"It is impossible to produce a superior performance unless you do something different from the majority."

- Sir John Templeton, founder of the Templeton mutual fund family (now Franklin Funds)

"In recent years, holding cash is so completely out of favor that it has become the ultimate contrarian investment."

– Seth Klarman, one of today’s most celebrated investors

Return Sequencing. Unquestionably, delving into a topic known as the "sequence of investment returns" isn’t as pulse-quickening or glamorous as, say, gene-sequencing, but for millions of boomers it might be more important. In fact, with valuations across so many asset classes as stretched as the truth in a political speech, I would argue understanding the concept of return sequencing is vital for Americans who have either just retired or are nearing "the golden years." (Thanks to the Fed’s relentless attack on livable interest rates.)

This month’s Guest EVA is derived from a source I have read nearly every day since the late 1990s, Horsesmouth. It’s published by my friend, Sean Bailey, and it is a true bargain for investment professionals at just $247 a year (click here to subscribe). One of their regular contributors is Craig Israelsen, PhD, who has authored some of the most erudite, yet accessible, essays I’ve come across over the years.

In this issue, Dr. Israelsen is making some exceedingly important points about how the sequence of returns impacts the three basic types of portfolios—at least in terms of timing inflows and outflows. As he notes, there are essentially three main versions: a lump-sum funded portfolio, a regularly funded portfolio, and a portfolio that goes the other way (i.e., it pays out a stream of cash flow).

In his view, and based on my nearly 36 years of working with high net worth individuals, the first situation is relatively rare, while the other two are much more common. The most relevant for the retiring Boomer generation is, of course, the third iteration, or what the good doctor calls a "distribution portfolio." This is a situation where regular withdrawals are needed, providing income such as to sustain a retirement lifestyle.

As you will read, when you are in distribution mode, it’s not just a question of what you make (or lose) but when a loss or gain happens. The key aspect is that for those nearing or starting their retirement years, incurring losses early on is devastating. Conversely, getting off to a fast start is highly beneficial.

Moreover, it’s my belief—bordering on a cold, hard fact—that this reality is particularly important right now with lofty valuations in almost every investment sector. Now, I realize those are fighting words for the "stocks are always cheap" crowd. So, for a moment, let’s just focus on bonds. It’s inarguable that high-grade bonds are presently providing yields that barely cover inflation. As a result, their real return is negligible (thanks to the recent sell-off in junk, "high-yield" debt at least provides something more like "modest-yield"). Consequently, for a retiree, or soon-to-be, with a balanced portfolio, that puts enormous pressure on the equity side to deliver higher than normal returns.

Of course, the huge glitch with this is that, thanks to so many years of rising prices—pushing valuations toward the highest ever seen historically—the exact opposite is almost certain from stocks, at least over the next three to five years. And it’s that timeframe with which those sniffing around retirement should be particularly concerned. Another 20% upside pop, followed by a replay of 2000/2002, or 2008/early 2009, is definitely not what the doctor—as in Dr. Israelsen—ordered.

In my opinion (I know, there I go again), the only way to cope with this extreme dilemma is to be willing to hold an unusually large cash reserve presently, standing ready to go on the offensive during intense sell-offs. We got a little glimpse of what that can do for future returns a couple of weeks ago (Evergreen was able to lock down some very attractive long-term yields in mid-October, but the window closed very quickly).

If retirement is something you’ve started, or plan to soon, please pay close attention to what may be one of the most important articles you’ve ever read.

![]()

WHEN THE SEQUENCE OF RETURNS MATTERS

Craig L. Israelsen, Ph.D.

Depending on the type of portfolio held, investors—especially retirees—can be devastated by an unfavorable sequence of returns. While you can’t control the market’s performance, you can control the risk level of a portfolio when it is particularly sensitive to losses. Here’s how.

The order in which returns occur matters…sometimes. And when it does matter, it really matters. Unless otherwise noted, all the published performance data we see in the marketplace and in periodicals is based on five assumptions: (1) a lump-sum investment, (2) no additional investments during the time period, (3) no withdrawals during the time period, (4) no inflation, and (5) no taxation.

While this gives us all a common starting point as we evaluate and compare performance data, it also creates a situation where published performance will disconnect with the real world based on what type of portfolio the investments are being used in. For example, there are at least three different types of portfolios (in terms of how money is being invested or withdrawn):

As we will see, the difference in outcomes based on the sequence of returns is astounding.

To study the issue of sequence of returns, we need some returns! So, we will use the performance of the 7Twelve portfolio—a 12-asset-class broadly diversified portfolio. Shown below are the annual returns as they actually occurred over the past 15 years. Let’s now examine if the three investing scenarios noted above play out if we alter the sequence of returns.

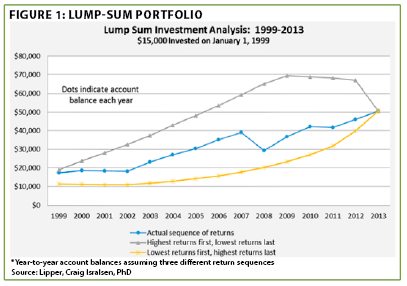

Lump-sum investment

As shown in Figure 1, the ending balance of a single $15,000 investment on Jan. 1, 1999, was identical 15 years later (Dec. 31, 2013) regardless of how the 15 annual returns occurred. The sequence of returns made no difference in the ending outcome. The blue dotted line represents the growth of $15,000 based on the actual year-to-year returns of the 7Twelve portfolio.

The yellow line with asterisks represents the growth of $15,000 assuming the lowest returns occurred first and the highest returns occurred at the end of the 15-year period. Thus, the return of -24.62% occurred first, followed by -1.66%, followed by -1.01%, and so on. The last return in the 15-year period would have been 27.09%.

The gray line with triangles represents the growth of $15,000 assuming the largest returns occurred first and the lowest returns occurred last. The ending result of a lump-sum investment is unaffected by the sequence of returns. The key word here is "ending" result. Obviously the account balances for the three different sequences of return were very different along the way. But at the end of 15 years, they landed in exactly the same place.

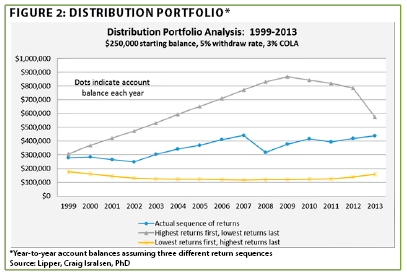

Distribution portfolio

As shown in Figure 2, the ending balance of a retirement portfolio that started with $250,000 on Jan. 1, 1999, was very different 15 years later (Dec. 31, 2013) based on the sequence of the 15 annual returns in the 7Twelve portfolio. The first of the 15 annual withdrawals was $12,500 (assuming a 5% initial withdraw rate). Each annual withdraw increased by 3% (referred to as a 3% COLA, or costof- living-adjustment). Thus, over the 15-year period, a total of $232,486 was withdrawn.

The blue dotted line represents the annual account balance of distribution portfolio based on the actual year-to-year returns of the 7Twelve portfolio. The ending portfolio balance was just over $438,000.

The yellow line with asterisks represents the annual ending balance assuming the lowest returns occurred first and the highest returns occurred at the end of the 15-year period. This, of course, is a catastrophic sequence of returns for a distribution portfolio, as shown by the ending account balance of under $160,000.

The gray line with triangles represents the account balance assuming the largest returns occurred first and the lowest returns occurred last. This is the ideal scenario for a distribution portfolio, as shown by the ending balance of over $573,000.

The ending outcome in a distribution portfolio is dramatically affected by the sequence of returns. Avoiding small or negative returns in the early years of the distribution period is critically important.

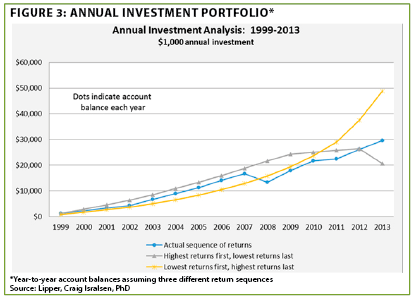

Annual investment portfolio

As shown in Figure 3 on the next page, the ending balance of a portfolio in which $1,000 was invested annually at the start of each year (from Jan. 1, 1999, to Dec. 31, 2013) was substantially different 15 years later based on the sequence of returns.

The blue dotted line represents the annual account balance of distribution portfolio based on the actual year-to-year returns of the 7Twelve portfolio—with an ending portfolio balance of just under $30,000.

The yellow line with asterisks represents the annual ending balance assuming the lowest returns occurred first and the highest returns occurred at the end of the 15-year period. This, of course, is the ideal sequence of returns for a portfolio that is being added to each year. The ending balance was just under $50,000.

The gray line with triangles represents the account balance assuming the largest returns occurred first and the lowest returns occurred last. This is the least optimal scenario for this type of portfolio, as noted by an ending account balance of just over $20,000.

The ending outcome in a portfolio that is being added to each year is significantly affected by the sequence of returns. Experiencing larger returns in the latter years is ideal, because those higher returns are affecting a larger account value.

So what?

What does all this mean? Clearly, it’s not possible to control the optimal sequence of returns. While it may not be possible to precisely craft the sequence of returns in a portfolio, it is possible to tilt a portfolio toward a certain level of return—which will be sensitive to the type of portfolio it is.

For example, a retiree’s portfolio is very sensitive to losses during the first 10 years after retirement (when money is now being withdrawn). Therefore, that type of distribution portfolio should be designed with a more conservative approach in the early years. If appropriate, the distribution portfolio could be tweaked toward a slightly more aggressive stance after the retiree is safely out of

the gate (10 or so years into retirement). The key principle being that a retirement portfolio that is in "distribution mode" (that is, sustaining annual withdrawals) should have two mantras: (1) avoid large losses and (2) provide a modest return.

Because sequence of returns matters to portfolios in distribution mode, they must be designed to avoid a bad sequence of returns in the early years. This is doable. The asset allocation (i.e., risk level) of a distribution portfolio can change and adapt over time. It can become more or less aggressive.

The message in this analysis is this: In the early years of a retirement distribution portfolio, don’t swing for the fences. Tend toward the conservative side so as to avoid an early meltdown. Or, have two to three years of retirement income in reserve and allocate the remainder of the portfolio to an ageappropriate level of risk.

This, of course, is simply another version of building a conservative retirement portfolio. Don’t make the mistake of over-risking a portfolio in order to make up for insufficient contributions in prior years. Mistakes of the past (not saving enough) do not justify taking undue risk in a retirement portfolio that may need to stay viable for 30-35 years. Job #1 is to safely grow and preserve whatever amount has been saved—not to swing for the fences in hopes of growing the portfolio account balance to what it should have been.

As it pertains to accumulation portfolios (either a lump-sum investment or annual investment portfolio such as an IRA account), the sequence of returns is either irrelevant (in a lump-sum investment portfolio) or only somewhat relevant (in an annual investment portfolio). In either case, the appropriate risk level for the portfolio design is largely dictated by the age of the investor. Younger investors typically want to maximize return potential from the start. Thus, their portfolios would be largely equity based.

The key issue for the annual investor would be to start tapering their portfolio risk as they approach their transition point (such as retirement). We know that negative returns at the end of the investment horizon are more painful for the annual investor than negative returns at the start of the time horizon. This is logical; we don’t want negative returns to act on a larger balance—and the larger balance will occur later in our investing time horizon.

In summary, the risk of a portfolio should be reduced as the investor is approaching retirement and for 10 or so years after retirement (assuming the portfolio is the primary source of retirement income). This logic produces a 15- year safety window (five years before retirement and 10 years after retirement) where the portfolio is designed to avoid a large loss. We can’t control the sequence of returns, but we can control the risk level of a portfolio during periods of time when it is particularly sensitive to losses.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.