Introduction

Health care continues to be one of the largest expenses in retirement. While many other types of expenses tend to fall in retirement – such as entertainment and travel – the cost of health care continues to climb and represents a larger percentage of retirees’ budgets. Health care inflation has historically been over 4%[1]. The Fidelity Retiree Health Care Cost Estimate forecasts that a 65-year-old couple in 2021 may need $300,000 to cover medical costs in retirement[2].

While these costs can be overwhelming, planning strategies can be utilized to help manage these expenses and be mentally and financially prepared. The earlier you can plan, the better. We recommend putting together a comprehensive financial plan 5-10 years before you retire so strategies can be put in place. However, if you are already in retirement, it is never too late to act.

Understand current costs

The first step in planning is to understand current costs and types of coverage you will be eligible for. Medicare is available to individuals and their spouses who are over the age of 65, are U.S. citizens or permanent legal residents, and have worked 10 years and paid Medicare taxes. On average, medical expenses for someone on Medicare runs a 65 year old roughly $500 per month and rises to $1,500 per month (in today’s dollars) by age 95[3]. These figures can vary significantly based on plans and needs.

What does Medicare Cover?

Part A: Covers hospital expenses after a deductible. Most people do not pay a premium for Part A coverage.

Part B: Covers doctor visits, tests, and outpatient hospital visits. The monthly premium starts at $170.10 in 2022 but can increase based on your income. Medicare Part B premiums increase to $238.10 for those with income above $99,000 for single filers ($182,000 married filing joint) and max out at $578.30 for those earning $500,000 ($750,000 married filing joint)[4]. There is a look back period of 2 years to determine the premium, so there are planning opportunities to accelerate income or realize capital gains 3 years before taking Medicare. If you have stopped work or have lower income you may be eligible to file an appeal to lower the premium.

Medigap/Part C: You can sign up for Medigap (also known as “supplemental”) or Medicare Advantage Part C to cover out-of-pocket expenses related to Parts A and B. Which plan you should choose varies depending on your needs, medical providers, and location. We recommend reviewing these coverage options with a medical insurance professional before you sign up initially, and then again annually during the open enrollment period October 15th - December 7th. We have a network of partners that help you understand the best plan options for you.

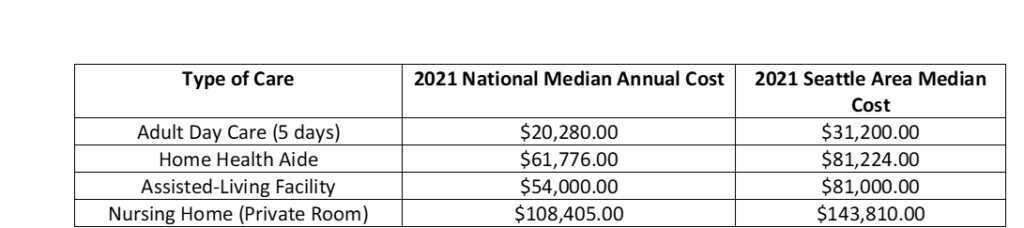

It is important to note what Medicare does not cover. Parts A and B do not cover vision, dental, or hearing, so individuals will need to purchase a supplemental policy for those expenses. There are also many out-of-pocket expenses that are not covered, so having funds available to pay for the unexpected is essential. In addition, Medicare does not cover long-term care. Roughly 70% of individuals turning 65 in 2021 will need some kind of long-term care services in their lifetime, while 48% will need paid care. The average duration of care ranges from 2 to 4 years. The table below illustrates costs for different types of care, both Nationwide and in the Seattle/Bellevue area.

Source: Genworth Cost of Care Survey 2021

Plan ahead before retirement

We recommend reviewing various scenarios within your financial plan before retirement to understand if you are sufficiently funded. As medical expenses can cost a few hundred thousand dollars over the course of retirement, it can be prudent to set aside funds specifically for these costs. These funds can be used to help bridge the gap until you are eligible for Medicare, cover premiums, out-of-pocket expenses, and long-term care costs.

Health Savings Accounts (HSAs) are the most tax-advantageous type of account that you can hold, as they offer triple tax savings. Contributions are tax-deferred, earnings grow tax-free, and any qualified distributions for medical expenses are tax-free. These differ from Flex Savings Accounts (FSAs), which have to be used within a calendar year. HSAs can be held ongoing and can be invested, capitalizing on the tax-free growth of the funds. To contribute, you have to be a participant in a high-deductible health plan, which have a requirement of a deductible of $1,400 for individual coverage ($2,800 for families) and $7,050 for max out of pocket ($14,000 for families). Contribution limits are $3,650 for individuals in 2022 ($7,300 for families). Individuals over the age of 55 are eligible for a $1,000 catch up contribution [5]. The triple tax benefits offered through these accounts make them extremely valuable to help with medical expenses in retirement.

If you are not eligible for an HSA, a Roth IRA is another tax-advantaged account that can be used for retirement expenses, like medical costs. Roth contributions are after-tax, but capital gains and distributions are tax-free. These funds are not limited to medical expenses, as HSAs are, so they do offer more flexibility in how they can be spent. To contribute to a Roth IRA, you must have earned income for the year, but contributions are phased out stating at $129,000 of income for single filers in 2022 (204,000 married filing joint) [6]. You can contribute $6,000 ($7,000 if you are over age 50)[7].

If you are not eligible to contribute to a Roth, you can consider a Roth conversion. This strategy is when you take all or a portion of an existing IRA and pay the income taxes on that amount in that year to add those funds to a Roth IRA, where they will grow tax-free. This strategy works best when you have low-income years and have the funds available to pay the income tax. By realizing the income in a lower tax year, you can convert funds to a Roth IRA to grow tax-free. This strategy can be very beneficial for some, and we recommend reviewing with a tax professional and a financial planner.

If neither of these options are available, keeping funds in a separate investment account can be a good strategy. We recommend keeping these funds invested instead of in cash because it is important to keep principal from eroding, especially considering the level of healthcare inflation.

Before you retire it is also prudent to consider purchasing a long-term care policy. These insurance products can help bring peace of mind, but they are not suitable for everyone. We recommend reviewing options with an insurance professional as there are various types of policies that can be purchased, including traditional long-term care, hybrid, and life insurance policies that can be utilized. Reviewing these options in your 50s and early 60s can help the probability that your application will be accepted and have a reasonable premium that can fit with your budget. Working in tandem with an insurance broker and a financial planner can help you understand the costs and benefits associated with the various options.

When can you sign up for Medicare?

There is a seven month Initial Enrollment Period (IEP) for signing up for Medicare, three months before you turn 65, the month you turn 65, and three months after you turn 65. There is an exception if you are currently employed and covered by a health plan, or if you are on the policy of a spouse who is actively employed. It is incredibly important you sign up for Medicare at the right time because if you miss the correct window you will face penalties for the rest of your time on Medicare.

If you are planning to retire before you are 65, know your options for health insurance. We recommend working with a medical insurance broker to find a plan that works for your needs and to perform an annual review during open enrollment as plans can change considerably from year-to-year.

How to best fund long-term care?

Many individuals will end up needing some kind of care, so it is essential to start planning as early as possible. We typically run different types of care scenarios through the plan to understand what is feasible. It is important to ask yourself the following questions:

If you live in Washington State and are currently a W2 employee, a new payroll tax of 0.58% will fund a lifetime benefit of $36,500 for long-term care expenses, indexed to inflation. This tax was intended to be implemented starting January 2022 but has been pushed out to July of 2023.

If you do not have an insurance policy, sufficient assets, or income to cover long-term care, Medicaid will pay for care. Rules vary based on your state, but to qualify you typically must spend the majority of your assets and have very limited income. If you think you may have to go on Medicaid, we recommend reviewing with an attorney to help qualify.

Conclusion

As plans change and life evolves, it is essential to revisit your financial plan to make sure you are on track to meet your goals and cover necessary expenditures. If you haven’t completed a comprehensive financial plan, or if you are unsure the best plan to handle these costs, reach out to info@evergreengavekal.com to schedule a consultation, or take the client compatibility survey on our website.

Katie Vercio, CFP®, CDFA®

Senior Financial Planner

To contact Katie, email:

kvercio@evergreengavekal.com

[1] BLS, Consumer Price Index

[2] https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

[3]Consumer Expenditure Survey November 2020 https://www.bls.gov/opub/btn/volume-9/how-have-healthcare-expenditures-changed-evidence-from-the-consumer-expenditure-surveys.htm

[4]https://www.medicare.gov/your-medicare-costs/part-b-costs

[5] https://www.irs.gov/publications/p969

[6] https://www.irs.gov/retirement-plans/plan-participant-employee/amount-of-roth-ira-contributions-that-you-can-make-for-2022