There may be no more well-known financial personality right now than Jim Cramer. With his high-pitched voice, his gatling gun verbal delivery, his frantic arm waving, and his uncanny Vladimir Lenin look-a-like looks, his extraordinary successful career on CNBC is more than a little perplexing. One could quip that he has a face made for radio but then there’s that voice which definitely isn’t.

So, what’s Jim got that has made him an unquestioned media super-star? I think it comes down to passion. He utterly and constantly exudes passion of the most intense degree, especially in comparison to his far more traditional and reserved colleagues on America’s most watched financial news channel.

The problem with all that emotion is that when it comes to investing—or dispensing investment advice—it’s more of a liability than an asset. Now, when it comes to entertaining, it’s a totally different story. And, if you didn’t know by now, I’ll clue you in: Jim is about 90% entertainer and 10% investor.

Now, that’s not to say he isn’t fabulously rich and that he hasn’t made a ton of money in his Charitable Trust that he’s always disclosing on his “Mad Money” show. But I’m old enough to remember how aggressively he flogged the tech mania back in the late 1990s and into early 2000 as it became the most extreme equity bubble in US history—until last year, of course. And it doesn’t take 40 years of experience in the investment business to recall his constant exhortations—delivered in his typically hyper-kinetic manner—to avoid all things energy related (with a couple of tepid suggestions, such as Chevron)—back in the summer and fall of 2020 when they were trading like they were uninvestable. In fact, that’s what Jimbo constantly told his audience as this sector was selling at early-1930s type valuations.

The most vivid recollection I have of that period was when one of his viewers called into his Mad Money show, in the late summer of 2020, asking about Enterprise Products Partners. Since that is one of my favorite investment vehicles of all-time, my ears perked up. His fan-guy asked him if at $13 and with a yield of, coincidentally, 13%, based upon a distribution that went up every year, including during two of the worst energy busts in history, it might not be a buy. (Ok, I paraphrased a bit, but not much.) Jim, who at that point hated almost all things energy-related, screamed to the effect “Uninvestable!” and then hit his infamous “loser idea” horn.

Fast forward to today and Enterprise is at $24. It now yields nearly 8% which, in a world of interest rates still gone (mostly) missing, is rather on the generous side, particularly considering its payout has risen much faster than inflation over the quarter-century of its publicly traded life. Thus, that would be a capital gain of 84% plus a distribution yield of 13% or close enough for government work to call it a double. Of course, in tech land, such returns over an 18 month, or so, holding period were totally passe…emphasis on WAS. These days, outside of the leviathans like Microsoft, the returns now mostly have minus signs in front of them, often attached to losses in the 70% to 80% range. A wag could observe that the COPS* have been busted.

Unsurprisingly, these days Jim is now mostly a tech-hater, again with some exceptions, like the ones that are still going up, and a sudden convert to energy bull status. Frankly, I think he’s right but a lot of returns have gone under the bridge, both ways, and contrary to his 2020 and 2021 urgings, before his epiphany. But that’s not really why I’m bring up Hail Cramer. (Is that really what he shouts every day? If so, maybe they should have him on those Caesar’s Palace commercials with the Manning guys and the woman with the golden dress; I “bet” all my male readers have noticed her!).

Rather, it was what he said on Wednesday of this week that once again caught my attention. He announced in his usual end-of-story way that the Fed is tightening and that’s bearish. To which, I thought, really?

First, is the Fed actually tightening. Well, no, in fact, it is still easing. Second, what usually happens to the stock market in the early stages of a Fed tightening cycle? If you answered it goes up, maybe you should have your own financial news show. Because it does—consistently and often for years.

However, stocks are going down despite ample history to the contrary and if there is one thing Jimbo respects it is market action. In his usual trend-following way, he’s picking up on the reality that something is different this time and, again, I think he’s on the right scent, unlike in 2000 when he stayed inside the tech bubble way, way too long.

As the EVA PR section of this newsletter has been pointing out for months, the Crazy Over-Priced Stocks, the COPS, were struggling even before the overall market entered correction mode this year. Per Morgan Stanley’s Mike Wilson, the most expensive stocks were already down 30% in the last two months of 2021.

This year has continued the carnage as reflected in the market price of the ARK Innovation fund which is a close proxy for the priciest stocks known to woman or man (of course, always with exciting stories!). As the first month of 2022 draws to a close, ARK Innovation has tumbled another 30% after a 25% decline last year when the S&P 500 vaulted by nearly 28%.

Since retail investors tend to be heavily exposed to high momentum stocks with alluring narratives, it’s surprising that they continue to pour money into equities considering the losses they must be incurring. According to the Financial Times, as reported by Jim Grant (he of bow-tie fame), retail investors have been on-balance buyers every trading day thus far in 2022. In fact, they have produced inflows this month to a greater degree than all but two days of 2021.

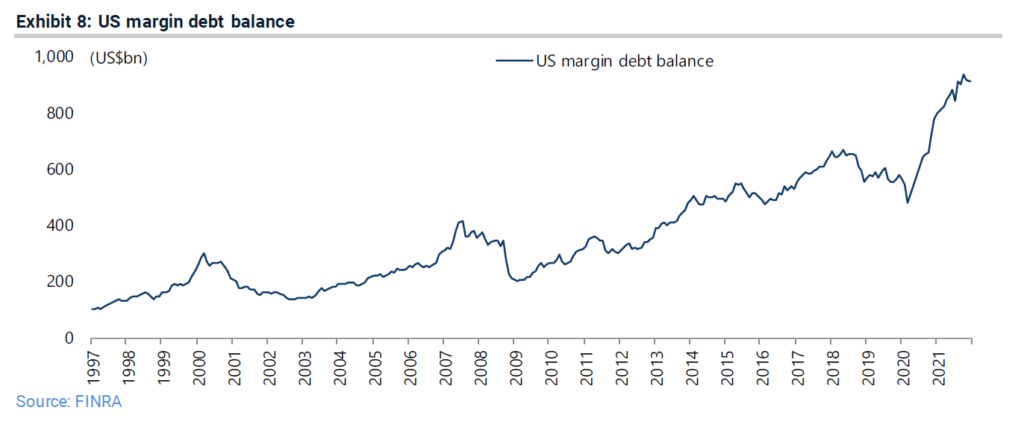

Moreover, margin debt has remained at dizzying levels. Based on these combined statistics, capitulation is clearly not in evidence. Because I’m a believer in one of legendary market technician Bob Farrell’s cardinal investing rules, “The public buys the most at tops and sell the most at bottoms” (with slight paraphrasing), that isn’t terrific news for the bulls.

Thus, this is another serious oddity, combined with such broad market weakness at a time when Fed policies remain as soft as a wet marshmallow. For sure, it is poised to tighten—finally—but that’s typically viewed as a sign of economic vitality and, accordingly, upward pressure for earnings and stock prices, at least until late in a tightening cycle.

Perhaps that’s why current conditions are so out of synch with history. Presently, fears are mounting the economy is heading in a southerly direction while inflation continues to be most non-transitory. Accordingly, the dreaded scourge of stagflation is hanging over the stock market. The Big Stag was a key factor in why the decade of the ‘70s was so punitive to equities. Accordingly, if it’s back to stay that’s staggeringly (sorry) bad news.

Although that seems to be what the market is now discounting—even if retail investors aren’t—I’m not buying the stagflation theme. It continues to be my belief that as Covid fades, with Omicron dramatically increasing herd immunity, and as inventories are rebuilt (like autos), the economy should reaccelerate by summer. In fact, it could be too robust by then, putting the Fed into another tight spot that might cause them to tighten—a lot and a lot faster than it normally does with its ultra-cautious and plodding style.

As a reminder, there is now around $2.7 trillion of excess savings on consumer balance sheets. State and local governments are also sitting on massive sums of unspent funds they are itching to deploy. And as my partner Louis Gave has repeatedly observed, US households have accrued a staggering $30 trillion of net worth increases since the virus crisis began.

In other words, the market may be pricing in the wrong problem. Later this year, there could be too much of a good thing, forcing the Fed to play even faster catch up. If I’m right, what might be excellent news for Main Street might be most problematic for Wall Street…and for retail investors who continue to buy the COPS despite a breakdown so obvious it’s causing Jim Cramer to recommend energy stocks. Yes, as a raging energy bull since the Covid price collapse, that does make me nervous!

*Crazy Over-Priced Stocks

Positioning Recommendations

Ok, I admit it—I’m feeling most faked-out by the big rally in the gold miners last week only to be followed by another bout of weakness. Thus far in 2022, they are still outperforming the overall market but not by much. Unquestionably, fears of a Fed on the warpath are behind the sell-off but I continue to believe our dear central bank will have an extremely hard time getting anywhere near tight. Thus, I continue to counsel patience with this group at a time when trillions of fake money have been dumped into the global financial system and are still sloshing around in it.

America’s largest copper producer has been hit hard lately due to concerns that the Fed is destined to overtighten. Earlier this week, I listened to its CEO and he was very bullish on the outlook for copper, particularly given the rapidly swelling demand for the red metal from electric vehicles as well as the increasing hostility of governments around the world toward new mine development. This is particularly the case in Chile which is one of the most important supply sources.

LIKE

NEUTRAL

Continuing on the theme of leading miners, the world’s largest uranium producer has come under intense selling pressure recently. Even the European Union has moved nuclear power into the green category and worldwide there is growing awareness that nuke energy is critical to decarbonization. I may move this one to official buy status before long (and I’m also hoping to be able to name names in the near future).

DISLIKE

Time for a shorty victory lap, maybe half-way around the track. Green energy stocks have been extremely weak of late. Some of the more utility-like members of this sub-sector, which were not part of my original negative appraisal, now look possible buy candidates. In this market, buying is small increments is prudent.

DISCLOSURE: This material has been distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, are subject to change, and reflect the personal opinions of David Hay (an employee of Evergreen Gavekal) as of the date of this publication. This publication does not necessarily reflect the views of Evergreen’s Investment Committee as a whole. All investment decisions for Evergreen clients are made by the Evergreen Investment Committee. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed, and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this letter have been selected to illustrate the author’s investment approach and/or market outlook and are not intended to represent Evergreen’s performance or be an indicator for how Evergreen or its clients have performed or may perform in the future. Each security discussed in this letter has been selected solely for this purpose and has not been selected on the basis of performance or any performance-related criteria. The securities discussed herein do not represent an entire portfolio and, in the aggregate, may only represent a small percentage of a Evergreen’s client holdings. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Before making an investment decision, the reader should do their own research and/or consult with their financial advisor. Past performance is no guarantee of future results. All investments involve risk, including the loss of principal.