“Speculators often prosper through ignorance; it is a cliché that in a roaring bull market knowledge is superfluous and experience is a handicap. But the typical experience of the speculator is one of temporary profit and ultimate loss.”

-BEN GRAHAM, the father of security analysis

POINTS TO PONDER

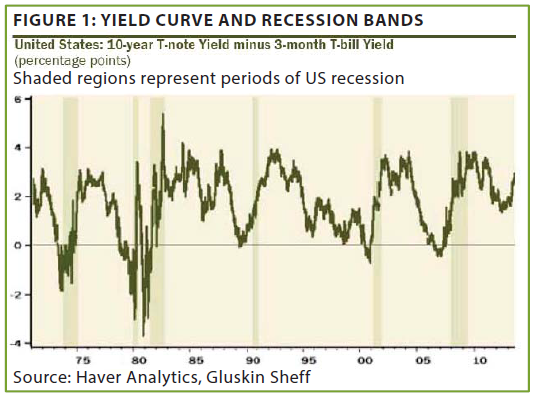

1. Based on the fact that the US has never entered a recession without short-term interest rates above long-term rates (i.e., an inverted yield curve), a new US downturn seems improbable in the near future. (See Figure 1)

2. Despite continually abysmal representation by US politicians and policymakers, corporate America has made a huge comeback. In 2009, only 3 US companies were among the 10 largest in the world. Today, 9 out of 10 are US-based.

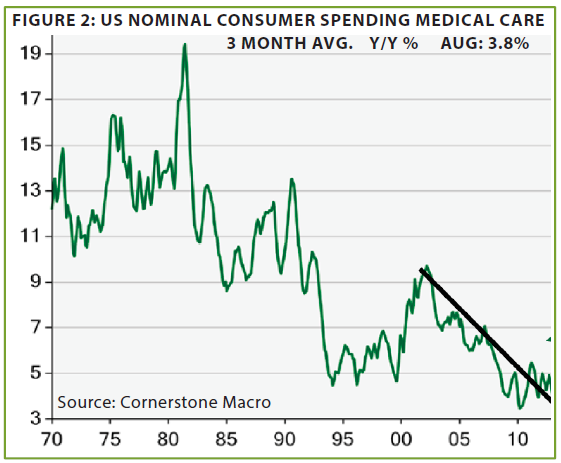

3. Rapidly slowing medical costs, at least partially due to consumers having increased incentives to minimize expenditures, could be a significant dampening influence on inflation, particularly given what a large share of the economy is now healthcare-related. (See Figure 2)

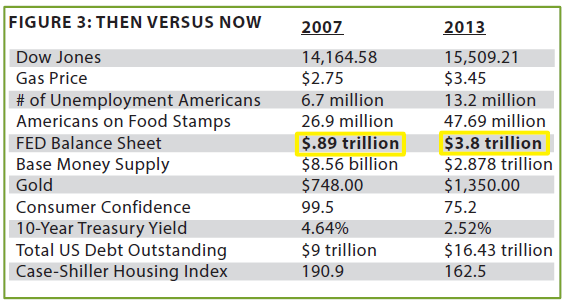

4. US stocks have recently made new highs, but the disconnect between economic fundamentals and the ebullience of the equity market is striking. A key reason for the disparity is almost certainly the $3 trillion the Fed has printed into existence. (See Figure 3)

5. In another example that the less fortunate are not benefitting from this recovery, according to Investors’ Business Daily , low-wage workers have seen their employed hours shrink to near recession lows.

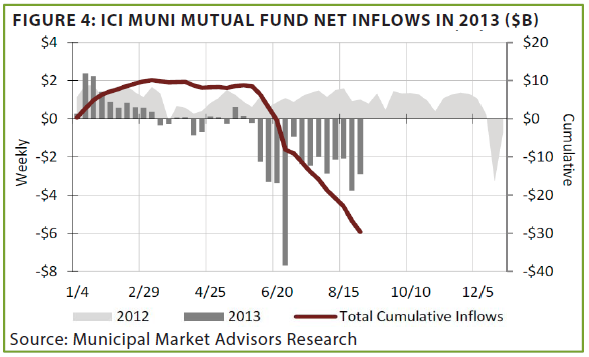

6. Municipal bond investors continue to vote with their fleeing feet. This creates an “interesting” yield opportunity for those willing to assume some interest rate risk in return for taxable-equivalent yields at, or even above, junk bond levels. (See Figure 4)

7. When even professional investors become exceedingly bullish or bearish, markets usually move against them. Thus, independent-thinking investors may want to note the recent Barron’s “Big Money” poll, revealing 89% of surveyed institutions are bullish on blue chip stocks and 92% are bearish on bonds.

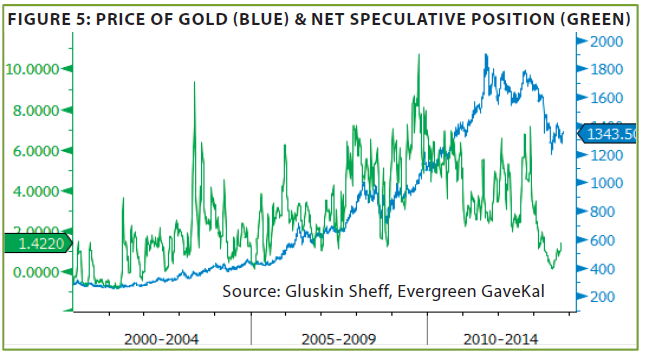

8. Once again showing it pays to be a contrarian in the face of extreme sentiment, gold has staged an impressive rally in the wake of ferociously bearish speculative positioning earlier this year. Bullion prices are now up 10% from their June trough when sentiment was particularly negative. (See Figure 5)

9. Further indicating pervasive stock market bullishness, hedge fund short positions are at record lows in the US and Europe. Yet, insider selling is running at 4 sells for every buy, versus the normal ratio between 2:1 and 2.5: 1. Meanwhile, retail investors are pouring tens of billions into stock funds.

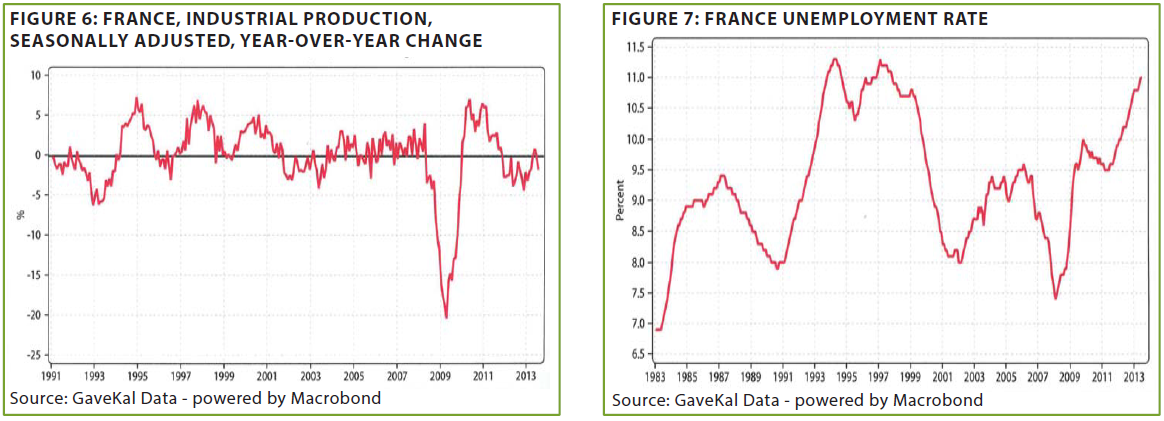

10. Even as Europe has begun to haltingly climb out of its deep economic hole, France continues to struggle. (See Figures 6 & 7)

11. Many experts are sticking with the assertion that global growth is accelerating but consumer product giants Unilever and McDonald’s disagree with that view. Unilever’s CEO said last week that “the global economy is not in as good a shape as some people would like to make it out.” McDonald’s chief executive similarly noted he expected the fourth quarter to bring a continuation of “tight macroeconomic and competitive pressures.”

12. It is not hyperbole to say that Brazil’s offshore oil reserves have immense potential. Yet, once again, the heavy hand of the state is fumbling the chance to develop an exceptional resource, similar to what has occurred in Russia, Mexico, and Venezuela. Brazil’s government has also treated its energy behemoth, PetroBras, like a government agency, trashing its stock price and inhibiting its ability to invest for the future.

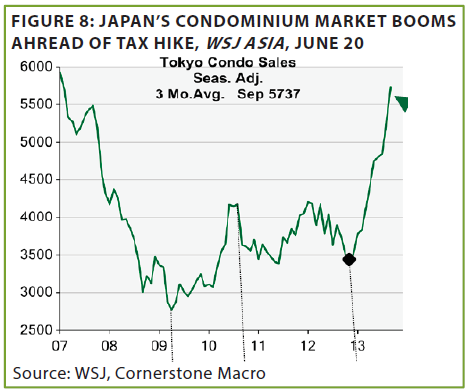

13. The Japanese real estate market, after years of stagnation, is ripping. However, much of the buying appears to be motivated to get in front of a looming 5% tax. (See Figure 8)

14. Despite rampant over-building in certain markets, a slowing economy, and very poor affordability, China’s housing market has avoided a Western-like crash. Perhaps it is due to the fact that 70% of all Chinese homes are bought with cash (versus 40% in the US). For financed purchases, 30% down payments are required, with 70% down necessary for second-home buys.

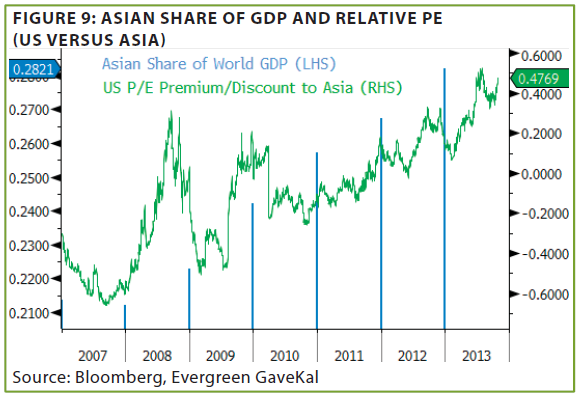

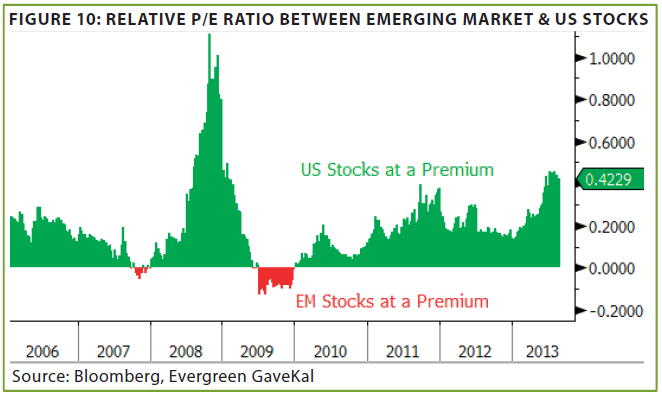

15. Over the last six years, Asia’s share of global GDP has risen from 21 ½% to 28%. Yet, in the same timeframe, Asian stocks have tumbled from a 40% premium versus US stocks to nearly a 50% discount. (See Figure 9)

You talkin’ to me? Robert De Niro’s famous line from Taxi Driver is highly relevant to last week’s EVA, which identified a number of investment biases and flaws to which most of us humans fall victim. One of the more interesting sections of that EVA, in my mind, literally pertained to the mind; specifically, what regions of the brain become engaged when we hear that others are making more money than we are. As many of you read, that would be the cortical areas involved in the experience of pain (click here for the October 25th EVA).

We might wish to believe that we are above such reactions, but I think if we are really being honest, most of us would admit that we at least wrestle with this primal tendency. My conclusion, after more than three decades of real-world observations, is that as long as the conditions causing this “return-envy” don’t persist too long, the majority of investors can tolerate the subliminal discomfort. However, should you have to listen to your least favorite cousin brag about his stock portfolio gains at your family’s 4th of July barbeque, and he’s still running off at the mouth about them at the New Year’s Eve party, your pain threshold may suddenly be exceeded.

Academics who believe in the cold rationality of market participants, like the recent co-winner of the Nobel Prize in economics, Dr. Eugene Fama, have traditionally paid little heed to the recurring tendency of rising markets—be they stocks, commodities, art, or condos—to literally go vertical at times. These straight-up phases typically don’t happen until the tail-end of an exceedingly powerful and long-lasting up-move. Yet, based on the efficient market theory as espoused by Dr. Fama and many other brainiacs, ballistic surges really shouldn’t happen at all. This is because there should be some rational seller always ready to pounce on an

over-exuberant buyer, thereby preventing prices from entering into the bubblesphere.

However, as Tyler noted last week, the man who co-shared the prize with Dr. Fama was Robert Shiller. Dr. Shiller is convinced of human fallibility and the inability of rational market participants to counterbalance the thundering (blundering?) herd of millions of pain-wracked investors when they are collectively crying “Uncle!”; in other words, when they just can’t stand to see others making seemingly easy money. And to take this logic one step further, it’s my belief that the offspring of the efficient market theorists—the index fund—plays a big role in the increasingly frequent “hockey stick” moves, followed by sickening plunges, we’ve seen over the last 15 years in various asset classes.

Turning lemonade into a lemon. Prior to the 1990s, index funds were a fast-growing but still relatively small force in the financial markets. Since that time, and particularly with the breathtaking proliferation of ETFs (which are generally index-type vehicles), funds that merely seek to mimic a particular benchmark have come to dominate markets to an ever-greater degree. This is especially the case when the countless vehicles that stealthily seek to replicate the returns of a benchmark—that is, the closet indexers—are included.

Initially, there was a lot to like about index funds, especially their low cost and their avoidance of underperformance. But, as I wrote several years ago, once a benchmark is investable and huge sums of money begin to treat it as an actual asset class, funny things happen.

Consider a story I heard at the end of 2009, when the US stock market was still struggling to dig out of its asteroid-like crater after the financial crisis. One of my longtime clients, whose portfolio was up 45% in that huge recovery year, had gone to a holiday party (aka, places where terrible investment advice is given) and was cornered by one of his friends. This individual proceeded to boast about his portfolio being up close to 70%. My client didn’t believe that was possible and he called me to ask if this could be true. I suggested he go back to find out if his friend was heavily invested in emerging markets. Sure enough, the answer came back “Si!”

In the old days, only a handful of mutual funds invested in emerging markets because they were viewed as too illiquid and too volatile for most investors. As a result, they attracted small amounts of capital and traded at a chronic discount to more established markets. Then along came the emerging market ETF…

This vehicle, seeking to track as precisely as possible the benchmark for the developing markets, gave investors the chance to hop into this once-obscure investment niche with the ease of a few mouse clicks in their E-trade account. Because it was now effortless to access developing markets and they had, as is always the case in a hot market, an exciting story to rationalize the

euphoria, the gains fed on themselves.

As more investors jumped in, the emerging market ETF immediately put the money to work. There was no such thing as closing to inflows or sitting on the cash. This chain reaction continued until, as you can see below, emerging markets were trading at a substantial premium to the US, a most unusual development. This happened in both late 2007 and the second half of 2009, after a period of, naturally, extreme outperformance relative to the US.

A fair amount of my time in 2009 and 2010, including in EVAs, was spent explaining to investors why their love affair with emerging markets might not end well. Rather ineffectively, I was also pointing out the undervaluation of the US stock market back then, especially considering its lower risk nature vis a vis the perpetually wild and wooly developing world. But the bullish story of faster growth and an ever higher share of global GDP proved irresistible to many.

Of course, the situation is almost totally inverted today.

Where have all the gatekeepers gone? These days, emerging markets are deep in the penalty box after having underperformed US stocks by 50% since the end of 2010. Meanwhile, even conservative US investors’ cortical pain centers are enflamed as they see the S&P 500 up 25%, not to mention stocks like Netflix rocketing 300% over the last year.

Funds are streaming back into the US market, often into index funds, causing prices to rise even further. At the same time, the flash-traders and other short-term-oriented market players are going with the flow and the “mo” (the flow mo?), particularly since it appears the Fed will keep printing full throttle, at least through year-end (some are even now speculating it won’t taper until October, 2014). So, we’re looking at the classic self-perpetuating cycle, aided and abetted by indexes masquerading as investment vehicles.

By striving to keep up with a benchmark, in this case the S&P 500, investors are driving an overvalued market (using a broad range of reliable long-term indicators) into even more nosebleed territory, reprising what happened in the late 1990s. The increasingly urgent impulse to get in on the action is unfortunately facilitated by the reality that so many investors these days have become solo pilots. In other words, they no longer rely on a trusted advisor but instead are self-advised (possibly because the prior advice, in many cases, wasn’t all that trustworthy).

Consequently, there is no one to caution investors against the extreme mood swings that are the result of violent up and down markets. When markets have been crushed, and bargains abound, the typical retail investor wants nothing to do with them, be they US stocks, corporate bonds, or, as is the case now, gold. And when they are soaring and over-priced, the do-it-yourselfer

can’t get enough of them. For all the flaws of the broker model of yore, at least the more experienced and conscientious financial consultants attempted to play the role of gatekeeper for their clients. (Having attempted to serve as a gatekeeper for my clients over many years, I can assure you it can often be a most thankless job.)

The fact that it is now so easy to trade and access even once-esoteric asset classes compounds the risks of an increasingly gatekeeperless investment world. Ironically, the creator of the first index fund, Jack Bogle, has for years bemoaned this new paradigm where the market itself has been broken down into a plethora of sub-indexes, giving investors many more manias to chase when they are in full-blown bubble mode. As Jim Cramer likes to say, there is always a bull market somewhere. What he fails to mention is that invariably by the time the typical small investor figures out where that is, the bull is about ready to jump out of the pen.

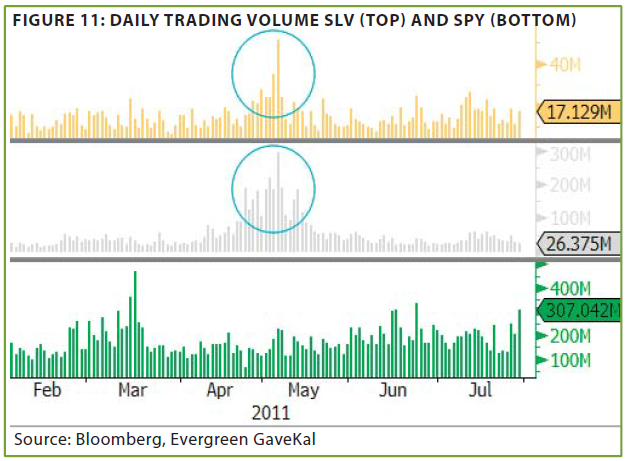

Consider gold: When US stocks were staggering in the summer of 2011, bullion was fast approaching $2,000 an ounce. It was impossible to listen to CNBC without hearing a steady stream of ads on gold’s attractiveness as well as that of its precious metal cousin, silver. In fact, earlier that year, trading in the silver ETF, SLV, exceeded for a time the volume of the S&P 500 itself. Similarly, the gold ETF was also experiencing an explosion in trading activity, indicating just how captivated the investing public was with precious metals at the time.

In the old days, buying silver or gold was a pain. You had to either play the futures market or actually buy the physical stuff, which was cumbersome and costly. But, as with emerging markets, the advent of the ETF made it as easy as buying Microsoft (and without all the bad press). In the absence of a gatekeeper to calm investors down and discuss things like excessive optimism and overvaluation, clients could, and did, madly charge into these various asset class-specific bubbles and mini-bubbles, including commodities, once only the playground of the arch speculator.

At its core, indexing is essentially “no-think” investing. Frankly, in a rising market, thinking is a liability because you start looking at those irritating things like P/Es and price-to-sales ratios, intense insider selling, excessive margin debt, etc. All of these considerations get in the way of simply going with the “flow mo.” It’s so much easier and, at least in the near term, so much more

profitable to simply buy an index ETF in whatever is en fuego, which right now is none other than our once reviled stock market.

Let’s face it: Americans are hard-wired to be performance-driven. In many pursuits, that’s a positive, but when it comes to investing, especially late in a massive rally, it can be an extremely expensive attribute. During times of hyperventilating markets, it is better to be lagging, as hard as that is to stomach, at least if that is a function of preparing for when the pin unceremoniously

meets the bubble. But most investors hate to lag, particularly when the gains have been coming fast and furious. This is a key reason why, as Tyler showed last week, they collectively experience such poor long-term returns.

In the medical field, gatekeepers have long played an essential role. Physicians prevent patients from self-destructive behavior and perform functions of which the typical layperson is totally incapable. Imagine, for example, if patients were able to prescribe their own drugs—it wouldn’t be long before we’d have most of the country hooked on oxycontin! But in the financial world, the

greedy pseudo-gatekeepers, along with many reckless media “experts”, have led millions of investors to believe they are better off going it alone. Of course, the way healthcare is trending these days, the medical gatekeeper might soon be an endangered species as well. And that will be very dangerous indeed.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.