“The first lesson of economics is scarcity: that there is never enough of anything to fully satisfy all those who want it. The first lesson of politics is to disregard the first lesson of economics.” -THOMAS SOWELL, American economist, political philosopher and author

“There are too many pigs for the teats.” -ABRAHAM LINCOLN, the 16th President of the United States of America

"To take from one, because it is thought that his own industry and that of his fathers has acquired too much, in order to spare to others, who, or whose fathers have not exercised equal industry and skill, is to violate arbitrarily the first principle of association, — the guarantee to every one of a free exercise of his industry, & the fruits acquired by it." -THOMAS JEFFERSON, the 3rd President of the United States of America

(Note: An astute EVA reader pointed out that our Thomas Jefferson quote from last week was erroneous. So, we have located the full and correct version, though we believe the spirit of the message is largely the same.)

To Invest, or Not to Invest, that is the Question. The Wall Street Journal recently ran an article debating whether the Social Security trust fund should be allowed to invest in stocks. The piece juxtaposes two opposing views; one side arguing ‘Yes’ and the other ‘No’.

Admittedly, as a Millennial with 38 years until I can collect support, Social Security benefits have been a distant thought. In fact, I’ve heard so many stories about the trust’s (almost certain) mid-2030s depletion of funds, that I’ve never counted on Social Security as a substantial source of retirement income. The silver lining for Baby Boomers, Millennials, and anyone expecting (or rather hoping) for full benefits after 2034, is that there is a potential solution to the problem.

During the bull market of the late-1990s, Bill Clinton proposed investing Social Security funds in the stock market. Opponents, including then-Federal Reserve Chairman Alan Greenspan, quickly shot down the idea claiming that the federal government shouldn’t meddle in equities. The L.A. Times even went so far as to question whether Clinton was a socialist for floating the idea.

While the solution is not necessarily new, it has received a recent shot-in-the-arm from current bull market optimists and a 2016 publication claiming that:

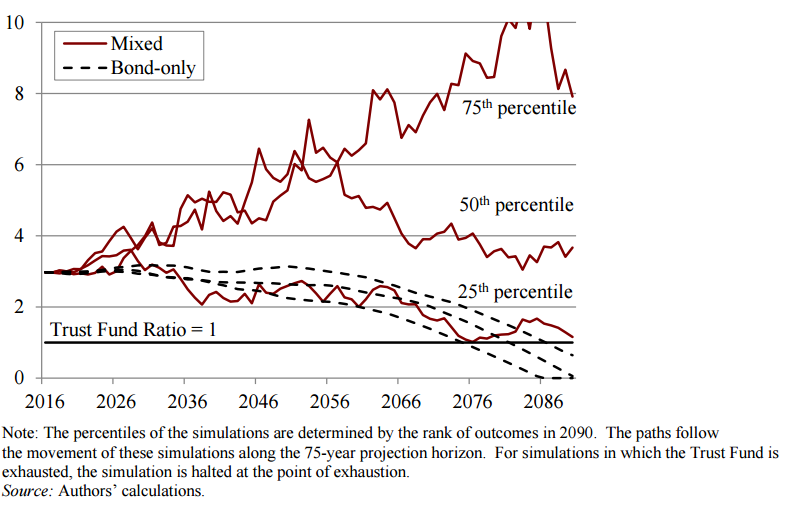

To support this claim, Figure 1 shows the projected median outcome would leave the Social Security trust fund ratio in decently better shape by 2090 than it is today. (The trust fund ratio is the ratio of total assets at the beginning of the year to the total outflow of funds during that year.)

FIGURE 1: PROJECTED TRUST FUND RATIO, 2016-2090

Source: Center for Retirement Research at Boston College

Source: Center for Retirement Research at Boston College

If all this is true, what reason would anyone have for opposing the investment of the Social Security trust in the stock market?!?

As the “No’s” would have it, there are still plenty of reasons to object.

The first reason proposed by Michael Tanner, champion of the “No’s”, is perhaps the most practical. Tanner states that:

“Bonds in the Social Security trust fund aren’t actual assets, but merely claims against future revenues. To invest those funds in other assets, the Social Security Administration would first have to redeem those bonds for cash…with the U.S. running a deficit and already $20 trillion in debt, finding money to redeem the bonds likely would require either additional taxes or borrowing or both.”

While his point is not without merit, it’s a weak opening salvo considering we live in an age where central banks and governments unapologetically meddle in the affairs of public financing.

A (seemingly) more convincing argument is that stocks owned by the Social Security trust fund “would be about 14% of [total] stock value.” That is, of course, assuming all of the $2.9 trillion trust is invested in the $21 trillion equity market. The logic here is that the U.S. government would own a significant stake in major U.S. companies and, for those against government in business, this is an undoubtedly troubling thought. But, evaluated more carefully, this is a very disingenuous position to take.

Not even those rallying around ‘Yes’ would argue for 100% of the trust to be invested in stocks. Rather, the argument that Munnell and others make is for a 40% ceiling on equity allocation, which would put the total value of stocks owned by the federal government closer to 5.5%. But do we really want the federal government owning any portion of U.S. companies? Should we heed the advice of our 31st President, Herbert Hoover, who said “it is just as important that business keep out of government as that government keep out of business”?

To fully comprehend where the debate on Social Security reform is heading, it’s important to understand the foundations of Social Security. In the following section, I will take readers through a brief history of our country’s bedrock social program before circling back around to the questions at hand.

A Brief History. Revolutionary War figure Thomas Paine was one of the first proponents of a modern retirement benefits system in the United States. In 1795, he published Agrarian Justice, which called for the establishment of a public system of security in America. While his revolutionary (no pun intended) idea was not widely accepted, he did lay the foundation for this type of social program in our young country.

In the 1880s, significant changes in America led to an increasingly obsolete traditional system of social support. Three triggering events were the Industrial Revolution, the urbanization of America, and an increase in life expectancy. The net result of these changes was that America was more industrial, more urban, and older.

Fast-forward a few decades… And imagine the opening bell of the New York Stock Exchange on the morning of October 24, 1929. Over the course of three months, the stock market lost 40% of its value. As America slipped into economic depression over the next few years, unemployment reached 25%, close to 10,000 banks failed, the Gross National Product (GNP) declined from $105 billion to $55 billion, and net new business investment was -$5.8 billion.

In response to this major depression, President Franklin D. Roosevelt announced his intention to provide a program for Social Security in a message to the Congress on June 8, 1934. The Social Security Act was signed into law one year later.

The new Act created a social insurance program designed to pay people age 65 or older a stream of income after retirement. The novelty of this was that workers contributed to their future retirement benefits by making regular payments into a Social Security fund during their working years.

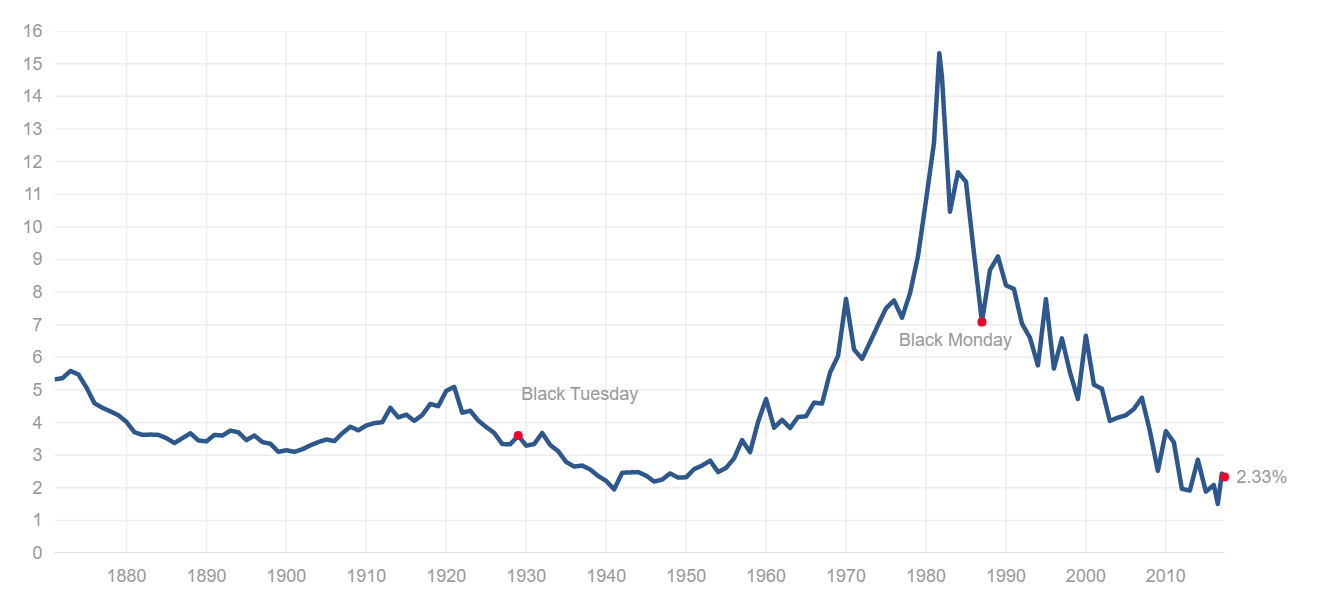

Declining Rates and Baby Boomers. To remind readers why the question of investing the Social Security trust fund in the stock market even exists, consider the following: interest rates have been trending downward for over 35 years. That means that an entire generation of professionals have experienced nearly their entire career in a declining rate environment. (Imagine if the reverse were true, and equity markets were in a 35-year free-fall!)

10 YEAR U.S. TREASURY RATE

The problem with this is that the Social Security trust is invested entirely in U.S. Treasury securities. So, an investment vehicle that once-upon-a-time yielded pretty darn good returns, has reached historic lows. Considering we live in an economic environment where even negative rates aren’t out of the question, no wonder people are looking for alternative solutions!

To add to the problem, Baby Boomers began to reach the age of 65 in 2011. As the largest generation in American history, with over 76 million Boomers born between 1946 and 1964, the population of people retiring at age 65 has started to outpace those entering the workforce and contributing to Social Security.

In addition, when the Social Security Act was signed into law in 1935, the average life expectancy was 61 years, which is lower than the age where most could collect their benefits! (Although, admittedly, this statistic is skewed due to the high infant mortality rate of the early 20th century. As the Journal points out, the life expectancy of anyone reaching 65 in the 1930s was actually 79 years.) Today, life expectancy has ballooned up to 84.3 years for men and 86.6 years for women.

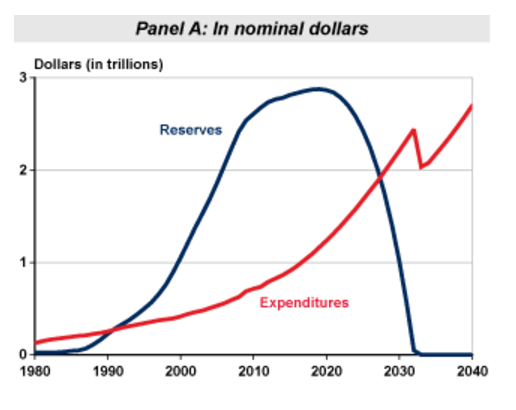

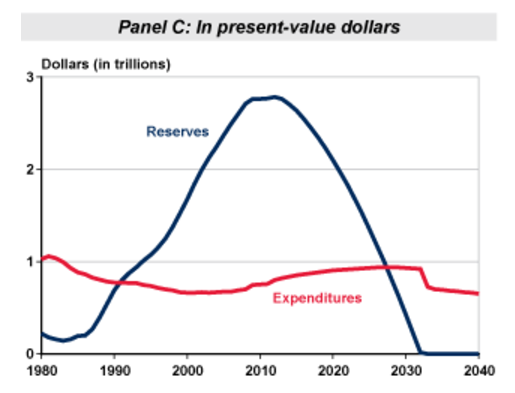

These factors – a low-rate environment and an aging workforce with longer life expectancy – contribute to the Social Security dilemma that trust reserves face a sharp drop-off sometime in the next 10 years, and a complete depletion around 2034.

SOCIAL SECURITY TRUST FUND RESERVES AND EXPENDITURES

UNDER TWO ALTERNATIVE MEASURES, 1980-2040

Source: Social Security Administration

But looking too far and too fast for a growth-based solution to this problem might lead to a gut-checking reality for those in the “Yes” camp.

When Bill Clinton proposed investing in the stock market in the late 1990s, America was experiencing one of the greatest stock market booms in its history. The tech bubble of the early 2000s brought an end to that optimism (and to the conversation that equities were a fail-safe option for people’s retirement income). Likewise, today, we stand squarely in the midst of another long economic expansion and, by most accounts, a fully-valued (if not seriously overvalued) stock market.

If we were, for a minute, to put aside concerns over how long until we experience a market correction and how severe that correction might be, we must ask ourselves, if the Social Security trust fund was to be invested in the stock market, what exactly would it be invested in?

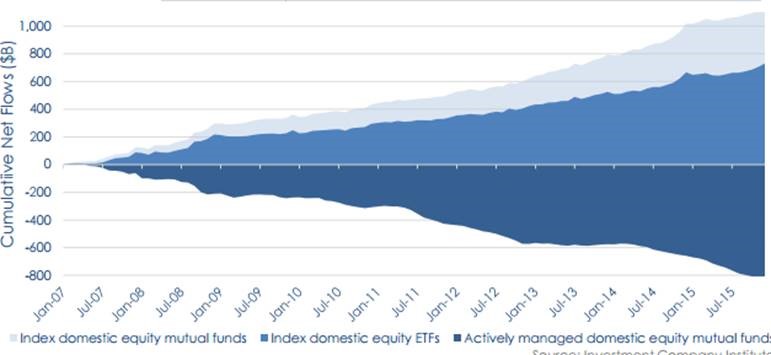

Answering that question requires an examination of where money has flowed over the past 10 years. The chart below shows the mass exodus out of active management (-$800 billion) and into indexed equities ($1.1 trillion).

CUMULATIVE NET FLOW FROM ACTIVELY MANAGED FUNDS TO INDEXES

Source: Investment Company Institute

It’s no coincidence that the chart begins in 2007 – the same year of the Great Recession. In order to “minimize risk” (we’ll see how this is a false premise below) that a stock could go from hero-to-zero in a matter of days, investors began to diversify their assets in index funds that owned a portfolio of strategy-based stocks.

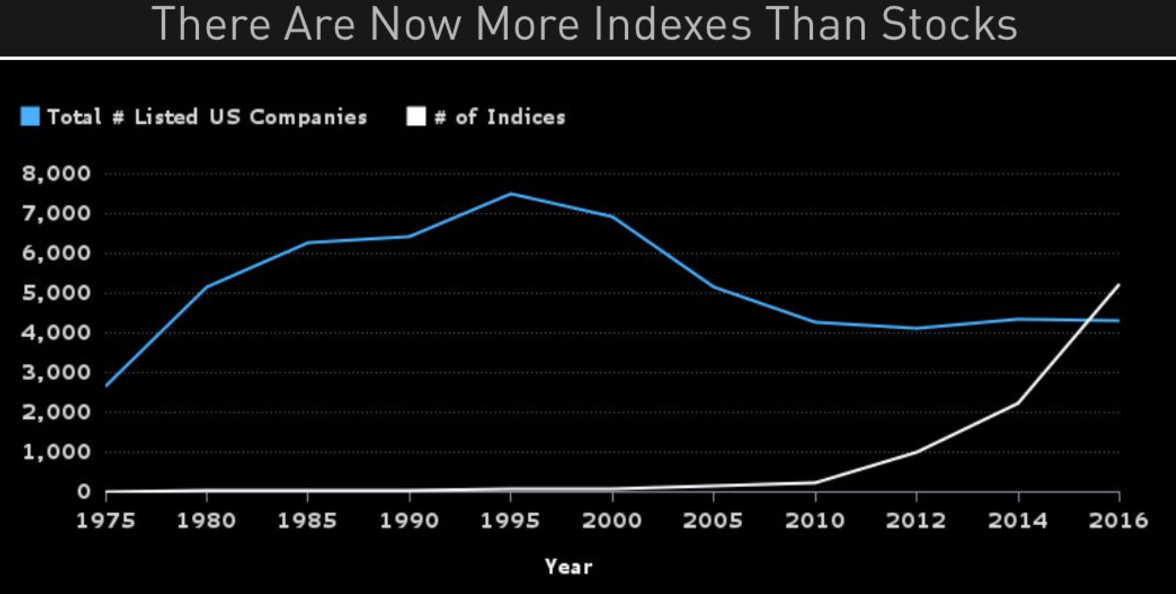

The result was both an influx of money from actively managed funds to passively managed funds (as shown above), and a boom in the number of exchange traded funds (ETFs). For example, in 2005, there were 204 ETFs in the United States. In 2015, that number grew to an astounding 1,594. Even more incredible, is that when you consider both ETFs and mutual funds, the number of indexes has overtaken the total number of listed U.S. companies!

NUMBER OF LISTED U.S. COMPANIES AND ETFS (1975-2016)

Source: Eric Balchunas (@EricBalchunas)

Source: Eric Balchunas (@EricBalchunas)

The Indexing Bubble. The reason this is significant is because the trend towards indexation would likely spillover to Social Security funds invested in equities – i.e. your retirement money would be invested in passively managed ETFs and mutual funds. Sounds innocent enough, right? Not quite.

As Steven Bregman of Horizon Kinetics points out in his presentation at the Grant’s Fall Conference, the trend towards indexation has created an artificial supply and demand in equity ETF indexes that has contributed to, what he considers to be, the greatest bubble ever. (This despite the fact that models aren’t showing abnormally high PE levels and volatility is low. Although, considering the last time the VIX reached these lows was February 2007, forgive me if that’s not especially comforting).

To support the theory that we are in an ETF bubble, Bregman states the following:

While nobody knows for certain when this bubble will burst (it could be three weeks; it could be three years, or longer), it is a troubling proposition to “just place 25%-30% of assets into passive index funds” as one reader in the Wall Street Journal suggests. One might argue that taking this approach could leave the Social Security trust in worse shape if the bubble pops, and equity markets correct, at the wrong time. (Note: The original Wall Street Journal article mentioned at the beginning of this EVA sparked a lot of debate. The Journal ran a follow-up article with an edited transcript of readers’ responses.)

Closing Salvo. Even though the “Yes” and “No” camps don’t have much in common, one thing both sides can agree on is that there needs to be Social Security reform. But what does that look like?

In Evergreen’s view, the overarching issue is the logic of investing trust fund assets completely in US government IOUs. Imagine if Boeing or IBM funded their retirement plans with nothing but their own debt. The howls of protest would be deafening!

Critics would rightly claim such a scheme is nothing but a totally unfunded liability. When the number of retirees was modest compared to the working population, it was a non-issue (except for those rational folks who looked far enough ahead to predict the coming demographic shifts). It should be clear, based on the foregoing, that we are rapidly approaching a reckoning point.

There have been several reasonable proposals floated in recent years to restore the solvency of Social Security that do not include investing trust fund assets in equities. Some of these ideas include means-testing and gradually extending benefit start dates (there has been some deferral of eligibility but, thus far, it’s been too modest to shore up the system). The problem is these proposed fixes have been regularly ignored. It seems nearly all politicians are terrified of touching the allegedly deadly “third-rail” of Social Security reform. As a result of this total lack of foresight and courage, the pain of making the necessary adjustments is increasing as future liabilities continue to mount.

We believe a gradual process of shifting the trust’s assets into a diversified and balanced portfolio of corporate stocks and bonds should be initiated. This could be done without reducing the government’s promise to pay benefits in any way. Thus, it would be similar to a defined benefit corporate plan where the sponsoring company is on the hook should returns fall short. However, by effectively dollar-cost-averaging into stock and bond markets, poor timing risks would be minimized.

Despite the claims of a forthcoming indexing bubble, we believe it’s most feasible to invest these funds in index vehicles with one caveat. We would suggest a valuation-sensitive approach to underweight expensive market sectors and overweight those that are inexpensive. While we realize this aspect is very unlikely to see the light of day, simply funding Social Security with assets whose returns are not a function of tax revenues – but rather are generated from the remarkable profits engine of the private sector—would be good enough for (sorry) government work…and for us.

Ok, enough editorializing. We want to hear your views. We concede there are no foolproof answers and both camps have valid arguments. But we also believe it’s a vital topic that impacts (or will impact) a large majority of the population. As such, we should all be actively involved in the discussion and weigh in on this issue. Please leave your opinion in the comments section of the blog post or email mjohnston@evergreengavekal.com.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.