Future glow. Unquestionably, one of the worst enemies for most investors is what academics call “The Recency Effect.” At Evergreen, we refer to this as “The Tyranny of the Temporary”, the time-proven inclination of the investing public to pour money into yesterday’s winners, particularly after a long period of outperformance, thereby creating tomorrow’s losers. The related cardinal sin is bailing out of areas that have been in the penalty box over prior years.

Aggravating this human frailty is the fact that generally hot areas often stay toasty, and cold sectors remain frigid, longer than expected. This reinforces the seeming wisdom of performance chasing. However, recent research has indicated that somewhere around the three-year mark a reversal point is typically reached. Thus, if a particular asset class has been on fire for around 36 months, the odds increase that a fire hose is waiting around the corner. Conversely, the long-term three-toed sloths often suddenly change into sprinting gazelles at roughly the same interval.

Naturally, there are exceptions to this pattern. Yet true investors, as opposed to traders and other momentum followers, should be looking to reduce those market segments that have been glowing and adding to those that have been shrouded in darkness.

Certainly, there are few asset classes today as behind the moon as commodities. Admittedly, some deserve to be in total eclipse and, based on fundamentals, might remain that way for a while longer. For example, oil only began to crack in the second half of last year. So, despite crude’s crunching, only partially reversed by a recent recovery, it’s likely considerable time needs to pass before it can enter into a sustainable up-phase. This also makes sense based on the lags in reducing production after a price crash.

But, other commodities have been the red-headed stepchildren of the investment world for much longer. Relevant to this week’s EVA, there is a specific commodity that has been treated as radioactive for years and now is seeing supply/demand dynamics shift dramatically in its favor.

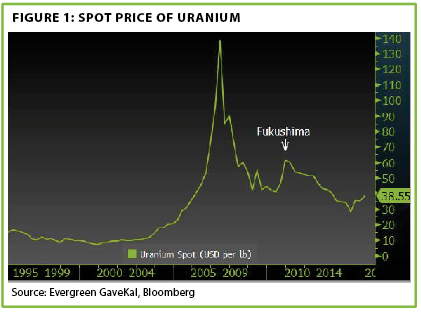

Actually, in the case of uranium, the commodity featured in this EVA, radioactivity isn’t such a bad thing—if properly controlled. Thanks to the devastating earthquake and tsunami that struck Japan’s Fukushima reactor four years ago, radiation leakage became a huge problem, leading to a shutdown of its entire nuclear fleet. Unsurprisingly, this coincided with a meltdown in uranium prices, as you can see in Figure 1.

This month’s guest EVA is a retransmission of an essay written last month by my friend and commodity mentor extraordinaire, Simon Hunt. Simon is one of the world’s preeminent experts on copper and, by extension, the red metal’s number one consumer: China. He also is one of the go-to sources for insights into other commodities the Chinese need to fuel their still mighty, though slowing, industrial machine. (To learn more about Simon’s highly informative research service, please click here.)

At our Annual Outlook event last month, I was asked to name my two favorite ten-year investment plays. Regular EVA readers won’t be surprised by my first answer: accumulating high income securities that have been slammed by the triple-whammy of plummeting oil prices, a resurgent dollar, and the blow-out in credit spreads we’ve written about so often in recent months.

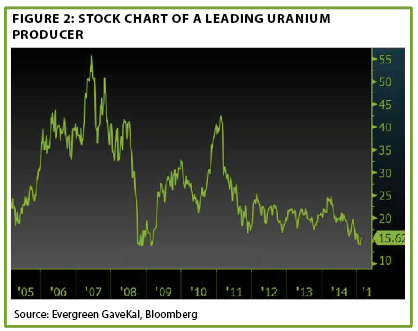

But my other recommendation was uranium and, specifically, the world’s largest producer of “yellow cake,” as U-92 is also known. Because our compliance folks are about as supportive of us naming specific companies as the Seahawk nation was of Pete Carroll’s pass call at the end of the Super Bowl, I’ll leave it to you to figure out the company’s actual identity (though I will show Figure 2 below with the name removed to protect the innocent, as the old TV shows used to say).

Certainly, both uranium and this stock qualify as multi-year laggards, and therefore, might well be poised to become overachievers in the years ahead. With commodities, the old saying “the cure for low prices, is low prices” is almost always applicable. But it’s still nice to have some catalysts. As you will soon read in his piece from last month—and the update he was kind enough to send me this week—Simon offers up a number of those, including that Japan is preparing to restart its nuclear plants.

But the really big driver is China. There are 70 new nuclear plants under construction globally, with 27 in China alone. The Middle Kingdom’s rush to more than double its atomic power fleet from 22 today can be summed up in one very dirty word: pollution. China desperately needs clean energy to avoid widespread and potentially regime-threatening social unrest.

Worldwide, nuclear power has fallen from 17.6% of total electricity production in 1996 to just 10.8% last year. But with the aforementioned under-construction plants, and another 183 on the drawing board (Simon assumes only about 60% of those will get built), that share should begin to rise meaningfully. Thus, future demand is soaring while uranium supply is shrinking due to the closure of mines that are uneconomical at today’s prices and, importantly, last year’s conclusion of the Megatons to Megawatts program. This great-for-mankind initiative (and everyone knows humanity can use all the positive news it can get these days) involved the decommissioning of Russian warheads into commercially usable nuclear fuel stock. But, alas, that is now fait accompli.

As you will also see, the consequence of this is that demand is now beginning to exceed supply, and this gap is projected to meaningfully increase as more reactors are activated and the ravages of low prices continue to inhibit output. In Simon’s mind—and mine—about the only way this can be resolved is by much higher quotes for uranium.

So, listen up all you contrarians—and even those of you who aren’t. This could be one of the most lucrative investment opportunities in a world where those are harder to find than a Seahawks fan who thinks Pete Carroll actually called the right play.

URANIUM NOTE

By Simon Hunt

Introduction

We were told by a good friend to have a close look at the uranium market since there is a prospect of prices doubling over the next two years. As part of our checks we contacted a good friend who supplies consulting services to China’s nuclear industry. He confirmed this optimistic picture and said that personally he had bought some uranium shares.

We decided then to go through the literature to see whether this optimism is warranted. We think it is. Thus, set out below is an aide memoire.

Summary

Demand

There are 70 reactors under construction which will use an average of 150 tonnes of uranium per reactor giving a total of 10,050 tonnes of uranium a year. Assume that 10 of the 13 Japanese reactors restart this year that’s an additional 1500 tonnes. There are an additional 183 reactors on order or planned though no certainty that they will all be commissioned. Assume that 100 are commissioned that is an additional 15,000 tonnes of uranium a year.

Those under construction will need to negotiate their long term contracts – normally around 80% of their feed requirements very soon. This means that uranium demand should jump from 66,000 tonnes to at least 77,550 tonnes by 2020 based on what is known. Given the new safety requirements of nuclear reactors it is more than likely that at least 100 of those on order or planned will be commissioned to give an extra demand of some 15,000 tonnes giving a total forecast demand of around 93,000 by 2020. Demand is likely to rise further in the short term as many utilities which have run down inventories as prices fell will bring them back to normal levels when prices start rising.

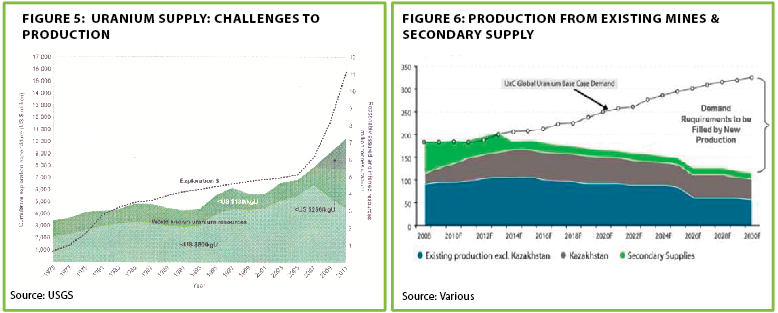

Supply: Mine Production

Mine production accounts for around 86% of supplies. Low prices have resulted in some mines being placed on care and maintenance or on standby. These include all of Energy Fuels’ US mines and the Kayelekera mine in Malawi. Rossing in Namibia has cut production. Cameco will not develop Kintire in Australia. Olympic Dam expansion will not go ahead, at least for now and so on.

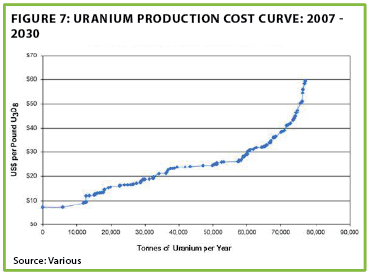

Mine costs are rising quite rapidly. Many miners are not prepared to negotiate prices at current levels. About 40% of mine production is losing money with prices below $40. The chart below shows the impact of rising costs on global supply.

The resources worldwide are available but only at higher prices.

Other Supplies

The big change is the end of the highly enriched uranium purchase agreement (HEUPA) down-blending program of Russian nuclear warheads to commercial nuclear fuel, an annual supply averaging around 9000 tonnes/year. The last shipment was made in November 2014.

Conclusion

A turning point in the supply/demand equation for uranium is in the offing. New known demand with the ending of the Russia-USA blending program will deplete supplies. Civil/military stocks won’t be placed on the market at current prices and may in fact be added to given the current security/geopolitical environment. Utilities have probably run down stocks; they will start replenishing them on any recovery.

The cost curve alone suggests that prices will need to rise to at least $60 to ensure that mines plus secondary sources meet demand.

There is a good chance that prices will double within two years.

URANIUM NOTES: ADDENDUM

In early January we wrote a small report on uranium which seemed to capture a number of clients attention. Since then we have been searching around for more grist to the bullish story.

It emerged in China from a senior executive of China Power Investment (CPI) which is in the process of being merged with China General Nuclear Power Corporation (CGN). What we learnt from within the company is that it has just been given authority to develop its uranium projects and find new ones to meet the country’s burgeoning demand for uranium.

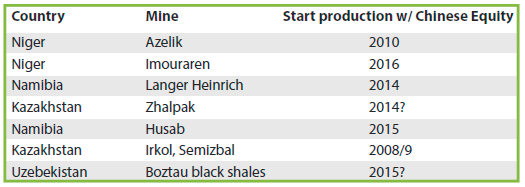

At an industry conference the chairman of CGN Uranium Resources, the uranium subsidiary of CGN, stated that the company already had projects in Namibia, Kazakhstan and Australia and was seeking uranium reserves in Canada.

China’s domestic production is around 1500t/y enough only for about 7000MWe. Its resources are low grade and production has been inefficient. The power companies are not depending on the national goal of sourcing one-third of their uranium demand domestically, but are ramping up their international program to obtain their long term uranium requirements either by market purchases or equity stakes in uranium mines.

Most imports originate from Kazakhstan, Uzbekistan, Canada, Namibia, Niger and Australia. Imports totalled 12,908 tonnes in 2012 and 18,968 tonnes in 2013. Low prices encouraged China to stockpile against future requirements.

China’s known equity stakes in uranium mines include the following:-

The reason for this accelerating nuclear power development is pollution. It is part of the government’s declaration of ‘’war on pollution’’. Other facets of this war are the development of ‘coal by wire’ in which power stations are built close to coal mines with the electricity being transmitted along ultra-high-voltage transmission lines. New smart technologies are being perfected that will increase the efficiencies of transmitting electricity over long distances. Other plans include the faster development of wind and solar energy.

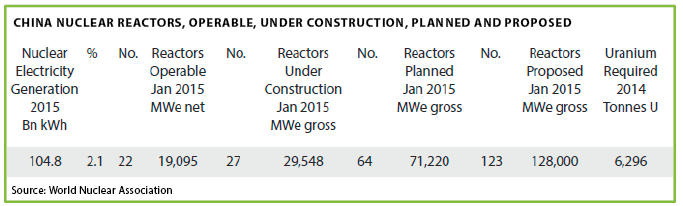

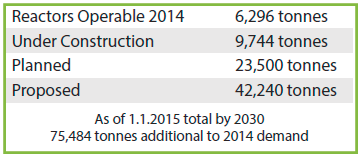

The development of China’s nuclear energy is an intrinsic part of this plan. The World Nuclear Association issued a report that includes only those future reactors envisaged in specific plans and proposals and likely to be operating by 2030 as of 1st January 2015. For China this means the following.

This translates into uranium demand:

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.