“Hubris is one of the world’s greatest renewable resources.”

-Humorist P. J. O’Rourke

As indicated last week, this is the second installment of a two-part Evergreen Virtual Advisor (EVA)—Exchange version—dedicated to the Mauldin Economics’ Strategic Investment Conference (SIC). It was held in Dallas at the end of last month and for the three days we were there, the sun wasn’t. The clouds were thick, the air was heavy, and, on the last night, we experienced the worst thunderstorms this Left Coast boy has ever seen.

Inside, as relayed in the June 3rd EVA, the conditions were largely the same. Gloom was the dominant sentiment, despite the fact that the financial markets have been on a roll over the past three months. It’s been a long time since I felt like the token bull but my brief speech on why I felt the corporate bond market would now be supported by central banks gave me a bit of a Pollyanna sensation.

My short talk also generated a mild amount of controversy. Former Dallas Fed President Dick Fisher told the crowd on the final day that there was zero chance the Fed would emulate the ECB in buying corporate debt to lower credit spreads. Though I have the utmost respect for Mr. Fisher, I would love to take that wager (what would the odds be when the probability is zero?) However, we won’t know until the next crisis strikes which one of us is right. According to the majority of speakers we heard, we won’t have to wait very long.

As Mark Nicoletti expressed last week, perhaps that should be viewed as bullish indicator. Typically, such intense negativity means a bottom is close at hand. Yet, again, we are at record high prices for real estate, stocks, and high-grade bonds. Consequently, like so many things these days, it’s a most confusing state of affairs.

Besides my talk, there were certainly some other occasional rays of optimism, as Jeff Dicks noted last week in his piece on Mexico. And, as I will explain below, our esteemed colleague Anatole Kalestky was also a lonely—though eloquent voice—of bullishness. On the other hand, his partner Charles Gave, was every bit as persuasive that the façade of prosperity central banks have created is beginning to crack. In addition to having my first chance to speak at the SIC, I was also given the honor of interviewing Charles, as you will soon read.

But, before we get to that, Jeff Eulberg summarizes his perception of one of the most important factors in the investment world today: the future path of the US dollar. Like all of us, Jeff came away a bit bemused by all the contradictory opinions on the greenback he heard at the SIC. It’s possible, though, based on last week’s stunningly weak US jobs release, that we now have a clearer sense of the path of least resistance. (Hint: it isn’t up!)

David Hay

During his impressive presentation at last week’s SIC, Mark Yusko, the founder and Chief Investment Officer of Morgan Creek Capital Management, quoted a friend: “He longed for the days when he didn’t know the names of the world’s central bankers.” This statement struck a chord with me; it seems that forecasting the moves of the world’s central bankers is increasingly being used to achieve investment outperformance. I was amazed at the quantity of presentations at the SIC that focused on this topic. It seemed that nearly every question coming from the audience was focused on past mistakes of the world’s central bankers and the eventual direction of future policy decisions. Until recently, these policy decisions have played a large role in dictating the values of the world’s currencies. Central banks of struggling economies have sought to depreciate the value of their currency relative to rival countries, thus making their goods more attractive on the global marketplace.

In 2013, after years of quantitative easing designed to depreciate the value of the dollar, Ben Bernanke started to taper the program, reversing the dollar’s decline and sending it on a significant uptrend measured against a basket of global currencies. As we wrote extensively back then, this was a dramatic change for the global economy. As much as China would love to have an increasing share of global trade settled in its currency, the yuan (aka, the renminbi), over 80% of global trade is currently financed in US dollars. Therefore, the fallout of a significantly stronger dollar has had immense ramifications for the global economy, as well as for asset prices.

Over the last three years, the stronger dollar has played a significant role in sending oil prices down over 70%, causing commodities in general to decline over 45%, and S&P 500 earnings per share to drop more than 6% year-over-year. Further, throughout the developing world we’ve seen those emerging markets that have high US dollar-denominated debt experience crisis after crisis.

Yet, in the last few months, the dollar’s appreciation has subsided, triggering a substantial recovery in all of the risk assets mentioned above. Therefore, since every market participant seems to be focused on the next moves of the world’s central bankers, and with the high correlation seen with many asset classes to the dollar, forecasting the eventual direction of the US dollar may be the sole determinant to an outperforming portfolio in 2016.

Recently, our partner Louis Gave—who was one of the headline SIC speakers--wrote a succinct and well-thought-out piece on this topic for Gavekal Research titled Much Ado About Nothing. In it, Louis outlines three scenarios for the dollar.

1.) Economic data remains weak; the Fed sits on their hands; interest rates are not raised. (In this scenario the dollar likely depreciates.)

2.) The Fed hikes in the near future but remains dovish about future rate increases in 2016. (In this scenario the dollar would likely remain range-bound.)

3.) The Fed hikes and forecasts further rate hikes in the near future. (In this scenario, the dollar likely starts a new uptrend and the assets that have recently recovered—like energy—will turn back down.)

For the last 12 months, Evergreen, as well as our research partners at Gavekal, have been a few of the lone wolves calling for the dollar rally to end. After attending SIC, and as Louis mentions in his piece, it seems that the consensus is that Scenario 3 is inevitable. Our good friend, Grant Williams, founder of RealVision TV and author of Things That Make You Go Hmmm, is firmly in that camp. During Grant’s panel discussion at the conference, he expressed his belief that the dollar rally is merely taking a breather and the ascent is about to regain steam. Brian Lockhart, the Chief Investment Officer of Peak Capital Management, took it one step further and proclaimed that the Fed will not only raise interest rates in June, they will also raise rates two more times in 2016. If that does happen—with no other central bank even close to raising interest rates, and in spite of the increasing US trade deficit—the dollar rally would likely induce a considerable unwinding of recent gains seen in energy, gold, commodities, and emerging markets.

Honestly, I left the conference conflicted: My contrarian nature leads me to want to believe that the dollar has peaked and the best values lie in the non-consensus camp of dollar weakness. However, I struggle with the simple notion that the Fed appears to be the only central bank even considering a tightening of monetary policy. I think we’re entering a period where economic data will actually dictate the underlying price of assets. If US economic data is strong, the Fed will raise interest rates, sending the dollar higher and US earnings per share lower. And, with an already expensive equity market, multiple expansion is unlikely from here. If US economic data remains weak, which was the case last Friday when the worst jobs report since 2010 was released, the Fed will back off and markets will maintain a tight trading range for a while. However, as Charles Gave noted in his excellent presentation at SIC, a US recession is far from off the table. Ultimately, whether it’s a US recession or a significantly higher dollar, I see no valid argument that US equity prices offer reasonable value in any scenario. Thus, I walked away from the conference realizing I need to keep a keen eye on both economic data and the US dollar while continuing to recommend a defensive portfolio structure. As Charles stated in his presentation, the goal should now be to build a portfolio that will get you through to the other side of the next crisis. Because that rings true to me, I don’t see the logic of having a full allocation to US stocks, especially considering near record-high valuations combined with a world that is becoming riskier, not safer.

Director of Wealth Management

To contact Jeff, email: jeulberg@evergreengavekal.com

As even intermittent EVA readers are likely aware, Charles Gave is one of my intellectual heroes. Accordingly, it was definitely one of my career highlights when I interviewed him last week for my dear friend Grant Williams and his Real Vision TV (RVTV) while we were at the Mauldin SIC.*

The fact that the “kal” in Gavekal—the influential London-based economist, Anatole Kaletsky—was also in attendance created an interesting juxtaposition. The reason I use that term is because, from a philosophy of finance standpoint, Charles and his longtime friend and partner couldn’t be further apart. While Charles is cut from the Austrian School of Economics’ cloth, Anatole is a self-described Keynesian.

For those to whom these distinctions are unclear, “Austrian” economists believe in sound money, high savings and investment, and the judicious use of debt; in other words, pretty much the antithesis of the policies the world has been following for most of this young century/millennium. The opposite end of the spectrum is occupied by the followers of John Maynard Keynes—hence, the term “Keynesians”. They believe the answer to economic malaise is creating increased demand, such as through larger government deficits and ultra-easy monetary policies. Essentially, they advocate any measures that stimulate spending with little regard for investment returns and their belief system has dominated, particularly since the global financial crisis.

Both Charles and Anatole spoke to the 700 or so in attendance at last week’s SIC. In fact, the former presented immediately after the latter (a tad miffed that Anatole left him with only a few minutes to make his case). Suffice to say, the contrast was striking. Even VERY intermittent readers of this newsletter undoubtedly realize I personally lean much further toward the views of Charles than those of his Keynesian partner. However, I have to admit that every time I listen to Anatole he makes a highly persuasive case for why the exceptionally extreme policies being pursued by many so-called advanced countries—like negative interest rates—actually make sense.

Regardless of my personal biases—and despite Anatole’s extremely articulate defense of developed world central banks--the accumulating evidence would seem to favor Charles’ mindset. To wit: global growth rates remain in a wicked bear market; likewise, productivity is trending in a decidedly southerly direction; it’s taking ever-larger amounts of debt to produce the same amount of GDP increase; large swaths of most developed countries remain un- or under-employed; and it’s becoming increasingly obvious—even to politicians—that there isn’t enough wealth being created to fund the coming tsunami of entitlement spending. There’s little doubt that all of the above—plus much more, such as rising economic inequality—is why Far Left and Far Right political candidates are growing in popularity throughout most of the “advanced” world (whose politics now seem anything but).

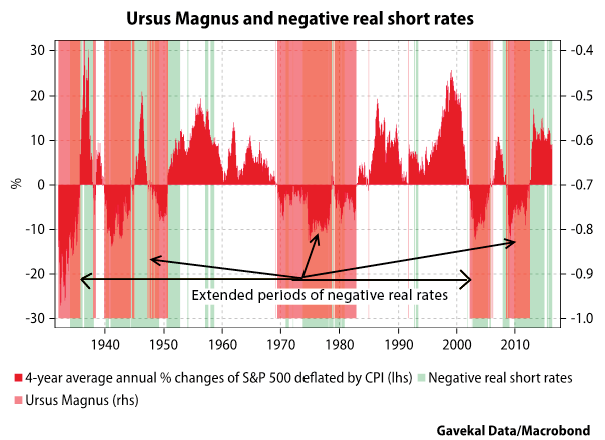

Defenders of the Keynesian approach like to point out that buoyant stock markets, at least in the US, seem to be prima facie evidence that their solution-set is working. Yet, as Charles expressed to me in our interview, the evidence is to the contrary—at least taking a longer view. Per his chart below, he notes that all of the worst bear markets have occurred during periods when interest, adjusted for inflation (i.e., real rates), have been negative. He remains extremely concerned we’ve got another of what he calls an “Ursus Magnus” (i.e., Whopper Bear) market in our not too distant future.

He also noted to me that the unprecedented debt build up and the constant movement to low, then zero, and, now, in much of the world, negative interest rates, has coincided with the worst economic expansion in post-WWII history. He has documented that periods of negative real rates have been consistently associated with long stretches of anemic growth. (I would also point out to readers that Ned Davis Research has verified this.) His view is that interest rates are paid to compensate savers for future uncertainty. Negative interest rates, therefore, must mean that the future is more certain than the present, which, in his words, is total idiocy.

Charles has written extensively on what he calls “the high cost of free money”. He believes that because central banks have pushed short-term interest rates below the natural growth rate of the economy, they are hurting, not helping. Based on the fact that nominal GDP (real GDP plus inflation) has been running at roughly half of its typical pace would seem to validate his concerns.

He also is worried that, contrary to popular belief, US long-term corporate borrowing rates are too high. With nominal GDP increasing at a mere 3.3% (versus an average non-recession rate from 1990 to 2007 of around 6%) and 15-year BBB bond yields at 5.2%, he is making a point many are overlooking. Consequently, lots of money is borrowed short-term to speculate (like through 1% margin rates offered by some brokers). Yet, at the same time, the long-term cost of capital for US companies is almost double the growth rate of the economy, discouraging capital investment. This may help explain why both “cap ex” and productivity are in such steep multi-year downtrends.*

Charles further told me in our chat that he didn’t take comfort in the fact that the majority of economists are not predicting a recession. As he observed, and history makes uncomfortably clear for that profession, the economics community at large has brilliantly failed to anticipate every single prior downturn.

Similarly, Charles’ concerns are not assuaged by the same consensus that tells us not to worry even though Corporate America is in an earnings recession or that the industrial sector appears to be contracting, as well. He disagrees with the cheery dismissal that these are irrelevant in a service-based economy, pointing out that manufacturing tends to lead the consumer economy.

Charles and I also spent some time discussing an emerging new “magic bullet” theory being pushed by many of the Keynesian persuasion. This involves the idea that central banks can simply cancel out accumulated national debt by creating even more fabricated reserves, buying their government bonds, and locking them away forever on their balance sheets. As I have argued in these pages, that “sounds too good to be true” thesis is a Faustian bargain. Either it leads to more of the stagnation we’ve seen for years (as money velocity continues to crash) or, should the trillions of reserves presently lying idle begin to circulate, virulent inflation. Charles concurred with this two-track scenario, both heading to unpleasant destinations.

He also relayed a conversation he had recently with an individual who not long ago was head of one of the world’s most important central banks. When Charles asked this gentleman what philosophy was guiding the Fed currently, he was told: “The S&P 500 over the next week.” In other words, propping up stock prices is Job One at the Fed these days.

It’s my contention that the question of whether Charles or Anatole are right is of the utmost importance. If it’s the former, we are on totally the wrong path and investment portfolios need to reflect that (such as with healthy portions of cash, treasuries, and gold). If it’s the latter, then the global economy should finally emerge from its long quasi-coma and stocks may well remain in a bull market (though even Anatole believes there is much more upside in overseas equities).

Ladies and gentlemen: place your bets. And place them very carefully.

*Due to the fact that it is nearly impossible to do justice to this interview in a two-page summary, we will be sending the full video version to EVA readers at a later date.

Chief Investment Officer

To contact Dave, email: dhay@evergreengavekal.com

OUR LIKES/DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Any specific securities mentioned in this piece are not necessarily held by evergreen and may not be purchased in the future. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.