Below are Evergreen Gavekal's Likes/Dislikes for December 3rd, 2021.

It’s not often I call attention to this section in our main EVA; in fact, I can’t recall ever doing so in the past. However, as I wrote in that part, there are some strange and significant things happening in the US stock market of late.

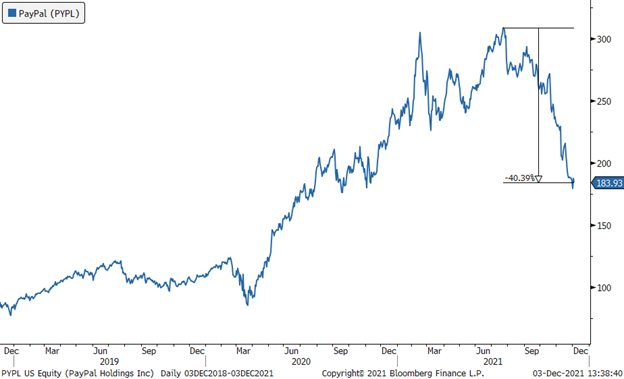

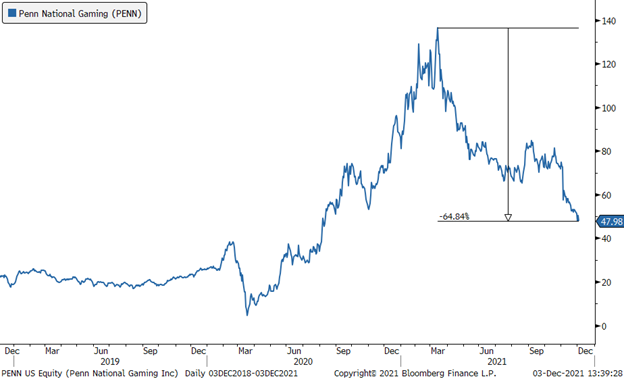

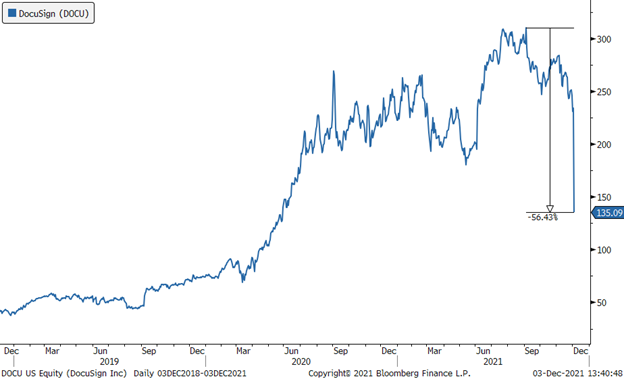

Per the comments in the main EVA about the divergence in new highs and lows, as well as the deterioration in the advance/decline ratio, even before Omicron I was surprised by the number of stock charts I was reviewing showing obvious erosion. This week, that phenomenon has gone into hyper-drive. Consider if you will the following charts of some of America’s more exciting growth companies:

Certainly, all three were trading at P/E ratios that looked like temperature readings in the Mojave Desert at mid-day in July. Accordingly, they were exceptionally vulnerable to this type of shellacking but they are not isolated examples. There is definitely spreading trauma out there.

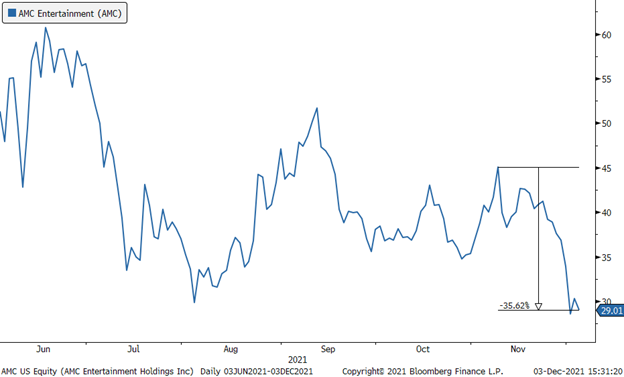

For example, when it comes to some of the most popular “meme” stocks—the playground of the Reddit/Robinhood “investor” cohort—the damage has been equally breathtaking, at least in some cases. AMC Entertainment is one graphic (literally, per the below) case in point. At least, I feel a 36% decline in about three weeks is breathtaking, though some companies, like Docusign show above, have managed to do that in a day.

My fellow newsletter scribe Kevin Muir, author of The Macro Tourist, one of my many must-reads, put out an extremely timely note earlier this week titled “The Pain Beneath The Surface”. Here was an amazing factoid he ran:

- During the 4th quarter of 2018, when the S&P 500 lost 20%, there were 380 stocks in the universe of common stocks that were above $2 and met a minimum volume threshold, that were down more than 25% in the previous month.

- Contrast that to Wednesday, when the S&P 500 was down 4% from all-time highs, yet there were more than 486 stocks with that same criteria that were down more than 25% over the previous month.

Kevin went on to point out:

“At the end of November, the S&P 500 had corrected only 3.88% from its all-time high. In the grand scheme of things, if you were looking at America’s largest capitalized stock index, it didn’t seem that bad at all.”

But, again per Kevin, here’s another shocker:

“Only 4.5% of the Russell 3000 stocks are above their 10-day moving average. This is a new low not seen since the March 2020 COVID crisis.” (Emphasis mine)

Kevin went on to point out that the overall market is being supported by a handful of mega-cap stocks, essentially, the famous FAANGM darlings (Facebook, Apple, Amazon, Netflix, Google, Microsoft). Of this illustrious assemblage, only Amazon has had a seriously sub-par 2021. Yet, as any veteran market participant is aware, a market that is propped up by a limited number of issues is highly vulnerable to nasty surprises. Lately, we are seeing that vulnerability playing out with a vengeance.

He also correctly observed that investors are storming out of their losers to buy more of the seemingly impregnable FAANGM-type issues. With year-end approaching, tax-loss driven selling might magnify this trend, as it so often does.

In my over 42-year financial career, I don’t recall ever seeing a time when there have been such a large number of stocks getting crushed with the broad market still within spitting distance of an all-time high. It could be we are setting up for a powerful year-end rally were the loser catch up with the winner. Or it could be the more typical situation where the market generals follow their troops into a frantic retreat.

If it’s not Omicron that’s behind this sub-surface carnage, what’s at work here? In my view, inflation has been increasingly nipping at the S&P 500’s heels in recent months. Market history is clear that rising inflation is problematic for high expectation/P/E stocks in particular (and it’s not great for most other equities, either.)

For many months, the market was pacified by Jay Powell’s repeated assurances that inflation was transitory. Lately, though, he has had to publicly (and embarrassingly) recant that view. This week was especially notable in that regard. When testifying before Congress, he indicated a refusal to stop the Fed’s just-begun tapering due to Omicron. Rather than focus on the economic risks, Mr. Powell homed in on the inflationary potential. Even worse, he stated the Fed might taper faster. This was not what the stock market wanted to hear.

This November and December are beginning to feel a lot like those months back in 2018. If you don’t recall, the market fell hard at year-end, when it usually rallies. The culprit was Mr. Powell himself who back then was telling the world that he would keep tightening, despite the S&P’s deepening swoon.

But, there’s a YUGE difference between then and now. In late 2018, the Fed had been tightening for a year, raising its overnight rate to 2 3/8% (today, you can leave off the 2) and also selling off hundreds of billions of its cache of treasuries (all bought with its magically fabricated money). Today, it is still in the easiest stance it has ever been—save for a few weeks ago when it was printing slightly more than it is now—emphasis on “slightly”.

Not only that, at the end of 2018, inflation was a non-issue. That’s lightyears from where we are today. Consequently, it’s exceedingly hard, if not impossible, for the Fed to come to the market’s rescue. This realization is, in my opinion, behind the sudden breakdown in a multitude of stocks.

As noted in the main EVA section, even reasonably priced value shares have not been safe-havens. This includes the energy sector, a long-time favorite of this newsletter.

Despite its detonation this past Friday, energy overall remains up over 51% in 2021 while the more conservative midstream infrastructure (e.g., pipelines) has still generated more than a 35% total return basis (i.e., including their high distribution payouts).

Valuations, which were attractive prior to this correction, are now mouth-watering. In many cases, dividend yields are several multiples of what the 10-year T-note pays. After the enormity of the up-move pre-Omicron, a sharp correction was almost a given. Well, it has happened and it is now time to go on the offensive. The shortages of oil and natural gas aren’t going away, at least not in my view nor that of the best energy pundit I know, Mike Rothman.

In twin podcasts this week (one with CNBC regular and star economist David Rosenberg), Mike made a very persuasive case why we’ll see even a greater deficit of crude oil in 2022 than we have today. He continues to believe triple-digit oil prices are probable next year, as do I. If so, there are bountiful profits to be made buying at current valuations for leading energy producers.

Because I am a believer that Omicron is not going to seriously impair the global economy, I feel that positivity should extend to almost all cyclical market sectors. These bounced nicely after the Delta variant fears receded and I think that will happen once this virus scare runs its course. Many economically sensitive issues may be tax-loss selling victims so they can certainly get cheaper between now and year-end but, again, my best advice is to dollar-cost-average into them if they do. Tax related selling tends to peter out by mid-December so the window of weakness should close soon.

One last point I’d like to relay before closing is one of this newsletter’s main theme since the start of this year—namely, my oft-repeated hostility toward what I have often called the Crazy Over-Priced Stocks or COPS. Many of these were being pounded even before this out-of-the-blue cliff-dive. Since then, it’s been a dizzying decline and, in most cases, they remain value-free. In other words, unlike sectors like energy, even though they are down considerably, they are no bargains. However, many former go-go names have come down enough to justify nibbling on them. So…nibble way and get ready to do some serious chomping soon.

LIKE

- Large-cap growth. (Avoid those that are beneficiaries of the flight into perceived mega-cap safety, per the above commentary.)

- Certain international developed markets, especially Japan (Use the recent pull-back for adding to or initiating position in ETFs like EWJ. The Japanese market should be a beneficiary of overseas investors pulling capital out of China.)

- Publicly traded pipeline partnerships, i.e., MLPs and other mid-stream energy securities. (Buy on weakness!)

- Gold-mining stocks (Ditto!)

- Gold (The miners appear far more undervalued at this point.)

- Silver (It has more snap-back potential than gold currently.)

- Select international blue chip oil stocks (Again, it’s time to be a buyer for long-term, contrarian investors.)

- Short-term investment grade corporate bonds (1-4 year maturities; favor shorter maturities due to rising inflation risks because of the likelihood that the Fed and the Treasury are over-stimulating the US economy.)

- Emerging market (EM) bonds in local currency (focusing on stronger countries, particularly in Asia)

- Large-cap value (Once more, per the above commentary, use Omicron-driven weakness to accelerate accumulation.)

- High-dividend equities with safe distributions (These, too, have been hit; thus, add selectively though they lack the rebound potential of more aggressive issues, outside of economically-sensitive areas.)

- Most cyclical resource-based stocks (Buy more aggressively.)

- BB-rated corporate bonds (Buy more selectively after a spectacular rally and favor shorter maturities.)

- Canadian REITs (Avoid office issues for now.)

- South Korean Equities (S. Korea remains one of my favorite markets.)

- Certain “Virus Victim” equities such as refiners, homebuilders, and select retail stocks (Certain retailers look extremely attractive right now, especially one that is based in Seattle with a famously generous return policy.)

- Investment-grade floating rate corporate bonds (Despite a vigorous rally this year, there remains decent long-term value in this bond market niche.)

- The higher quality mortgage REITs (Previously, we had recommended profit-taking; use recent weakness for re-accumulation.)

- Floating rate bank loans (Although GDP growth this quarter came in much slower than Q2, this should be a pause not a reversal. Thus, the still healthy US economy reduces default risks and the floating-rate structure of bank loans mitigates inflation risks.)

- Copper producers. (The largest US copper producer has declined about 11.3% recently, creating an attractive entry, or further accumulation, point.)

- A relatively new sector recommendation is healthcare stocks. Many have corrected and are trading at alluringly attractive valuations, often with lush dividend yields. (Use the recent weakness in some pharma names to accumulate; others, though, have rallied hard and in those cases decrease accumulation.)

NEUTRAL

- Uranium and uranium producers (There are better opportunities elsewhere for now.)

- Renewable Yield Cos (Based on the hefty rally that has occurred with this group in recent months, justifying our buy rating on them earlier this year, we are downgrading them to neutral; some profit-taking is reasonable despite bright long-term prospects.)

- A wide range of high-income securities, including preferred stocks (Preferred stocks look less attractive with prices up, yields down, and inflation risks on the rise. As with bonds, we prefer the floating-rate variety.)

- Intermediate-term investment-grade corporate bonds, yielding approximately 2.25% (Now rated neutral due to our increasing inflation concerns and the paucity of attractive yields; they have been under pressure lately due to rising rates overseas and escalating inflation concerns.)

- Mid-cap value

- Emerging stock markets; however, a number of Asian developing markets look undervalued (Caveat investor: These are much less bargain-rich than they were a year ago. China is an exception; its market has been crushed creating interesting value plays for brave investors. However, it’s continuing war on its best companies is a large and legitimate concern. Further, I would note key Chinese equities are breaking multi-year support.)

- US-based Real Estate Investment Trusts (REITs) (It is critical to be highly selective with this sector; however, the reopening of the US economy, despite recent challenges, should relieve pressure on some of the most impaired sub-sectors of the REIT universe—unless they are exposed to cities and/or states that are seeing significant population and business outflows.)

- Cash

- Canadian dollar-denominated short-term bonds (The recent yield spike makes these even more interesting—literally.)

- One- to two-year Treasury notes

- Traditionally “safe” sectors such as Staples and Utilities (Most utilities have had healthy price bumps lately; consequently, they are less appealing.)

- Virus Victors (I.E, those companies that have benefitted from global lockdowns and now sport premium valuations. Many have retreated significantly of late; Clorox, for example, remains down materially from its peak.)

- Small-cap value (This style has corrected 9% of late; however, it has held up considerably better than its growth-oriented peer—see below.)

- European banks (Shifting these back to neutral due to improving vaccination prospects on the Continent. Still-prevailing negative interest rates in Europe are very hard on bank profitability.)

DISLIKE

- Intermediate-term Treasury bonds (They have rallied lately due to pervasive negative sentiment—in other words, they were oversold—and Omicron-driven growth fears; longer-term, all distant maturity treasury bonds look decidedly unattractive.)

- Small-cap growth (Since late-February, around the time of our negative call on this style, it is now down 14%; in fact, it has swooned by that amount in just the past three weeks.)

- As a relatively new tactical recommendation related to the above bullet, investors seeking to reduce equity exposure might want to buy an inverse small-cap ETF. One of these offers twice the upside—and downside—of the small cap index; i.e., should small caps fall 10%. (After the recent correction, this position is slightly positive.)

- Long-term treasury bonds (These are in the dislike category due to both Evergreen’s and Gavekal’s rising conviction in a looming burst of inflation; despite a now faltering rally over the last few months, long-treasuries remain down 2.8% on a total return basis this year.)

- Long-term investment grade corporate bonds (These are viewed negatively because of the narrow yield gap, or spread, between corporate debt and treasuries combined with our escalating inflation fears. However, there are a smattering of long-term issues that still offer attractive yields. Long-term corporate bonds have had a negative total return of -0.5% for the year.)

- Most municipal bonds (Munis have bounced a bit lately but we remain negatively disposed to longer issues.)

- US dollar (The dollar has rallied recently, pushing it up roughly 6.9% for the year. This is despite the fact that the US is running a trillion-dollar trade deficit and the Fed continues to fabricate money at a $1.5 trillion annualized rate. Thus, the dollar’s long-term outlook appears very challenging and it remains overvalued versus many currencies, especially those in Asia.)

- Many semiconductor tech stocks (Semis have held up comparatively well during the shakeout; many of these names look extremely pricey and hence vulnerable.)

- Mid-cap growth

- Lower-rated junk bonds (For the first time ever, junk bonds “provide”, on average, a yield below inflation; thus, their other moniker, high yield, no longer applies. In my view, the lowest rated junk bonds offer the worst/risk reward.)

- Green energy stocks (Note, this refers to equities not the Renewable Yield Cos; most of the former had explosive up-moves in 2020 and into this year; lately, though, many green energy plays have been hit hard, especially the dodgiest issues like Lordstown Motors and Nikola. The recent new EV truck maker Rivian looks ludicrously overvalued; justifying that negativity, it has lost about 40% of its value in recent weeks.)

- SPACs (Special Purpose Acquisition Companies, which are structured to greatly favor insiders and disadvantage retail investors. The SPAC ETF has fallen 36.2% from its February highs, justifying our negative stance on this highly speculative slice of the market.)

- Most new issues (Earlier this year, the IPO market was as frothy as I’ve seen it other than the giddiest days of the dot.com era; there are also signs the new-issue craze is fading, even though some recent IPOs have had explosive moves…if you were able to attain shares at the initial offering price, which every few are. Be very careful about chasing these in the secondary market.)

- Despite a disastrous February, most of the popular Reddit/WallStreetBets stocks still have material downside. (As noted above, my repeated bearish views on these lottery tickets has been vindicated, at least for now.)

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.