“The chance which now seems lost may present itself at the last moment.”

-JULES VERNE

Around the world in eighty days eighteen minutes. For all the non-bibliophiles reading this week’s EVA, Around the World in Eighty Days is a classic novel written by French author Jules Verne. While the book is fictional, it has inspired several real-life adventurers to follow in protagonist Phileas Fogg’s footsteps and circumnavigate the world in 80 (or less) days.

For instance, American journalist Nellie Bly set out for this mission in 1889, and completed her travels in seventy-two days. (She even met with Verne in Amiens, France during her trek!) Fellow-Seattleite James Willis Sayre set out on his journey in 1903, setting a then-record for circumnavigating the world in 54 days, 9 hours, and 42 minutes. (Interestingly enough, that was the same year Wilbur and Orville Wright made their maiden voyage on a powered aircraft. That probably could have saved him even more time.) Golfing legend Arnold Palmer even got in on the act sixty-three years later by setting the around-the-world business aircraft record in 1976, flying his Learjet from Denver, Colorado, and back again, in a mere two days, 25 minutes, and 42 seconds.

Since we fancy ourselves rather ambitious here at Evergreen Gavekal, and because we only have your time and attention for a short period each week, we’ll attempt the cross-continent travel in… drum roll please… eighteen minutes (or however long it takes you to get through this blog post).

To begin, we’ll journey with a good friend and partner, Charles Gave, through US and foreign markets. In his paper titled Whether or Not to Underweight the US, Charles evaluates how investors should position themselves based on valuation and non-valuation factors.

From a valuation perspective, Charles identifies the US dollar, US corporate bonds and US equities as overvalued relative to global peers. Historically, valuation metrics have been good indicators to exit expensive markets and enter less-expensive ones. However, from an economic fundamentals perspective, the evidence for an exodus from US markets is a bit more muddied. Namely, because there is a shortage of dollars globally and, during periods where this is true, US equities tend to outperform non-US equities.

Given this split conclusion, what should investors do? Well, keep reading, for one thing…

Next, we’ll continue our journey to France with another close friend and partner of Evergreen’s, Louis-Vincent Gave. As most have heard by now, Emmanuel Macron and Marine Le Pen will go toe-to-toe in France’s May 7th runoff. While markets have baked-in a Macron victory, Louis is less convinced of the widely-held outcome. In fact, Louis provides a scenario where Marine Le Pen could slide past Macron in a tight contest and potentially upend markets and popular opinion much like Brexit and the US election (and last week’s Survey EVA).

While Evergreen is not convinced that this scenario will play out – much depends on voter turnout and all signs seem to point towards a Macron victory – it’s worth considering given the recent wave of populism spreading across Europe and North America. Whatever the outcome, one thing remains clear: the great debate between globalists and populists will be a centerpiece in elections for years to come.

Finally, we’ll wrap-up our journey with Louis in the Middle East. In The Consequences of Trump’s Syrian Strike, he notes that Trump’s recent airstrike put the US in the middle of an Islamic war that pits the region’s Sunni Muslims against Shia Muslims. With so many countries tangled in this conflict (Saudi Arabia, Iran, and Russia, to name a few) there are plenty of macroeconomic implications.

But those big-picture considerations might not be as clear-cut as one might presume. While oil and arms are clear winners from increased tension in the Middle East, Louis notes other, less direct and more efficient, ways to position and protect portfolios.

For the journeyman, that includes trips to places like Canada, Mexico, Russia, Indonesia and Australia. What else would you expect from an excursion around the world in eighteen minutes?

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

WHETHER OR NOT TO UNDERWEIGHT THE US

By Charles Gave

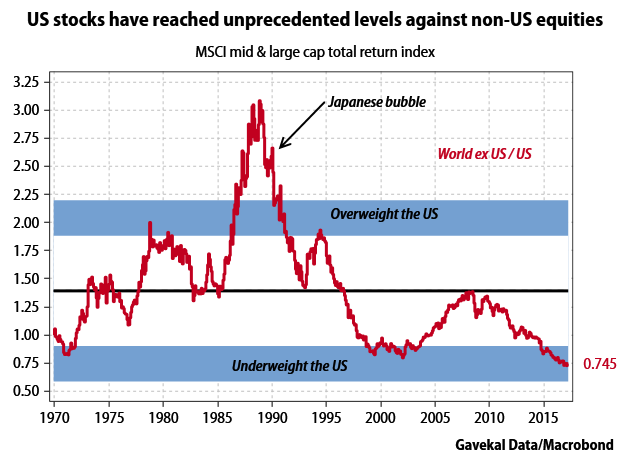

At recent Gavekal seminars, I have argued that investors should start to underweight US assets in favor of foreign equivalents. This call was squarely valuation-based as my models show the dollar, US corporate bonds and US equities as being overvalued. Moreover, on a relative basis US stocks are unprecedentedly expensive when compared to non-US alternatives. The aim of this paper is to assess this position in light of non-valuation-based macroeconomic factors.

First however, let me briefly summarize that valuation argument: stock markets are a forum for measuring the return on invested capital across economies. In a truly “open” world, returns should tend to equalize on a trans-national basis to a single common level. As such, the ratio of two stock markets' total returns should exhibit no trend, and—strange as this may seem—over the long term, this is indeed the case.

Yet from time-to-time a core global stock market will become cheap relative to its peers. Since mean reversion is inevitable, at such times any manager who is serious about asset allocation must buy the cheap market and sell the expensive one. Since 1970, there have been three key times to buy US equities and sell the rest of the world; namely 1979, 1987-89 and 1994. By contrast, key times to sell the US and buy the rest of the world were 1971, 1999-2002 and the period since late 2014.

As the chart below shows, should the relationship between the US and the rest of the world revert to its long-term mean—never mind overshoot— then an equity portfolio orientated to this outcome would achieve 100% better performance than one exposed merely to US stocks.

Source: Gavekal Data/Macrobond

Source: Gavekal Data/Macrobond

And yet, until recently I was reluctant to recommend such a switch as my US equities model (for the most part) pointed to the market being fairly valued. But with US stocks making a clear move into expensive territory over the last six months, that has changed. It thus follows that the time is right to get out of the world’s biggest equity market.

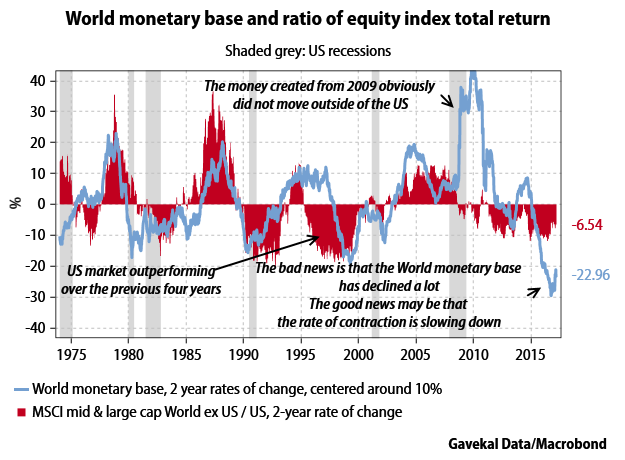

But perhaps a more fundamental question is why, cycle after cycle, do US equities display such a pattern of outperforming for a few years followed by a lean period of underperformance. To me it seems fairly clear that this effect stems from the US dollar being the global reserve currency. Simply put, in periods when the rest of the world is awash with US dollars, non-US equities always outperform. But as night follows day, these phases are followed by periods of US dollar scarcity in the rest of the world—and these times always see foreign markets underperform their US counterparts.

To this end, measuring worldwide demand for dollars is a big headache. However, mapping the supply side of the equation is far simpler. The chart below shows the WMB’s (World Monetary Base) two-year rate of change. It leads by 12 months the two-year rate of change in the ratio of total returns for non-US versus US equities.

Source: Gavekal Data/Macrobond

To cut a long story short, when the supply of dollars goes up, non-US markets should outperform. When their supply falls, non-US markets will underperform. So how to explain the 2011-13 period when the WMB was expanding, yet non-US equities underperformed? It could be argued that US equities were simply way too cheap (my valuation argument), or more worryingly that money printed in the US through quantitative easing did not, in fact, leave the confines of the US. If correct, this would offer one more sign of monetary velocity collapsing on a global basis—this has been a core contention of mine in recent years.

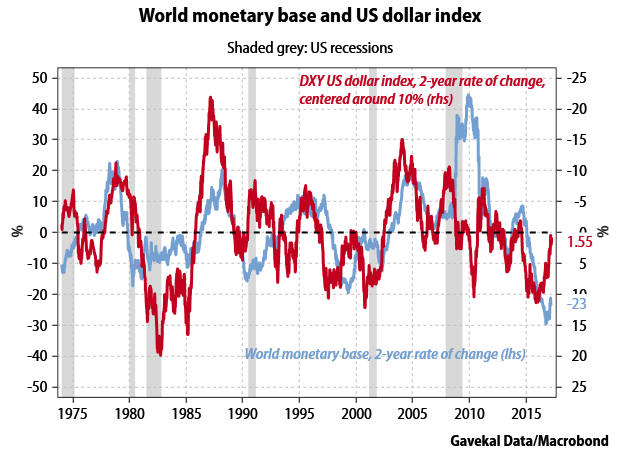

This leads to a split conclusion. While on valuation grounds investors should be moving away from the US, the fundamental argument is less compelling as the world seems to face a structural shortage of dollars. To complicate matters, monetary factors often have delayed and variable impacts on both real economic activity and financial markets. Variations in the WMB tend to correlate tightly with moves in the US dollar exchange rate, as shown by the chart below, and this time there is no lead. Thus an optimistic take is that since the dollar is no longer appreciating, the world monetary base may once again be growing.

Source: Gavekal Data/Macrobond

Source: Gavekal Data/Macrobond

If this were to be confirmed in the next few months, then my valuation-based call to move out of US assets in favor of the rest-of-the-world would be confirmed by economic fundamentals. In such a situation, investors should adopt a massively underweighted position in US risk assets.

By contrast, if the US dollar resumes a clear appreciation track then all bets on non-US assets would be off.

Investment conclusion Hence, my advice to asset allocators is to hold a market-weighted position between US and non-US equities. Protection should be sought with out-of-the-money call options on the US dollar. The hope would be that these calls never move into the money as that would likely mean losing bundles on both US and international equity positions. In such an environment, owning a few puts on the overvalued US equity market should also help limit the damage.

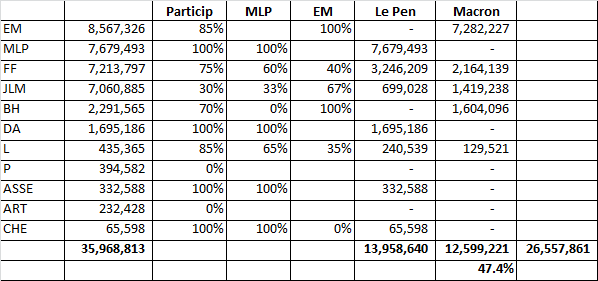

SECOND ROUND COULD STILL BE QUITE CLOSE...

By Louis-Vincent Gave

The reason Brexit and the US election surprised people is that everyone thought the race was already won and so voters for the “perceived winning team” (especially young people) didn’t bother to vote. And that was enough to tip the balance.

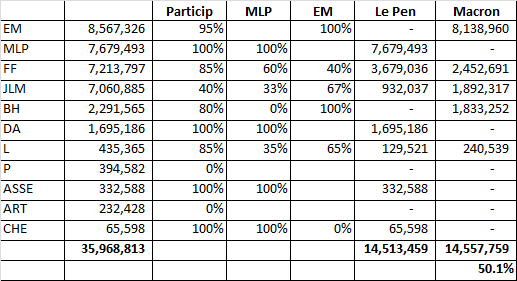

Could we see the same thing in France? Taking the final votes tally from the first round, we made some simple projections.

SCENARIO 1:

Let’s imagine that…

With these conditions, Macron wins with 50.1%!

SCENARIO 2:

Let’s imagine that…

In this scenario, Macron loses with 47.4%!

Unthinkable? A lot will depend on the turnout… With markets, pundits, and polls all pointing to a massive Macron win, a lot of Melenchon/Hamon (and even Macron) voters may well decide to stay home.

THE CONSEQUENCES OF TRUMP’S SYRIAN STRIKE

By Louis-Vincent Gave

In his 1992 book Give War a Chance, P.J. O’Rourke remarked that “wherever there’s injustice, oppression and suffering, America will show up six months late and bomb the country next to where it’s happening.” Now, in fairness to Donald Trump, the bombing of assorted Middle Eastern countries by the US armed forces did not just start. Nonetheless, by launching his cruise missiles at a Syrian airbase, Trump has now waded into the Islamic civil war that pits the region’s Sunni Muslims, broadly supported by Saudi Arabia, Qatar and Turkey, against the region’s Shias, backed by Iran and Russia. The question now has to be whether the US intervention will tip the scales against Bashar al-Assad’s Syrian regime, which until just a few days ago looked set to survive to the detriment of the Saudi-Qatari coalition.

Interestingly, the markets do not seem to care that much about the answer. After five years of horrors, the world has clearly grown immune to daily reports of barely describable human suffering. Yet beyond the harrowing images coming out of Syria lies an important question: does the US intervention mean that the latent conflict between Iran and Saudi Arabia, which so far has been fought mostly through proxies in Syria and Yemen, will now explode into the open?

If it does, it seems obvious that Trump is ready to throw in his lot with the Saudis—unlike Barack Obama who always sounded ambivalent about Saudi and seemed keen on normalizing the US-Iran relationship. Indeed, within a few weeks of his inauguration, Trump had already carried out more than 30 airstrikes against Yemen’s Houthi rebels, who are backed by Iran. That is as many as the US air force carried out in the whole of 2016. Of course, the fact that Vladimir Putin has clearly aligned Russia with the region’s Shias only throws further complications into the picture.

Needless to say, the reason this will end up mattering for investors—as ever with the Middle East—is linked to oil (and arms). So far, the market seems to have greeted Trump’s intervention in the Middle Eastern civil war by bidding up both. On the face of things, this makes sense. After all, Obama’s policy of bringing Iran in from the cold coincided with the major drop in oil prices. Investors naturally reasoned that Iran’s vast hydrocarbon reservoirs, which for years had been unproductively exploited, would, over time make their way to the global market.

Since then new discoveries have revealed large and exploitable oil basins, from Brazil, to the Permian Basin of Texas, to Alaska. The idea of “peak oil” has been buried for at least a generation, if not forever. These discoveries, of course, make Middle Eastern conflicts that much less threatening to global growth, and reduce the need for other countries to stockpile oil at the first sign of trouble.

So, returning to Syria, investors are left facing a simple decision tree. The first question is this: Does the US intervention make a Saudi-Iran war more, or less, likely? Investors who fear that the odds of open conflict have now increased will likely want to overweight the US dollar, defense sector companies, and energy stocks. However, there may be other, less direct and perhaps more efficient, ways of playing the same theme, including:

With all this in mind, perhaps policymakers from Jakarta to Ottawa, Canberra to Mexico City, will be hoping that the decision-makers in Riyadh and Tehran will follow P.J. O’Rourke’s advice and “give war a chance”? Right now, it doesn’t seem that policymakers in either Washington DC or Moscow are holding them back.

OUR CURRENT LIKES AND DISLIKES

Changes in italics.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.