“It’s a bubble that’s going to give a lot of people a lot of exciting times as it rides up and then goes down.”

-JOSEPH STIGLITZ, former World Bank Chief Economist and Nobel Memorial Prize in Economic Sciences winner

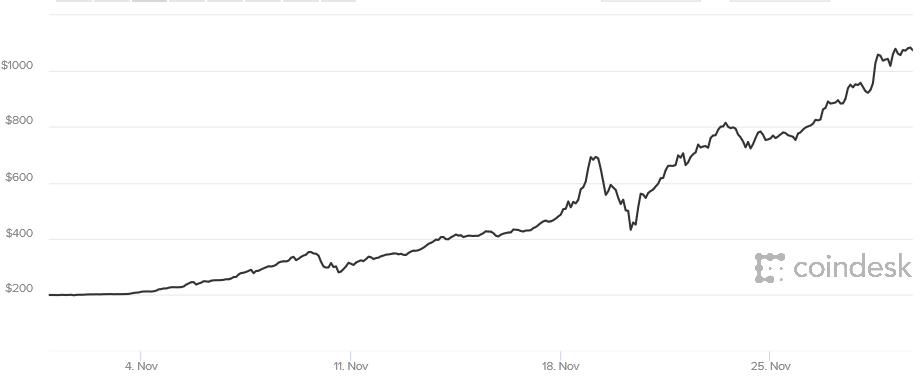

I asked myself that very question as the price of Bitcoin doubled from $200 USD to $400 USD over the first two weeks of November 2013. My conclusion was to stick to the investing principle I had been taught by my father at a very young age: never buy into something that is hype-driven.

Unfortunately, sticking to that sage wisdom cost me a 170% return over the next two weeks, as the price of Bitcoin roared to nearly $1,100 by the end of November.

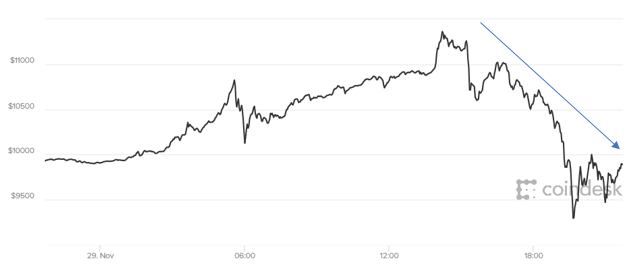

Source: Coindesk; November 1 – November 29, 2013

Source: Coindesk; November 1 – November 29, 2013

Even more unfortunate is that if I had bought into Bitcoin at that $400 price point in mid-November 2013 and had the courage to ride out its return-trip south to $177 in January 2015, I would be laughing my way to the bank with a 2,400% return* in four years.

Who ever said playing the “what if” game wasn’t fun… Should we keep playing?

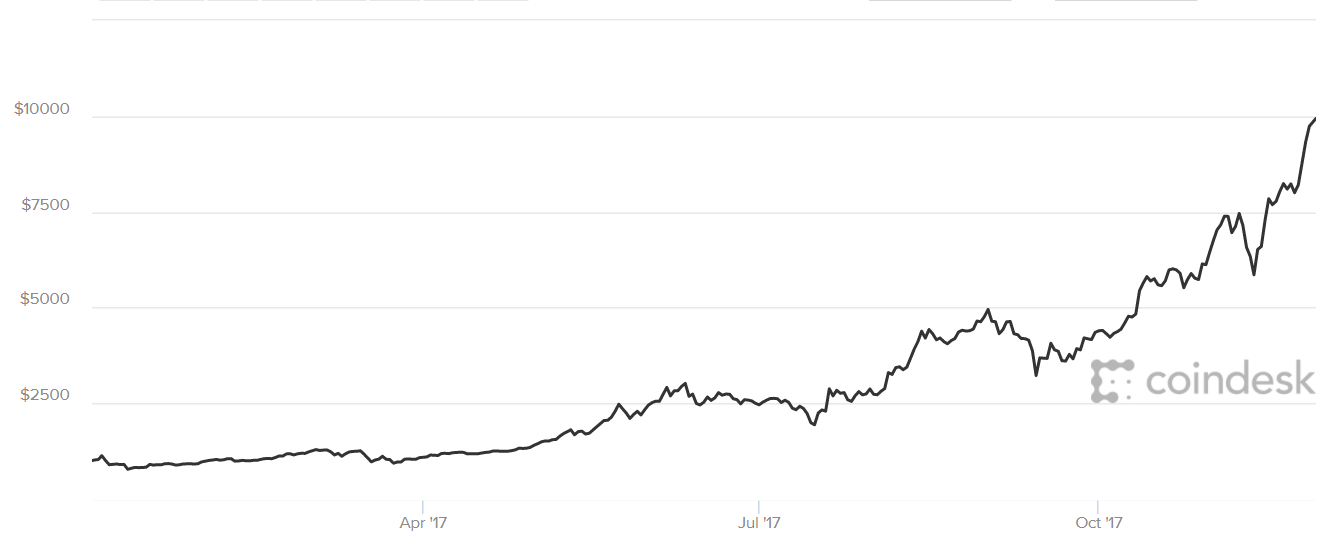

What if… I only looked back at the past year, and bought into Bitcoin at the beginning of 2017? Well, in that case, Christmas would have come early for me because I would have returned roughly 900%* in 11 months.

* As of 2:00pm on November 30th, 2017

Source: Coindesk; November 1 – November 28, 2017

Source: Coindesk; November 1 – November 28, 2017

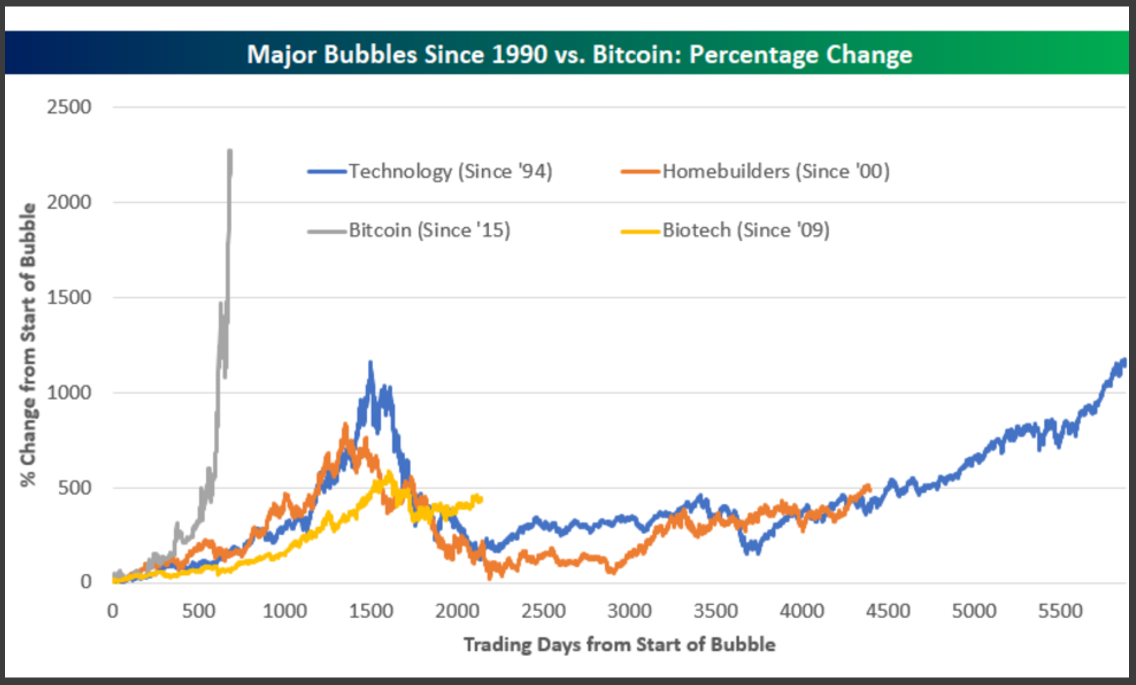

To say Bitcoin has created an investment frenzy is an understatement. It has created a tidal wave of speculation not seen since Tulip Mania in the early 17th century.

Source: Danielle DiMartino

Source: Danielle DiMartino

And none of the three major bubbles since 1990 even came close to eclipsing the meteoric rise of Bitcoin in pace or rate.

Source: Bloomberg

Source: Bloomberg

But not everyone is jumping onto the Bitcoin bandwagon. Jamie Dimon, head of JPMorgan Chase and someone we’ve featured in these pages before, had some pretty harsh words for the cryptocurrency:

“I could care less about bitcoin… I don’t personally understand the value of something that has no actual value… If you’re stupid enough to buy it, you’ll pay the price for it one day. The only value of bitcoin is what the other guy’ll pay for it. Honestly, I think there’s a good chance a lot of the buyers out there are out there jazzing it up every day so that maybe you’ll buy it too and take them out.”

In fact, he even proclaimed that if a JPMorgan trader began trading in bitcoin, he’d “fire them in a second.”

And Dimon isn’t alone in his disdain for the “currency”. Saudi billionaire Prince Alwaleed (now under house arrest in his own country but long-regarded as a very astute investor) stated that he foresees an “Enron-like” demise for Bitcoin:

“I just don’t believe in this bitcoin thing. I think it’s just going to implode one day. I think this is Enron in the making. It just doesn’t make sense. This thing is not regulated, it’s not under control, it’s not under the supervision of any central bank.”

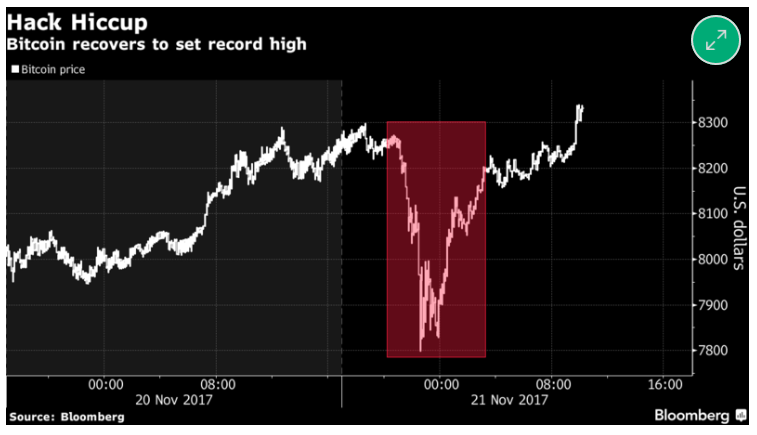

Both of those statements were made in October, while Bitcoin hovered below $6,000 per coin. In a month’s time, the cryptocurrency has made Dimon look like the “stupid” one, as Bitcoin shattered expectations to the upside, eclipsing $10,000 on Wednesday.

And Bitcoin bulls don’t believe the historic run is going to end anytime soon.

Given these diametrically opposed positions – one side arguing that the cryptocurrency is literally worthless and the other that it is infinitely valuable – it’s worth revisiting the question posed at the onset of this EVA: Should you invest in Bitcoin?

While there are certainly cases to be made for investing in the cryptocurrency, we believe that the Bitcoin bubble is a ticking timebomb best avoided. Below, we outline five reasons why you should avoid investing in Bitcoin.

1. Bitcoin is extremely volatile

Many of our clients and readers are nearing, or have reached, retirement age. Tried and tested investment advice should steer individuals in this phase of life away from extremely volatile holdings. And Bitcoin defines volatility. As the chart below shows, Bitcoin has plunged over 25% three times in 2017.

Source: Bloomberg

Of course, the major caveat is that this volatility has rewarded those willing to buy into dips, as the cryptocurrency has seemingly defied logic and continued its parabolic trajectory. Case in point: Bitcoin shrugged off the hack of nearly $31 million on November 21st, setting higher-highs within hours.

2. Bitcoin doesn’t behave like a currency

Typically, currency is defined by economists as having three attributes: it functions as a medium of exchange, a unit of account, and a store of value. Regarding the first attribute, Bitcoin holds up decently well. While not as widely accepted as, say, the US dollar, there are a growing number of companies and individuals willing to accept Bitcoin as a form of payment.

Regarding the second and third attributes, Bitcoin performs poorly as a unit of account and store of value. Most notably, Bitcoin faces challenges due to rampant hacking attacks and theft, and Bitcoin has virtually zero correlation with the U.S. dollar, euro, and yen. In addition to failing to meet the basic definition of a currency, Bitcoin cannot be deposited in a bank and has no form of protection comparable to deposit insurance.

3. Bitcoin isn’t backed

Bitcoin is completely unregulated. There is no government agency, bank, company, or tangible asset backing the cryptocurrency. Some proponents advocate that this decentralized ecosystem is actually an advantage, as there is no monetary system in place or central bank to regulate the crypto. But this point is often championed by those hoping to deal in the black market and avoid institutional oversight.

Now, there are many who don’t hold Bitcoin for these purposes, but the very regulations and systems some try to avoid are what protects the collective whole.

Imagine two scenarios: one scenario being that you hold corporate bonds and the other that you own Bitcoin. The company whose debt you own goes bankrupt and Bitcoin falls from $10,000 to $0; what happens to those investments?

In the case of corporate bankruptcy, you would likely be in line to recoup at least some of your investment. In the case of Bitcoin, you would have no claim to recover any of the money because the cryptocurrency is not backed by a company, government or central bank.

The bottom-line? If the Ponzi scheme falls apart, Bitcoin investors will be s%!t out of luck; there will be no last line of defense to bail them out.

4. Bitcoin is extremely expensive

What’s that adage again… what goes up, must come down? Fundamentally, adhering to the most basic investment principle to buy low and sell high, Bitcoin’s recent surge puts it in the category of “It’s really, really, really time to sell. Like, right now.”

Of course, at the risk of Bitcoin riding its intergalactic tailwind out of the ether and into “never, never land,” the cryptocurrency could very well continue its rapid run past $10,000. But banking on that (no pun intended) would be speculative in the extreme. It has just as likely a chance of plunging another 29%, 38%, or 40% (or more) as it did earlier in 2017.

5. Bitcoin could become banned

China banned the trading of Bitcoin on domestic exchanges in early September. Since China accounts for 23% of total Bitcoin trades and is home to the world’s biggest Bitcoin miners, the price of Bitcoin went tumbling before rising from the ashes – again! More recently, Vladimir Putin, the dictator president of Russia, expressed concerns over cryptocurrencies, flagging them as a way to launder money, evade taxes, and fund terrorism (he obviously doesn’t want competition for the activities at which his government excels!).

UBS (the world’s largest wealth manager) CIO Mark Haefele made a similar argument in mid-November, saying:

“All it would take would be one terrorist incident in the U.S. funded by Bitcoin for the U.S. regulator to much more seriously step in and take action… That’s a risk, an unquantifiable risk, Bitcoin has that another currency doesn’t.”

Given the fact that Bitcoin is not regulated, there are many threats the cryptocurrency poses to governments and systems globally. As such, the possibility of a more widespread crackdown or unified global policy could take hold. Imagine if the next major terrorist attack is funded completely by Bitcoin and what that might do to the price and future of the cryptocurrency.

In the meantime, don’t be shocked if Bitcoin continues to go postal. But, if you are tempted to jump in with all but your most speculative coinage, you might want to pause and wait a few hours.*

* The price of Bitcoin fell 18% (from $11,363 to an intraday low of $9,300) in the course of 5 hours on Wednesday, November 29th.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.