"Who will buy treasuries when the Fed doesn't? Yields may have to go higher, maybe even much higher to attract buying interest."

-Pimco's BILL GROSS

POINTS TO PONDER

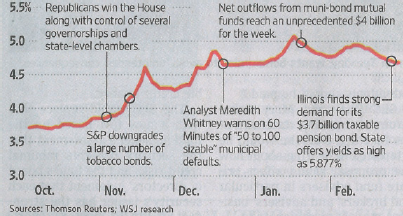

1. Thanks to intense media attention on the fiscal woes of some municipalities, retail investors began withdrawing in droves from tax-free bond funds late last year. This exodus hit a crescendo in January as rates on long-term AAA-rated munis briefly rose above 5%. Since then, prices have rallied and yields have fallen sharply.

2. Bond titan Bill Gross has revealed that Pimco recently sold all of its US Treasury holdings, noting that yields on the 10-year note may hit 4% by June when the Fed’s second iteration of quantitative easing (QE II) ends. However, showing treasuries retain safety appeal, their prices rose, lowering yields, during Thursday’s stock market selloff.

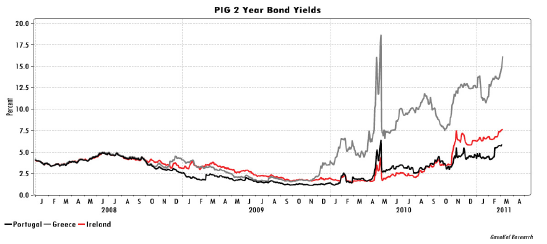

3. The uprisings in Mid-East, and now Japan’s devastating quake, have pushed Europe’s financial crisis out of the spotlight. However, Sean Egan, CEO of independent bond rating agency Egan-Jones, pointed out on CNBC this week that Ireland has $300 billion of outstanding liabilities bearing interest at 8%, or $24 billion. Its total tax revenue is just $20 billion.

4. European banking regulators appear poised once again to undermine their credibility by rubber-stamping another less than stressful “stress test” of their financial institutions. This is despite persistently high and rising bond yields on government debt in several peripheral countries depressing prices and implying huge losses for Continental banks.

5. Downgrades continue to afflict sovereign debt globally, with Greece cut to deep junk status. More ominously, critically important Spain also had its rating slashed yesterday. On the other side of the world, Moody’s downgraded Japan’s AA minus credit outlook to negative. Six Japanese companies now have a higher credit rating than their government.

6. Illustrating why surging agricultural costs are so inflationary in emerging countries, food expenditures amount to 30% of consumer spending in Brazil and China, and 47% in India.

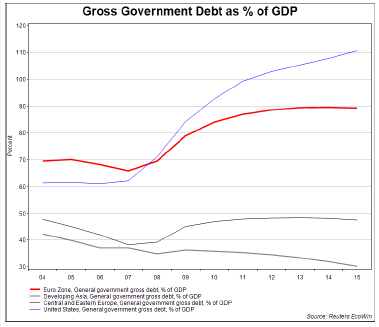

7. Even as governments in the developed world wrestle with unprecedented debt levels, the emerging nations continue to boast low-leverage balance sheets, with developing Asia actually shrinking its liabilities as a percentage of GDP.

8. The US media has been riveted on the confrontation with public workers’ unions in Wisconsin. However, in far more populous and industrialized Ohio, dramatic compensation and unionization reform looks nearly certain to be signed into law.

9. Since 1965, US entitlements have expanded 11 fold versus just a 2.7 increase in GDP (in real terms). Notably, there is an 82% correlation between swelling entitlement outlays and declining personal savings.

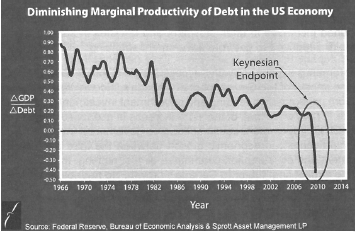

10. Among the many reasons why Western societies should be renouncing their debt-fueled economic models is the fact that additional, or marginal, leverage is producing little, if any, growth benefit.

11. Past EVAs have observed that US stocks were poised for a correction. Another potential catalyst for a retracement is that insiders are shedding their own shares at a record rate.

12. Another theme from earlier EVAs has been the richness of smaller companies relative to the blue chips. Similarly, shares in midsize (midcap) firms are trading at 22 times their past year earnings, close to their peak of the last decade, while the largest enterprises are trading at a trailing P/E ratio of 16, near 20-year lows.

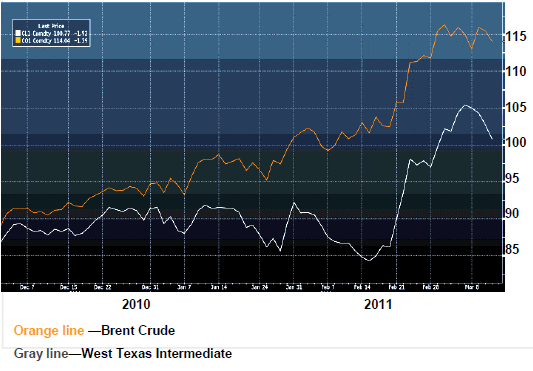

13. In recent months, an unprecedented gap has opened up between Brent crude oil, traded and delivered in Europe, and the US-based West Texas Intermediate (WTI). Brent crude has soared to $115 per barrel and, unfortunately for US drivers, pump prices are based on this benchmark. The lag by WTI is due to a surplus of oil in North America.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.