ben Bernanke announced his QE taper. It became extremely questionable after October 2014, when the QE ended completely. And it became fully irrational after December 2015, when the Federal Reserve started to raise interest rates. After these reductions in stimulus the US economy did not fall back into recession or stagnation as predicted by skeptics. Instead the US matured from its post-crisis recovery phase, fueled by extreme monetary stimulus, into a steady expansion powered by a virtuous circle of employment growth leading to consumption growth, leading to corporate activity and more employment growth.

And asset prices, far from collapsing, accelerated to new highs. In fact, the US equity market broke out from its long-term bear market trading range two months before Bernanke’s tapering announcement. After the brief “taper tantrum”, US equities have steadily risen. The lesson is that QE and ZIRP helped to create a genuine, sustainable economic recovery and not just a temporary “narcotic high”, to be followed by an inevitable economic “cold turkey”. And as initial doubts about the Fed’s monetary experiment have been put to rest, the US has provided a road-map which other economies have followed, albeit with long and variable lags.

Reason #3: Because of the long lags between policy responses in the US and other countries, this expansion is geographically de-synchronized in a way not seen before. Full-scale monetary stimulus was launched in Japan in 2013 and in Europe in 2015, six years after the US. Many emerging economies only started easing monetary policy last year and may not reach the limit of their stimulus until 2018 or beyond. As a result, national business cycles, profit cycles and monetary cycles are less synchronized than in any previous global expansion. This is a source of strength to the global economy and financial markets. It will help to moderate the impact of US monetary tightening and delay the inflationary pressures that a coordinated global expansion would normally create.

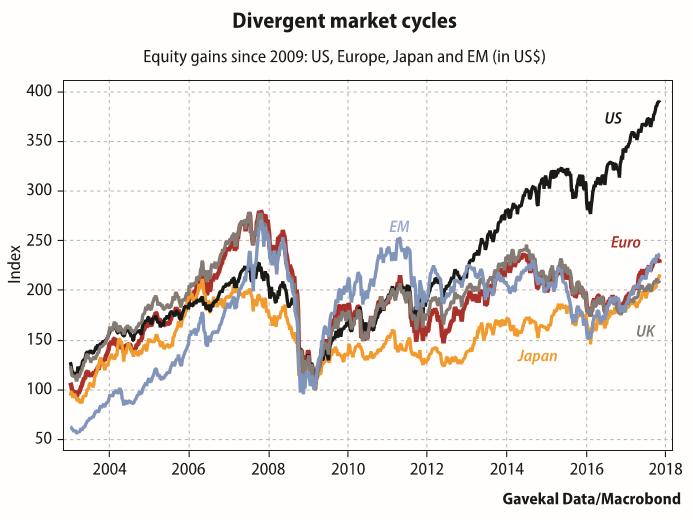

The unsynchronized character of this expansion is also creating new investment opportunities by encouraging a rotation of global profits. While the US is moving beyond the most attractive period of the cycle, when profits are rising but monetary policy is ultra-stimulative, Japan, Europe and many emerging markets are only just entering this Goldilocks phase. The lag between US monetary leadership and the cyclical catch-up in other countries has created an unprecedented divergence in equity performance, especially since Wall Street’s breakout from its bear market trading range in 2013. This cyclical gap has now begun to narrow. And this narrowing should continue, both through relative equity performance and through currency appreciation against the US dollar, creating good investment opportunities for several years.

Reason #4: Since the financial crisis, market psychology has been blighted by two other great fears beyond the “cold turkey” effect of withdrawing monetary stimulus: a possible breakup of the euro and a crisis in China. Both of these clouds have now lifted. Mario Draghi’s QE program removed the possibility that bond markets or bank runs would trigger a euro breakup. This still left the threat that nationalist politics might break up the euro, or even the entire European Union, after the Brexit vote. But this political risk was eliminated by last spring’s French election. Risks of nationalist politics may return to haunt the eurozone, but not until the next election cycle in four or five years’ time.

Market fears of a Chinese banking or currency crisis in 2015 never made much sense in our view, but many of the world’s most influential investors got carried away with full-scale China panic in early 2016. With the Chinese economy recovering strongly, the fear-mongers have been silenced and China panic, like euro panic, is unlikely to blight global financial markets again, at least for the next few years.

Reason #5: A more controversial reason to believe that the equity bull market has room to run could be described as “behavioral economics” but is really just common sense. Beyond improved cyclical conditions, there are structural questions about the world economy’s long-term prospects. Will excessive leverage be permanently mitigated by low interest rates? Will productivity suffer more from the distorting effects of low interest rates than it gains from technological progress? Will demographic aging hurt asset prices by reducing growth and profits, or boost markets by suppressing interest rates? Will nationalism and protectionism dominate competition and globalization?

This list could go on, but most of these questions have one thing in common: none of them can be answered definitively for many years ahead. What can be said with confidence is that predominant market views about such questions will be strongly influenced by what is happening to the world economy in the short term. In recessions, investors get obsessed by long-term headwinds such as aging, capital misallocation and debt burdens. But in a global upswing, investor psychology shifts to the benefits of low interest rates, the opportunities of leverage and technological progress.

When this shift towards optimism goes too far, asset valuations start rising exponentially and bull markets approach a dangerous climax. In some parts of the technology sector, this is already happening—cybercurrencies are the obvious example. But most global equities’ valuations are not excessive, given zero or negative real interest rates, especially in non-US markets. Investors are nervous rather than euphoric—and equity prices are continuing to climb a fairly steep “wall of worry”. After dismissing many of these worries in this article, my follow-up piece will address specific investment opportunities that flow from this bullish outlook and some of the risks that could cause my analysis to go wrong.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.