"Asset purchases may act like a sweet poison for the governments. The rude awakening may come when the purchases are reduced or stopped altogether."

- Bundsbank President Jens Weidmann

"We may never know where we are going, but we’d better have a good idea where we are."

–Howard Marks, famed investor

POINTS TO PONDER

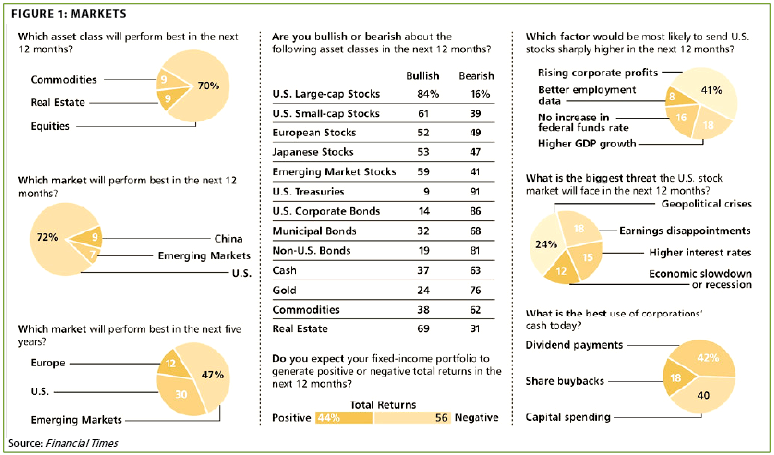

1. Every major Wall Street firm was bullish on stocks and bearish on bonds at the start of 2014. As observed at the time, this was a powerful indication, at least to those who are suspicious of group-think, that bonds were poised to out-perform stocks. Thus far, that is what has happened and, based on the latest Barron’s Big Money poll of institutional investors, this consensus-confounding trend may have legs. (See Figure 1.)

2. A long-standing EVA forecast has been that the Fed would continue to taper until the stock market cracked. Validating that view, even the mild correction seen thus far in US equities has caused two senior Fed officials to either propose "tapering the taper" or launching QE4. It will be very interesting to see how our central bank reacts when a 20% to 30% market reversal occurs.

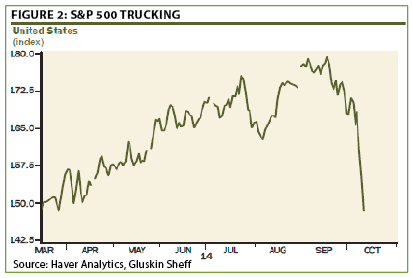

3. In addition to the various indications of a deteriorating backdrop for stocks—such as far more new lows than highs and a breathtaking erosion in the advance/decline ratio—the price action of transportation stocks is ominous. Trucking stocks, which are classically economically sensitive (and are not subject to ebola fears, unlike the airline shares), truly ran off a cliff lately, before bouncing vigorously this week. (See Figure 2.)

4. Beyond the bullish unanimity discussed in Point to Ponder (PTP) 1, professional money managers and strategists feel the odds of a global recession are a mere 8%. Yet, based on the nearly 40% implosion by industrial metal commodities, and numerous sovereign bond markets trading at yields lower than during the Great Depression, this view seems dangerously complacent.

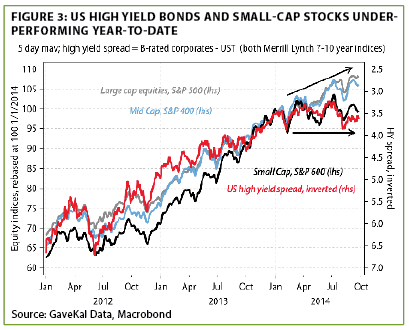

5. Recent EVAs have highlighted the warning signals broadcast by credit spreads expanding materially (which, once again, gave an excellent heads-up for October’s market dislocations). In addition to low-grade bonds struggling, riskier stocks, like small-caps, have also been limping badly. The pressing question is whether they perk up between now and year-end or larger stocks come down to their level. (See Figure 3.)

6. Underscoring the wages of financial engineering versus real engineering, capital expenditures in the US have been in a long decline, especially relative to corporate profits. In fact, until recently, there was never been a four-year period when "capital-deepening" declined. This has serious negative ramifications for productivity growth, a critical factor when overall population increases are slowing.

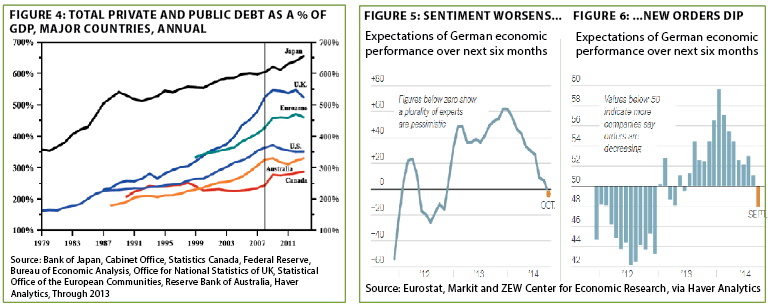

7. Despite the Fed’s creation of nearly $3.5 trillion of synthetic money (technically, reserves injected into the banking system), the Canadian dollar is now at an 11% discount to the greenback. Two knocks on the "Loonie" are that both households and provinces up north are over-leveraged. Yet, when looking at total private and public sector debt as a percentage of the size of leading economies, Canada is clearly in the best shape. (See Figure 4, left.)

8. The German juggernaut, the most robust of Europe’s economies, continues to lose steam. New orders fell in September and future expectations have tumbled to the lowest level since the eurozone’s existential crisis in 2012. (See Figures 5 and 6 above, right.)

9. Emerging market bonds, even those denominated in dollars, are almost certain to come under pressure in the event of another financial crisis and/or flash crash. However, considering that debt markets from developing countries have seen almost two years of outflows—historically, a bullish dynamic—any potential crescendo of panic-driven selling might create an epic buying opportunity. The overall credit rating of emerging bonds has also dramatically improved, up 5 notches from B in 1993 to BBB-minus this year.

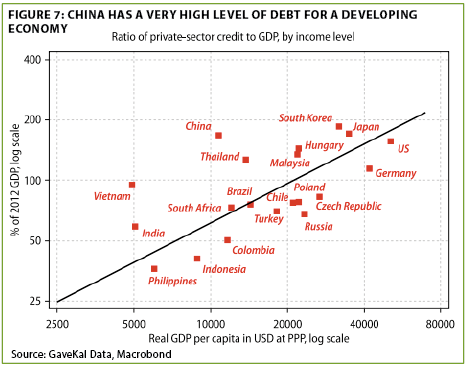

10. One of this author’s overriding concerns is that the planet’s fundamental problem is too much debt combined with too little growth. This toxic combination is not limited to Japan and the west, either. China also is suffering a pronounced economic slowdown and, despite massive foreign currency reserves, its private-sector debt is extremely elevated for a developing country. (See Figure 7.)

THE EVERGREEN EXCHANGE

By Tyler Hay, Jeff Eulberg, and David Hay

Fall in full effect. Market cycles generally go something like this: peak, recession, trough, and then recovery. The seasonality of weather follows a similar pattern. I spent a few falls in Boston during college, and I miss being there this time of year for the fall foliage, crisp nights, and pumpkins dotting doorsteps. Although Halloween is still several days away, last week’s market drop brought home its fears early for equity investors. Prior to last week’s gyrations, markets had slipped to multi-year lows in volatility. To put it bluntly, investors were becoming complacent. This week’s rebound is providing a window of opportunity for investors who have, intentionally or unintentionally, deviated from their target asset allocation to get back in line.

This isn’t the first time we’ve pointed out that the bull market that’s been romping since 2009 has delivered generous returns for those in US equities. Admittedly, we’ve been prematurely warning that equity markets look extended on various metrics.

But, for those of you who want a reason to believe that this bull has room to run, here’s some fodder. On a forward P/E basis, this market doesn’t look that expensive. Meanwhile, the US is still perceived to be the most muscular member among the 80-pound weaklings that make up the dubious club of developed world countries. Also, while this bull market is definitely up-there in years, at over 5 ½, the bull market in the 1990s ran longer. Finally, although the 221% return since March of 2009 is well above the 180% average, it once again pales in comparison to the "Roaring ‘90s" which ended with a 516% total again (but also produced the spectacular "tech wreck").

Basically, upon superficial analysis, we aren’t necessarily in oxygen-mask-required atmospheric zones. But, as Dave has often pointed out, when you normalize for profit margins currently being far above normal, the price-earnings ratio does get into the stratosphere. It’s also a fact that this rocket-ride for stocks began from a much more elevated valuation platform than almost all previous moon-shot markets.

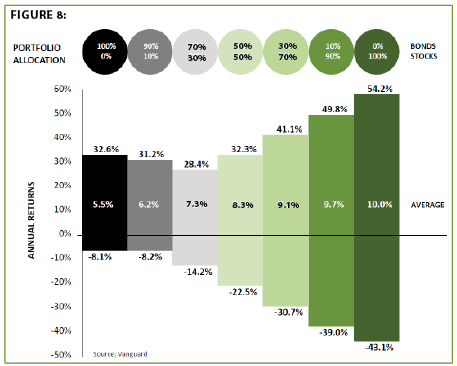

If the shakeout last week caused you to question whether you could handle further pain, don’t let this week’s bounce-back reassure you. Investors are often too focused on their return goals and not enough on their risk tolerance. Said another way, you shouldn’t arrive at your asset allocation target by selecting your desired return level. Instead, you should really approach it from the opposite direction (ask yourself: How much pain can I take?). Last week’s visit from a forgotten foe—volatility—provided investors with a coffee-smelling moment to reassess their risk tolerance. The chart below is helpful for confirming if you’re properly positioned.

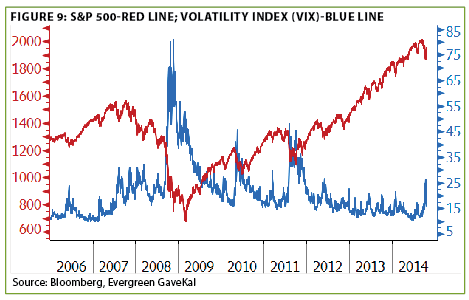

The idea that investors have grown sloppy may seem odd during a time when there is such a high level of social discomfort. So is it true that investors have become complacent in regards to risks facing the market? The chart below shows that, as the market continues to climb, investors have apparently forgotten the lessons learned during the last financial crisis—until this month, that is.

One of the more interesting behavioral phenomenons we’ve observed is that during long market rises, like the one we’ve just had, investors’ projections of future returns rise and their perceptions of risk fall. Late in bear markets, it’s just the inverse. Of course, as any rational market observer realizes, the reality is the exact opposite. This backward-looking and illogical tendency is a big reason the typical investor tends to buy high and sell low, causing their returns to fall way below the market itself.

This leads to another even more important question: Has market performance in recent years caused investors to place too much of their portfolio into equities, leaving themselves overly exposed to a market decline?

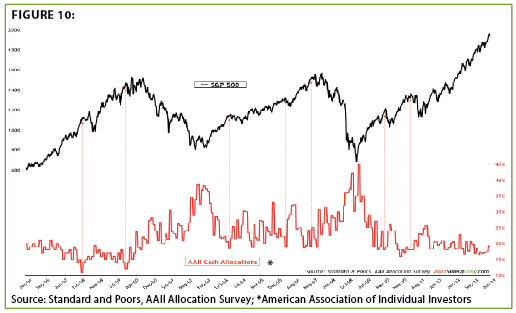

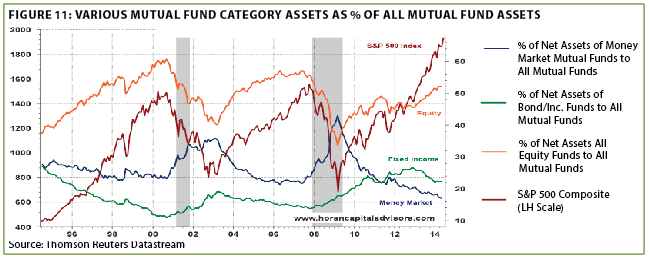

The black line in Figure 10 above shows the surge in the S&P 500 since 2009, while the red line shows a continual erosion of cash allocations within a retail investor’s portfolio. Obviously, investors are becoming dangerously low on cash relative to historic levels. But it’s not just amateur investors who’ve run down their reserves, as professional investors’ behavior looks eerily similar. The chart on the next page shows money market holdings have fallen consistently during this bull market, while stock holdings increased markedly. Both professionals and amateurs are being lulled to sleep as volatility had become almost non-existent prior to the October scare.

As mentioned earlier, both weather and market patterns follow a similar cycle. Warm summer nights are followed by cold and rainy Fall evenings, which turn to blustery winter conditions, which are eventually met by the refreshing air of spring. I don’t think there’s anybody who believes we’ve entered a new investment period where it’s summer year-round. Therefore, the longer this bull market lasts, the more likely we are to see a change in the season. Yet, even a quick analysis of investor behavior doesn’t show preparations being made for a change in weather. Investors who don’t insulate their portfolios for the changing season are likely to get left out in the cold when this Indian summer for stocks finally ends.

Back to the Twilight Euro Zone. As Director of Wealth Management at Evergreen, I meet with many of our prospective clients, and I’m commonly asked, "What does Evergreen see as the biggest threat to the global economy?" As my fellow Investment Team members will attest, my biggest fear is the lack of stability in the European Union (EU). To some, I know I sound like a broken record, but I’ll continue to play this album until the EU is capable of prescribing a viable long-term solution to cure its many ailments.

As noted in previous editions of Evergreen Exchange, EU equity markets have declined since European Central (ECB) Bank chief, Mario Draghi, announced new monetary programs aimed at supporting the struggling EU economy. Back in 2012, Draghi proclaimed he was ready to do whatever is necessary to preserve the EU. Apparently, the market wants Draghi to literally put the ECB’s money where his famous mouth is. However, the market may be forgetting that Draghi only promised more monetary support after the EU agreed to a "fiscal compact." Moreover, he recently said, "My main message today is that only if structural, fiscal, and monetary policies go hand in hand, will the euro area see investment return." In other words, unless Europe’s political elite is prepared to institute radical reforms, don’t expect Draghi to open wide the monetary spigots.

Meanwhile, in Germany (the EU’s largest economy), fiscal reform equates to reduced government expenditures with deficit spending only utilized as a last resort. So much so, the Black Zero, a 2013 campaign promise of German chancellor Angela Merkel, aims towards having a German budget surplus by 2015 for the first time since 1969. Despite pressure from other European countries, this commitment by Merkel and her party is unwavering. At the recent International Monetary Fund (IMF)/World Bank meeting—under intense outside pressure—Germany’s Federal Minister of Finance, Wolfgang Schaueble, said, "You can’t always spend other people’s money in a monetary union… as soon as France and Italy implement substantial structural reforms, the situation in Europe will change." Then, last week, German Economics Minister, Sigmar Gabriel, said, "While boosting European growth is necessary, flash-in-the-pan, short-term stimulus programs are not the answer."

In France (the EU’s second largest economy) and Italy (the EU’s fourth largest economy), however, the current political momentum is actually pushing for increased deficit spending as a way to spark growth. Pushing the envelope of expenditures, France recently proposed its 2015 budget to the EU—one that revealed an increased deficit of 4.4% (exceeding the EU mandated deficit limit of 3%). Despite this immediate growth in the deficit, French Economy Minister Emmanuel Macron, offered to cut spending by €50 billion over the next three years. He also called for an investment by Germany in the same amount to offset the decline in the EU economy. This again puts the German government in a rather uncomfortable position. While they don’t want to support the increased deficit spending, they also fear any sign of diminishing support for the EU could trigger a tailspin in European bond prices, which have recently displayed some weakness.

Major structural reforms, like the kind necessary in France and Italy, will only be successful if proposed by a dynamic leader capable of gaining broad support from constituents. Unfortunately for France and Italy, the next Margaret Thatcher does not appear to be in charge of either country. France’s current President, Francois Hollande, has a 13% approval rating—the lowest of any French president in the last 50 years. Italian president Matteo Renzi, a confident 39-year-old, has a long and arduous fight ahead against the formidable Italian labor unions. As an example of what Renzi is up against, Article 18 of the Italian labor code makes it all but impossible for companies of 15 or more to fire any employee. In contrast to the French and Italian leaders, Merkel has a 79% approval rating and broad support for her policies. Compounding the complexity in the EU, anti-European political parties are gaining steam and increasing pressure on governments to act in the best interest of individual countries—not the EU.

In addition to political wrangling, the IMF has increased the odds of a European recession to greater than a one in three chance. With that being said, most European budgets do not forecast a recession. So, if one does occur, tensions in the EU will likely be amplified. Budget deficits will become much larger, debt ratios will surge, and political unrest will continue to grow, leaving politicians without any workable solution.

Europe is obviously of great importance to the global economy. This is not just because of the sheer size of its collective economy, but also due to the unknown ramifications of unwinding a monetary union on this scale. Today, we have a broad slowdown in the European economy and governments are vastly divided on an effective solution. For European markets to rally from here, Germany would need to compromise and increase government spending, allow higher budget deficits, and support the ECB’s effort to dramatically increase monetary programs. Because Germany has a deep disdain for these economic policies, I find this to be an unlikely scenario. Over the last two years, as optimism grew for a stronger and more united Europe, yields on government bonds sank. If investors start to value these bonds based on individual country fundamentals—as opposed to an ECB supported investment—yields will shoot higher. This sequence of events could potentially deal a deathblow to the European Union. In terms of the global economy, Europe is far from the only concern. But even if the EU is not the catalyst for the next global panic, I fear it may end up accentuating the severity of the eventual decline.

My Not So Darling, Inclement Times. A consensus viewpoint is that until lately the US stock market was a paragon of invincibility. Yet, that’s really not true, as is the case with many widely-held convictions, not the least of which was that 2014 was destined to be another year in the Great Rotation from stocks into bonds.

It’s been largely forgotten now but as far back as January market action was indicating there was a transition to less ebullient conditions. During 2014’s opening month, the S&P 500 fell 3.5%, a striking departure from the past few years, as I noted at the time. There were a few market pundits, besides me, mostly of the technical persuasion (charts, trend-ines, etc.), who warned that as goes January so goes the year overall.

In my case, I opined that the long overdue correction, at least of any magnitude, was unlikely to begin at that point. Rather, I contended the real deal was much more probable come Fall, when stocks might really—ahem—fall. My reasoning came down to what has been, over the last six years or so, the most dominating market force: the Fed.

Because our precious central bank had made it abundantly clear it intended to continue pumping out its seemingly endless performance-enhancing bucks through the end of this month, despite a clearly recovering economy, I felt the most likely time for trouble was in late summer or early Fall. Not long ago—like in the first half of September—that seemed to be just another one of my overly negative views of the US stock market.

The more popular view (there’s that dangerous attitude again) was that since everyone knew that QE3 would end in October, its demise wouldn’t impair stock prices. Superficially, that made a lot of sense—until the conclusions of QE1 and QE2 were considered. Everybody also "knew" when those were going to end, and that didn’t prevent the stock market from doing a skydive immediately thereafter. And, since there was such pervasive equanimity about QE3’s wind down, a rational contrarian should have been on high alert. But let’s face it—being a rational contrarian hasn’t been very rational for the last couple of years, at least when it came to navigating the stock market.

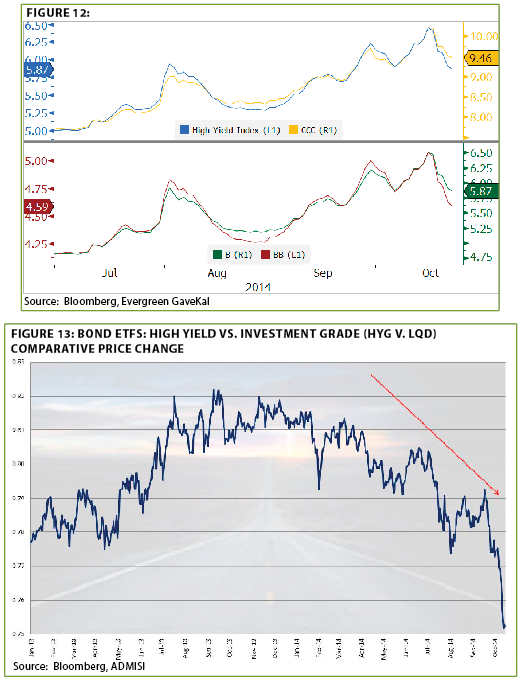

Therefore, it’s now time to trot out that question from January: Is this the start of a serious shakeout? Don’t go into de-fib good reader, but I’m going to answer that in the unequivocal affirmative this time. Actually, I feel like I’m cheating or, perhaps more accurately, stating the obvious. There has already been enough serious damage done, especially to a couple of Evergreen’s long-criticized asset classes, to call this fait accompli. Specifically, both low-grade stocks and bonds have already come under severe pressure as noted in PTP 5.

As you can see below, the carnage in these two areas has been appreciable. CCC bonds, the riskiest of all non-bankrupt bonds, are now yielding over 10% after their yields slipped to under 7% earlier this year. It was when yields fell to that historically skimpy level that we pointed out the worrying reality investors in this space were accepting "return-free risk"—at least, when adjusted for the high levels of defaults these dicey bonds typically incur.

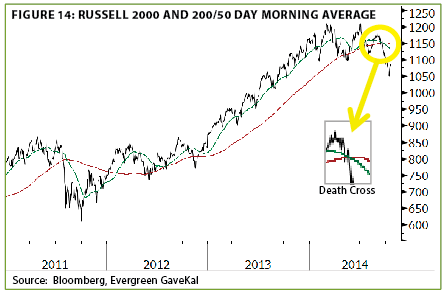

Similarly, small-cap stocks tumbled 15% from their peaks this summer to the low-point on October 15th. In the process, they have executed the infamous "death cross," where the 50-day moving average falls below the 200-day. (See Figure 14.)

Death crosses are certainly not always fatal as sharp rallies often occur after this signal. Yet, based on the broad deterioration across so many asset classes and sub-sectors (such as the trucking stocks per PTP 3), this is likely to be the end of the 14-year outperformance of small-cap over blue chip stocks. They have benefited mightily during the years of reckless risk-acceptance; now, they are likely to be victims of a much warier investor mindset.

Unquestionably, after the severity of the sell-off in so many areas, there will be some powerful snap-back moves. Again, there already have been, with small-caps having rebounded about 6% from last week’s lows, but I believe these are definitely rallies to sell into. Unless the Fed is willing to totally sacrifice what scrawny credibility it has left, QE 3 will end in the next few days.

On that score, the fact that certain Fed-heads, as mentioned in PTP 2, are bringing up QE4 (what we call QE Quatro or QEQ), speaks volumes as to how disingenuous the Fed has become. After all, the economic data remains decent, though not great, and the official jobless rate is below 6%. Even the Fed seems to finally be getting it that a large pool of those unemployed are never coming back into the workforce, at least not without serious entitlement reforms.

Therefore, the only justification to bring up QEQ is to continue the Fed’s Great Levitation of asset prices, especially the stock market. Yet, even as feckless as this Fed is, I don’t believe they will do QEQ unless stocks fall at least 20%, if not more. The recent bounce by the market makes it even more probable QE3 goes the way of all flesh.

Of course, I could be wrong and maybe everything we’ve seen lately is just a little indigestion. But I doubt it. Foreign stocks, currencies, commodities, and bond markets are all screaming that we have a severe shortage of growth (and, sadly, just as severe an excess of debt). The realization also seems to be setting in that the Era of the All-Powerful Central Banks is fast approaching its sell-by date.

If nothing else, the events since mid-September should make us aware of how rapidly the market’s atmospherics can switch from benign to inclement, which reminds me of an old sorrowful song…

Oh, my Darling, oh my Darling,

Oh my, Darling Inclement Times.

Thought you lost and gone forever,

but history—she sure rhymes,

‘cause the taper, caused a vapor

and the markets did decline.

Rather badly, so we sadly

Welcome back, Inclement Times!

![]()

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.