“I never give them hell. I just tell them the truth and they think it’s hell.”

-Harry S. Truman, aka, “Give ‘em hell, Harry”

-One of Wall Street’s most strongly held beliefs is “Don’t Fight the Fed”. This means to be a buyer of stocks when it is cutting rates, or is on hold, and to sell stocks when it is tightening. However, the terrible performance of the stock market in the early 1930s, at the start of the 2000s, and from mid-2008 to early 2009—all times when the Fed was aggressively easing—calls this conviction into question.

-“Don’t Fight the Spread” might be a better mantra. The episodes cited above were all times when credit spreads (the difference between government and corporate borrowing rates) were rapidly expanding.

-The good news currently is that the impressive break-out to new highs by the S&P 500 has been accompanied by a further decline in credit spreads. These have been contracting since early February. As usual, this narrowing has coincided with a powerful rally in almost all markets.

-The US stock market clearly has upside momentum right now and may be entering a “blow-off top” phase. However, not all indicators are supportive, particularly those of a fundamental nature, such as earnings. S&P 500 profits are back to where they were in 2006, when this index was trading at 1300, some 40% lower than today.

-While Brexit turned out to be a non-event, at least from a lasting stock market standpoint, there is another risk emerging in Europe. Italy has a crucial vote coming up in October. Due to how severely the Italian economy has suffered since the euro was introduced in 1999, there is a distinct chance of the anti-European Union (EU) party winning this fall. This would likely threaten the entire EU project.

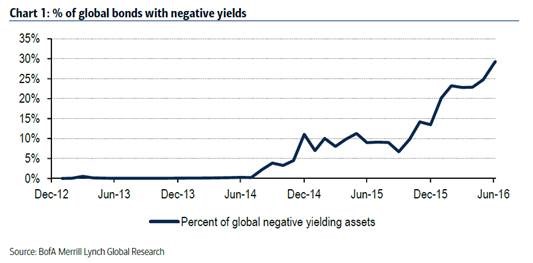

-A long-running EVA prediction has been the increasing “Japanization” of the developed world. This means very slow growth combined with interest rates falling to previously unimaginable levels. 30% of global bonds, amounting to around $12 trillion, now have negative yields. The US is actually one of the last bastions of decent cash flow. Corporate America represents just 12% of total worldwide investment grade debt but is producing 33% of aggregate income. The world continues to be exceedingly growth-challenged despite (or because of) these miniscule rates.

-In the US economy, some recent data has been surprisingly positive. Most notable in this regard was the June jobs number reported in early July showing an extremely healthy employment increase. However, the Household Survey (not as well known as the official Payroll Survey) showed job losses and now shows over 500,000 net terminations this year. Historically, the Household Survey has been better at picking up pivot points in the economy.

-Economic releases tend to be contradictory when the economy is in transition such as from expansion to recession and vice versa. We are seeing considerable amounts of “dueling data” currently. However, when Evergreen weighs the positives and negatives, the scales seem to be leaning more toward an economy that is very late cycle.

Random Thoughts. For this month’s full-length EVA, I am going to employ a different format—one we may use on a regular basis depending on reader feedback—based on the preceding title. Now, I realize that many of you think my thoughts are pretty much always random. Consequently, I should be able to pull this off without quitting my day job as Evergreen’s Chief Investment Officer.

The basic idea behind this is to run a series of short commentaries—almost like vignettes—on the critical themes, memes, and, in some cases, dreams affecting the economy and financial markets (the things investors tend to care about the most). It would be most helpful to us if you could let us know what you think of this version and also which topics you care about in particular (for future coverage and analysis).

With complete absence of hype, I believe this is the most extraordinary era in the history of markets. We’ve all heard that Chinese saying: “May you live in interesting times.” Well, we certainly do—with one notable exception: the disappearance of interest rates. This reality is affecting almost every critical aspect of our lives: From housing prices that are exceeding the old bubble highs of 2007, to a stock market that seems to have broken free from gravitational forces, to the inability of pension funds to earn adequate returns; to young people being forced to question how they can save for retirement. And, most ominously, for those who are retired, or close to it, and are terrified (or should be) about the prospect of funding “their golden years” when investment yields have been crushed.

One could reasonably argue that national and global conditions are the most chaotic and angst-ridden since the late 1960s, another time of elevated stocks prices and low interest rates (though the latter were higher than now and definitely on the incline rather than the decline). But, as these pages have noted so often, there is always opportunity in chaos and turmoil. So, with that in mind, let’s get random.

Don’t Fight the Spread. There are few Wall Street axioms that are as widely accepted as “Don’t Fight the Fed”. Thus, it’s exceedingly risky on my part to attack this bedrock belief but, as longtime readers know, often I can’t help myself. Yet, I try not to take on these convictions without having data and/or history in my corner.

Before you think I’ve lost it, just consider these facts: The three worst bear markets in modern history occurred when the Fed was in frantic easing mode. The early 1930s, 2000-2002, and 2008 to early 2009, all coincided with a period of rapidly falling rates, as the Fed repeatedly cut in vain to prevent contractions in both stock prices and the economy. Stocks fell at least 50% in each of those “Big Easy” episodes. Accordingly, the core principle of “Don’t Fight the Fed”—that stock investors should align themselves with Fed policy, buying when they are easing, or at least on hold, and selling when they tighten—should be immediately called into question.

Certainly, lower interest rates are generally supportive for stock prices. So, what was different about those episodes that caused the precise opposite result? We believe the facts are clear—two simple words: credit spreads, the difference between what a company like Nordstrom pays to borrow money and the rate on US government debt.

Actually, Nordstrom is an ideal example because, as some veteran EVA readers recall, the interest rate on “Nordy’s” bonds rose from 6% to 13% in the fall of 2008 even as the Fed was cutting its overnight rate like Johnny Depp attacking the hedge in Edward Scissorhands. In price terms, this meant the Nordstrom bonds fell by 40%!

This was no aberration. Overall, US corporate credit spreads erupted to highs unseen (not coincidentally) since the early 1930s. Consequently, even as the Fed was slashing rates, the corporate bond market was caught up in a nearly unparalleled and ferocious tightening. It’s no exaggeration to say that this moon-shot by spreads almost crashed the global financial system. Of course, it also gave cash-rich and intrepid investors the yield locking-in opportunity of a lifetime, if not several. (You can click on this link to view an EVA we wrote back then on this epic chance to nail down double-digit cash flow returns.) Unfortunately, most investors were too traumatized back then—or were too fully invested—to capitalize on this manna from the market heavens.

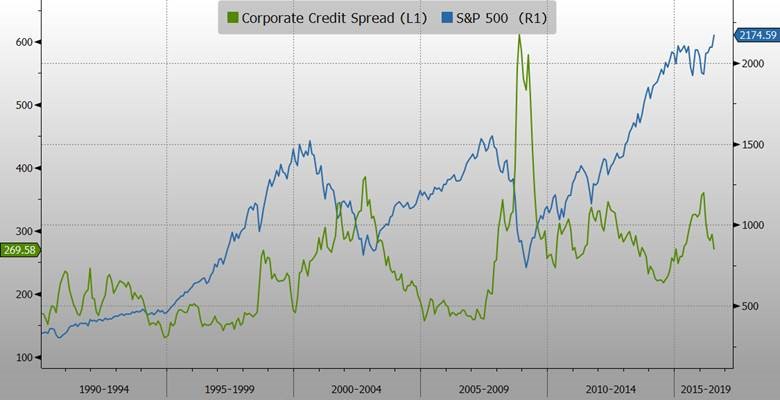

In case you think this can’t happen again, with the Fed having effectively taken rates far below 2008 lows (through its repeated QEs that have dumped over $3 trillion into the system), last year was proof positive it can. As you are able to see in the chart below, spreads began rising in the summer of 2014 and kept soaring until February of this year. The market typically ignores the first third or so of a credit spread-widening event and this time was no exception. But as spreads kept expanding, stocks began to crack, first in August of last year when the Dow fell over 1000 points in less than an hour (even prior to the Fed hiking). Then, in January, the S&P quickly receded 15% from its high in May, 2015, with small-caps down nearly 30% (after a mere ¼% Fed rate nudge).

Source: Evergreen Gavekal, Bloomberg

Fortunately, as you can see above, spreads started falling in early February. As is so often the case, this downward inflection in spreads precisely corresponded with the rousing rally that began at that point. (You can also note how spreads rose decidedly prior to the vicious bear markets that started in 2000 and again in 2008.)

So what message are spreads telling us about stocks as July comes to a close?

Look out above… Frankly, we didn’t think it would happen but the S&P has broken out to yet another new high after over a year of paralysis. To some important technicians, such as Ned Davis and Walter Deemer, this is an extreme positive indicative of a “breadth thrust” and “breakaway momentum”, in their respective views.

Credit spreads are also in synch with this bullish scenario. They have continued to fall and team Evergreen is most pleasantly surprised by how much the bonds we hold for clients have risen lately, with even some recent purchases up 10% to 15%. (Falling spreads almost always means rising prices, similar to how lower rates drive up bond values.)

Accordingly, we believe there is a very good chance we are entering into the “blow-off top” phase of this very old bull market. Money can be made quite quickly during these times as prices tend to go parabolic. The dark side of this, if it does happen, is that it tends to suck in unsophisticated investors at the worst possible time.

…but don’t forget your parachute. It’s important to emphasize that not all the evidence is bullish right now. Although breadth (the number of advancing stocks vs decliners) is decidedly positive, volume has been light. Also, both small caps and the Dow Transportation average are not confirming this breakout.

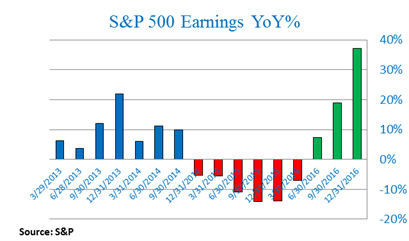

Beyond technical considerations, the actual fundamentals are underwhelming at best. We are the first to concede that we have underestimated the staying power of this seemingly eternal bull market. However, we were among the few to correctly warn back in 2014 that the earnings cycle was likely peaking and that, directly related to this, US corporate profit margins were poised to contract off of all-time highs. This clearly has been happening as you can see below.

Source: The Closing Print, Michael O'Rourke

Source: The Closing Print, Michael O'Rourke

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

An earnings recession occurs when there are two consecutive quarters of negative earnings growth. Clearly, we are way beyond that and even more disconcerting is this factoid: reported profits for the S&P 500 are back to where they were in 2006! Yes, that’s a decade of earnings nothingness, but there’s one notable difference: The S&P was at 1300 back then (vs 2160 today).

The bullish spin on this is that earnings are now poised to surge again, based on the reduced headwinds from the energy sector (where profits were eviscerated due to crude’s bungee jump) and the strong dollar (which hurt multinational firms’ income). It could be but let’s hold off on that conclusion until we review the economic section of this EVA in a bit.

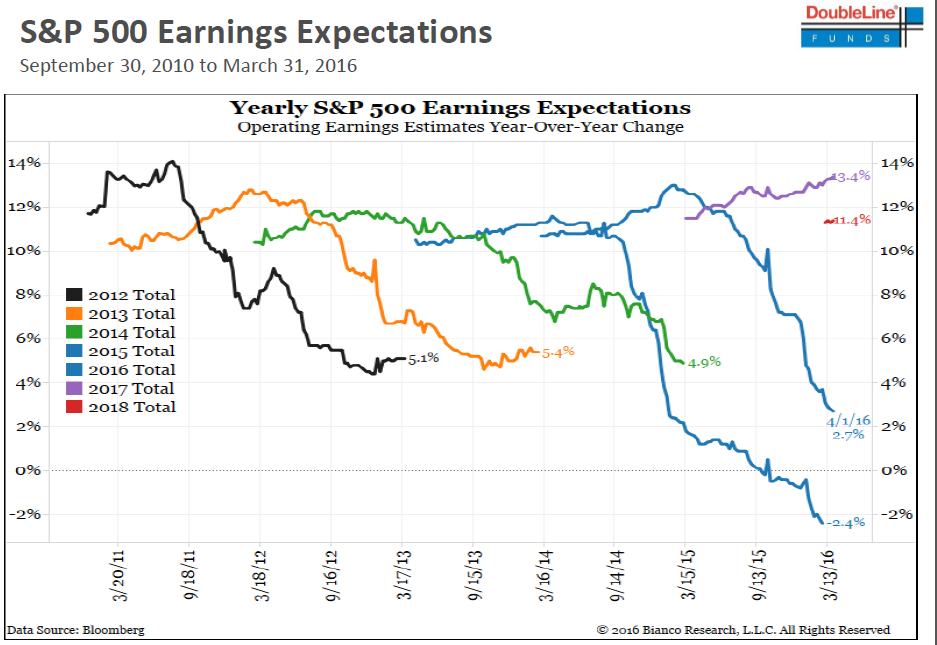

The fact that Wall Street’s profits crystal ball has been so absurdly optimistic, per the charts below, and continues to be, is reason enough for skepticism. Therefore, it may be more prudent to value the market based on what it has actually earned—based on GAAP* rules, rather than through the rose-colored lens of the analyst community.

Source: Bloomberg, DoubleLine

Source: Bloomberg, DoubleLine

Source: The Leuthold Group

Source: The Leuthold Group

Near-term, though, such fundamental considerations are almost null and void. Momentum rules the battles, even if valuations eventually win the wars. Before you decide to jump in with both feet, however, it’s worth reflecting that the CNN Money Fear and Greed Index just hit 90, indicating extreme risk-taking. Additionally, Ned Davis Research (NDR) has an intriguing new indicator that tracks the most hyperactive investors known to humanity—those who speculate in leveraged (double and triple) exchange-traded funds (ETFs). As NDR has found, you want to be selling when these folks are buying and vice versa. Right now they are moving into the max bullish zone. Caveat speculator!

Source: Ned David Research

Source: Ned David Research

Arrivederci Brussels? There’s another reason to rent this stock rally rather than buy it and it’s a five- letter word: Italy. A major risk for that beautiful country is another five, as in the Five-Star Movement. This political party’s leaders are extremely hostile toward Brussels-based eurocrats and want out of the European Union (EU). They are currently leading in the polls and gaining momentum. There is a crucial referendum coming up in October put forth by Italy’s present prime minister, the youthful Matteo Renzi.

letter word: Italy. A major risk for that beautiful country is another five, as in the Five-Star Movement. This political party’s leaders are extremely hostile toward Brussels-based eurocrats and want out of the European Union (EU). They are currently leading in the polls and gaining momentum. There is a crucial referendum coming up in October put forth by Italy’s present prime minister, the youthful Matteo Renzi.

Most US investors seem as oblivious to this risk as they did to Brexit. One could certainly argue that since the latter only briefly hit US stocks, the potential for Italxit is non c’e problema (no problem). But we think this is dangerous thinking. Italy is the third largest economy in Europe as well as the third biggest bond market in the world (Italy isn’t that great at making cars or appliances anymore but they sure excel at producing debt!). Further, an Italxit would turn the cross-hairs on terrorism-plagued France where the anti-EU sentiment is even stronger.

It’s also well known that Italy’s banking system is a shambles with dud loans three times the level of US banks even during the worst of the Great Recession and housing implosion. Italy’s financial system desperately needs a bail-out but those pesky eurocrats are against it—supposedly. Our view is that due to how disastrous it would be to the EU if Italy says “andiamo”, Brussels will cave in and allow some type of banking rescue. Recent comments by ECB head honcho Mario Draghi are supportive of our view.

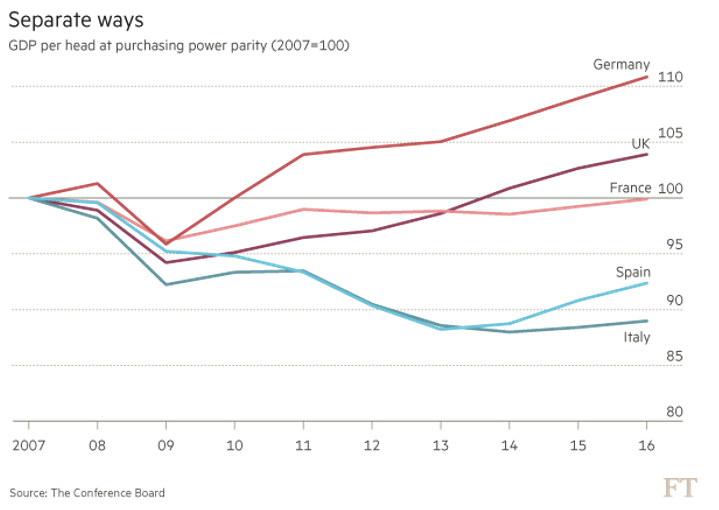

If so, this could apply another lift to the S&P. But, should a bail-out happen, we think it would be a fleeting propellant. The real problem is that the Italian economy is as bad off as its banks and there is no miracle cure for that malady. Per the following chart, Italy’s GDP has been contracting for years, underperforming even Spain where unemployment remains around 20%.

Source: Financial Times, The Conference Board

Source: Financial Times, The Conference Board

Incredibly, despite all of Italy’s baggage (and carry-ons, too), it’s 10 year bond trades at a yield of just 1.3%, lower than even the comparable maturity US T-note. Which brings up another disturbing overseas phenomenon…

Rotten sushi. Another long-term trend Evergreen recognized early on is what we have referred to as the Japanization of the developed world. For a considerable time, this was an extremely maverick view but lately mainstream media sources, like the Wall Street Journal, are picking up on it.

Essentially ever since its monstrous bubble in stocks and real estate explosively burst in 1990, Japan has been stuck in an economic Twilight Zone, oscillating between feeble growth and mild, but repeated, recessions with long-term growth far below the prior trend-line. This reality calls a couple of popular notions into question.

The first is that you can’t have recessions without an inverted yield curve (when short-term rates go above long-rates). As noted, Japan has had a slew of those despite its yield curve not inverting once since 1990. (By the way, the same has been true in Europe in recent years and while the US has avoided double/triple/quadruple-dip recessions, our expansion has been the weakest ever since WWII).

The other at-risk belief is that exceptionally low interest rates are enough to force stock prices higher and keep them there. Japan has had the scrawniest rates in the world for the last quarter-century and yet its stock market has been in a secular, or long-term, bear market during that entire time-frame (punctuated by numerous “counter-trend” rallies).

JAPANESE STOCK MARKET SINCE 1990 Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

Japanese-like yields is an increasing fact of life throughout the developed world (rates still exist in emerging markets—for now). In actuality, negative rates are spreading around the planet like some kind of slow-moving epidemic with 30% of bonds now “sporting” minus signs in the yield column.

Somewhat resisting this extinction of interest rates, US bond yields, particularly in the corporate world, remain on the sunny side of zero, in many cases by a decent margin. This has created the remarkable situation where Corporate America’s investment grade debt represents just 12% of total global IOUs but a significantly disproportionate 33% of aggregate income.

Consequently, a profound question is whether the US will become more like the rest of the “rich” world or the world will become more like the US. Economic trends likely hold the answer to this query.

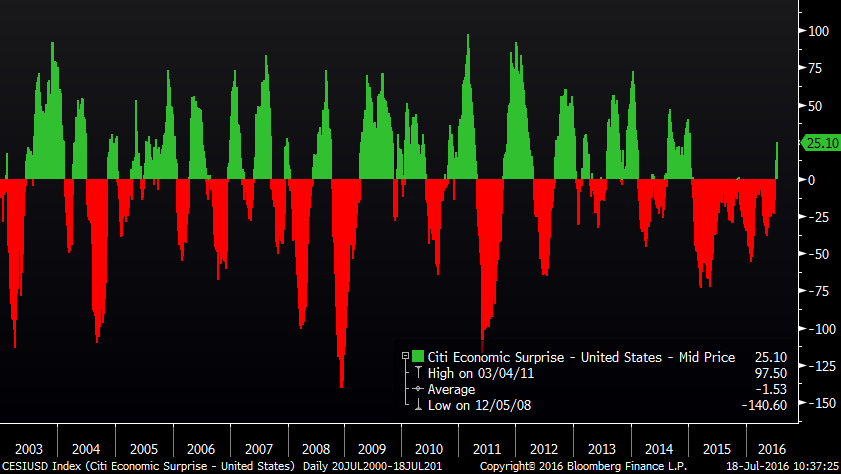

Fooled by recentness? Let’s cut right to the chase regarding the recent performance of the US economy: It has definitely shown signs of perking up. (If econ isn’t your game, feel free to skip this section.) The very closely followed Citigroup Economic Surprise Index has had a nice spike, as you can see in the following chart.

CITI ECONOMIC SURPRISE INDEX Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

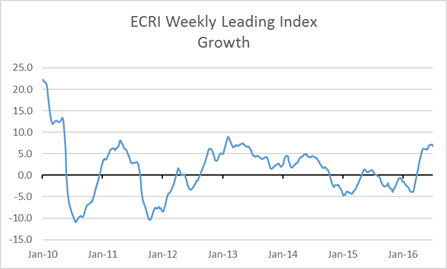

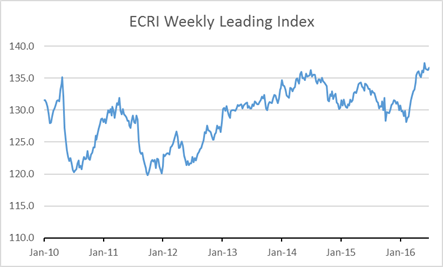

Also, the leading indicators from the firm with the best recession forecasting record, ECRI, are clearly trending in a northerly direction.

Source: Economic Cycle Research Institute

Source: Economic Cycle Research Institute

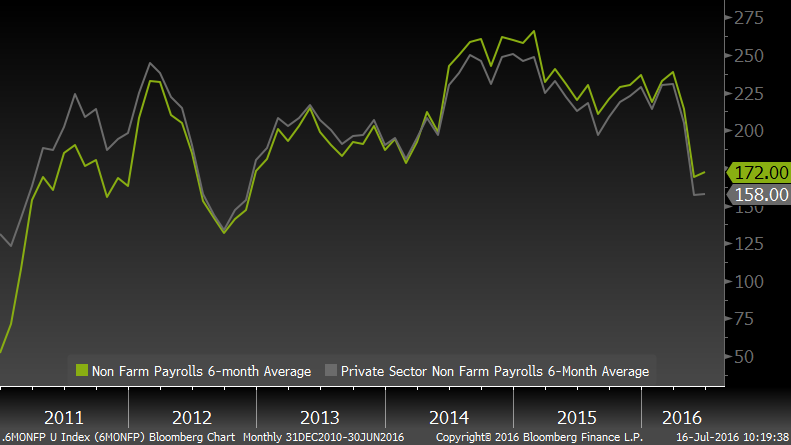

However, it was the June jobs number released in early July that really got the bulls’ juices flowing. As a reminder, May was a stunningly bad “print”, but June was just as shocking on the upside. This has caused Wall Street to believe that May was the wild-hair number while June was the real deal, triggering the aforementioned stock-market breakout above the May 2015 peak.

The problem with this happy thought is that it is contradicted by two important factors: The six-month trend in the official jobless survey and the less-focused on Household Survey (HS). As you can see, the trend in the first half of this year for the so-called Payroll Survey is not encouraging.

PAYROLL SURVEY—US LABOR MARKET Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

Perhaps more worrisome is that the HS showed a job contraction in June! And this isn’t a one-month fluke. The HS has revealed a total of 517,000 net positions eliminated this year. What’s crucial about this survey is that it traditionally is much better at spotting inflection points in the jobs market. This means that at the end of recessions it turns up before the payroll survey and at the terminal stage of expansions it turns down first.

We plan to expand on this theme in an upcoming chart-focused EVA (or, possibly, webinar) but suffice to say there are more and more economic markers throwing off negative signals. These include tax receipts falling year-over-year for both individuals and businesses, and state sales tax collections close to three-year lows.

Added to that, unsold wholesale inventories are nosebleed high, with auto inventories back to where they were in 2007 (you know what happened after that)! Additionally, two of the best pre-warners of a recession—core capital goods orders and the coincident-to-lagging indicator—are flashing dark orange, if not red. And even though the Citi Economic Surprise Index has bounced it’s in deeply negative territory and has been sub-zero for the longest stretch in the past 13 years, as you can see in the Citi Economic Surprise Index chart above.

Back on the critical employment front, job openings fell the most in May since 2008, new hirings were the weakest since March 2009, and Janet Yellen’s favorite Labor Market Conditions Index has been negative for six straight months, a streak not seen since 2009. Do you detect a worst-since-the-Great-Recession pattern there?

To end this section on a somewhat cheery note, jobless claims are not remotely in a recession heads-up mode, nor is the Fed’s highly comprehensive Chicago National Index. Therefore, one can take either a bullish or bearish view of the economy’s flight path.

It’s not unusual to have conflicting releases on the state of the economy at turning points, which we may be approaching. At potential pivots junctions like this, it is essential to weigh the evidence to see which side of the scale is heavier. Right now, the negative side appears to be the winner but not decisively enough to conclude a recession is close at hand (although today’s release of another punk GDP number—a mere 1.2% increase—may indicate the next downturn is not in the distant future, either).

Still hazy after all these years. Many years ago, I brought up the anecdote that President Harry Truman was once so exasperated by “on the one hand, but on the other…” economic reports that he yelled: “Bring me a one-armed economist.” If Harry were around today, it’s a safe bet he’d be shouting those words again.

The highly contradictory economic data, even if seemingly tilting toward worrisome, just adds to my overall sense of confusion, which I admit I am inundated with these days. There are so many things I just don’t get. For example, how can the stock market continue to trade at one of its spendiest levels ever despite such deep societal malaise? Even the late ‘60s were characterized by strong economic growth to offset the social fissures that were occurring at that time (also the market was poised to endure a brutal next half-decade).

And how can the stock market be signaling all-clear when the bond market is reflecting a deep recession and/or deflation? Clearly, one of these asset classes has it very wrong and, generally, bonds get it right more often than stocks. (Even in countries like Canada where central banks are not suppressing yields, bond rates are at historic lows.)

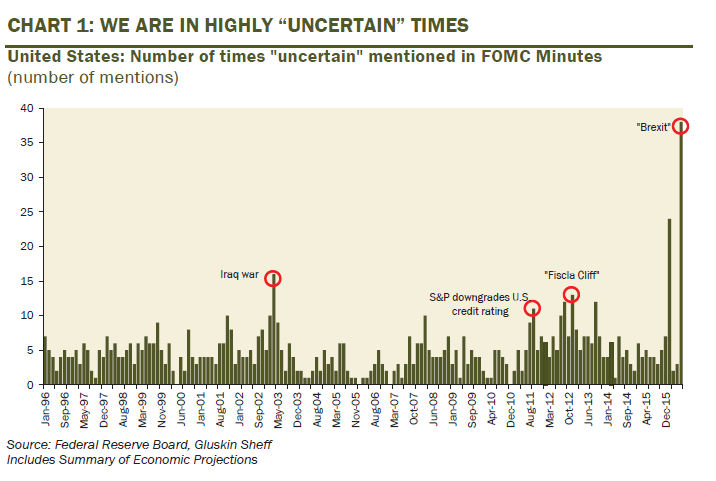

Even the perpetually recession-blind Fed is recognizing that these are exceptionally uncertain times. These eras don’t correspond to priced-for-perfection stock markets.

It’s also unprecedented to have stocks valued like happy days are here again after many quarters (possibly as many as six) of falling corporate profits, per the chart at the top of page 4. Major stock market tops are always associated with peak profitability and an apex in capacity utilization. Both of those look like they are at least two years in the rear view mirror.

It’s additionally perplexing to me that millions of investors seem to be buying stocks for income and bonds for appreciation, the antithesis of normal behavior. They also seem to be content with a broad equity market which has essentially gone nowhere for two and a half years, with even the S&P 500 badly lagging treasury bonds since the start of the millennium, as well as from the end of 2013.

NYSE COMPOSITE (A BROADER INDEX THAN THE S&P 500)

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

Perhaps the biggest befuddlement, though, is that we have two of the least-liked personalities in the history of US politics vying to be elected leader of the free world. Is it just me or do you yearn for a straight-shooter in the White House like the one they called “Give ‘em hell, Harry” who had a sign on his desk, “the buck stops here”? If you do, you’re almost certain to keep yearning for at least another four years—and that’s another thing I don’t find bullish in the least.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

*Generally accepted account principles, i.e., real not “made as instructed” earnings.

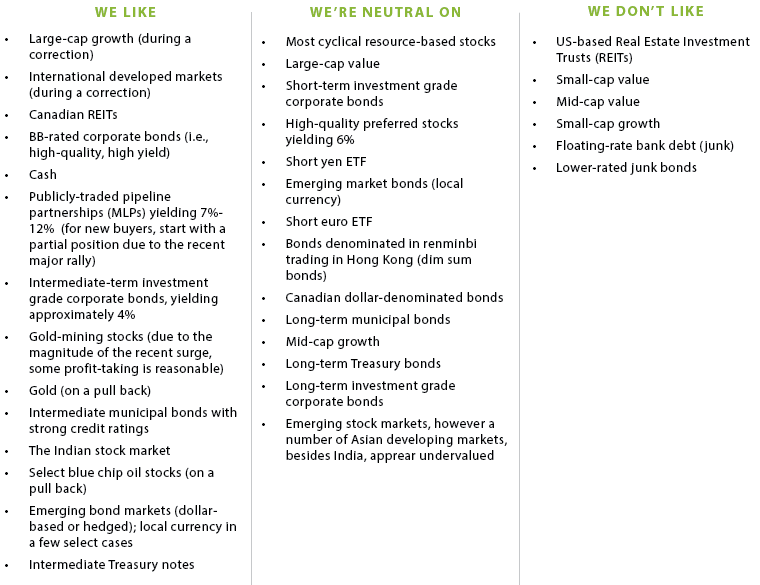

OUR CURRENT LIKES AND DISLIKES

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.