“Whenever you find yourself on the side of the majority, it is time to pause and reflect.”

-Mark Twain

Last week’s EVA gave readers a healthy dose of Charles Gave. In this edition, we are highlighting some recent insights from his son, and Gavekal’s founder, Louis Gave.

Louis is one of the most innately upbeat individuals I know. Accordingly, when he is concerned it leads me to believe my caution isn’t just a function of advancing years (and, some might say, advancing senility). As befitting his preternaturally sunny disposition, Louis isn’t bearish; he just believes the risk/reward proposition for stock prices is much more attractive outside of the US, particularly in Asia.

Yet, as you will read, even Louis concedes that should a serious economic or financial market disruption hit the US, it will be very difficult for Asian stocks to avoid collateral damage. But it’s hard to get badly hurt when you are falling out of a basement window. And Asia’s stock markets have clearly been cellar-dwellers since 2012.

Four years seems like an eternity these days even though it really wasn’t that long ago when investors were gaga over emerging markets and, at the same time, resoundingly apathetic toward home-grown shares. Today, the majority view seems to be that the US will continue to be the planet’s equity market pacesetter. The consensus also appears convinced that Asian stocks will stay in the deep freeze with investors particularly negative on China and Japan, two of Asia’s most important markets. However, that same dismissive attitude prevailed toward gold mining shares right before they did their recent moon-shot. If you haven’t noticed, mood swings happen very suddenly of late.

Therefore, please keep an open mind and let Louis make his case for putting some Asian cuisine on your investment menu.

Beyond doubt, last weekend delivered its fair share of stomach-knotting news: from the shocking, and depressingly familiar, terrorist attack in Florida, to the surge in UK opinion polls in favor of a Brexit vote (perhaps reminiscent of 2014’s pre-referendum surge in favor of Scottish independence? or something deeper?), to the new lows in OECD* government bond yields, to the confirmation that two candidates with 60% negative approval ratings are now heading the US presidential tickets, to the growing realization that China is becoming ever more assertive in its greater neighborhood. In short, there are plenty of reasons to explain why, all of sudden, European and Japanese equities are down 8% and 10%, respectively, in local currency terms for the month to date. So what investment conclusions should we draw from this latest market hiccup?

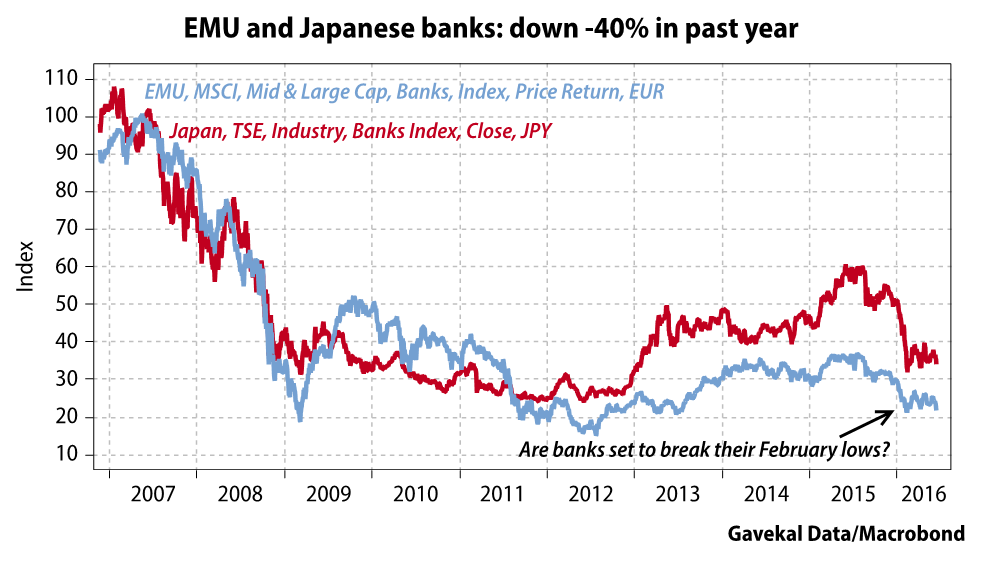

The first observation is that bank stocks in Japan and Europe are leading the markets lower. This is troubling, as the relative performance of bank shares has generally been an important leading indicator of broader financial health. Simply put, for a bull market to have legs, the banks usually need to participate in the party. Unfortunately today, either by mistake or by design, policymakers seem to be slowly walking banks either towards irrelevance, or alternatively nationalization.

The second observation is how quiet the foreign exchange markets have been in the face of this latest sell-off. Following the global financial crisis, the Pavlovian reflex of markets was to bid up the US dollar whenever global risk assets moved into “risk-off” mode. In recent months, this “weak equities-strong US dollar” relationship has broken down. Even the British pound (priced in dollars), which arguably should have suffered as heavily as global equity markets in recent days, has held up relatively well. This inability of the US dollar to push higher on a stream of bad news reinforces my core belief that the US dollar is done rising.

The second observation is how quiet the foreign exchange markets have been in the face of this latest sell-off. Following the global financial crisis, the Pavlovian reflex of markets was to bid up the US dollar whenever global risk assets moved into “risk-off” mode. In recent months, this “weak equities-strong US dollar” relationship has broken down. Even the British pound (priced in dollars), which arguably should have suffered as heavily as global equity markets in recent days, has held up relatively well. This inability of the US dollar to push higher on a stream of bad news reinforces my core belief that the US dollar is done rising.

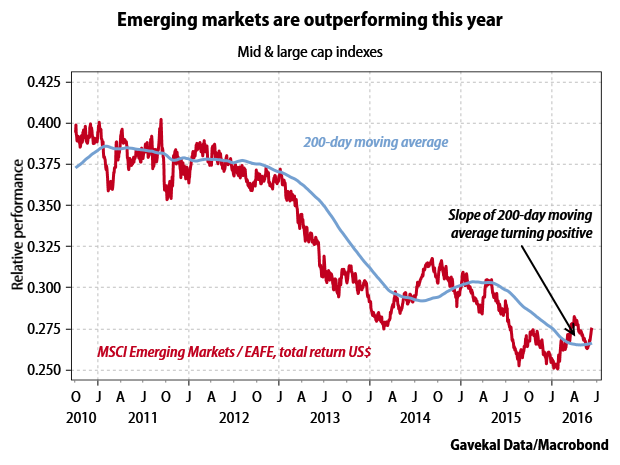

Which brings me to the third observation, namely the 8% year-to-date outperformance of emerging markets against MSCI EAFE**, and the fact that in the recent sell-off, emerging markets have broadly held their own. To most investors, this seems unusual; after all, over the past five years, not only have emerging markets been dogs, they have been volatile dogs to boot. In a typical market “risk-off” period, one expects emerging markets to fall more than others. However, so far in June, this does not seem to be happening. Take Asia as an example: In US dollar terms, Taiwan, Indonesia, Thailand, and Singapore are all up, while Korea, Malaysia and India are down minimally, (Hong Kong and Chinese H-shares are faring worse at minus 3% but are still outperforming Europe and Japan this month).

Behind this relative stability of emerging markets lie four realities. 1) The US dollar’s failure to break out to new highs is great news for emerging markets. 2) Emerging markets, unlike developed markets, are benefiting powerfully from falling long-term domestic interest rates. 3) Unlike in developed markets, emerging markets risk premiums tend to be on the high side of their historical ranges***. 4) Fiscal easing, notably in China but also in India, the Philippines, Indonesia and Argentina, bodes well for earnings. What market does not like the combination of easier monetary and fiscal policies?

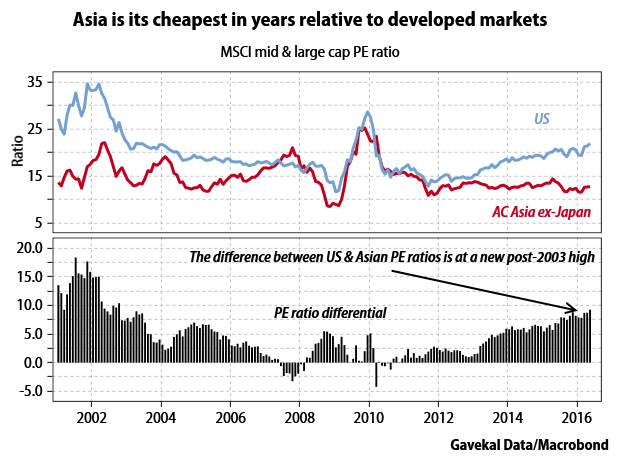

This last point brings me to another question facing equity investors. On the one hand everything seems to favor an overweight position in Asian equities: attractive valuations, easier monetary and fiscal policies, a broad lack of political uncertainty, a US dollar that is no longer rising, and very conservative foreign investor positioning. On the other hand, the highly cyclical nature of Asian earnings means that regional markets have historically fared poorly in periods of weak US market performance, and even worse in periods of weak OECD economic growth. Hence today’s quandary: Can US, European and Japanese equity markets withstand uncertain domestic political environments, meek global growth, and stretched valuations, thereby allowing a bull market to unfold elsewhere, notably in Asia? It happened in 2003, and perhaps the recent market moves indicate that we are set for a repeat of such Asian outperformance. After all, the valuation gap between Asian and Western markets today stands mighty close to 2003 levels.

Unquestionably, though the largest Asian market—China—has to climb the Great Wall of Worry. Underscoring this angst, in a recent meeting with a British pension fund manager in our HK office I attempted to tackle the vexing question of the past decade’s large increase in Chinese debt, and whether China would soon confront a debt crisis. And although I firmly believe that it is not on the path to financial perdition, the case for the prosecution is strong enough that our conversation lasted for a good hour. Still, as we went through the motions of discussing China’s current “predicament” (personally speaking, I don’t see much of a predicament as I tend to like undervalued markets where the policy makers are embarking on easier fiscal and monetary policies), I could not help but feel that too many investors are like French WWI generals, always focusing on the last battle, instead of the next one. Indeed, because this past August and January market hiccups were driven by China, investors today are fearing more of the same. Instead, it seems increasingly likely that the pain will come from elsewhere. And funnily enough, the client across the table was drawing the same conclusion at the same time I was. Indeed, as the meeting concluded, the Brit observed: “You know, it’s funny. For the past nine months, all we have done in our investment committees is discuss China and all my portfolio managers seem to fear is an impending Chinese doomsday… Meanwhile, I only have 2% of our fund invested in China; while half of our money is deployed in the US. I guess our underlying assumption is that the US will be fine, because, over time, it always is…”

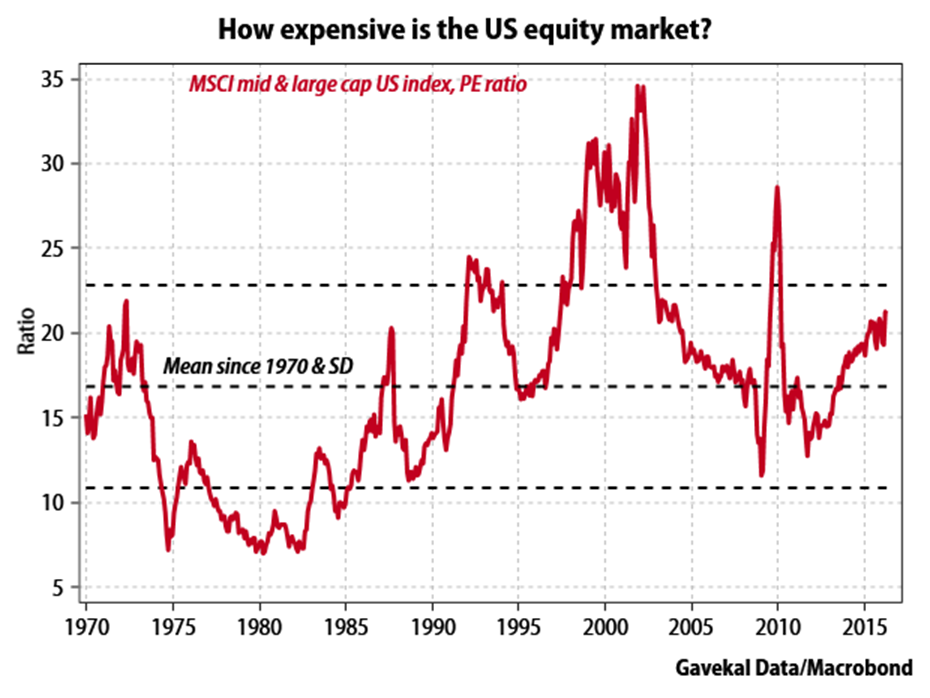

This off-the-cuff remark sparked a fuse in me for, if anything, the US may well be the most dangerous investment destination today. After all, rendered to its bare bones, an equity price is a stream of future earnings, discounted by both a risk-free rate and an appropriate risk premium. And at its core, this simple equation summarizes the challenge confronting investors in US equities for it is clear that the risk-free rate will struggle to move much lower, while current valuations point to a risk premium that is near its floor (the US P/E ratio stands at 21.5x, or almost one standard deviation above its historical average; high P/Es equate to low risk-premiums).

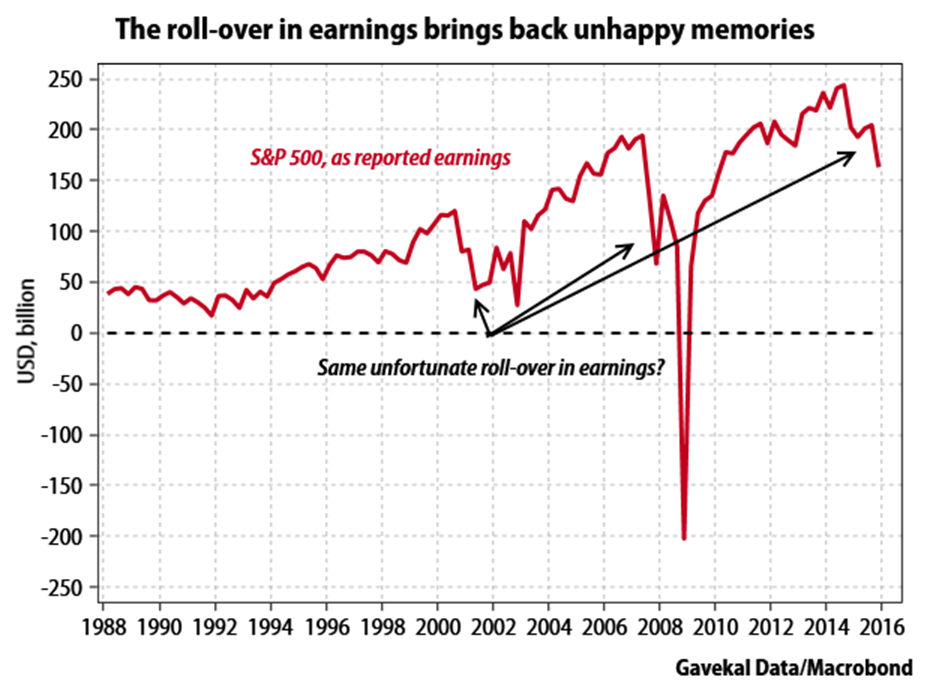

Hence, for any investor operating on the basis that US equity prices will move higher, logic dictates that they must expect a very solid stream of future US corporate earnings. And herein lies the rub: US earnings have lately been pointing in the wrong direction.

In other words, the only way one can hope to make money on US equities from here is for US earnings growth to be very strong. But what are the odds of that happening given that we have now had two consecutive quarters of falling EPS growth? What can turn US earnings around? The strong US dollar means it is unlikely that many American exporters will generate a fresh surge in profits from overseas operations. Meanwhile, the recent roll-over in earnings may simultaneously indicate that, after seven years of zero interest rate policies and massive share buy-backs, corporate America is hitting the wall on financially engineering its way to profitability. (Perhaps reflecting this, an index of companies with the most aggressive share repurchase programs has underperformed the S&P 500 by 8% over the past year.)

In other words, the only way one can hope to make money on US equities from here is for US earnings growth to be very strong. But what are the odds of that happening given that we have now had two consecutive quarters of falling EPS growth? What can turn US earnings around? The strong US dollar means it is unlikely that many American exporters will generate a fresh surge in profits from overseas operations. Meanwhile, the recent roll-over in earnings may simultaneously indicate that, after seven years of zero interest rate policies and massive share buy-backs, corporate America is hitting the wall on financially engineering its way to profitability. (Perhaps reflecting this, an index of companies with the most aggressive share repurchase programs has underperformed the S&P 500 by 8% over the past year.)

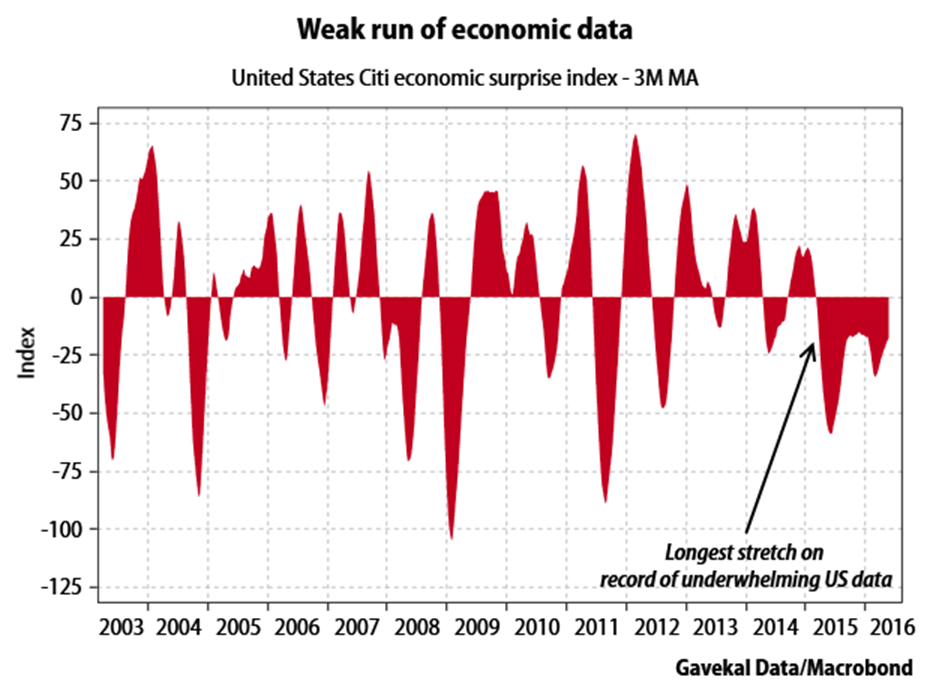

If so, this means that any rise in US corporate earnings in the coming quarters will have to be the result of improved US economic activity. And this is where things gets challenging, because over the past 18 months US data has disappointed on a fairly reliable basis (the hugely disappointing June jobs release being the most recent—and perhaps glaring—case in point).

An argument can, of course, be made that the US economy has lots of pent-up demand and is primed to rebound. Perhaps. But then the next question would be whether the current political environment in the US is conducive to the unleashing of such a coiled spring? Put yourself in the shoes of a US businessman today: on the left, Hillary Clinton is promising the greater business community a higher minimum wage, potentially increased medical coverage costs, more capital gains taxes and possibly higher tariffs (rejection of the Trans-Pacific Partnership free trade deal and all that). On the right, Donald Trump is (definitely) promising higher tariffs, along with a rise in the minimum wage, greater difficulty in hiring foreign talent, increased capital gains taxes and potentially higher medical costs.

An argument can, of course, be made that the US economy has lots of pent-up demand and is primed to rebound. Perhaps. But then the next question would be whether the current political environment in the US is conducive to the unleashing of such a coiled spring? Put yourself in the shoes of a US businessman today: on the left, Hillary Clinton is promising the greater business community a higher minimum wage, potentially increased medical coverage costs, more capital gains taxes and possibly higher tariffs (rejection of the Trans-Pacific Partnership free trade deal and all that). On the right, Donald Trump is (definitely) promising higher tariffs, along with a rise in the minimum wage, greater difficulty in hiring foreign talent, increased capital gains taxes and potentially higher medical costs.

With this kind of uncertainty, who is going to hire workers or break ground on a new factory? Simply put, could the uncertainty surrounding a potential Trump presidency, along with the Clinton campaign being forced to the left by the Bernie Sanders insurgency, be one of the reasons for the recent disappointing US jobs numbers, weak durable good orders, rising inventories and falling industrial production? And, if so, will the situation really change in the coming months? Moreover, is the Federal Reserve actually going to raise rates in such an uncertain political environment? Surely, the better Trump does in the polls, the more likely the Fed is to delay any rate hike until after the election (of course, should Trump get elected, there may not be another rate hike for years!).

Before we fall prey to excessive pessimism, it should be remembered that conditions outside of the US are somewhat different. Specifically:

In summary, forget about Chinese debt. With every hedge fund investor in the world studying the situation up and down, the shock to the system won’t come from there. Instead, the shock will likely come from complacency about US corporate profits and economic activity should the current deterioration continue, surprising the consensus which seems convinced an upside reversal is looming. At that point, investors will once again be reminded of Mark Twain’s cruel words: “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so”.

*Developed countries

**One of the main international stock indexes

***Meaning stock and bond prices are depressed, implying high future returns

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.