With the 2020 US Presidential election fast-approaching, many investors are likely wondering how November's election results will shape markets and the economy in the months and years ahead. In this quarter's version of Evergreen Roundtable, we are offering different viewpoints from several members of our investment team on six important questions related to the 2020 US Presidential election:

Evergreen’s investment decisions are not made by any single individual. Instead, our team confers nearly every business day to discuss our various investment strategies. This team consists of people with very different lenses through which they view the world and, oftentimes, these daily investment discussions become quite “spirited.” We foster the competition of ideas. Evidence and logic outweigh seniority or rank.

Jeff Eulberg (Managing Director, Family Office, Partner), Jeff Dicks (Director of Portfolio Management), Tyler Hay (Chief Executive Officer), and Mark Nicoletti (Managing Director, Family Office) all weigh in on this special edition newsletter. As always, we welcome your feedback and appreciate your loyal readership.

Tyler Hay

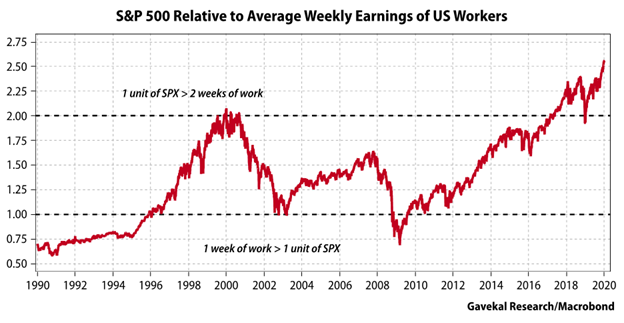

Many investors are counting on the presidential election to be a pivotal event for equity markets. This may be true in some areas, but as a whole, I think this viewpoint misses the mark. Instead, I’ve directed my focus to the effects of fiscal versus monetary policy. Said more simply: the stock market has returned on average 14.5% per year from 2009-2019, while over the same time period, workers’ wages have only increased 2.9%. Meaning Wall Street and those people who own assets (real estate, stocks, bonds, etc.) have seen a massive surge in wealth following the Great Recession while the average worker has been left in the dust.

Regardless of which candidate wins, either will almost certainly be forced to face this reality. I can think of a number of ways whoever is elected may choose to address this growing wealth gap. There’s a punitive approach, in which you try to slow down the success of the “winners”. This could manifest itself in raising taxes on the wealthy. The reason that I think a “wealth tax” is likely is that Biden’s most recent tax plan clearly looks to be headed in this direction. Another punitive approach would be the pursuit of antitrust regulations aimed at some of the tech giants. While the merits of antitrust regulation or higher taxes should remain a topic for another day, the pursuit of either policy would likely not be welcomed news for the stock market. More benign tactics to address the disparity in wealth could be an increase in the minimum wage, a universal basic income, and a national infrastructure upgrade similar to Roosevelt’s WPA, or Works Progress Administration, a key part of his New Deal. (The latter being most pragmatic in my view.) Instead of focusing on who wins the election, I’d advise investors to focus on how each candidate proposes tackling the growing wealth gap, which is the real elephant in the room for markets.

Mark Nicoletti

Should the President prevail in November, the original post-Hilary ‘Trump trade’ from four years ago will probably still hold this time. Which stocks are poised to do well on the premise of tax cuts and deregulation? Financials, energy, and more broadly value stocks, should thrive. However, this rosy scenario carries one major potential asterisk: a re-escalation in the trade war with China. Post a Trump re-election, the dollar will likely strengthen temporarily, as it did four years ago.

The Biden trade, as stated above, hinges in my opinion on the presumption of a Blue Wave. His plan to raise corporate taxes from 21% to 28% is, and should be, one of any prudent investor’s major concerns. His policies would be bullish for publicly- traded pass-through tax entities, including REITs (which are not required to pay corporate taxes). If you examine how stocks have been moving this summer in response to odds for a Biden victory, it’s telling. Relative to the market as a whole, technology, consumer discretionary, communication services, and healthcare have all outperformed when the polls have favored Biden. Meanwhile, financials, industrials, and energy have all tended to move inversely. This scenario is the exact opposite of what happened after the Trump victory in November ’16 when cyclical stocks outperformed and defensive sectors (excluding tech) lagged behind.

Mark Nicoletti

As do most of my peers, in some way or another, I interface with our firm’s clients on a regular basis. My unscientific opinion is that there are three predominant issues on the minds of our client base. They are, in order of concern: 1) The election 2)The pandemic 3)The Fed’s policies.

Although I’ve definitely learned more from our clients than they have from me over the years, I would argue these sentiment readings are in reverse order to the threat they potentially pose to portfolios.

Among them, I believe the Fed’s easing policies (still) have the most potential impact on asset prices, followed by the backdrop of the ongoing pandemic, and lastly the election results. I’m not suggesting the markets won’t rally on a Trump victory or a working vaccine coming to market - they probably will. I’m also not suggesting investors shouldn’t prepare as effectively as possible for the upcoming election - they absolutely should. I’m simply suggesting that, although political uncertainty will always cause market volatility, the fundamental impact of a Biden victory is not the most critical market input.

The reality is that Biden’s manifesto contains multiple policies that could safely be described as business-unfriendly, such as tax increases and regulation, which can weigh on corporate profitability. However, this same manifesto is also likely to include additional rounds of fiscal stimulus. While I acknowledge the likelihood of a negative short-term impact on risk assets resulting from a Biden victory, I think it might be short-lived.

Time will tell.

This election comes at one of the more turbulent times America and, indeed, the world has seen in decades. The ongoing pandemic, social unrest, and bipartisanship are (or should be) all clear concerns, but, given the fact that an unprecedented number of Americans are expected to vote by mail, there is a material risk that any election result is contested. That sort of chaos, which I’d call likely, is almost certain to cause a market selloff. During the 5-week Bush-Gore fiasco in 2000, the market dropped 12%.

Jeff Eulberg

In order to anticipate market swings, we must first do our best to understand current market expectations. Depending on the National poll, Biden holds anywhere from a 4% to 10% lead over Donald Trump. Yet, important swing states are much tighter, and the electoral map is far from a slam dunk for Biden. Beyond paying close attention to the races in those key states, we also look at gambling markets where bettors are truly putting their money where their mouths are. Currently, Biden has a slight lead at -135 (bet $135 to win $100) to Trump at -110 (bet $110 to win $100).

Over the last six months, the market rally has coincided with Biden’s polling gains. This could lead one to conclude that investors aren’t concerned about a Biden presidency. I would argue that the market might not be alarmed due to the potential change in the executive branch but would become much more concerned if the Republicans were likely to lose control of the Senate, too. In the Senate, the Democrats need to keep their current seats and flip three others from the GOP. Four races are seen as competitive for incumbent republicans (North Carolina, Maine, Arizona, and Colorado). Meanwhile, the Democrats are fighting to maintain a seat from Alabama in a state where Trump won by more than 29% in 2016. At this point, I believe the Senate will remain controlled by the GOP, thus, I don’t anticipate a lasting market sell-off due to the Presidential election results.

If Biden wins the election and the Senate was to flip to the Democrats, I would anticipate a short-term market sell-off. The market would foresee higher taxes and increased regulations, obviously not conducive to higher earnings. Ultimately, I wouldn’t recommend selling equities in any of the above scenarios. I’ve long believed that adjusting your allocations due to a change in the Presidency is misguided. While Biden would like to raise taxes, he’s unlikely to do so in the middle of a recession. And, if he does, that would lead to a challenging mid-term in 2022 and could swing the Senate back to the conservatives. Regardless of who wins in 2020, the market environment for the next 4 years will be very challenging. The next President will have a tremendous amount of work to do to get the economy moving in the right direction and current market valuations don’t leave much room for error.

Tyler Hay

My previous answer could have easily been copied here (as I do think it’s the most important long-term issue facing our country). That being said, I do not think the wealth gap is the most urgent matter the next POTUS will face. We are now nine months into this global pandemic and so much uncertainty remains, such as:

I think it’s wildly optimistic to assume that this Pandemic will be turned off like the flip of a switch, instead it’s more likely to dim over time. In the meantime, the economy, particularly in certain areas, is being decimated. It goes without saying that no president wants to preside over a flagging economy. The approach we’ve taken so far has been the equivalent of trying to hold our breath underwater; eventually, we have to come up for air. Therefore, the next 4 years will largely be defined by how the next POTUS navigates this ongoing virus crisis.

Jeff Eulberg

The most important issue for the next President will be managing the impact of the Coronavirus. If we can’t keep our hospital systems from being overwhelmed, it will be all but impossible to achieve much else during the term. If corona is managed, the next most important task will be reviving the U.S. economy. While always a top concern, the pandemic has amplified this need with over 11 million Americans currently out of work, along with the steepest decline of Gross Domestic Product (GDP) in history. At this point, we have no idea how society will adjust to our new normal. What jobs have been lost permanently? To compound issues, the next President will be tasked with achieving this goal as the nation is more divided than any time in my lifetime.

As I highlighted in my market reaction discussion, I don’t currently believe the Democrats will be able to gain control of the Senate, leaving either President with a split congress. And, much like the US population, Congress is also incredibly divided and unable to find much common ground (see: the long-awaited stimulus package 2.0). Therefore, it will be an uphill battle for either to make sweeping changes in an effort to jump-start the US economy.

One bipartisan idea that will likely be implemented is a large infrastructure spending bill. From an investment perspective, this would lead us to look at cyclical companies that would benefit from such a package. Fortunately, many of these companies currently offer attractive valuations, especially relative to some of the highflyers of the last 6 months.

Mark Nicoletti

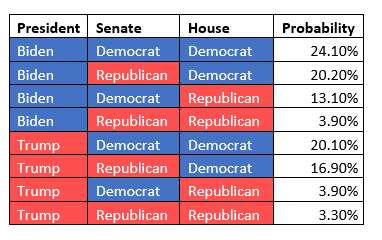

There are four plausible electoral scenarios, two of which result in a unified government. The impact of divided vs. unified government is enormous; and probably a better predictor of future policy change than which candidate prevails.

Historically, election platform policies often struggle to become legislation but this time around, there is plenty at stake. Tax reform, broader regulation, and COVID-19 related responses, among others, are all potential battlegrounds.

This notwithstanding, the potential for a unified Democratic government is greater than in recent years, and probably the only scenario worthy of dissection. It’s quite possible voters view Biden and the Dems as more trustworthy on healthcare reform and possessing greater ability to navigate a second wave of Covid-19.

If victorious with a Blue Wave tailwind, Joe Biden will seek to increase spending on climate change mitigation, expand federal-funded healthcare, and raise taxes on corporations and high-income earners. The initial investment implications of this scenario will undoubtedly focus on taxes and the negative business sentiment more regulation will bring. The longer-term scenarios to be weighed are almost certainly climate policy and energy efficiency, and the corresponding winners and losers due to changes in both.

Jeff Dicks

One way to calculate the odds of a unified government is to simply look at the betting odds for the President, the House, and the Senate. According to www.electionbettingodds.com, the odds of Republicans taking the presidency, controlling the Senate, and controlling the House, are 44.3%, 45.5%, and 16.3% respectively. For all three of these events to occur, we can multiply each of them together, which works out to 3.29% odds of a Republican sweep. At the Kentucky Derby, this would be like betting on a 30-1 longshot, which can happen, but not very often. In that scenario, in terms of policy reform, it would be very much a continuation of what we have seen the last four years. On the tax side, the Republicans have floated an unspecified tax cut for individuals. In addition, there would be a potential tax credit for moving manufacturing abroad to America, with extra emphasis on bringing manufacturing jobs from China to the US. These firms would potentially be able to deduct 100% of expenses to hopefully incentivize the shift stateside. Within Trump’s second term agenda, there would be a focus on lowering prescription drug prices and attempting to reduce insurance premiums. We’d also likely see a continuation of the tough stance against illegal immigration, a refunding of our police, and continued deregulation of the energy industry. Donald Trump’s second term agenda can be found via the following link. The agenda is rather ambitious but was a bit lacking in terms of actual details surrounding key objectives in another term. As mentioned, at this point, a Republican sweep appears unlikely, but elections in the past have been difficult to call and predict.

The flip side shows the odds of the Democrats winning the Presidency, the Senate, and the House at 53.1%, 54.4%, and 83.60% respectively. This works out to a 24.15% chance of a Democrat sweep. Out of any combination, a Blue sweep currently commands the best odds. However, some sort of split would be the most likely over a united government at over 70%, given the 24% odds and 3% odds of a Democratic and Republican sweep respectively. The policy shift under a Blue sweep would be significant since there are limited barriers to implementing these policies. The Biden administration would look to unwind most of the tax cuts under the Tax Cuts and Jobs Act. For instance, Biden has proposed raising the corporate tax rate to 28% from 21% (this was lowered from 35% to 21% under President Trump). In addition, Biden would look to raise taxes on the individual side and to increase the capital gains tax for high-income earners to the ordinary income rate. Biden would also look to expand health care coverage, and like Trump, look to lower healthcare costs. The Democrats’ platform would prioritize climate change via restriction on the energy industry and expansion in terms of pro-renewable energy policy (see energy response below). Overall, stricter regulation is expected across most industries with this impact being felt most acutely among financials, pharmaceuticals, and even technology. A Blue wave would be less restrictive on immigration, along with dialing back the Trump administration’s travel and immigration bans, reinstating protections for “dreamers,” and rescinding funding for a border wall. Finally, an infrastructure spending bill would likely get passed, which appears to have bipartisan support. From a financial markets perspective, that corporate tax increase may be the most market-moving item under this scenario. RBC capital markets estimates the proposed increase would likely fall 5.5%-10% with higher corporate taxes.

Here are the odds of each scenario currently bases on the current odds.

Jeff Dicks

US energy policy would be one area that would see a rather large shift under a Biden presidency. Day 1 President Biden has publicly stated he will restrict new oil and gas drilling on federal lands and waters. It’s worth noting this is a much scaled-down ban relative to what was floated by Elizabeth Warren, which proposed banning all drilling on federal lands. A few points here would be that producers will likely move to other regions where production is primarily on private lands, as well as stockpile public land permits ahead of Biden taking office. With that said, this policy will restrict energy production in the US relative to current policy. With the collapse in energy prices due to Covid-19, we have seen a major reduction in capital expenditures across the energy industry both in the US and abroad. Further restriction on production likely would lead to higher energy prices over the near-to-medium term. We believe the beneficiary of lower US production would be international energy producers that can make up the production shortfall, as well as benefit from higher prices.

Biden will also make a big shift to becoming net-zero carbon emissions by 2050. Getting our country there will require companies to carry the cost of the pollution being emitted, which likely lowers the profitability profile for corporate America. Along these lines, Biden will rejoin the Paris Climate Agreement and make a push towards limiting carbon emissions internationally. In the US, as we have continued to shift away from coal to natural gas and renewables, we have seen CO2 emissions per capita go down since 1970. Globally, a critical aspect of reducing carbon emissions is shifting countries like China away from coal. China makes up over 28% of carbon emissions, and per capita emissions have more than tripled in China since 1980. We would point out that regardless of the President, this is a very important shift that needs to take place. This is also a shift that will benefit companies exposed to producing and transporting natural gas in the US. We feel this trend will be critically important for our environment, and also a smart place to allocate capital over the next 20 years.

Biden has expressed the desire to make a very large investment into clean energy, which would expand the power generating capacity in areas like wind and solar. It will be important to allocate funds efficiently given many European countries have seen higher electricity costs from similar programs. With that said, it’s been promising to see that many areas across the country have seen dramatically lower costs for clean energy. From an investment standpoint, we have continued to increase our exposure to companies tied to clean energy, and under a Biden presidency, we believe this area would gain shares against traditional energy power generation. Ultimately, we would expect to continue to allocate a larger proportion of our clients’ assets in companies that benefit from this trend.

Jeff Eulberg

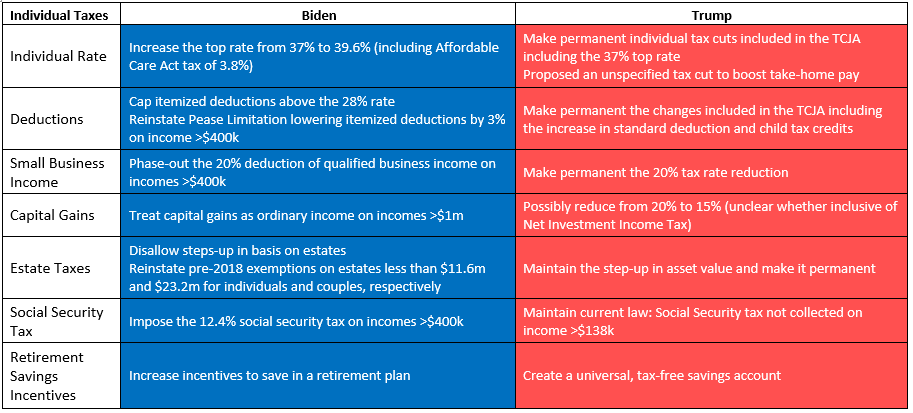

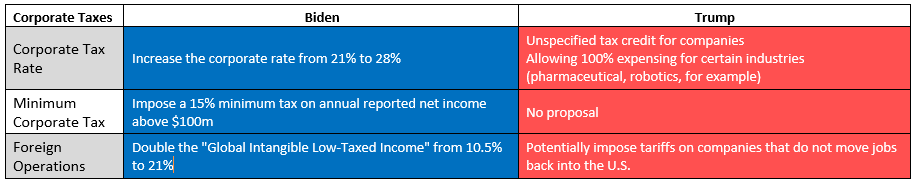

The table above outlines the key differences in both tax plans. Biden is campaigning to roll back several of Trump’s recent tax changes. However, what Biden wants to do and what he can do are two very different things. As mentioned in all of my answers for this piece, without the Democrats flipping the Senate, many of these proposals will never be implemented. Further, even if the Democrats can flip the Senate, Biden is unlikely to make an aggressive attempt to raise taxes with so many Americans unemployed and the economy just starting its recovery process. If a major tax hike was implemented, the low hanging fruit for the Democrats would be to raise taxes on two smaller voting groups - the wealthy and corporations.

I would anticipate a corporate tax increase to at least 28%. From an economic standpoint, Evergreen has written several times that the Trump administration’s dramatic corporate tax rate cut in 2017, when the economy was in a strong growth phase, was misguided. Most disturbingly, it led to unprecedented deficits during good economic times. Thus, while a partial reversal will certainly impact earnings, longer-term it wouldn’t appear to be a catastrophic shift.

Wealthy individuals could see increased ordinary income and capital gain rates with meaningful estate tax adjustments. In 2017, we were shocked to see the Federal estate tax exemption go from just over $5.6m to $11.2m. If a new tax bill was to pass, these increases will very likely be rolled back before they’re set to lapse in 2025. If we get closer to November and it appears that the Democrats are likely to flip the Senate, you can expect us to advise on potential estate tax techniques to utilize the higher exemptions, recommend liquidating concentrated long-term gain positions and pulling income forward to 2020. That said, for now, much of the tax increase concern might be a bit overblown and an inevitable outcome of election season rhetoric.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.