“You can check out anytime you like, but you can never leave.”

–THE EAGLES, from Hotel California

“Outrageously easy monetary policies (has) become the Hotel California of central banking. By encouraging consumers, corporations, and governments to take on excess debt, policymakers were painting themselves into a corner from which normalizing policy would be impossible.”

–LOUIS GAVE, co-founder of Gavekal Research

“Disparity in wealth, especially when accompanied by disparity in values, leads to increasing conflict and, in the government, that manifests itself in the form of populism of the left and populism of the right.”

–RAY DALIO, hedge fund titan and billionaire

“Bernie Sanders could win this time.”

–Longtime GOP strategist KARL ROVE

Say what? It’s my suspicion that many, if not most, EVA readers have heard the term secular stagnation without quite fathoming what it means. It could be that the comprehension problem lies in that highfalutin word “secular”.

Intellectual folks, like former Treasury Secretary Lawrence Summers, probably use it in front of stagnation because it sounds more impressive and scholarly than merely saying something plain-spoken like “long-term”. In fact, to those of you who grew up in faith-based schools, “secular” meant the opposite of “clerical” or “religious”. Ironically, that last word might have special applicability to this week’s Guest EVA which is on a subject that has attained a level of fervency usually associated with religious beliefs. That would be, for those who have missed the last two EVAs, the increasingly famous Modern Monetary Theory, or MMT.

As promised, this EVA is dedicated to presenting the most credible endorsement I’ve come across so far of this economic theory that has so rapidly come to dominate the discourse among policymakers and financial pundits. For years, I’ve read with great appreciation the work of Gerard Minack in his Down Under Daily. Since almost everything these days is converted into an acronym—including, of course, Modern Monetary Theory—a cynic might be tempted to abbreviate Gerard’s weekly missive as DUD. But I can guarantee you that would be a most inaccurate initialization.

Thus, it was with some degree of surprise that I read his February 23rd edition titled: “MMT Can Kill Secular Stagnation”. My bemusement wasn’t due to the confident opinion expressed by the title. In actuality, I agree with it--at least on a medium-term (I guess that would be semi-secular) basis. Rather, what caught me off-guard was the relaxed attitude by Gerard to what I view as an economic model that is highly likely to ultimately severely destabilize America’s economy and currency.

But I’m getting ahead of myself once again. The first order of business is to agree or disagree with the contention that the developed world, and possibly China, are in reality bogged down in secular long-term stagnation. As you will read, Gerard doesn’t spend much time on this aspect, implicitly treating it as a given. Frankly, I think he’s right but a lot of people, especially the legions of stock market perma-bulls, would disagree. After all, it’s inconvenient to argue that stocks will continue to appreciate at double-digit rates, as they’ve done seemingly forever, during an era of chronic economic underperformance that shows no signs of ending.

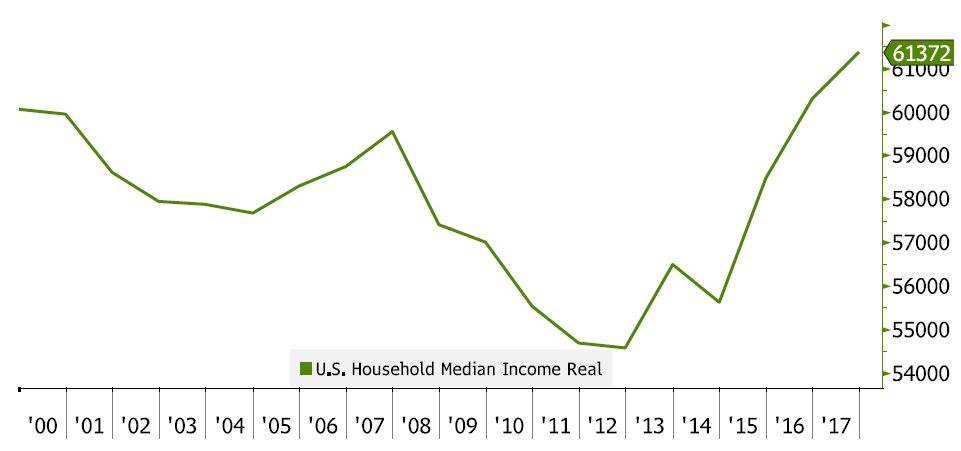

As these pages have repeatedly noted--and in doing so have merely been restating a fact--this expansion has been the weakest of the post-WWII era. Moreover, it is taking ever larger amounts of debt to generate even the meager 2% growth seen for the last decade (down from 3% to 4% in the 1980s, 1990s and the pre-crisis 2000s). Perhaps the worst aspect for the typical American is that inflation-adjusted median household income has flat-lined over the last 20 years, rising a pathetic 0.12% per year.

And to really rub salt in the wounds of Joe and Jane Sixpack, wealth in our country is the most concentrated it has been since 1929. Maybe that’s a key reason that, according to RealClearPolitics, 56.4% of Americans feel the country is on the wrong track.

Gerard’s main reference to this quagmire and the related rising societal dissatisfaction is as follows: “Secular stagnation is caused by a growing gap between the private sector’s desired saving and investment. For 30 years the main policy response to this growing gap has been to reduce interest rates.” In other words, the private sector has been saving too much and investing too little (though, in my view, the saving part is a bit hard to swallow, at least in America, but there’s not much doubt about the under-investment assertion).

Further in his view, as with most who support at least some of MMT’s core principles, the US government has been far too parsimonious when it has come to deficit spending. To this line of thinking, an over-reliance on free money (i.e., from central banks like the Fed) and an under-reliance on fiscal profligacy (also, i.e., via governments running massive deficits) has led to the stuck-in-the-mud global economy.

In my mind, though, the proof-positive that long-term economic stagnation is real is the ascendance of populist and, even, socialist politicians. You may have read that the Democratic party bosses are expressing growing alarm that Bernie Sanders will win their party’s nomination in 2020. And as the last two “Bubble 3.0” EVAs on MMT noted, Mr. Sanders is a big fan of this theory. That’s no shocker but the fact that a lengthening list of mainstream thinkers, like Gerard, are writing words such as this definitely is: “One reason this (MMT) may be attractive is that it is increasingly clear that monetary policy is exhausted, at least in the developed economies.” Since the conclusion that wildly imprudent highly questionable central bank policies have hit the wall was one of my main points in “Bubble 3.0, No Way Out” EVA, he’ll get no argument from me on that score. Basically, monetary remedies wouldn’t be looking hapless and helpless if most economies around the world weren’t sucking wind.

Consequently, as I’ve previously written and Gerard is also contending, the time is ripe for MMT. Call me pig-headed, old-fashioned, and an MMT kill-joy but I'm personally convinced giving US politicians the ability to spend whatever they want until it becomes clear that inflation is out of control will lead to horrific secular long-term problems. This is not to say it can’t create a fleeting boom, but it’s almost certain to be of the inflationary variety as money printing goes from stealth-mode (QEs) into hyper-drive (MMT). What I’m trying to say, probably awkwardly, is that while I have little doubt MMT will end secular stagnation, I believe this will be a case of the cure being worse than the disease.

As you will soon read, even Gerard feels the investor class – which has benefited so handsomely from the economic sluggishness of the last decade – is likely to find itself with a serious case of nostalgia. Therefore, with fair warning to all similarly pig-headed, old-fashioned and MMT kill-joys, please read on…but for “mature” folks like me, you might want to have your blood pressure meds close at hand.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

MMT CAN KILL SECULAR STAGNATION

By Gerard Minack

The theory behind Modern Monetary Theory (MMT) is both correct and obvious. But a factual theory is a descriptive device that has no policy implications. MMT is controversial because many of its adherents argue that the theory permits aggressive fiscal expansion. Whether or not you agree with that conclusion, I think MMT is likely to be used to justify aggressive and unconventional policies in the next cycle. If MMT were deployed as many MMT advocates suggest then it would bring the curtain down on secular stagnation.

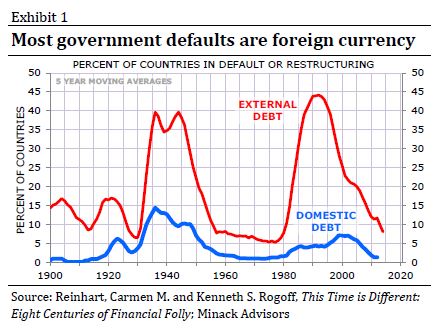

MMT is based on a handful of obvious observations. The first is that a government that issues debt in a currency it controls can always fund itself. Therefore no government that has a printing press need default on debts denominated in that currency. Oddly, some governments have defaulted on their own debt, but most public debt crises have been on foreign-currency debt (Exhibit 1). Governments can also run into strife on debt issued in their local currency if they don’t control the printing presses – as the European euro-periphery and state & local governments in the US have discovered.

A second (obvious) MMT observation is that there are limits to the productive capacity of an economy.

These two observations imply that it is wrong to see government fund raising – either by taxation or debt issuance – as a prerequisite for government spending. The government does not need to tax to fund itself. The principal reason for a government to tax the private sector is to reduce the private sector’s demand. Put another way, taxation doesn’t need to be adjusted to the level of government spending; it needs to be adjusted to balance the productive capacity of the economy and aggregate demand from public and private sectors.

The third observation is that in a closed economy net saving (saving net of investment) is zero – or, put another way, saving by one sector must be matched by dis-saving by other sectors.

This isn’t really a theory; it’s an accounting identity. The world is a closed economy. So if one country saves (runs at external surplus) there must be other countries running external deficits.

Likewise, this implies that if the private sector, in aggregate, wants to save then the public sector must dis-save. Put another way, without the public sector running deficits it would be impossible for the private sector to save.

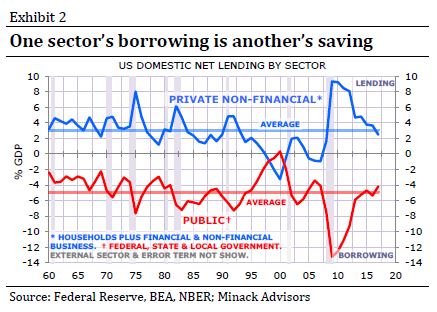

In an open economy, net domestic saving (or dis-saving) is equal to the external surplus (or deficit). In practice, the largest swings within most developed economies are not the internal/external balances adjusting; it’s private and public sector net savings balances adjusting in an offsetting pattern. Exhibit 2 shows how net lending by the private and public sectors in the US tend to be mirror images of each other. The adjustment in the external sector (not shown in the chart) is a second order factor. The only time the US public sector has become a net lender (that is, run a surplus) the private sector was running an unusual – and unsustainable – deficit.

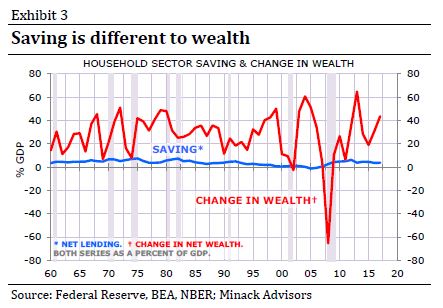

As an aside, it’s worth highlighting the difference between saving and wealth. Saving is a flow. A sector saves if it consumes less than it produces. In the net lending series ‘consume’ includes investment spending as well as consumption spending. Wealth is a stock. While net saving in a closed economy must add to zero, the same is not true of changes in wealth. Historically, changes in wealth are dominated by asset price changes, not the flow of asset purchases or sales. Exhibit 3 compares household net lending in the US and the change in household sector net wealth.

The key observations behind MMT seem to me to be incontrovertible. However, they imply a view of debt and deficits that runs against conventional thinking. But as a theory it is only a descriptive framework without any direct policy implications. The key point now is that MMT is being used as an argument to justify important policy changes.

The key argument – one that goes back to the roots of MMT in Abba Lerner’s idea of ‘functional finance’ – is that the public sector should adjust spending to achieve full employment and price stability. If the result is large and sustained deficits, then so be it.

Put simply, this would see fiscal policy play the role that monetary policy has played for decades. One reason this may be attractive is that it is increasingly clear that monetary policy is exhausted, at least in the developed economies.

If this policy approach were implemented it would be fatal to secular stagnation. Secular stagnation is caused by a growing gap between the private sector’s desired saving and investment. For 30 years the main policy response to this growing gap has been to reduce interest rates. (And that is why it is nonsense to point to average growth rates remaining relatively steady and then claim secular stagnation doesn’t exist. The point is that it has required lower and lower rates to achieve any given growth rate.) Increased public dis-saving is the direct antidote to the private sector’s rising saving.

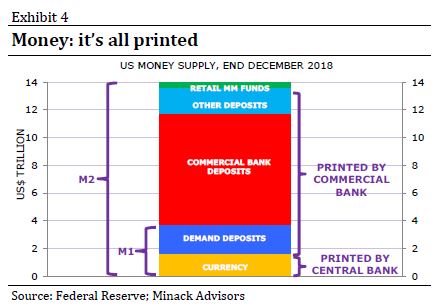

A second argument is that the deficit spending can be financed by money printing, not debt issuance. This causes many people conniptions. However, the fact is we now live with fiat money. Under a fiat system printing is the only way to create money. Historically most of the printing has been done by the commercial banks (Exhibit 4) but there’s no in-principle reason why the government couldn’t increase its share of money printing. In any case, money is a public debt. But – conveniently – it’s debt that pays zero interest and is non-redeemable.

Whether or not you agree with any of the above is not really important. It seems to me that MMT is the perfect theory for the times. It appears to justify a switch from monetary to fiscal policy as the key tool of macro management. It also appears to justify a shift to fiscal expansion after fiscal austerity. And, more aggressively, it can also be used to fund popular policies after years of plutocrats’ policies. Most important for investors, if there is a broad-based adoption of MMT in the next downturn it will end the secular stagnation era. Secularly stagnating was great for investors, a MMT era probably not so.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.