“The problem with socialism is that eventually you run out of other peoples’ money.”

–Former British Prime Minister MARGARET THATCHER

“Maybe the economy and the market are so abnormal that they can’t handle the move back toward policy normalization (by the Fed).”

–Economist DAVID ROSENBERG

This week’s edition of Bubble 3.0 is a continuation from last week’s chapter, “What Price Prosperity? (Part I)”. If you are just joining us in the middle of this ongoing series, which will eventually culminate in a full-length publication, please take a few moments to review the prior installments in the series:

WHAT PRICE PROSPERITY? (PART II)

(Continued from the January 11th, 2019 EVA “What Price Prosperity? (Part I)”)

The surprise election victory by Donald Trump in November, 2016, radically changed conditions overnight, not just in the US but internationally as well. It was literally the election heard—and felt—around the world. At first, the positive reaction was limited to investor, business, and consumer confidence. Soon, though, what had been a lethargic expansion, even in the US, and recurring recessions in many leading economies, evolved into what would be known by the end of 2017 as a “synchronized global expansion”.

S&P 500 earnings, which had stagnated since 2013, began rising in 2017. As that year progressed, and especially as odds of an enormous corporate tax cut jumped, the stock market started discounting a 20% rise in profits by S&P companies in 2018, leading to 2017’s outstanding full-year return of 21.8%. After years and years of anticipating robust earnings that never arrived, the market finally got it right in 2017. But, as is so often the case, the year of the actual earnings surge—2018—saw stocks initially sprint to the upside and then retreat. The usual culprit for this seemingly counter-intuitive result was the Fed, which was belatedly taking away the proverbial punch bowl.

Moreover, the synchronized expansion aspect quickly faded as one nation after another started reporting disappointing growth numbers. By the late summer of last year, it was pretty much only the S&P and the US economy that were still expanding to a meaningful degree. Even in the US, conditions began to fray with housing prices in several key markets actually falling, leading to a nasty bear market in home building stocks. Then it became clear the US auto industry was decelerating despite record-breaking incentives to move the metal.

Meanwhile, in the US stock market, a sharp correction early in the year soon faded into investors’ memories as prices rebounded and the S&P hit a slight new high in late September. Yet, below the surface, there was definite erosion occurring. Fewer and fewer stocks, mostly tech companies with valuations pushing $1 trillion, were leading the advance. This narrowness, along with an accumulation of eight prior Fed rate hikes and the commencement of quantitative tightening—the aforementioned punch bowl removal by the Fed—were classic warning signs the bull market might not make it a record-breaking 10 straight up years. As we know now, the swooning coal mine canaries back in the fall were falling off their perches for good reason.

As 2018 matured, many (besides this author) questioned the wisdom of the budget-busting Trump-engineered corporate tax cut. Some, such as the estimable Lacy Hunt, were pointing out that the red ink situation was even worse than it appeared on the surface—and that was bad enough. The official deficit for the fiscal year ended 9/30/18 was roughly $800 billion. That was up 17% from the prior year, despite an economy that increased just 4 1/2%. However, according to Mr. Hunt, the true deficit was closer to $1.3 trillion. The difference was due to creative accounting by the Federal government as it considered about $500 billion of spending “off-budget”. (Don’t you wish you could do the same?) Validating his view, the government sold approximately $1.3 trillion in debt to finance itself. As they say (sort of), the proof is in the borrowing.

Similarly, the reigning King of Bonds, Jeff Gundlach, opined in a lengthy CNBC interview last month that the reported (i.e., much too low) deficit is running at a $1.3 trillion annualized rate through the first two months of this fiscal year. He believes the number that will actually need to be financed through the end of this Federal fiscal year, 9/30/19, should end up around $2 trillion or about 8% of GDP.

There are a couple of shocking aspects to this. First, deficits are supposed to fall—not run wild—during the latter stages of an economic up-cycle. Second, if $2 trillion turns out to be the real deficit for this year (and I’m inclined to take the over on that), it means an 8% of GDP deficit is providing in excess of 100% of the overall growth rate of around 5% (in nominal terms, meaning including inflation). For emphasis, it’s taking 8% deficits to produce 5% growth! This is every bit as insane as the monetary policies that central banks have pursued since the Great Recession. (Deficit spending—is there any other kind these days?—is considered fiscal policy.) So, as I asked several times in last week’s EVA, what price prosperity?

A key goal of the corporate tax reduction was to encourage $4 trillion of profits being repatriated back into the US. The actual numbers were $300 billion in Q1, $170 billion in Q2 and an estimated $100 billion in Q3. That’s just a little bit of a short-fall, don’t you think?

It was also supposed to cause companies to splurge on capital spending but as you can see that hasn’t happened, either.

The National Assoc. of Business Economics found in a recent survey of 116 companies that 81% hadn’t increased their capital investments as a result of the Trump tax cuts.

David Rosenberg was one of the precious few economists who recognized the housing bubble and also anticipated the economic disaster it would produce. Here’s what he wrote right before Christmas on the erupting deficits caused by Trumponomics: “The fiscal recklessness from not ensuring the tax reform would be ‘revenue neutral’, and jeopardizing the quality of the national balance sheet in the process, will be viewed by historians as one of the greatest economic mistakes the US government has ever made.”

And yet it was this massive policy error that catalyzed the last hurrah of the late, great bull market (yes, I’m calling what we are in now a bear market and not a mere correction à la 2015 and 2016). As the bill comes due for this incredible fiscal profligacy, along with the years and years of monetary incontinence, it’s most unlikely this will be the “pause that refreshes”—i.e., just a fleeting correction before the bull market resumes—as almost all Wall Street strategists expect. As I’ve noted before, every single one of these pundits has the S&P rising this year—even the most “bearish”, Morgan Stanley’s Mike Wilson. In my view, they are as likely to be disappointed in 2019 as they were in 2018, possibly much more so.

In examining the costs of these twin manifestations of government stimulus run amok, I would be remiss if I didn’t point out how the concerted efforts of central banks to inflate the value of almost everything to dangerous dimensions has fed the worldwide populist backlash. Perhaps that’s why a proposed 60% to 70% tax on the super-rich in America by a freshman congresswoman named Alexandria Ocasio-Cortez has caused such a media frenzy and even a sympathetic reaction from some most unusual quarters.

To wit, consider this quote from a recent Op-Ed in one of America’s most prestigious newspapers: “…[Ms. Ocasio-Cortez] is building a claim to be one of the most important political figures of our age.” Given that AOC, as she is known, is an avowed socialist one might think the paper that ran this was the New York Times or the San Francisco Chronicle. But, au contraire, it was the Wall Street Journal! (By the way, I’m wondering if “AOC” doesn’t also stand for All Out Class-warfare.)

The WSJ author, editor Gerard Baker, went on to state that “Faith in the American model of capitalism has been crumbling for a decade—and not just on the left.” In his article, he also cites Tucker Carlson’s recent rant against capitalism. Again, this wasn’t aired by CNN or MSNBC. It was on Fox! (Carlson’s critique of our current economic “model” is worth a listen, if you have the time, though I disagree with some of his points and I suspect most EVA readers will, too.)

Baker’s article added this for good measure, referring to AOC’s platform: “The eye-catching proposals—the Green New Deal, universal free health care and education—seem like unfundable pipe dreams, and you don’t need a slide rule to know that a 70% top marginal tax rate really isn’t going to get you there. But if you think these messages—idealized symbols rather than developed policy proposals—don’t appeal to a rising generation of voters, for whom, opinion polling tells us, capitalism is a failure, then you need to get out more.”

What’s remarkable about this emerging populist trend, both on the left and the right, is that it’s happening when economic times are still good, at least superficially. Ostensibly, Donald Trump’s election was a populist event. If so, he’s a very strange populist. Putting aside his immense wealth (though it’s probably not as immense as he likes to boast), some of his most important policy achievements, like the “yuge” corporate tax cut that is trashing our national balance sheet, are the polar opposite of what most people would consider populism.

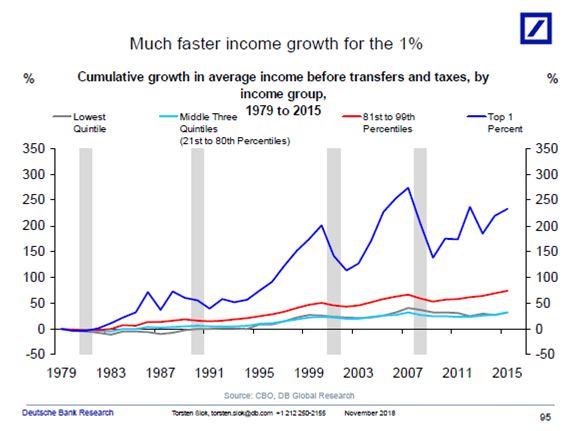

Similarly, his obsession with the stock market, at least when it was rising, is another odd fit with a true populist politician. After all, who was really benefiting when the stock market was in its final blow-off phase in 2017 and most of 2018? The hard statistics are quite clear in that regard.

Incredibly, 0.7% of the planet’s adults control 46% of the total wealth. Similarly, income has grown much faster for the top 1% than it has the rest of Americans. Thus, it’s no wonder that ordinary Americans are disaffected by this pseudo-prosperity produced by what I believe has been pseudo-capitalism.

For most of the last ten years, nearly the only policymakers pursuing the seemingly reasonable goal of getting back to the pre-Great Recession economic growth rate has been the central banks. As governments around the world appeared confused and used conflicting approaches—some employing fiscal “austerity” (which was never actually austere) and others using aggressive deficit spending—their monetary branches (the Fed, the European Central Bank, etc.) led the charge to bring the so-called wealthy nations back to their former trendline GDP growth rates.

This was despite a number of economic experts, usually outside of the central banks, who pointed out this was nearly impossible based on towering debt levels and aging work forces. The extreme indebtedness meant that additional debt brought little bang for the buck (witness what is happening in the US today). And the vast Baby Boomer generation heading into retirement meant the labor force was destined to grow slowly for years to come. Basically, 2% GDP was the new 4% but the monetary magicians refused to face up to that fact.

Yes, there have been a few spurts above 2% (or in Europe’s and Japan’s cases, up to it) but once whatever extraordinary stimulus wore off, it was back down to that formerly paltry rate. Essentially, in their maniacal pursuit of prosperity—or what they perceived prosperity to be—the central banks collectively decided the only viable approach was to pump up asset prices. In other words, they elected (not that they were; they are appointed) to make the rich richer.

Former Fed head Ben Bernanke expressly stated this in a now-legendary Washington Post Op-Ed piece in November 2010. The theory was that higher stock, bond and real estate prices would make US consumers more prone to do what they do best—consume. But there were a couple of problems with this logic.

First, the Fed’s own studies showed minimal benefit from goosing asset values. Second, since the rich own most of the assets, as clearly shown above, they were the main beneficiaries of this scheme. Yet, as all economists know, the propensity to save by the wealthy is far higher than the inclination to spend. Ergo, there was almost certain to be a negligible boost to Main Street, just as the Fed’s internal studies projected.

On the other hand, money-for-nothing policies were a lavish gift to Wall Street. But in the process, these too-clever-by-half (in Brit-speak) central bankers have birthed a bastardized form of capitalism. A tragic aspect of this is that in the next recession/bear market, politicians like AOC, and many more, are likely to throw capitalism under the bus.

Tucker Carlson, in his scathing tirade against the current economic paradigm, said that: “Libertarians are certain to view any deviation from market fundamentalism as a form of socialism but that is a lie. Socialism is a disaster. It does not work. But socialism is exactly what we are going to get and very soon unless…responsible people in government reform the American economy in a way that protects normal people.”

To his point, 80% of Americans live paycheck to paycheck and only 39% are able to cover a $1,000 unexpected expense out of savings. Northwestern Mutual Insurance has reported that, overall, Americans have on average just $84,821 in retirement savings. 21% have nothing at all saved up for their “golden years”.

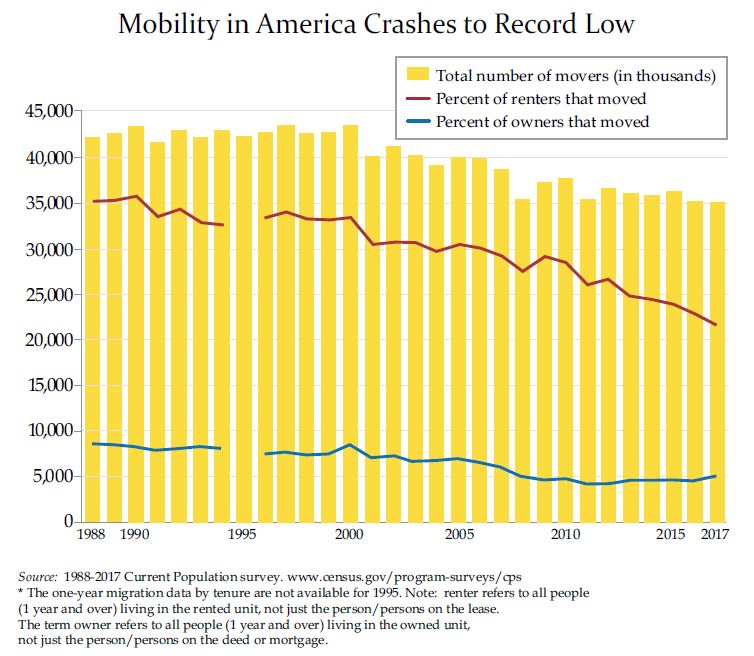

The pseudo-prosperity produced by gargantuan fiscal and monetary stimulus has also caused mobility in America to crater. In this case, I’m not referring to upward mobility, which has undoubtedly been impaired, but the mere ability to move between homes—or from a depressed region to a more prosperous one. Homeowners with very low mortgage rates are understandably reluctant to pull up stakes and move if their monthly payment is going to rise by 40% (measured from the trough in mortgage rates to the recent peak).

Of course, in the most economically vibrant cities, housing is usually prohibitively pricey for all but the most affluent first-time home buyers. This reality afflicts most “rich” countries where the housing wealth is highly concentrated in the hands of the older generations while the young are largely priced out. That’s not great for social tranquility, and the insanely low interest rates created by hyperactive central banks played a massive role in this triumph of inequity.

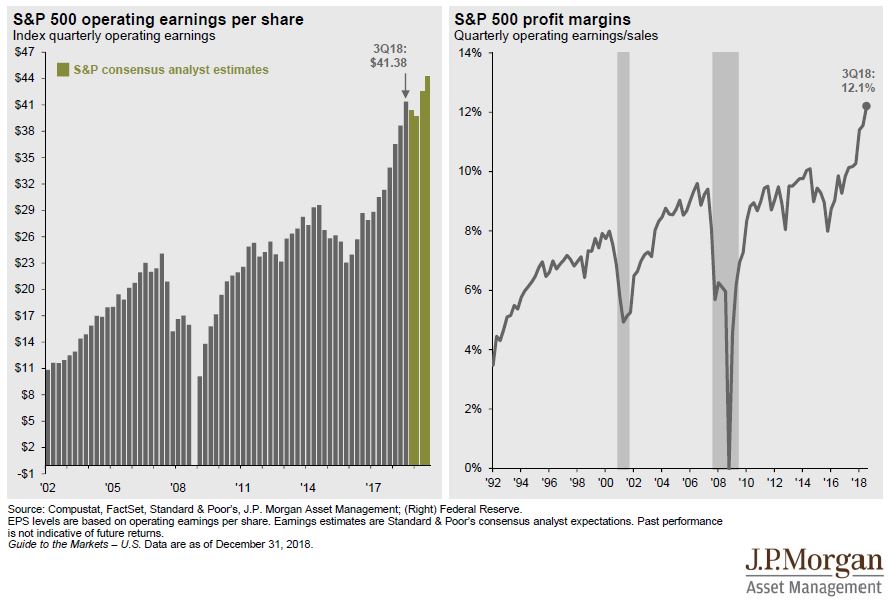

Their grand monetary experiment also encouraged companies to leverage up their balance sheets to buy-back stock with capital investments being consistently disappointing through most of this expansion, not just recently. That’s why we see charts like the one below.

This collapse of interest rates has additionally wreaked horrible havoc on nearly all pension plans, both corporate and government. It’s my conviction that in the fullness of time we will learn how much wealth was destroyed by these retirement plans as they desperately seek to make up for the eradication of return on the crucial bond side of their portfolios. The underfunding of these entities is worth a chapter unto itself—which will be hitting your inbox in the not-too-distant future.

Perhaps the average American, whoever he or she is, subliminally realizes how fragile conditions are despite the pseudo-boom caused by the central banks’ machinations. They may sense that their 401ks are soon going to turn into 201ks, as they did in early 2009, due to the creation of serial asset bubbles. Maybe that’s why there is such an undercurrent of unease and even outright panic among so many in the developed world these days. They are losing faith in capitalism but the irony is that what we’ve seen for most of the last 20 years or so has been a perverted form of it, not the real deal. Repeated and extreme government interventions have distorted normal market mechanisms, creating a series of bubbles and busts, along with consistently disappointing economic growth.

Frankly, I’ve had high hopes that current Fed chairman Jay Powell realized this sorry situation and was willing to move away from such meddlesome policies. But maybe he can’t. Perhaps it’s simply too late. Maybe the Fed is in too deep already, with its thumbprints all over the bubble-blowing machine and too afraid to be caught holding the pin that pricks the bubbles that haven’t yet popped.

In this regard, I was stunned to read in my friend Danielle DiMartino Booth’s recent newsletter (pithily titled “The Powell Punt”, a play on the “Fed Put” thesis). In it, she recounted that Mr. Powell, at a press conference with his two predecessors, recently apologetically said: “I was one who raised concerns when I first got to the Fed…they (his concerns) didn’t really kind of bear fruit…We didn’t see asset bubbles.”

Like me, Danielle thought Jay Powell would be a flashback to much stauncher Fed chairmen like William McChesny Martin and Paul Volcker. And, also like me, she is losing faith. In fact, she wrote about his quote shown above: “To this asinine observation, I rebut with: ‘Jay, speak for yourself.’” (By the way, Danielle was highlighted this week in Barron’s revered “Up And Down Wall Street” column.)

Mr. Powell’s “no asset bubble” remark is truly asinine. In last week’s EVA, there were multiple charts on display utterly rebutting this ridiculous viewpoint. But based on the above I feel compelled to run a few others.

The only reason some can claim the overall stock market is reasonably priced (again, Evergreen is finding numerous underpriced stocks but there continue to be slew of nose-bleed valued issues) is due to the above. It’s arguable that one of the biggest bubbles is in profit margins and it’s foolish in the extreme not be prepared for the inevitable crash in the same. This will, of course, immediately and most negatively affect earnings per share which have also been greatly flattered by share repurchases. (The latter are likely to decline significantly, a topic for a future “Bubble 3.0” chapter: “Bye-bye Buy-backs”.)

Because earnings and margins are highly cyclical, Evergreen prefers to use Price-to-Sales ratios rather than Price-to-Earnings (P/E) ratios, as often relayed in these pages. Sales are much less volatile and much less easy to fudge. On that latter point, the January 12th Barron’s also ran its iconic Roundtable article which yours truly has read since the mid-1980s. One of the new members is Rupal Bhansali, the chief investment officer at Ariel Investments. In her remarks, she took US corporate earnings to task: “…just as there has been a resurgence of fake news, there has been a resurgence of fake earnings. I track at least 50 countries, and the US has the worst corporate governance on that front…we keep calculating P/Es on fake earnings; We don’t incorporate legitimate expenses such as stock-option compensation and restructuring charges.”

Amen, Rupal, which is why rational investors—and Fed officials who aren’t wearing bubble-blinders—should track the Price-to-Sales ratio instead of the P/E ratio.

There are so many factoids and charts that I could display totally refuting Mr. Powell’s “no asset bubbles” viewpoint but it’s time to wrap up this EVA and the “What Price Prosperity” chapter. (For those who missed it—God forbid!—a cursory review of last week’s issue, would provide further rebuttal evidence.) But what he could have said, and been infinitely more accurate, is that there aren’t as many bubbles as there once were. That’s because some of the most spectacular, like Bitcoin and the other cryptos, have already blown apart.

Time will tell if the rest of the US stock market will join the bombed-out status of the many companies that have been popping up on our bargain-hunting radar. But when you read comments like the below from Senator Elizabeth Warren, again highlighting the escalating war on capitalism, it’s hard not to conclude time is running out—if not run out—for this once unstoppable bull market. (Note: Sen. Warren announced this proposed law back in August, but it’s garnering more attention today based on both the House’s changeover to the Democrats as well as the rising tide of anti-capitalism. In fact, one of Wall Street’s leading strategists sent this out a few days ago, indicating his concern over what these pages have warned is a looming “leftward lurch” in American politics.)

Elizabeth Warren’s Accountable Capitalism Act

“The central premise behind the bill, according to Warren, is that the “root cause of many of America’s most fundamental economic problems” is corporate devotion to “maximizing shareholder value.” In her view, a singular focus on maximizing shareholder value, as opposed to balancing other stakeholder concerns, results in a system that benefits CEOs and wealthy shareholders at the expense of workers, consumers, and the broader public interest. Under the bill, businesses with revenues in excess of $1 billion must apply for a federal charter that explicitly obligates these businesses to consider the interests of all stakeholders, including employees, customers, shareholders, the suppliers of the corporation, the local and global environment, the communities in which they operate, and any other stakeholders that may be referenced in the charter.”

As one of Evergreen’s more perceptive clients wrote us upon seeing her proposed legislation: “Holy ___!” (Evergreen is a PG-publication so we can’t run the word that rhymes with spit.) But for those investors who believe the “crashette” in nearly all financial assets late last year was a fleeting bad dream, this political trend indicates something much more ominous—and lasting. While there is almost zero chance of Sen. Warren’s Accountable Capitalism Act becoming law this year, 2020 or 2021 are different stories, especially if Sen. Warren, or one of her soulmates, should ascend to the Oval Office next year. If someday it does become the law of the land, for fully-invested bulls this outcome would be a far cry from holy and much closer to, shall we say, “spitty.”

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE *

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

** Due to recent weakness, certain BB issues look attractive.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.