“Over the past decade a combination of diverse forces has created a significant increase in the global supply of saving - a global saving glut.”

-BEN BERNANKE, in a 2005 speech

Ben Bernanke popularized the term “global saving glut” in March 2005 when speaking to the Virginia Association of Economists in Richmond, Va. In his statement, he argued that several forces had created a high volume of global savings and that this “saving glut” helped explain the many years of historically low yields. And that was long before the Fed and its fellow central banks, through their coordinated actions, engineered the virtual extinction of interest rates!

While this glut has baffled luminaries including Mr. Bernanke’s mentor—the once-revered “maestro” of the Fed, Alan Greenspan—the associated low rates have almost certainly propelled markets to higher highs over the past several decades. But, even considering the buoyancy that markets have received from this supposed excess of liquidity, the saving glut phenomenon hasn’t completely barred bear markets. In fact, we’ve seen the two worst declines since the Great Depression in the era of the saving glut.

Following the most recent global meltdown, Mr. Greenspan, even testified to the Financial Crisis Inquiry Commission in 2010, that: “Whether it was a glut of excess intended saving… the result was… a fall in global real long-term interest rates and their associated capitalization rates. Asset prices, particularly house prices, in nearly two dozen countries accordingly moved dramatically higher. U.S. house price gains were high by historical standards but no more than average compared to other countries.”

This complex relationship between global savings, investments, and interest rates is incredibly important to understand when analyzing and projecting market movements. In the pages below, Will Denyer, of our partner firm Gavekal, draws important conclusions about how these factors have and will continue to influence asset prices.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

THE SAVINGS GLUT'S LONG LIFE AND SLOW DEATH

By Will Denyer

Demographics, some say, can explain two-thirds of everything (the problem of course is knowing which two-thirds). Demography has certainly influenced long term asset-price trends. For roughly 35 years, from the early 1980s until just recently, global capital markets were lent wings by a major demographic tailwind. Changes in the age structure of the world’s population created a “global saving glut”, to use the term popularized in 2005 by then Federal Reserve governor Ben Bernanke. The high volume of savings looking for a home bid up asset prices massively, propelling secular bull markets in both equities and bonds. It was a great time to be in finance.

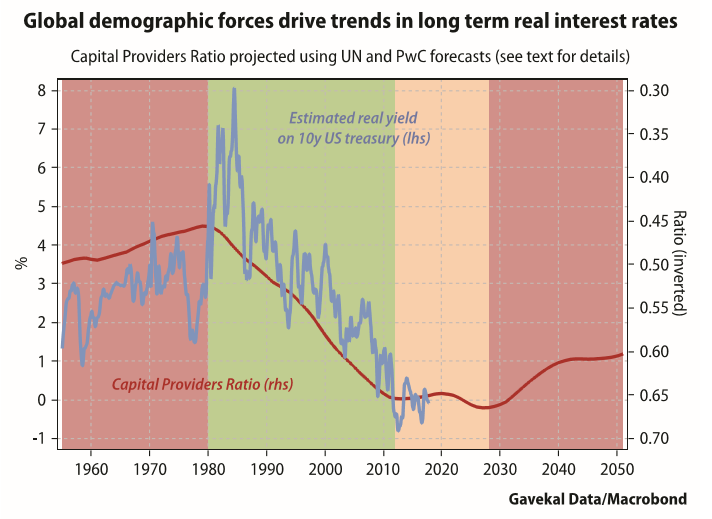

Now that demographic tailwind is fading. And a decade hence it is likely to reverse, turning into a headwind for asset prices. To chart the impending changes, this paper introduces a new measure, the Capital Providers Ratio, which translates demographic shifts into trends in real interest rates, and so to asset prices. The basic conclusion is that real rates will stay at roughly their present low level for another 10 years or so, and then start to move up as the supply of excess saving begins to thin out.

Saving / investment stage 1: The Baby Boom Effect

Globally, saving must equal investment. But capital is mobile, so it does not follow that savings must equal investment within individual economies. Even China, which restricts private capital flows, still sees large capital outflows through official—and unofficial—channels.

As a result, different countries show different propensities for saving versus investment. Analyzing data from 85 countries between 1960 and 2005, economists at the Brookings Institution found that a country’s propensity to save is likely to exceed its propensity to invest when the population is skewed toward the ages of 35-64.

This pattern of saving and investment makes intuitive sense. Children earn nothing and consume plenty, so they are a drain on national saving. At the same time they call for investments in schools, clinics, larger homes, and so on. Higher education extends the period in which young adults are saving little, while much is invested in their education.

After they enter the workforce, most young adults will not earn enough to do much saving. And these young workers either invest a lot themselves (buying their first home and other durable goods) or encourage companies to invest on their behalf (directly, for example through worker training, or indirectly, e.g. by building factories for them to work in). So, when a country has a baby boom and has a population increasingly skewed toward children and young adults (0-34 years) it will show a stronger propensity to invest and a relatively weak propensity to save.

In a single country, this shift might manifest itself through more borrowing from abroad. For the global economy, a closed system, saving and investment must be brought into balance by a change in the clearing price for saving—i.e. a higher real rate of interest. This is what happened in the West between 1946 and 1980, as the Baby Boomers were born and grew up.

Stage 2: The Middle-Aged Worker Era

As the population ages and the dominant group becomes older workers (aged 35-64 years), the situation reverses. These are the peak earning years for most people, so they can save a lot. At the same time, their investment needs fall; they have finished their education and have already bought their homes. Companies, facing both an aging customer base and a workforce nearing retirement, will be more reluctant to make new long-term investments.

In this era, the propensity to save exceeds the propensity to invest. Individual countries in this situation will tend to export more capital. And if it happens on a global scale, again the clearing price must adjust. The real rate of interest must fall to the point at which savings and investment balance. This roughly describes the period from 1980 to the present: first as the western Boomers matured into their peak-earning years, and then as demographic trends in China and other emerging economies generated plenty of excess savings.

The largest demographic movement in the developing world was China’s baby boom in the late 1960s and early 1970s, before family planning measures that culminated in the one-child policy brought down birth rates. When this group started to have their own children, they created an “echo” baby boom in the early 1990s—a cohort which will reach prime earnings age in about 7-10 years, tilting the savings-investment balance a shade more towards savings.

Stage 3: The Retirement Home

The final stage of the long demographic arc comes when the baby-boom generation starts aging into retirement (assumed to be around age 65). Now the propensity to save falls again, because the typical retiree is a net drain on national savings. Once they stop working, the elderly start to consume their own savings and/or draw on national savings via a public pension plan or national healthcare system. Meanwhile, at this stage investment demand makes a modest rebound, probably because of the need to build new hospitals or nursing homes.

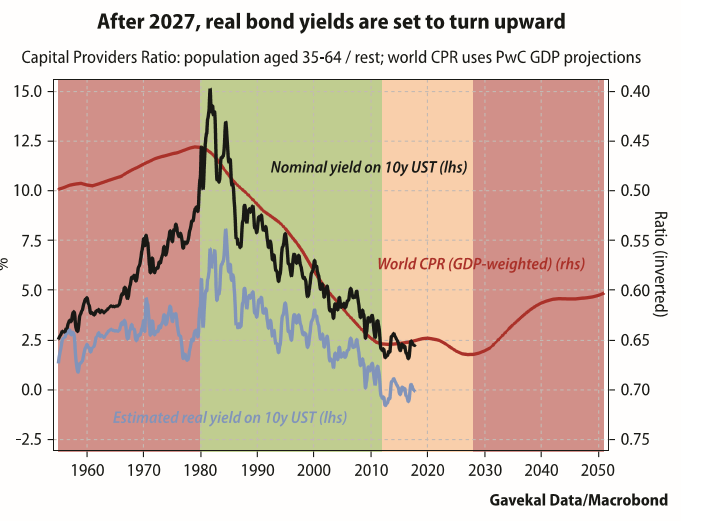

As a result, a very old population, like a young population, sees its propensity to save fall below its propensity to invest. Capital must be borrowed from other countries or, if it is a global phenomenon, the real rate of interest must rise to bring savings into equilibrium with investment. This is the situation the world will find itself facing from roughly 2027 onward.

To make it useful, apply CPR

My Capital Providers Ratio (CPR) presents these shifts in saving and investment behavior in a way that helps explain the demographic impact on interest rates and asset prices. The basic idea is that countries with a relatively large cohort of people aged 35-64 will have excess savings and will tend to export capital, putting downward pressure on the global real interest rate. Countries with relatively large populations younger than 35 or older than 64 will tend to dis-save and push up the global real rate.

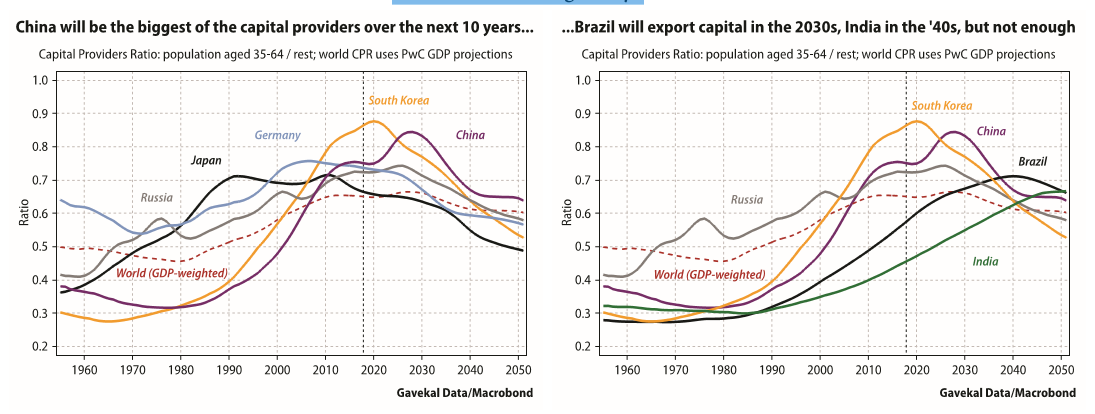

So, to calculate the CPR, we divide the number of people in the 35-64 cohort by the sum of those in younger and older age cohorts. Looking first at the national level, there are no surprises about the identities of the big capital exporters. Japan has been a consistent large-scale capital exporter for 40 years and was best-in-class in the 1980s. But with population aging and its CPR declining towards the global average, Japan no longer features as such a big capital exporter. Today and for the next 10 years, the biggest capital providers will be China and Germany. Smaller but still sizable contributions will come from South Korea and Russia, which have high CPRs but much smaller economies.

Germany will decline as a capital provider after 2030, but China is likely to ramp up quite a bit over the next 10 years, and along with Russia and South Korea will remain an important net provider of capital until 2040. After that, aging will take its toll and these countries’ propensity to save and export capital will decline. Brazil and India will then take up the baton in the excess-savings relay.

The country-level data is interesting, but what we really want to know is the global saving-investment balance and its impact on interest rates. And a moment’s reflection should make clear that, at least under present conditions, the relationship between demographically-driven savings balances and interest rates should be more stable at the global level than at the country level.

The reason is simple: in a world with low barriers to capital mobility, global effects can overwhelm parochial ones. Generally speaking, when the CPR rises—meaning that saving rises faster than investment—real interest rates should fall (and equity multiples rise). If all that mattered was a country’s own saving/investment balance, Japanese rates should have bottomed in the early 1990s when its CPR plateaued, and Germany should have seen its rates bottom in 2005. One reason they did not is that the global saving surplus continued to rise until at least 2010.

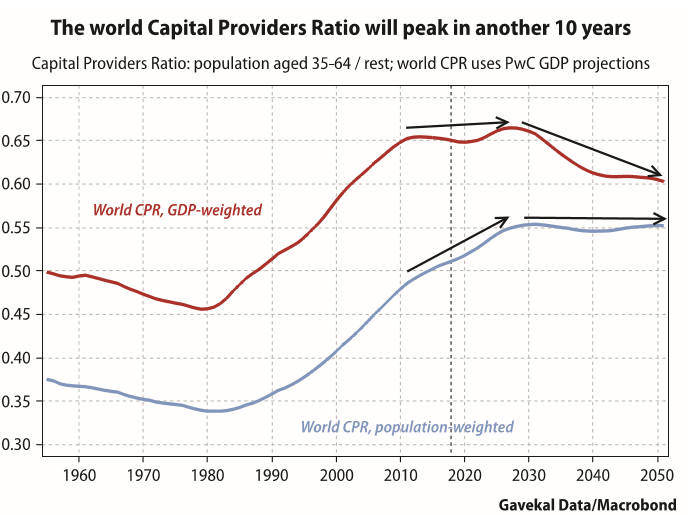

To calculate the global CPR we need to make a choice: weight countries by population or by GDP. On a population-weighted basis (using United Nations population projections), the global CPR is still rising and will not level off until 2030 or so.

But a nation’s ability to export capital is determined by the size of its economy, not its population. So, a GDP-weighted global CPR measure will be more accurate. The red line in the chart below shows an average of the CPRs of the 32 largest economies in the world today weighted by PricewaterhouseCoopers’ long-term GDP projections. These countries make up about 85% of world GDP, and so serve as a decent proxy for the world economy.

On this basis, the world CPR leveled off around 2012. Over the next 10 years it will edge slightly higher once again, thanks largely to the savings contribution of China. But from roughly 2027 onwards it will decline. This implies that global real interest rates are now close to their structural bottom and may start to rise structurally after 2027.

For reference, I have left in the more optimistic population-weighted measure (blue line). It enables us to imagine the trajectory of global CPR if per-capita GDP in high-population, low-income countries such as Nigeria, Egypt and Indonesia grows faster than in PwC’s projections. On the whole, though, the GDP-weighted series is not overly skewed in favor of today’s winners, since it already includes the three countries just mentioned plus India, Vietnam, the Philippines and South Africa—all of which have big populations, strong demographic outlooks and are projected by PwC to enjoy rapid GDP growth in the coming decades.

Watch out for falling long bonds

In short, global real rates have ended a three-decade period of structural decline, will continue to bounce along the bottom for another 10 years or so, and will then begin an inexorable rise. The next question is: What does this mean for asset prices?

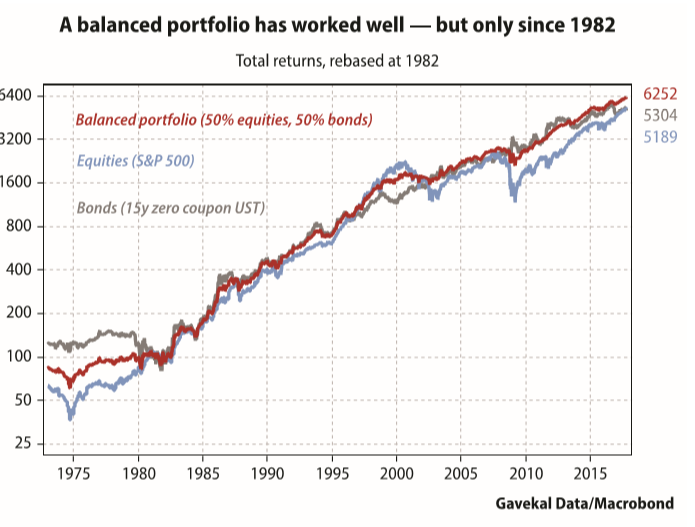

The first observation is that since the early 1980s, investors could have reaped rich rewards simply by holding a balanced portfolio of 50% equities and 50% extremely long duration bonds, such as 20-30 year zero-coupon US treasuries. This has long been Charles’s preferred allocation.

Why did this strategy work? As interest rates went into structural decline between 1982 and the present, equities and bond prices enjoyed a secular bull market—together. But while the long-run trends of the two asset classes were aligned, their short-run variations tended to show an inverse correlation, especially at times of market stress. Thanks to this combination of long-run positive correlation and short-run negative correlation, over the last 35 years a balanced portfolio has offered similar long-term returns as an all-equity portfolio, but with lower volatility.

What worked extraordinarily well during Charles’s career may not work so well over the course of my career. Charles’s approach was to use a very long treasury bond, for example a 30-year zero coupon US treasury—as the basis of his bond holdings, only reducing duration tactically when bonds looked overvalued or overbought.

This strategy could potentially have another 10 years of life in it. But if my demographic analysis is correct, then buying a 30-year bond today may eventually turn out to be dangerous—because it would lock in today’s low interest rates beyond the 2027 structural turning point implied by my Capital Providers Ratio.

Forward projections of current demographic trends suggest the new default for the bond portion of a balanced portfolio should be notes maturing within the next 10 years, before 2027. Investors can tactically reduce duration when valuations warrant (and they should consider doing so today). They can also extend duration tactically when long bonds offer a sufficiently high yield. But investors should be careful about buying bonds with maturities beyond 2027, making sure that the term premium sufficiently compensates them for the fact that the demographic winds are likely to move against existing bond-holders in roughly 10 years’ time.

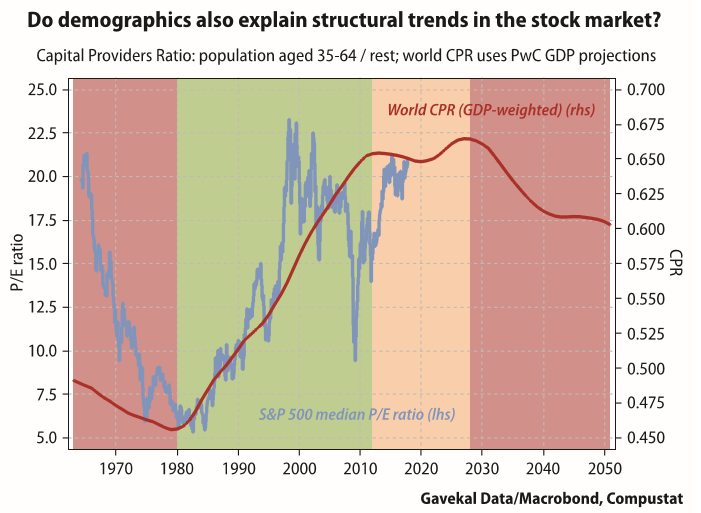

Demographic analysis may also help solve a longstanding equity market puzzle: what lies behind the structural increase since the early 1980s in the S&P 500’s equity multiples? Anatole has long pointed out that investing based on a return-to-the mean for P/E ratios has been a money-losing strategy for the past 25 years. In all that time, it has issued just one buy signal—in early 2009. As the next chart suggests, the rising world CPR since 1980 may have driven up structural equity valuations.

Conclusion

This paper is just a preliminary study of the slow-moving demographic forces that drive long-run trends in asset prices. More detailed work remains to be done. But it does suggest answers to two questions that are very much at the center of investor concerns today:

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.