“Remember, Fed tightening cycles start off benign but 10 of the 13 in the post-WWII era have ended in tears.”

-DAVID ROSENBERG, Canada’s most prominent economist

“It wasn’t raining when Noah built the ark.”

-Financial commentator HOWARD RUFF

Nearly one year ago to the week, this newsletter made the wild-hair case that the Fed was serious about raising rates. At the time it was a contrarian call—as so many of ours are—because, for years, Ben Bernanke and Janet Yellen had consistently failed to “normalize” interest rates.

The reason for the quote marks is that, even in those days, the US economy was expanding at a slow but steady pace and normal rates would have been multiples above the ½% fed funds rate at the time. On the longer end of things, as recently as the summer of 2016, the 10-year US T-note yield crashed all the way down to 1.3% in the wake of the Brexit vote. Both of those levels were actually below the prevailing rates during the hardest hard times of the Great Depression. Obviously, such itsy-bitsy yields were totally at odds with a growing economy, even one that was expanding more slowly than during prior up-cycles.

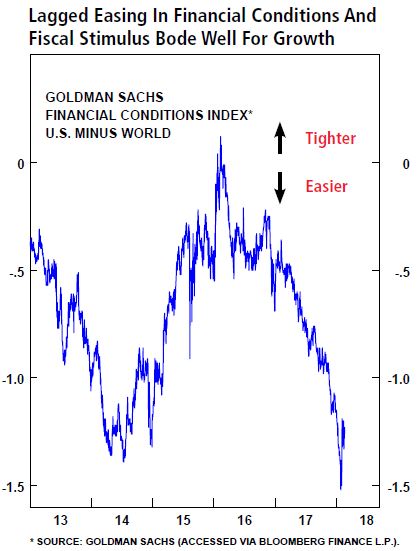

At the same time that the Fed was beginning a timid move toward so-called normalization, its overseas counterparts kept the monetary pedal to the metal. As recently as mid-2017, the level of global quantitative easing (i.e., central bank binge-printing) was running at the hottest clip over the entire post-crisis era. Consequently, even as the Fed has now jacked up its overnight rate six times since it started hiking, global financial conditions have remained exceptionally lax.

Compounding this problem for the Fed, markets themselves have made conditions easier. This is particularly true in the corporate bond market where credit spreads (the gap between treasury and corporate borrowing costs) have remained close to all-time lows.

String bikini-like credit spreads mean companies can still borrow inexpensively to buyback their own stock and goose dividends. It also means that investors remain totally unfazed by the Fed’s belated attempts to take away the proverbial punch bowl. This, of course, is also reflected in a stock market that remains close to its zenith (despite renewed softness this week) and is still one of the priciest in history.

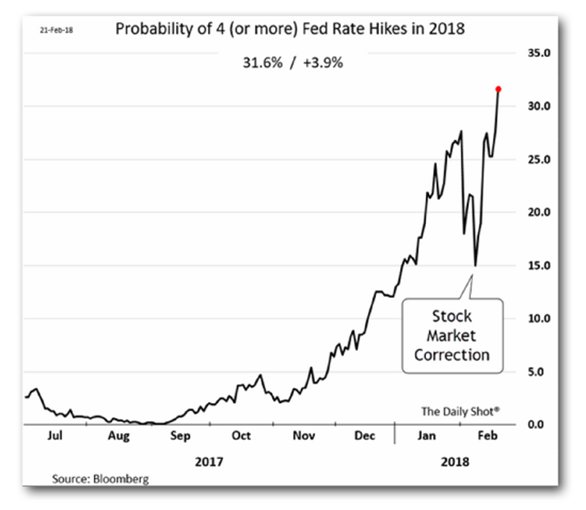

Now, though, we’ve got a new Fed chairman who is, for the first time in decades, not an academic by training. As noted in these pages last month, he’s already shown that he’s cut from a different cloth by not uttering the usual soothing words during the early February correction (unlike his European equivalent who quickly promised to whip up more fake money to bolster stock prices).

Because of this and the fact the US economy is in decent shape, Evergreen has been of the opinion that the Fed is likely to hike four more times this year, rather than the three the markets are anticipating. Ours remains a minority view but you can see that we’re not as out-there as we once were.

As much as I like the initial look of Jay Powell, I have to say that I think he is in a no-win position. His choice is to raise rates slowly and predictably, which may allow asset values to become even more outrageous. Or if, say, a high inflation number rears its ugly head, he might use that as cover to goose rates by ½% rather than the usual ¼% at a single meeting. That would increase the risk of a sudden and dramatic fall in stocks, quite possibly setting off a negative global chain reaction. In other words, he’s damned if he’s gradual and he’s damned if he’s aggressive. Basically, it’s a damn tough fix he’s in.

The greatest yield opportunity in our lifetimes. As many EVA readers know, Evergreen is responsible for managing significant sums of income-oriented assets on behalf of clients. Thus, what happens with interest rates and credit spreads is of paramount concern to us. Frankly, what’s been transpiring—and is likely to at an accelerating rate—is the worst of all possible worlds for yield-focused investors.

Perhaps the easiest way to convey the challenges faced by the yield-needy these days is to imagine the alternative, the “dream scenario”. To do that most credibly, let’s reflect on the global financial crisis (GFC) of a decade ago. As you will see, it was actually a two-step tango to income-generating nirvana despite—or actually because of—the sheer terror that gripped even corporate bond investors in those days.

Clearly, what happened a decade ago was in the extreme almost beyond parallel, with the exception of the early 1930s. Thus, some mental adjustment should be made to scale things down a bit. Yet, the basic sequence is pretty much the same. As the economy begins to overheat, the Fed raises rates repeatedly. Long-term treasury bonds go down in price (up in yield), at least initially. However, as the Fed’s hiking cycle intensifies, market-set rates stop rising. The Fed continues to hike, though, causing the difference between short- and long-term rates to converge and then even invert (meaning short rates go above long rates).

At this point, it’s human nature to say—as I’ve often heard from clients over the last 39 years, whenever short rates rise above long rates—why buy a 20-year bond when I get a higher yield on a 2-year piece of paper? And during each of those prior yield curve inversions my answer has been the same: Because in two years your high-yielding bond will mature and you’ll be renewing at much lower rates. This answer was invariably met with skepticism but that’s what’s happened every time the yield curve inverted.

The next step in the “dream scenario” for yield investors is that in the wake of a long Fed hiking campaign, the economy typically tanks, causing credit spreads to vault skyward. The string bikini becomes more like a show-no-skin swimsuit from the Victorian Era. Thus, even as longer treasury yields quit rising, the market rate on corporate debt starts soaring, often quite dramatically.

In the case of the last crisis, yields went over 20% on junk debt and even high-grade credits like Comcast and Nordstrom’s were yielding in the low teens. Meanwhile, Master Limited Partnerships (MLPs) and preferred stocks were, at their low points, producing cash flow returns in the mid-teens or even higher (in the case of the former).

It was during those panic-stricken days that this newsletter repeatedly urged readers to get out their checkbooks and buy almost everything and anything. About the only asset we didn’t like at the time was cash--the one thing with which most investors were afraid to part back then.

What happened next was the stuff of legends—at least in the staid world of yield investing. Treasury yields, as usual, collapsed after the panic, generating equity-like returns for those intrepid bond investors who had extended maturities as the yield curve inverted.

Once it became obvious the world wasn’t coming to an untimely end, the next move was to sell out of longer treasuries and buy corporate bonds and preferred stocks, particularly from financial entities that now had a government back-stop behind them. Credit spreads began an epic plunge, driving prices on previously trashed corporate bonds through the roof. As a result, conservative securities like preferred stocks posted 145% returns, or more, from March 2009 lows over the next two years – or roughly 57% per annum. The debt-like preferred of AIG went even more postal, rising by 820% from March of 2009 through March of 2011 and eventually up 925% by the time it was called at par in June of 2013.

Junk bonds actually outperformed the S&P 500 from the panic low in the winter of ’08 through the end of 2016, generating 15% per year in annual returns along the way relative to 14.4% for the S&P 500. Now, that was an income rally for the record books!

My, oh, my, how times have changed!

Keeping the bat (mostly) on our shoulders. Today we are faced with the opposite set of circumstances. Unlike in 2008 when the Fed was cutting its overnight rate (following 16 quarter-point increases that raised it by 4% or 400 basis points), the current funds rate is still a long way from what could be considered a realistic peak. In fact, even with this month’s latest boost, the sixth, the fed funds rate is still just 1 5/8% (at its mid-point). This means, net of the present 2%ish CPI, it is still negative by about 3/8% (38 basis points).

When it comes to longer maturity treasuries, even at 2.9% on the 10-year note, it’s hard to get excited about the after-inflation return, especially if we are starting to see wage pressures push consumer prices up further. Meanwhile, credit spreads are near all-time lows. Junk bonds, for instance, are producing a less than pulse-quickening yield of 6% which, adjusted for defaults (likely to explode during the next recession), isn’t worth the risk—save in a few special situations. High-grade corporate credit spreads are also near all-time lows.

So, what’s a rational income investor to do? Much as we hate to suggest it, we think it’s time to prioritize capital preservation over cash flow generation. In other words, it’s one of those Will Rogers—“I’m more concerned with the return of my money than the return on it”—moments.

Warren Buffett has often said he likes to wait for the fat pitch when it comes to buying stocks. Accordingly, it’s logical to assume that if he was more of a player in the income ballpark, he wouldn’t be doing much swinging these days. However, one of the few fat pitches currently available in today’s yield game is to pull cash out of bank and brokerage money funds and buy short-term debt securities. (Based on recent disclosures by Buffett’s Berkshire Hathaway, he is doing exactly that, implying he’s having a hard time finding fat stock market pitches presently).

Frankly, it’s both shocking and infuriating to see how minimally US financial institutions have raised their money market rates. In fact, one of the biggest custodians actually recently cut its money fund yield materially. (It is now paying the average for so-called bank sweep accounts which is a nanoscopic 0.12%!) But don’t get mad, get moving—like into one-year treasuries.

Due to the repeated Fed hikes, you can now get 2% on a one-year T-note. That’s a huge increase from the ¼% to ½% that most banks and brokers are paying on cash. There is a liquidity give-up—but not much. Treasuries are highly liquid and when we encounter the next panic, bear market, and/or recession, the price of the one-year T-note is likely to go up a bit. But that’s a side benefit. The main objective is pick up 1 ½% (150 basis points) or so of return with no risk. We have been doing this in a big way for our clients recently and intend to do even more.

Evergreen, as conveyed for months, is also buying copious amounts of high-grade, short-term floating rate corporate debt. There is more credit spread risk with these but that’s offset by the short maturities and the near-certainty that the rate will be rising materially over the next year as the Fed tightens further (yields on these should be moving up from 2% to near 3% over the course of the year, barring something nasty that would cause the Fed to pause). Moreover, if these extremely defensive and rate-protected securities drop slightly in price, it almost assuredly means that other corporate yield securities have been clocked, creating a stellar buying opportunity.

Most definitely, there is going to come a time before too long to extend maturities with treasuries as we did after the 2013 “taper tantrum”. We could be wrong, but we don’t think 2.9% is it, under current circumstances, unlike in late ’13 and early ’14. Certainly, the extreme present bearishness on the treasury debt market is helping to support prices where they are but once that is worked off we think the downtrend in prices (meaning up-trend in yield) continues.

To sum up this section, we believe preservation of capital is paramount right now which means forgoing some income for the time being. The good news is that for the first time in many years, parking cash is decently profitable—as long as you don’t rely on your bank or brokerage firm to do it for you.

However, there is one area where yields in the 7% to 12% range are very achievable...if you are willing to channel your inner contrarian.

Here we go (down) again! March doesn’t just mean madness in NCAA basketball this year. In the case of MLPs, conditions went crazy last week, as many of you no doubt have noticed.

MLPs have been an alternating source of exaltation and despair for their holders ever since the big collapse that began in mid-2014 and ran until early 2016. Over the last two plus years, in the aftermath of “The Great Thrashing”, they have mounted some ferocious rallies, particularly once sentiment had become ragingly negative, only to succumb thereafter to sharp corrections.

The most recent rally occurred in December and January, lifting the MLP index by about 15% and leaving them up about 50% (or about 65% on a total return basis) from their early 2016 trough. Then came the brief but sharp February stock market seizure. Unfortuntately, MLPs came right down with stocks—despite their husky yields of 7% or more. But, unlike with the S&P, MLPs didn’t bounce back. And then there was last week’s shocker…

On Thursday, March 15th, the Federal Energy Regulatory Commission (FERC) issued a surprising tax ruling, causing panic selling among MLPs. After being down nearly 9% in the first hour following the report’s release, MLPs recovered but still finished 5% lower on the day. They proceeded to rally an additional 3% on Friday, March 16th, before getting slammed again on Monday, the 19th, dropping another 3 ½%. As this EVA “goes to press”, the MLP index remains down 6% from its pre-FERC ruling level, which was already quite depressed.

The reason for the negative reaction—which we would characterize as an overreaction—was a change the FERC made to the way certain MLPs charge their customers. In making its decision to disallow MLPs from collecting an income tax allowance (essentially, for assumed taxes paid by the underlying MLP holders), the FERC reversed a multi-decade precedent.

Fortunately, for the majority of MLPs, including most of those Evergreen owns for clients, this is either a non-event or of minimal impact. In some case, though, cash flows are likely to be hit. In some rare cases, we have seen estimates as high as a 20% reduction but, again, those are the outliers.

The fact that the entire sector was spanked so hard leads us to believe it was a classic case of throwing the baby out with the bath water. As usual, we are attempting to capitalize on the blind selling which may have been exacerbated by computerized trading. These programs are often set to sell instantly when their algorithms recognize something adverse but, often, these applications of artificial intelligence tend to be more “artificial” than “intelligent” (as was also seen early last month with the overall stock market).

Beyond the FERC ruling, we believe fundamentals have generally improved for MLPs over the past year as US oil and gas production has been on a steady incline. In fact, as the MLP sector has recently dialed back on new projects, we envision capacity becoming extremely tight in coming years. This is particularly probable given the difficulty of securing permits for new projects and forecasts of significant production growth over the next five years. Consequently, we believe the likelihood of MLPs enjoying improved pricing power going forward is quite high.

It further appears that this ruling will not go into effect until 2020 and we would expect an industry appeal of the FERC’s decision almost immediately. Of course, that may be unsuccessful, and we do think it’s realistic to expect this event to reduce the recovery potential of at least some MLPs. Additionally, refunds of past rates may be required in some cases.

As a result of all of the above, Evergreen believes MLP investors should stand pat and if they have room for additional purchases to begin dollar-cost-averaging into them now. It may make sense to do some swapping out of the issues most exposed to the FERC ruling and into those with less regulatory risk but the market price for the latter group appears to be pricing in a worst-case scenario—and then some.

One thing that has hit me as I’ve read a slew of research reports on MLPs recently is how cheap many of them are trading on a P/E ratio basis, even before the latest tumble. Typically, reported earnings for MLPs are well below cash flow available for distribution or, as it’s popularly known in the industry, distributable cash flow. This is due to the significant amount of depreciation MLPs are able to record, sheltering much of their income from taxation but also increasing the P/E (by lowering the earnings figure in the price/earnings ratio).

Mid-teens P/Es are now becoming commonplace and in some cases, they are even approaching 10 times earnings which is something I’ve never seen in over 30 years of owning MLPs (perhaps save for a very brief period in early 2009, when almost everything was totally crushed, and the 2015 energy collapse).

It’s also interesting to compare how MLPs have done versus the mighty S&P 500 since the start of this century/millennium. As you can see below, despite having experienced a bruising bear market in recent years, and being pushed down yet again, their returns have greatly exceeded that of the S&P.

Source: Bloomberg, Evergreen Gavekal

Source: Bloomberg, Evergreen Gavekal

We are sticking by our belief that MLPs are poised to do a replay of what happened when the stock market bubble of the late 1990s exploded. As you can also see, MLPs returned 49.12% from the 12/31/99 to the market trough in 2002, even as the S&P lost a whopping 45%.

Source: Bloomberg, Evergreen Gavekal

Source: Bloomberg, Evergreen Gavekal

Yes, it’s a trying time to be a MLP investor if you are simply looking at their recent performance and since mid-2014. Yet, as the legendary Howard Marks once wrote: “Most great investments begin in discomfort…bargains are usually found among things that are controversial, that people are pessimistic about, and that have been performing badly of late.” Discomfort...controversial…pessimistic about…performing badly of late. When it comes to MLPs that would be check, check, check, and check. As a matter of fact, the same thing could have been said about them in early 2009 and at the start of 2016, right before they checkmated all the naysayers. It could be that we’re on the verge of a three-peat!

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.