"The only function of economic forecasting is to make astrology look respectable."

- John Kenneth Galbraith, one of the 20th Century’s most venerated economists

Another year, another blur. Every year I’m struck by how quickly it’s time to write our annual forecast EVA, and this year is no exception. It continues to be my belief that there is a theory of relativity at work as you get older: When you are 10, a year is 10% of your life but, when you’re pushing 60, it’s less than 2%. As a result, the passage of time does seem to shift gears from leisurely to head-snapping as we become "mature"—chronologically, if not emotionally. (Some of you may have heard the old joke: What’s the difference between a bond and a man? The bond eventually matures.)

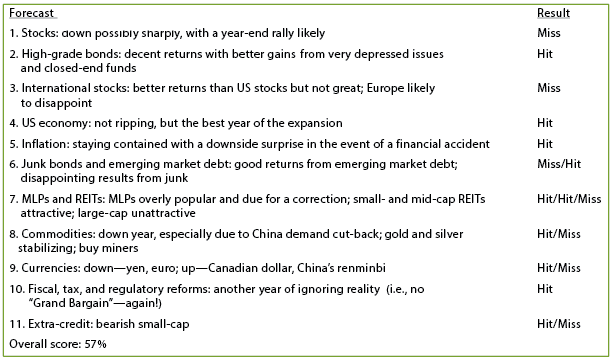

As is our custom in this issue, we will first review our forecasts from last year and then make a few brief comments before focusing on what we see unfolding in 2015.

Once again, the US stock market was my glaring mistake. My belief was that, correctly as it turned out, the Fed would continue to dial back on QE3 (the infamous taper) unless stocks fell out of bed. But where I was wrong was in believing that as QE3 neared its end, stocks would suffer. For a time, in October, they did, and the Fed quickly made noises about more monetary amphetamines. This did the trick and triggered the year-end rally I felt would happen if stocks sold off hard. But the reality is that the S&P 500 only experienced a mild correction in the fall, followed by a vigorous rally, so this was a clear whiff on my part.

The bullish bond call, though, was both lonely and spot-on. The only quibble is that I wrote the 3% level at the start of the year on the 10-year treasury probably wasn’t the peak in yields when, in actuality, it was. However, I was definitely among the few who felt bonds were attractive. Moreover, tax-free closed-end bond funds bought during the taper-tantrum produced excellent total returns, essentially rivaling those of stocks. High-grade intermediate term corporate bonds produced decent, if not S&P-like, returns.

In order to focus on next year, I’m not going to review all of the 2014 calls in detail but there are a few others, which I’ll discuss. First, with emerging market debt and junk bonds, that might have deserved a bit better score based on my view there would be considerable dispersion between bonds from healthier developing countries faring much better than those with current account deficits and/or fragile finances. We liked Chinese debt, for example, and that performed well even as the bonds from countries like Russia and Venezuela were crushed. As 2015 progressed, we also made it clear that we felt the lower-tiers of the junk bond market were where the trouble would hit, which turned out to be accurate.

Our MLP call was solid and we went into the fall with the lowest allocation to this asset class in years. This helped mitigate the damage from what became a true bloodbath for these generally stable securities in the fourth quarter. We also did well with some of the small- and mid-cap REITs we owned or bought during the year. However, large-cap REITs also had a strong year.

The commodity forecast would have been superb had we not suggested buying gold producers. They worked for awhile in the first half of 2014 and then fell down the mine shaft once again.

As far as small-cap stocks went, that was actually a pretty decent prognostication as they did materially lag the market. They were also slammed hard in the fall, tumbling over 15% from their spring apex to their autumn trough. Nevertheless, small-caps rallied enough at year-end to finish in the black.

Now for our views on 2015…

Forecast #1: Stocks. It’s heel digging time! We’re not waving the white flag despite the US market’s impressive imperviousness to sustained selling pressure. It’s more than stubbornness; the fact of the matter is that the higher stocks soar, and the longer the bull runs, the more vulnerable they are. It continues to amaze me that so many feel that the further the market rises, the better the future outlook becomes when the math—and over a century of data—screams the opposite. But, one prominent sell-side Wall Street strategist just proclaimed that the bull has another five years to go! That would make this up-cycle four years longer than any previous winning streak. I’m not thinking so!

A constant bullish refrain I hear is that stocks aren’t as zanily overpriced as they were in the late 1990s, and that’s true in some ways. But on our preferred price-to-sales ratio, the median stock is actually more expensive than it was in that ultimate go-go era.

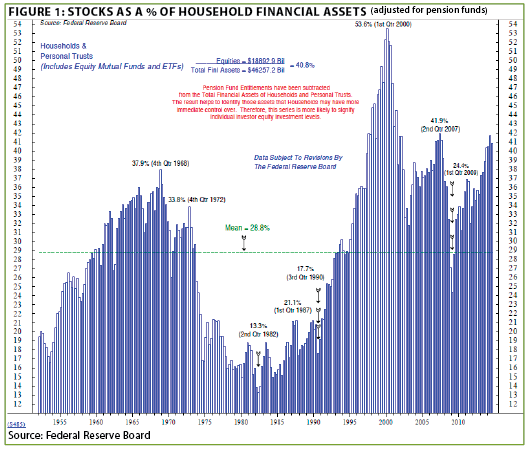

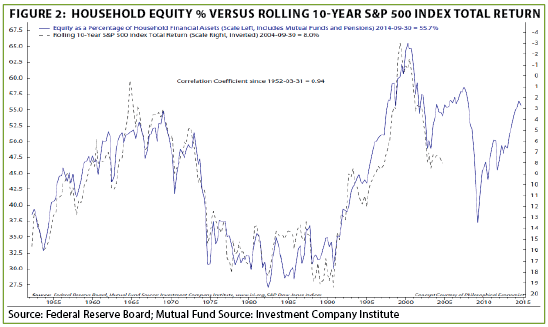

Similarly, as Ned Davis Research points out in the following charts, US households already have the second highest commitment to stocks as a percentage of total financials assets ever (essentially tied with 2007). And, per Figure 2 (on the next page), you can see that this has been a remarkably accurate measure of future returns. In other words, when investors are loaded up on stocks, gains over the next ten years are sub-par and when they are light on equities the opposite is true. As far as I know, they are the only firm that has run this intriguing study. (Note, the return scale is inverted in Figure 2.)

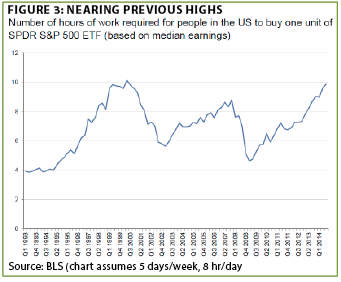

The following chart is also a unique way of looking at stock market valuation and tells much the same story.

Last year, we felt the odds of a "crashette" were unusually high but, as I pointed out, that didn’t mean an air-pocket type event was likely. These are always low probability situations. But the additional passage of time and the further upside extension continues to raise those odds.

The equity area we targeted for poor performance—small-cap issues—did materially lag in 2014, as mentioned on page 1, but they still rose. We’re expecting a serious break this year, not just relative underperformance.

Overall, we think there will be a deep pull-back in the broad market at some point, likely causing the Fed to float the notion of QE4, particularly if the decline is part of a deflationary shock scenario (more on this under inflation). Yes, I realize this might seem really strange if the Fed has, at long last, started raising rates prior to any market convulsion. Yet, one thing we’ve all learned is that what seemed impossible a few years ago is anything but these days.

Forecast #2: Bonds. We’ve already seen a notable divergence since last summer between longer-term US treasury issues and corporate bonds, even of the investment grade variety, and we think more of the same is possible. Like almost everything in this year’s set of forecasts, so much is contingent on whether fears that the global economy is coming off the rails continue to build as 2015 progresses.

Frankly, it’s a bit daft, as the Brits say, to be making forecasts when none of us has seen this set of conditions before. There is simply no precedent. Accordingly, take our predictions, and any other firms’, with much more than a grain of salt—make it a Costco-sized bag, if not a couple.

But, irrespective of the qualifiers, we believe that the bond, currency, and commodity markets are sending us an urgent message that something is very much amiss. This is despite the standard-issue sunny outlook from virtually every Wall Street brokerage house (which should be enough to make experienced investors extremely wary).

Therefore, when it comes to fixed income, we think US treasury yields can surprise on the downside. With corporate bonds, we already see considerable value but we are mindful that credit spreads might expand further. Our plan is to hold an increasing amount of cash and treasuries as the year unfolds. Even if corporate bonds fall further, losses should be minor and the yields they would then offer will be truly compelling.

Forecast #3: International stocks. We are steadfast in our belief that many overseas equities offer better multi-year return prospects than does the S&P 500. However, if things get panicky, cheap markets can become even cheaper. It’s likely that, as in 2014, results are going to be highly varied with some markets, like most of those in Asia, performing well, at least on a relative basis, and others continuing to swoon. Ergo, color us neutral to cautious on international shares for 2015, with Asia deserving a better rating, as valuations are attractive and it is a big beneficiary of cheap oil.

Forecast #4: US Economy. Barring a really nasty shock of some kind, we believe the US economy will remain in expansion mode. However, we feel it is likely to decelerate as the year passes. Those who say a recession is virtually impossible because, for example, the yield curve is far from inverting (short rates higher than long rates) may be missing a sea change.

In the past, we have been ardent supporters of the yield curve inversion indicator. Our focus on that led us to be one of the few firms forecasting a recession back in the fall of 2007, the last time the curve inverted.

However, in a post-credit bubble world, such as we are in now, we are of the belief that recessions can happen in the absence of inversions. Look at Japan for the last 20-plus years or Europe since the Great Recession: There have been multiple recessions without short rates exceeding long rates (this also happened in the US in 1937, a period we believe bears some resemblance to current circumstances—huge credit bust, big recovery, increasing isolationism, anti-business administration, regulatory over-kill, etc.).

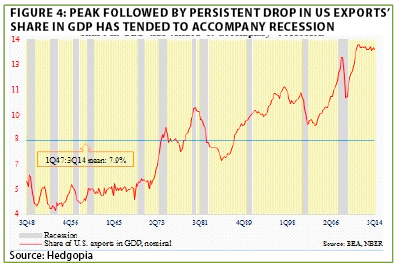

The following chart, from the excellent financial blog Hedgopia, also raises a bit of discomfort regarding what looks to be a rolling over in US exports as a percentage of the economy. This has been problematic in the past other than during the mid-1990s soft-landing.

The bottom-line, in our view, is that the next US recession is not likely to be caused by a flip in short versus long rates but rather by a financial market paroxysm of some kind.

Forecast #5: Inflation. It is once again a hot topic but, this time, because prices are so cold, rather than the usual angst about overheating. Get ready for even more chilling news on inflation.

We plan to home in on this vital topic in an upcoming full EVA, but if one were looking for signs of a deflationary shock in the making she or he would be on alert for:

Maybe this is some kind of epic head-fake but I have to say our deflationary-accident sensors are in full alert mode. The US stock market seems to be taking a bit of notice lately but, then again, it has whistled past so many graveyards it clearly has no fear of mortality.

This may be the most important topic to monitor in 2015. Longer-term, however, the pendulum could swing back to inflation, possibly of the high-, or even hyper-, variety down the road. As noted in past EVAs, William White, former chief economist of the central bank’s central banker—the Bank of International Settlements (BIS)—has warned how quickly deflation can morph into hyper-inflation. Are all you architects of Abenomics* (reputedly including Paul Krugman) listening?

Forecast #6: Junk bonds and emerging market debt. This could be a case of "rough start, strong finish." Our sense is that there could be one of those exceptional buying opportunities with both high-yield and developing country bonds at some point this year. If history is any guide, the closed-end funds that specialized in them will provide the highest returns once the bottom is in. Even now, debt from developing countries appears undervalued but, especially if a deflationary accident occurs, it could become much more so. Our preference in this space remains high-grade, high-yield bonds where we believe positive returns are likely.

Forecast #7: MLPs and REITS. Unlike MLPs, REITs have continued to levitate. A simplistic reason is that the latter doesn’t have energy exposure, unlike the former. Fair enough, but REITs were big-time victims of the last deflationary bust in 2008/2009. If we do experience another, their lofty valuations and yields that are barely half of most MLPs are unlikely to provide much downside protection.

We certainly won’t be surprised to see MLPs weaken further, and plan to up our buying if they do, but large-cap REITs look far more vulnerable. Net/net, we see a somewhat down year for MLPs with a rally by year-end; for the REIT index, we are anticipating the worst year since 2008 (though we doubt it will be anywhere near as calamitous).

Forecast #8: Commodities. These have been so bombed-out that a powerful snap-back rally or two is highly probable. But our view is that, outside of precious metals, it’s going to be another challenging year, even if less painful than 2014. What could light a fire under commodities would be if certain central banks actually start printing currency (or directly sending checks to its citizens) in order to fight inflation. The Fed implementing QE4, in the event US stocks fall precipitously, could also catalyze a commodity comeback. We see gold and silver generating positive returns but our favorite natural resource is becoming uranium, where prices are below production costs for many miners. Further, there are several positive factors converging to jump-start U-92, including new reactors coming on-line in China and old ones returning to service in Japan.

*Japan’s last-ditch effort to vanquish deflation and catalyze growth.

Forecast #9: Currencies. The dollar has become the Taylor Swift of the currency markets, but we won’t be surprised if its uber-popularity wanes a bit in the next few months. Any setback is likely to be brief, however, and fairly shallow. Should a deflationary accident of some sort hit, it is almost certain to be highly supportive of the dollar.

Long-time EVA readers know that we have been bullish on the dollar versus the yen and the euro for most of the last four years. That has worked extremely well for Evergreen clients and the trend is still our friend. However, we feel much of the upside has been realized (barring a disaster in either Europe or Japan, neither of which is out of the question). As far as the Canadian dollar is concerned—a long-time favorite we’ve been wrong about—we think the extended outlook is very positive. Once again, though, should there be a crisis of some kind, the dollar is an odds-on favorite to rise further, even against the Loonie. Hopefully, that will happen from a higher point than its current deeply undervalued level. Canada may also be one of the few countries to join in raising rates along with the Fed if nothing nasty this way comes.

The biggest aspect about currencies, however, is that the devaluation one-upmanship is arguably the most powerful force behind the rising deflationary tide. Frankly, we missed this until a year or so ago, but we now get it and it’s another flashback to the 1930s, when countries sought to steal market share from each other through currency debasement. Unfortunately, we don’t think this bloodless war is over.

Forecast #10: Geopolitical. We profess no ability to predict what might snap, but we agree with famed economist and historian Niall Ferguson that America’s military and foreign policy "taper" is making this always tumultuous planet even more unstable. This, combined with some serious economic pain now being felt in many countries, is a dangerous mix that we believe will lead to unpleasant surprises this year which is a good segue to my final anticipation…

Forecast #11: Extra credit. The Year of Living Undangerously. Admittedly, I’ve trotted out this word-play on the old Mel Gibson movie a few times over the last twenty years (as some really long-time clients might recall), but it sure seems apropos to recycle it now. In this case, I’m referring to the financial markets and the return of that long dormant characteristic known as VOLATILITY.

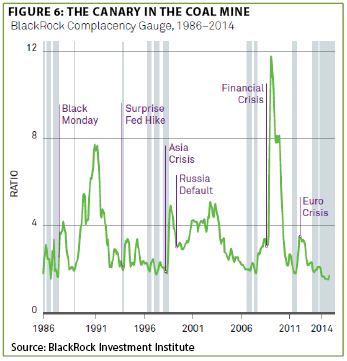

Prior EVAs have noted that 2014 was one of the lowest volatility years on record, at least for US stocks. Similarly, the mammoth money manager Blackrock recently noted in their excellent 2015 Investment Outlook that there has been a tremendous bull market in complacency—and an equally powerful bear market in volatility. This strikes me as totally inconsistent with the world we know.

Central banks have won the battle to suppress downside volatility for now but will they win the war? The extreme price swings—mostly in a decidedly southerly direction—recently afflicting so many markets would indicate that perhaps the answer is no.

It’s certainly possible a deflationary convulsion of some kind can be avoided (though, for anyone directly, or indirectly, involved with the energy business one has already occurred). It’s also reasonable to believe that volatility will rise gently, not explosively. In next week’s Evergreen Exchange EVA, we will examine the three most likely volatility scenarios including where it merely normalizes. However, it continues to be my personal belief, as I’ve conveyed before, that years and years of artificially repressed volatility is highly likely to lead to an extremely chaotic release of that pent-up pressure.

Yet, at least when it comes to US stocks, most investors, judging by their totally relaxed attitude, seem to believe my apprehensions are seriously misplaced. That’s been a valid criticism for the last couple of years, but as Woodrow Wilson said a century ago: "I would rather fail in a cause that will ultimately triumph than triumph in a cause that will ultimately fail." That’s a darned good saying for investors to keep in mind these days.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.