“In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.”

-Famed German economist, RUDIGER DORNBUSCH

“Risk is most dangerous when it is least apparent, and least dangerous when it is most apparent.”

-JIM GRANT, Grant’s Interest Rate Observer

This week marks the maiden voyage for our webinar version of the Evergreen Virtual Adviser. As you will soon see, this issue expands on some of the themes covered in last week’s “Random Thoughts” EVA. However, it also discusses several prevailing memes (basically, currently popular beliefs that circulate among investors) influencing the financial markets. In some cases, Evergreen believes these memes are more like dreams that may soon experience a rude awakening.

A couple of the charts in this slide deck are repeats from last week’s EVA but most are new. They focus on topics investors tend to care about the most: the stock market, bonds/credit spreads, the economy, and energy/master limited partnerships (MLPs).

Last week’s extremely disappointing GDP release perhaps makes some of the economic comments in this EVA more timely. If you missed it, the second quarter growth rate was essentially half of what was originally expected. Moreover, the first quarter was revised from an already underwhelming 1.1% to a totally limp 0.8%. Therefore, it’s worth considering the views of those who are increasingly on-guard about the next recession.

Back to the Harry Truman “on the other hand” point from the July 29th EVA, today’s jobs release appears to be robust both on the surface and in the details. Thus, the intense crosscurrents we noted in last week’s issue remain in full force. This is now two very robust employment reports in a row; consequently, we have a new upwardly sloping mini-trend. But the key word is “mini”. The longer-term trend remains worrisome. Additionally, Janet Yellen’s favorite employment indicator, the Labor Market Conditions (LMCI) has been eroding for six straight months. The LMCI has nineteen different components, making it far more comprehensive than the notoriously volatile monthly payroll survey that is producing so much enthusiasm today. (In fairness, the Household Survey, which had been extremely weak this year, also rebounded dramatically.) The bottom-line on the jobs market, in our view, is that it remains mixed with a long-term downward bias.

On the subject of MLPs, due to time constraints, I didn’t discuss how MLPs have fared during the recent nasty correction in oil prices. Yet, I realize many readers are extremely interested in this topic.

Accordingly, very briefly, the good news is that the publicly-traded partnerships—which own and operate much of the nation’s most critical energy infrastructure assets—have been holding up reasonably well. They certainly have corrected but, for the most part, it’s been a controlled pullback. This is in vivid contrast to the hammering MLPs experienced last year every time oil fell materially. Specifically, the MLP index has eased just 3% even as crude has declined over 20%, putting oil officially back in bear market status.

The other positive development has been the benign behavior of credit spreads*. Last year, each time oil took a dive credit spreads expanded, putting pressure on nearly every corner of the income world. However, over the past few days there has been some spread-widening. So far, it’s been a minor expansion but, regardless, we are watching that shift very, very closely. Expect more updates on this crucial lead-indicator in the near future.

As always, your feedback on this new format is welcomed and appreciated.**

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

*The yield gap between what companies pay to borrow money compared to US government borrowing costs.

**Thank you very much to all those who replied to last week’s “Random Thoughts” EVA. As a result of the encouragement we received, we plan to use this format at least quarterly in the future.

View this week’s webinar version of EVA below. Click to view the PowerPoint in PDF.

https://vimeo.com/177611378

Important Disclosure: The included webinar link was originally published on 8/5/16. The material in the webinar is being distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of the date posted (8/5/16) and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.

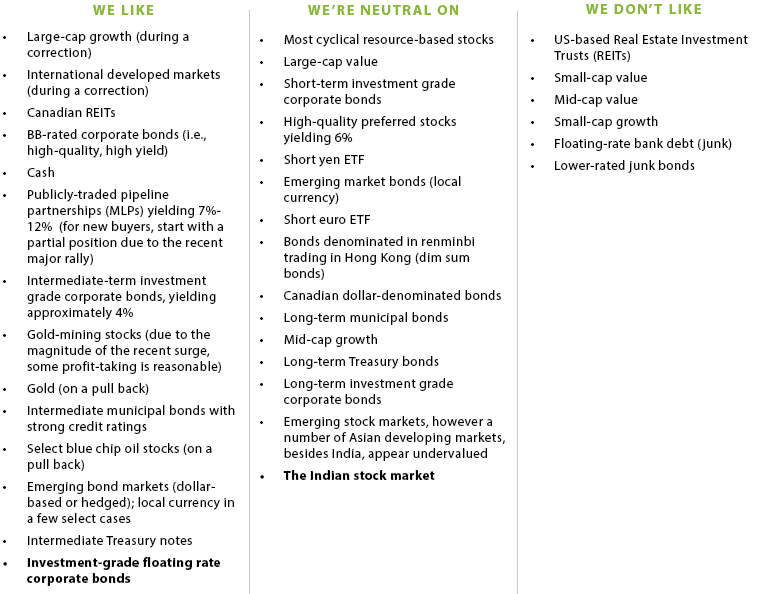

OUR CURRENT LIKES AND DISLIKES

Changes are bolded below.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.