"Like all bubbles, these exaggerated increases (in commodities and other higher risk assets) can rapidly reverse when interest rates return to normal levels."

-MARTIN FELDSTEIN, former chief economic adviser to Ronald Reagan, referring to the Fed's QEII program

POINTS TO PONDER

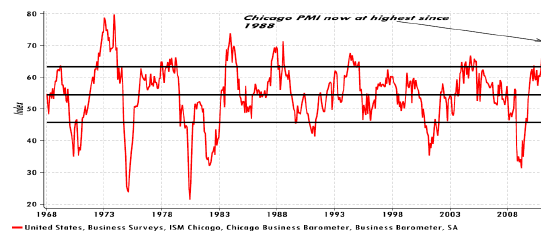

1. Continuing the pattern of conflicting economic releases, the Chicago Purchasing Manager’s Index is now at its highest level since 1988. However, US fourth-quarter GDP was revised down from 3.2% to 2.8%, heavily influenced by a sharp contraction in state and local government spending.

2. The public worker labor strife continues in Wisconsin, reminiscent of the federal standoff with the air traffic controllers’ union 30 years ago. Salaries are not the issue; the average Milwaukee teacher’s pay is a reasonable $57,000. However, once multiple benefit plans are included, total compensation rises to $100,000.

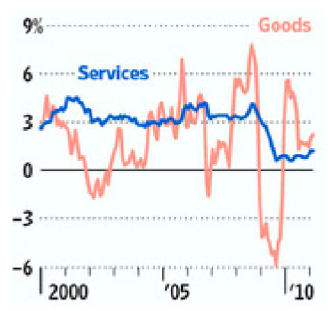

3. For most of the last decade, inflation in services exceeded that in goods. Over the last year, this has reversed with goods inflating at a 2.2% rate while services rose just 1.2%, far below the average rate of increase of 3.4% seen by the latter from 2000 through 2008.

4. For the majority of state and local governments, the new fiscal year begins in July and most are planning broad spending cuts. Mark Zandi, Moody’s chief economist, estimates this will shave nearly a half percent off US GDP.

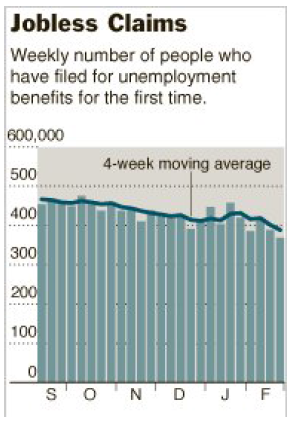

5. Today’s closely scrutinized jobs report revealed that the unemployment rate fell once again to 8.9%. In a similar vein, jobless claims slid even further below the critical 400,000 per month level to 368,000. Additionally, the percentage of industries showing job gains was the highest since 1988.

You say you want a revolution. Few would confuse the professorial Ben Bernanke with firebrands like Che Guevara, Ayatollah Khomeini, or even the much more subdued Lech Walesa. But it could be that our own Federal Reserve chairman has done more to bring about serial regime change in numerous thug-ocracies than any other influence, including Facebook.

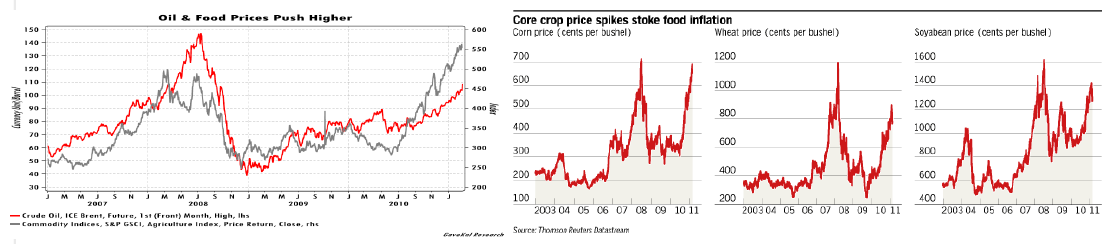

If this sounds a tad outlandish, consider that soaring food prices have been behind much of the unrest that has swept through northern Africa and the Mideast. The World Bank’s index of food prices is up 29% over the last year, with wheat alone soaring 95% in the last eight months, causing an estimated 44 million people in the emerging world to fall into extreme poverty.

Certainly, horribly repressive government policies in those countries have been breeding discontent for years. Yet, the reality is that for decades the oppressed citizenry of these countries has remained largely quiescent.

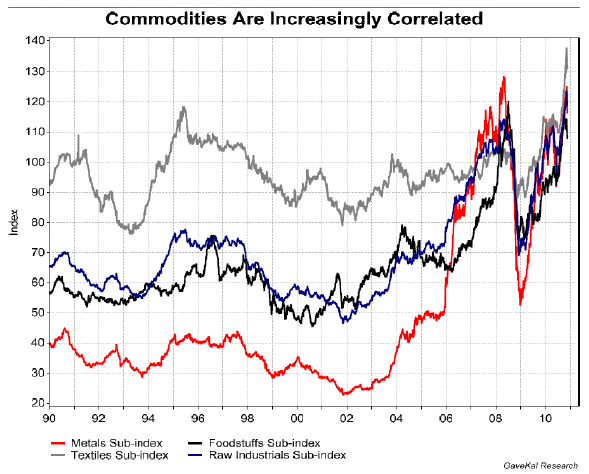

There are numerous factors pushing up food prices right now, but it seems to me that their latest vertical move eerily coincided with the Fed’s telegraphing of its impending second round of quantitative easing (QEII) back in September. As the charts below illustrate, oil and agricultural prices were already stirring last summer but the big liftoff came in the fall, just as markets were beginning to appreciate the implications of QEII. It would be unfair to pin all the blame on the Fed for the parabolic move in most things agricultural. Undoubtedly, diverting 36% of our domestic corn production into ethanol isn’t helping matters. And there is no doubt that emerging market consumers are shifting their diets, leading to more demand for proteins like beef, pork, and chicken, lifting their prices and elevating pressures on feed-grain supplies. But neither corn diversions into ethanol nor emerging market dietary trends are new developments.

Moreover, inflationary pressures are evident in areas beyond the “ag” complex. Overall producer prices in the US have also been on an upward march over the last six months or so. In fact, almost all commodities have been heading north at a furious pace since QEII was advertised by Mr. Bernanke last September. As the perceptive folks at GaveKal Research have pointed out, this does call into question how likely it is that nearly every corner of the commodity world could be experiencing shortages at the same time.

But how much of all this is really the Fed’s doing?

How soon they forget. For those of you who are still wondering what Bernanke and Company’s easy money policy has to do with the trends mentioned above, let me take you back to the summer of 2008. In those days, as you can see from the preceding charts, commodity prices were also in the throes of an amazing ascent. This is despite the fact that recession evidence was mounting in leading countries like the US. It was also becoming clear that the popping of the global real estate bubble had the potential to aggravate any downturn as well as to be highly deflationary.

From our perspective, covered in numerous EVAs at the time, we felt that many on Wall Street were oblivious to this emerging reality in their nearly fanatical embrace of both commodities and emerging markets. The groupthink, with which we took considerable issue, was that both of these asset classes would prosper even as the US slipped deeper into crisis.

But, as is also illustrated above, commodity prices confounded their fans by instead plunging at a horrible rate. Emerging stock markets fared little better, falling by two-thirds from peak to trough. These twin implosions rendered laughable the then-popular notion known as “decoupling.”

Now here’s the parallel with today: A key driver of the lust for commodities and emerging markets back in the summer of 2008 was the sense that the Fed would have to continue to ease. The assumption was that this would lead to further weakness in the US dollar, which had already been pounded as money fled into perceived beneficiaries of dimming American prospects.

While the first part of this turned out to be true, as the Fed was forced to frenetically cut interest rates, once the crisis hit the fever-pitch stage the second half of this calculus went totally awry. Instead of weakening, the dollar erupted. Rather than being impervious to US (and European) ills, emerging markets and commodities were decimated as fears of a global recession went viral.

Despite this severe drubbing in the relatively recent past, there has been a surprisingly swift return to the precrisis mentality. This is even more remarkable given the precipitous decline commodities experienced last spring. It’s hard to believe that the “flash crash” occurred less than a year ago and it was a symptom of a worldwide flight from risk following a rather minor shift in the Fed’s monetary policy. (Mr. Bernanke had stated that the Fed was allowing its already massive hoard of government securities bought with printed money—i.e., QE I―to begin to run off as some of these issues matured.)

The plunge in risk assets that started in May of last year along with the “double dip” economic scare were the main catalysts behind QEII. Ironically, the avowed goal of the Fed’s latest easing move was to lower interest rates. In reality, the polar opposite occurred as intermediate- and long-term yields jumped significantly. For commodity prices, however, the results were radically different. Better economic news, unlikely a function of the Fed’s actions because of how rapidly the data improved, in conjunction with QEII produced another boom. The idea was, and still seems to be, that with the Fed printing more money on a daily basis the coast is completely clear for another commodity run. The fact that global economic growth is accelerating rather than contracting, as in 2008, is frosting on the cake. Therefore, the Fed has, unwittingly or not, created an environment that has caused commodities to do another moon shot.

Unlike in 2008, though, US stocks have been rising right along with commodities. Mr. Bernanke has publicly expressed considerable satisfaction with the stock market’s positive response to his most recent extreme pumppriming efforts. Conveniently, he has ignored or played down the unintended consequences of this latest commodity spike, including the fact that the increase in oil prices alone since Labor Day is siphoning off $80 billion of disposable household income.

Overseas, however, the Fed’s policies are turning out to be much less than a mixed blessing.

Bonfire of the manipulators? Some 40 years ago, during one of the greenback’s many bouts of weakness, then Treasury Secretary John Connelly responded to complaining European officials by harrumphing that, “the dollar is our currency but it’s your problem.” These days, this could be updated to: “QEII is our monetary policy but it’s still your problem.”

And instead of being a headache for Europe, the Fed’s current policies are bedeviling the developing world. As in 2008, institutional money is flooding into the comparatively small commodity markets, for the reasons mentioned above, greatly exacerbating price increases. Because emerging economies tend to be bigger consumers of raw material, China being the most graphic example, this has an immediate impact on inflation.

Food in particular gobbles up a larger wallet share in the former Third World (I guess it’s been promoted to Second World status as I never hear that term anymore). In China, for example, CPI increases are running uncomfortably high at 5% but the food component is much worse, leaping at a 10% annualized clip.

Double-digit food inflation may be one reason that Chinese authorities are reportedly on high alert over possible unrest among China’s populace. It’s also not just a Chinese phenomenon as surging food costs pose serious challenges to price stability and domestic tranquility around the world. Overall prices are inflating at a 10% rate in the world’s second most populous country, India, with food inflation even higher.

Energy expenditures also represent a much larger percentage of GDP in emerging countries--13% versus just 6% in developed nations. Consequently, high oil prices are also much more painful for the aspiring world.

Consequently, numerous overseas authorities are criticizing the Fed for stoking the inflationary flames. In fact, it’s probably fair to say that Ben Bernanke is now about as popular among foreign central banks as Charlie Sheen is with CBS.

But the fact of the matter is that the Fed is not the only central bank that has contributed to the commodity frenzy. Many emerging countries have sought to tie their currencies, either directly or indirectly, to the US dollar and, hence, our monetary policy. China is, of course, the poster child for this manipulation. (Furthermore, it has been a huge factor in the commodity boom by being the major buyer of most key resources due to its own enormous stimulus programs.)

Much as it is illogical to have the same monetary policy in Germany as in Portugal, it’s equally irrational for the US and China to do likewise. The latter is experiencing boom conditions with an increasingly tight labor market, obviously very different than our circumstances.

Once again, this is far more than a China-only condition. JP Morgan believes that official interest rates in the emerging world are, after subtracting inflation, in negative territory. Combined with rapid economic growth, this is a potent combination to drive prices up even further. It also causes me to believe that much more tightening is up ahead.

This in turn leads me to reiterate a point I made at our annual Outlook event in January. Specifically, it has been my experience that whenever rising interest rates meet rising commodity prices, the rates eventually win.

If I’m right, this has significant implications for the financial markets.

A very different sequence. In days gone by, tightening cycles in monetary policy were led by either the Fed or the Bundesbank (now the ECB), or both. Thus, the Fed would begin raising interest rates and the rest of the world, especially those emerging markets seeking to peg to the dollar, would move in lockstep. If they didn’t, they could see a run on their currency―which has happened to numerous countries in the past.

As has been pointed out by various folks more in the know than moi (I realize that’s not saying much), this is the first tightening cycle being led by the developing world. Consequently, unlike in 2008, emerging stock markets and commodities are the asset classes that have decoupled. Tighter money, and the prospects of much more of the same, has cut the legs out from under the bull market in emerging market stocks.

This is a big and unpleasant surprise to the investment community yet again. As recently as December, 75% of professional money managers were bullish on the outlook for emerging markets (as is often the case, Evergreen was in the minority).

While they slightly outperformed the S&P 500 last year, this was only due to an extraordinary performance by some of the most obscure and riskiest markets. The marquee countries, like China and Brazil, collectively disappointed (India did well in 2010 but it has tumbled 10% this year). Thus far in 2011, the average emerging market stock fund is down 6% versus a 5% rise in US shares.

Notwithstanding this underperformance, the institutional love affair with emerging markets still seems to be on, with just a touch of apprehension (retail investors, on the other hand, have lately been heading for the exits).

When it comes to commodities, however, there is no uncertainty; they continue to be viewed as the ultimate beneficiary of the Fed’s ongoing munificence. In fact, the nearly religious zeal of commodity bulls is strikingly reminiscent of the fervor for emerging markets prior to their rollover.

But, in my opinion, investors in this realm should be afraid, if not very afraid.

Dangerous addiction. There is an old saying on Wall Street (probably home to more jingles than even Madison Avenue) that goes: “Three steps and a stumble.” This refers to the time-honored tendency for the Fed to raise rates three times after which the stock market does a face plant.

Interestingly, China has just raised its official rate for the third time even though its market was already flirting with actual bear market territory (meaning a 20% decline). As noted in past EVAs, the Chinese market has been the pilot ship for other stock markets, including the US, over the past few years.

It has also been a leading indicator of eventual trouble in the commodity complex. One would think this should cause some concern, but so far it is apparently being overlooked, at least judging by the continuing ebullient prices. The belief seems to be that as long as the Fed is ultra easy, the good times will continue to roll.

However, with US economic data making it harder for the Fed to run its printing presses 24/7 and a scheduled termination of QEII in June, the clock is nearing midnight. Additionally, obvious and unusual dissension at the Fed has been revealed over this program; therefore, the probability of a third round of “large-scale asset purchases,” as our central bank likes to call it, is about the same as John Boehner keeping a dry eye during a speech.

Consequently, we will soon be dealing with a situation where emerging central banks are yanking liquidity out of the system at

the same time that the stimulant the markets most rely on (QEII) is removed. Call me naïve, but I don’t think that’s a great recipe

for further commodity price appreciation.

Those who would disagree, and they are legion right now, might also consider the long-term performance of commodities. From about the time I arrived on this tumultuous sphere in the mid-1950s, commodity prices in aggregate have fallen 75% in real, or inflation-adjusted, terms despite their recent spike.

By contrast, over approximately this same period, the S&P 500 (with dividends reinvested) has increased by a factor of roughly 50 even after inflation is considered. When commodities are priced far above production costs, as most are today, their future returns look particularly unpromising. After all, they don’t call them commodities because they are scarce.

Yes, I realize that abundant liquidity around the world and high demand from countries like China have been powerful underpinnings of this latest commodity boom (dare I say bubble?). But both of those props may be eroding, particularly if China succeeds in cooling its growth rate as it appears intent on doing. US stocks will not be invulnerable to the changing liquidity backdrop. They have been big beneficiaries of the Fed’s efforts and are likely to have trouble staying at current levels once QEII ends, much less begins to be unwound. It continues to be my belief that the Fed will contract its nearly $2 trillion of government securities before raising the overnight lending rate.

With bearish sentiment on the dollar running extremely high, the developing world in full-blown anti-inflation mode, high commodity prices draining global consumer purchasing power, fiscal tightening in many leading countries (even in the US at the state and local level), and unresolved dysfunction in Europe, there is a distinct possibility of something snapping. When it does, get ready for today’s darlings to be tomorrow’s dogs.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.