“Truth has no special time of its own. Its hour is now—always.”

- ALBERT SCHWEITZER, physician and humanitarian

“The nice part about being a pessimist is that you are constantly being proven right or pleasantly surprised.”

- GEORGE WILL

“Successful investing is when people agree with you…later.”

- JIM GRANT

For those who haven’t been to the Mauldin Economics’ Strategic Investment Conference (SIC), or are not aware of it, today’s edition of the Evergreen Virtual Advisor (EVA) will provide a glimpse into what takes place at this event. Every May, wealthy individuals, professional investors, strategists, and economists alike flock to whichever city John Mauldin and his crew decides will play host. For three days last week, attendees sat in a dark ballroom at a Dallas Hotel. Each luminary shares the lens with which they view the state and fate of the world economy and financial markets. It’s truly a “who’s who” of outstanding minds. The legendary James Grant was there. Niall Ferguson, the esteemed Harvard historian and author, also spoke. Former Dallas Fed Chair Richard Fisher gave his assessment of the world. The list goes on and this year the Mauldin team decided to give attendees a hefty dose of Gavekal/Evergreen viewpoints by inviting four of our team members to speak.

Clients often tell us they take comfort in knowing we have differing opinions within our investment team. Similarly, readers (now approaching 11,000) of EVA enjoy hearing from a variety of perspectives on the same topic. In an effort to both convey much of the very valuable material that was presented, and at the same time provide differing perspectives, Mark Nicoletti, Tyler Hay, and Jeff Dicks will each recap one key takeaway they felt worthy of sharing with our readers. To prevent financial information overload, we are splitting this issue into two parts with Jeff Eulberg and David Hay summarizing their impressions next week.

One of the guiding principles of Evergreen that stands out—adopting a contrarian spirit when appropriate—can make us look like fools at times. The flip side, running with the herd, or trend following, is easier after all. Trend followers look good for a long time, providing the trend persists. Contrarians look like idiots until the trend reverses and then they clean up, much to the dismay of the herd…who usually calls them lucky. Being different is easy, being different and profitable is challenging. My colleagues and I strive for the latter but there are times when being different—like buying energy last year during an epic meltdown—can delay the profitable part.

Last week, I attended the 13th annual Strategic Investment Conference (SIC) for the 8th straight year, accompanied by my several of my team members. In my experience, most of these events are more about networking than content. The SIC is the opposite; nobody skips sessions to sit by the pool or in the lounge. From the first speaker to the last, the room is full and the audience is engaged. The expert speaker list was as robust as ever with the likes of: Lacy Hunt, David Rosenberg, Charles Gave, Louis Gave, Michael Lewitt, and our own David Hay, in addition to those mentioned above.

For me, unlike years past, the conference had a decidedly bearish tone. The ‘experts’ are worried. Central banking action (U.S. politics runner-up) dominated the presentations. Will the Federal Reserve raise rates as they insist? Or “spit the bit” coming out of the starting gate? The divergence trade—the decoupling of the Federal Reserve from other major central banks and the effect that could have on interest rates and currency valuations—was the common theme among speakers. Economists and professional investors seemed to agree, an outlier in its own right: regardless of what the Fed does, we are entering a low return environment for U.S. equities. This was different versus years past. It sounded different as I soaked it in and it still sounds different as I recap it. This resounding sentiment, even coming from experts, gives me pause (see the first paragraph). Most EVA readers are familiar with Evergreen’s cautious stance and corresponding portfolio allocations. What now, unanimity? Are we all wrong by being worried? Has quantitative easing worked and we are just entering a new growth stage? Or maybe, just maybe, the widespread realization that the central bank emperors have no clothes is just over the horizon?

The most interesting speaker, and it wasn’t even close for me, was Jim Grant. I confess though, that I’m a disciple of Grant. His musings and frequent appearances on various financial television programs typically stops me in my tracks. Forget the content, he’s a gifted orator. Among many favorite quotes, this one from Jim Grant stands out: “People never exactly forget what it is to lose money, but it is something that is not in the front of their minds at moments such as this, of great overwhelming prosperity. I think the fear of loss is a little bit like the fear of a punch in the nose. You never exactly forget it, but it is never exactly in the front of your mind until somebody is sailing a fist toward your face. So it’s something that people never exactly lose, but they can tend to forget momentarily.”

Grant calls monetary policy a virus and contends that central bankers will be the villains when this period’s history books are written. He believes that gold is a monetary asset, as it’s always been throughout history, and an investment against monetary disorder. He quipped: “This is not going to be news, Jim Grant is bullish on gold. People will say well that’s a hedge against armageddon, no, armageddon won’t happen; but we are in the midst of monetary shenanigans, and I see no real chance of there being fewer of them, and a great chance there will be more of them.” On what investors can do to protect themselves from what is coming (other than gold), Grant recommends holding cash: “Cash is invariably a nice thing to have, even though it yields nothing. It’s an option. It gives you the flexibility to move and to buy things.”

I can’t help believing Jim Grant will be vindicated, at least partially. Manipulation is not healthy and not a dynamic tenet of capitalism. I can’t help but agree with the groupthink at this year’s SIC (as uncomfortable as it is for me) that the markets are fraught with the risk of something big going wrong. David Hay has noted that most of the folks who are worried now were also worried nine years ago. The SIC is made up of a lot of them. So maybe my contrarian feathers shouldn’t be ruffled by the consensus view, at least among this elite assembly, of trouble ahead.

I relish being called lucky by the herd, possibly sometime soon.

MARK NICOLETTI

Family Office Director

To contact Mark, email:

mnicoletti@evergreengavekal.com

As a first-time attendee at the SIC, I have to say it lived up to, or even surpassed, my high expectations. As Mark noted, the roster of speakers was truly remarkable. My key takeaways were mostly re-affirming in terms of our big picture outlook and portfolio positioning. The main point several high-profile speakers made was our world simply has too much debt. This has led to debt-servicing making up a bigger proportion of government and corporate cash flows, significantly reducing global growth rates. In response, central bankers have monetized even more debt through quantitative easing and have adopted zero, and recently, negative interest rate policies. These measures have pushed investors into riskier assets and pulled forward returns for both stock and bond markets. Or, said differently, they have lowered future returns for investor portfolios. Thus, we came home even more convicted that our key portfolio positions of being underweight stocks, overweight cash, and overweight investments with reliable cash flows makes sense.

As Mark wrote, the mood of the conference wasn’t exactly upbeat. However, there were some very positive topics several of the speakers touched on. My focus will be on one specific country that garnered significant attention and was brought up several times over the course of the week. This region is literally near—but probably furthest from dear—to our hearts. If you haven’t guessed yet, or couldn’t tell by the title, I am referring to Mexico. When most people hear Mexico, the unfortunate words that come to mind are drug trafficking, corruption, and illegal immigration. The current presidential race has sadly magnified this perception. For the last few years at Evergreen, we have followed the positive trends of the Mexican economy, despite popular perceptions to the contrary. This past week enhanced in my mind the encouraging future outlook for our neighbors down south. I hope to highlight the positive tailwinds their economy is enjoying, including a significant labor cost advantage, positive demographic trends, and what many are calling a manufacturing renaissance. My hope is that readers glean a few upbeat items about Mexico, hopefully improving their views of the 11th largest economy in the world.

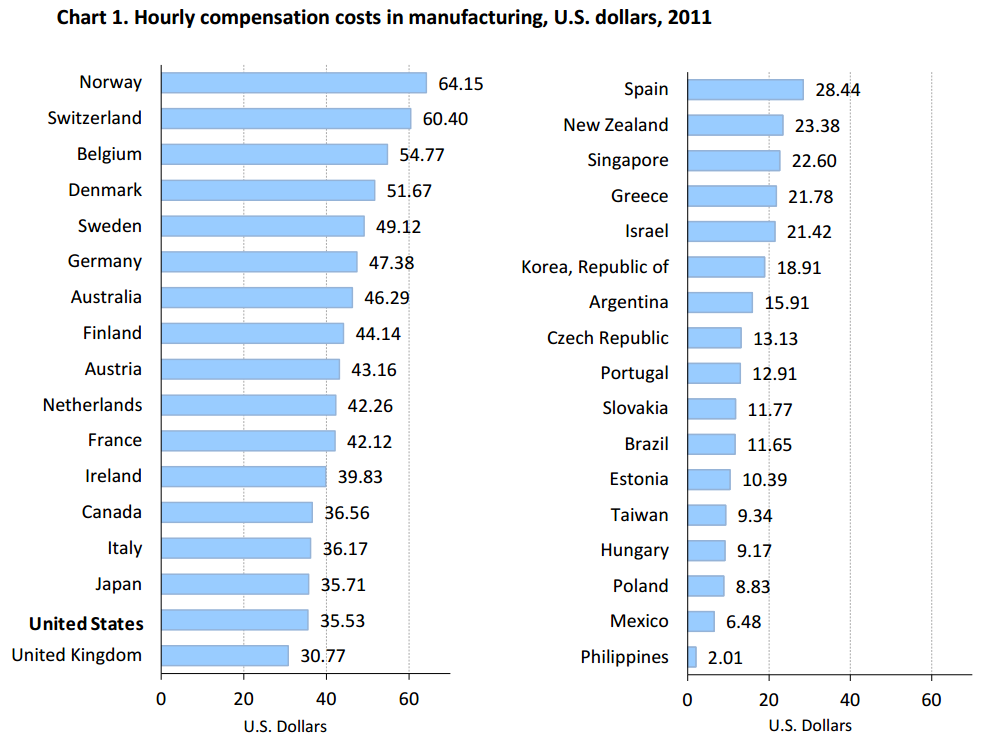

A country’s labor costs are a key input in determining its competitiveness on a global scale. Mexico in this regard is uber-competitive. As you can see in the table on the next page from the Bureau of Labor Statistics, hourly compensation costs in Mexico are roughly one-sixth to those in the US. Additionally, you can see that Mexico is more competitive than most countries in Latin America as well as versus Asia Pacific. One of the speakers we were fortunate to see, Dr. Pippa Malgrem, highlighted that the cost of labor in Mexico is now 20% cheaper than even China. Additionally, with Mexico’s prime location bordering the U.S., it puts them yet further ahead of the game when competing for exports to the US. We believe this is both a significant and durable competitive advantage for Mexico.

Source: Bureau of Labor Statistics, US Department of Labor

Mexico is also fortunate to have very favorable demographic trends. 86% of its population is under the age of 55, which compares to around 73% for the US. Additionally, more than 45% are under the age of 24, meaning Mexico will have a huge proportion of their population entering the labor force over the next 20 years. During this same time-frame, according to the US Census Bureau, the percent of Americans past the age of 65 is expected to grow from 14% to over 20%. A key theme from the speakers last week was that the developed world is aging and this will continue to be a drag on growth for these nations moving forward. In Mexico, on the other hand, demographics are likely to be a major tailwind.

The one-two punch of a lower cost of labor and positive demographics has led to a surge in foreign direct investment for new manufacturing in the region. Auto manufacturing is a prime example. General Motors, Ford, Volkswagen, Honda, Audi, Kia and Nissan have either opened, or are in the process of opening, manufacturing plants in various regions of Mexico. This has led to higher auto production in Mexico relative to the US. But, it’s not just auto manufacturing that has seen a massive surge. Companies in other industries such as General Electric, Bombardier, Alcoa and Honeywell are also moving into Mexico or expanding operations there. Initially, one would question whether Mexico truly had the quality of workers to fill these jobs, but a sobering stat, at least for the US, is that Mexico now produces more engineers per year than the US. The Mexican unemployment rate has moved down close to 4%, and so far, they have been able to fill these skilled positions.*

We had the pleasure of listening to Mexico’s secretary of agriculture, Jose Calzada, and his main message was continuing to improve relations with the US. He addressed immigration, drug trafficking, and corruption, and highlighted that, despite more work needing to be done, there has been significant headway. In fact, in terms of immigration there is now negative immigration to the US. Essentially, there are roughly 1.2 million Mexicans moving from the US back to Mexico each year relative to 800,000 coming into the US (maybe a bigger wall is needed to keep Mexicans from leaving the US!). Additionally, Mexico’s president Enrique Pena Nieto has continued to crack down on both corruption and illegal drugs through critical reforms. The mainstream perception is still poor in Mexico, but when you think about the widespread changes that are occurring they are certainly heading in the right trajectory. All of this has helped the Mexican economy grow at 3.2% annually since 2010 vs. just 2.1% for the US.

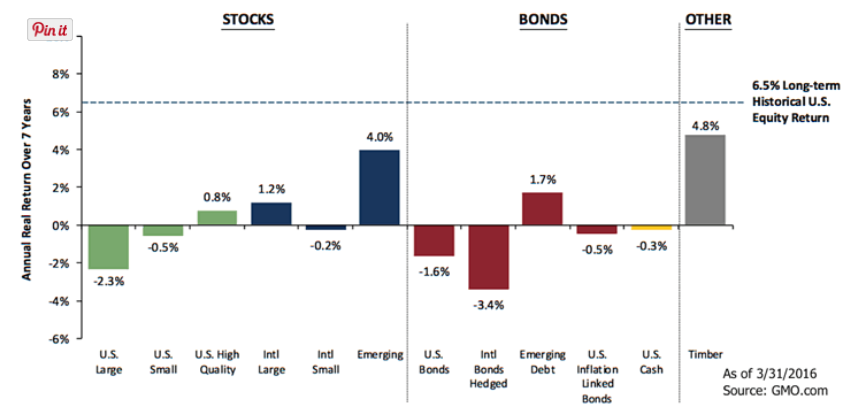

In terms of investment implications, we continue to believe that select emerging market debt will be one of the best areas to be invested in over the next several years. With 30% of the world’s government bonds yielding under 0%, we believe the current 6.1% yield on a 10-year Mexican government bond* is noteworthy. As you can see below, star forecasting firm GMO predicts emerging market debt over the next 7 years will have real (after-inflation) returns that exceed US government bonds by more than 3% per annum. We also think the Mexican peso, given its 35% fall relative to the dollar since 2014, looks undervalued, as well.

JEFF DICKS, CFA

Portfolio Director

To contact Jeff, email:

jdicks@evergreengavekal.com

*The specific securities identified and described do not represent all of the securities purchased, held, or sold for advisory clients, and you should not assume that investments in the securities were or will be profitable. General Motors, Ford, Volkswagen, Honda, Audi, Kia, Nissan, General Electric, Bombardier, Alcoa, and Honeywell are used only to illustrate well publicized events regarding these companies developments in Mexico. See important disclosures included following this letter.

**The California model of giving entitlements, drivers’ licenses, and, potentially, voting rights, to illegal immigrants does not qualify, in our minds, as “rational”.

In this edition of our EVA, I only have a couple pages to recap my takeaways from the Strategic Investment Conference (SIC), so I will attempt to be more concise than usual.

Below lists the main themes from SIC:

- Rates are too low and have been for too long.

- The lowest in history rates have made the rich richer but haven’t helped anyone else.

- Ultra-low rates don’t actually spur actual growth; look at Europe/Japan.

- Negative rates are a 50:50 probability to eventually land in US.

- We are trapped with too much debt.

- Gold is an insurance policy against inflation or deflation.

- There’s a widening income gap and a hollowing out of the middle class.

- Central bankers are viewed as omnipotent; in reality, they are impotent.

- We may be headed for a cashless society.

- Central banks have no idea what they are doing; they are also becoming increasingly desperate.

- Everyone’s favorite thing to own in today’s economy….cash. (Former Dallas Fed president Dick Fisher spoke and when asked to describe his personal portfolio positioning he replied: “Fetal.”)

So, a really upbeat conference! Sarcasm aside, the consensus viewpoint of speakers was that we are in trouble and central bankers cannot save us. To be fair, many of the voices heard at the conference weren’t what I would categorize as a group of optimists. However, many of them have made very prescient predictions over the years, making correct calls about the financial crisis, currency wars, secularly slower economic growth, etc. Negative? Sure. But they aren’t a bunch of fear mongering idiots. They have data, history, and logic underlying their cases. Many of them are super-successful and either directly control large asset pools or advise some of the wealthiest and most powerful people in the world with their investment decisions. It would be foolish to ignore them (and I like to believe that I’m no fool). So, I won’t ignore them. However, I will challenge their basic assumption.

I’ll grant them the fact that every single one of the concerns above may in fact occur or continue occurring. That’s okay because there’s hope. It comes in the form of a race. The race is between technological advancements, or progress, versus governmental interference. In developed countries, where most of the innovation is occurring, there are increasing regulations on businesses, high-risk monetary policy experimentation, and political systems that have left the masses grasping for anything non-consensus.

The legendary coach and announcer John Madden used to say, “In football, winning is a great deodorant.” It can cover up coaching mistakes, locker room unrest, and player deficiencies. In economics, growth is the great deodorant.

Now, many will point to the lackluster GDP growth and say, “What innovation?” But GDP is not a perfect measure of progress. GDP cannot measure health, free (or very inexpensive) access to amazing services (like GPS apps), or increased happiness. Profits aren’t a perfect metric, either. Amazon*, perhaps the fastest growing and most dominant company on the planet, has a profit chart that looks like the EKG line of a corpse. Today, we’ve entered permanently into a period of information overload. There’s enough data to spin whatever tale you want to tell.

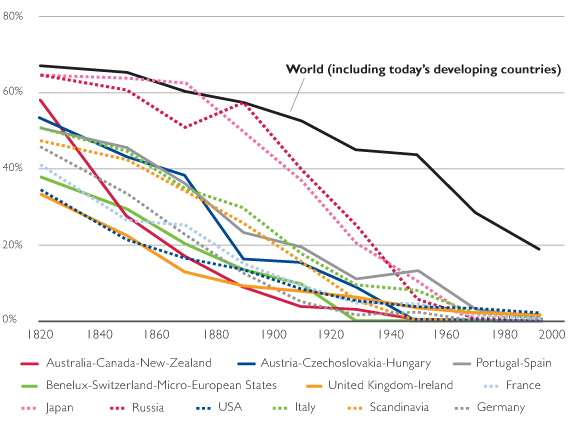

I think there are many of us who believe that we are at the end of the road of progress. There’s no doubt that political bungling on both sides of the aisle has derailed our train of economic growth and set us on a collision course with social unrest. But I want to approach the question of where we are going from a different angle. Isn’t today the best time to be alive? Life expectancy is up and infant mortality is down.Quality of life has improved in nearly every country. Information is more accessible. Communication with those we wish to interface with (or have to) has been made easier and a lot cheaper. More people are traveling than ever before. Most societies are more tolerant than at any other time in human history. I’ve included some charts that support many of the above statements.

% of People Living Below Poverty Line

Did you really need to see the charts to know this? At the dawn of WWII, wasn’t the outlook for the whole world far bleaker? In the US and Russia, at the height of the cold war, innocent children rehearsed the protocol of a nuclear launch. Wasn’t the future more frightening then? In frontier countries, where curable or preventable diseases were ravaging populations, enormous strides have been made. Looking back, I see a road of progress. Looking forward, I see more of the same—maybe even much more of the same.

Some may say the tone of SIC was bleak. Specifically, those who believe the central banks have put themselves between a rock and a hard place, but I disagree. There will be a painful unwind at some point as we deal with failed policies. The political scene in many developed nations has reached a tipping point. People are sick of the establishment. As hard decisions come down the pike, it’s likely that sacrifices will have to be made. Parties will be reshaped and new ideas will need to be forged. Debts will have to be reduced slowly over time or restructured quickly with steeper losses. All of these events could set off a chain reaction of uncertainty and fear within financial markets.

As people always do, they will extrapolate these fears and worries indefinitely into the future. For steady-handed investors, these events will present a chance to acquire assets on the cheap. The problem will be that whatever future problem we experience won’t be a replica of our last. Each time of uncertainty is particularly scary because it presents something unknown. History can serve as a guide but doesn’t alone hold the playbook. To quote Warren Buffett “If past history was all there was to the game, the richest people would be librarians.” So when the next crisis hits, tune out the noise, the fear, and the loud voices of gloom. Then bet that progress will win the race, as it always does—at least in America.

Please allow me to end with another quote. During times when our country seems to be rapidly heading in the wrong direction, it’s good to remember what Winston Churchill once said: “You can always count on Americans to do the right thing—once they’ve tried everything else.”

TYLER HAY

Chief Executive Officer

To contact Tyler, email:

thay@evergreengavekal.com

*The specific securitiy identified and described do not represent all of the securities purchased, held, or sold for advisory clients, and you should not assume that investments in the securities were or will be profitable. Amazon is used only as an example to illustrate a our belief of a change in the view of corporate profits among investors. Certain clients may hold Amazon in their accounts, at their discretion; this security is not a recommendation of Evergreen. Please see important disclosures included following this letter.

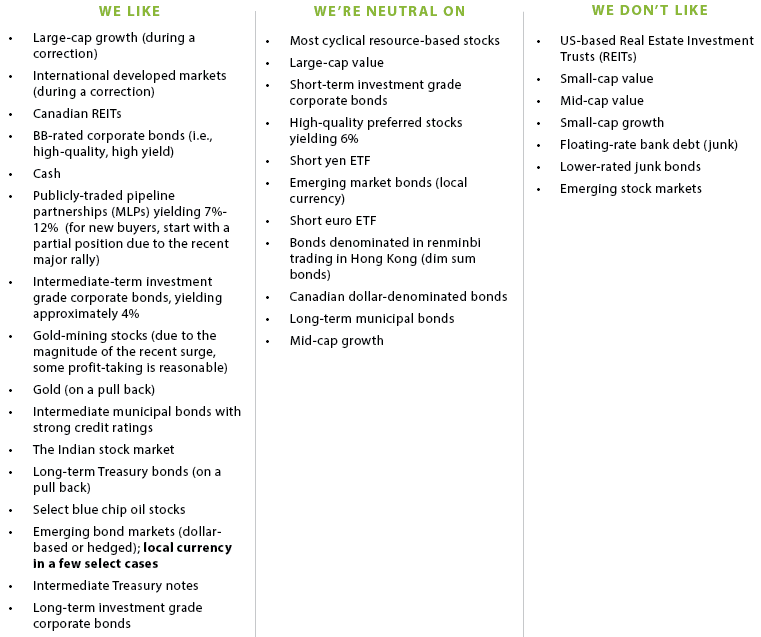

OUR LIKES/DISLIKES

Changes are bolded below.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Any specific securities mentioned in this piece are not necessarily held by evergreen and may not be purchased in the future. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.