Quote

"2021 shatter[ed] records for [the] number of new startups valued at $10B+."

- Gené Teare, senior data journalist at Crunchbase

Step Aside Unicorns, 2021 Was the Year of the Decacorn

Over the past three years, we’ve published three separate newsletters highlighting burgeoning startups that were expected to hit public markets in 2019, 2020, and 2021. The key commonality between these companies at the time of publication was that they were all venture-backed unicorns (privately held businesses valued at over $1 billion). Despite a few unsuccessful IPO attempts (see WeWork and Ant Group), many of these companies hit public markets as planned.

According to CBInsights, today there are nearly 1,000 unicorns worldwide with a combined market cap of ~3,106 billion. What’s shocking is the pace and frequency at which new unicorns have been minted in less than a decade. Back in November 2013, Aileen Lee, founder of Cowboy Ventures and former investor at Kleiner Perkins, wrote a landmark article that defined a new breed of startups titled, “Welcome To The Unicorn Club”. At the time, there were 39 “unicorns” and on average, about 4 unicorns were born each year.

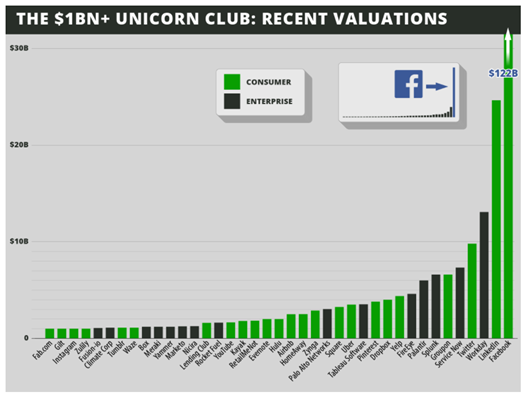

Looking at the chart below, one can see a clear picture of the unicorn landscape from 2013. What’s notable is the heavy weight (62%) of consumer-based companies that made up “The Unicorn Club.” Additionally, at the time of publication, only three companies were part of the $10 billion club. Facebook was the obvious outlier valued north of $100 billion. What’s shocking is that Facebook – now Meta –accounted for almost half of the $260 billion aggregate value of the unicorn breed in 2013.

As such, Facebook was given a special title at the time – “super-unicorn” – for being worth over $100 billion. Fast-forwarding eight years to December 2021, the terminology for such a company is now hectocorn. At the time, there was no terminology for a company valued at over $10 billion. But oh, how times have changed.

Source: TechCrunch

The Year of the Decacorn

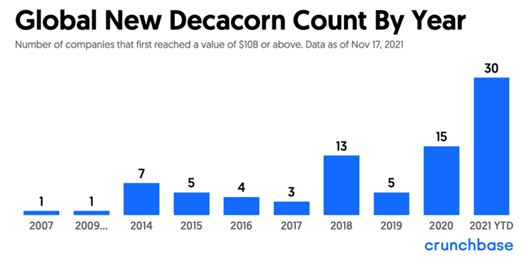

As Crunchbase recently noted in a November publication, “more new startups valued at $10 billion or above have been minted in 2021—far more than in any prior year, and double the number created in 2020, which set the previous record for new “decacorns.”

In total, 84 decacorns have been produced since the first private $10 billion valuation in 2007 (Facebook for anyone who’s tracking), meaning 36% of decacorns were birthed in 2021 alone.

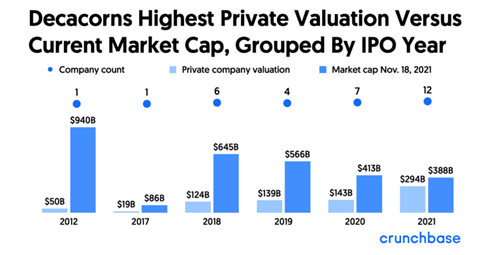

To date, 33 of these have since exited (either through IPO or SPAC), leaving 51 decacorns in the private purview. However, what’s fascinating is that while 2021 was a banner year for newly minted $10 billion+ companies, decacorns that hit public markets in 2021 fared worse than any other year on record.

Which leads one to wonder, are private market valuations currently inflated?

According to a recent article published by the Wall Street Journal, the answer is a resounding yes. As they noted, “SPACs and venture capitalists are plowing money into startups at record rates, looking past worries about lofty valuations… Investors are defying a share-price slump for newly public companies to make hundreds of billions of dollars available to startups, a cash pile that promises to inject a torrent of money into early-stage firms in 2022 and beyond.”

Despite lackluster performance on public markets and valid concerns raised by pundits, as we head into 2022, investments will likely continue to flow into high-growth companies pre-IPO, as investors chase new opportunities in a “technological golden age” where the convergence of several macro and micro factors present significant long-term upside. Of course, not every unicorn or decacorn will turn into the next hectocorn (a la Facebook), but with more than 90 companies currently valued between $5 billion and $10 billion, and hundreds of billions of dollars sitting on the sideline waiting to pour into promising high-growth companies, we’re unlikely to see a noteworthy slowdown in the space as animal spirits continue to run wild.

Michael Johnston

Tech Contributor

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.