“People willing to trade their freedom for temporary security deserve neither and will lose both.”

-BENJAMIN FRANKLIN

Hello darkness my old friend, I’ve come to talk with you again… The famous first line of the 1964 hit by Simon and Garfunkel The Sound of Silence feels relevant this morning.

Whether Thursday’s historic moment in European history will be remembered as a day of darkness will only be revealed with the convenient benefit of hindsight. Nevertheless, it’s put the world on the edge of its seat. Investors around the globe are coming to grips with an event that will hit many like a knockout punch no one saw coming based on pre-vote polls showing “remain” a safe bet. Internationally, many risk assets have been getting crushed following the news, with even the ever-resilient US stock market falling over 3.6%. Yet, despite steep declines in certain markets, an actual selling panic hasn’t transpired. In the four sections to follow, we, along with our partners at Gavekal, explore the implications of Britain’s momentous decision and whether this is just another hurdle to be overcome on the way to higher stock prices and, possibly, even lower interest rates.

By Anatole Kaletsky

There are moments in history when the impossible becomes inevitable without ever passing through improbable. The period after the Lehman Brothers bankruptcy was such a time. Last night’s unexpected repudiation by British voters of 40 years of European Union membership is another. The outcome of the referendum is a shock fully comparable to the Lehman collapse. Rarely, if ever, has a G7* currency fallen by -10% in a single trading session, as the pound did last night in Asia, ending up at its lowest level against the US dollar since 1985.

Whether the pound or other assets will enjoy some kind of technical rebound or plunge further, and the longer term impact on financial markets and the world economy, will depend on a host of political developments in Britain, the rest of Europe and other countries. By definition these political events will be as unpredictable as the referendum itself. Rather than trying to base a strategic response to this earthquake on purely speculative assumptions about British or European politics, trade negotiations or monetary policy, this is a time to behave tactically. As in the immediate aftermath of the Lehman bust, the priority must be to protect positions, raise cash and retain optionality to respond to whatever opportunities or disasters may emerge in the coming weeks and months.

After maintaining ever since 2009 that economic fundamentals around the world were gradually improving and therefore that more risk-on positioning was justified, I have been arguing for the past two months that 2016 was turning into a year when politics, rather than economic data or corporate results, would set the course for financial markets. This became obvious in the past few weeks as markets around the world started to follow the gyrations of British opinion polls. What never seriously occurred to me was that the populist revolt was in reality even bigger than the opinion polls suggested and would acquire enough momentum to overthrow the entire political structure of the world’s most stable and generally moderate democracy. For better or worse, that is what happened last night—and as a result all the assumptions behind the risk-on thesis must, at the very least, be temporarily suspended, and possibly turned upside down.

What this means in practice is that Charles Gave's longstanding expectation of an Ursus Magnus (major bear market) must now be considered the most likely scenario, at least for the months ahead. There are four reasons to jump straight to this dismal conclusion, even if many of my previously bullish economic and financial arguments were valid before last night’s Brexit vote.

First, the UK is a significant part of the global economy and the prospects for trade, investment, asset prices and banking stability in Britain will be gravely damaged—at least for the next few months—by the unprecedented policy uncertainty that begins this morning. While Britain’s share of global GDP may only be 2.5% to 4% (depending on market or purchasing power parity exchange rates) its weight in global finance is much greater. More importantly, as we learned from the sub-prime crisis, and again from Greece and Ireland, serious disruptions in a small part of the global economy can be magnified many times over by global interconnections—and this amplification process is much more powerful and much faster when it works through financial markets and investor expectations, and not just through the interconnections in trade and manufacturing that dominate conventional economic models. Given Britain’s very large current account deficit and the exposure of the British banking system to property values, the potential for a financial crisis and then contagion to the rest of the Europe is a clear and present danger.

Secondly, the political impact of British withdrawal on other EU countries is potentially huge but also totally unpredictable. Whether this will mean a tightening or a loosening of ties among the other EU countries or even perhaps the total breakup of the EU or the eurozone will emerge only gradually in the months ahead. But what can be said for certain is that the credibility of the EU and European Central Bank’s efforts to prevent another outbreak of the euro crisis and to keep Spain, Greece and Italy within the euro will be severely tested and questioned by the markets—and even more importantly by the citizens of all these countries.

Thirdly, the Brexit vote will surely encourage similar political upheavals in other countries. In the rest of Europe direct imitation is highly probable. In the US, the connection will be subtler but powerful nonetheless. Although US voters will not be inspired to support Donald Trump by the British example, financial markets and political pundits will be forced to take the Trump phenomenon much more seriously because expert opinion and prediction markets turned out to be so misguided in the British referendum result. That means that Trump will acquire greater credibility and financial support—and it also increases the risk that political uncertainty ahead of the presidential election will trigger a US financial crisis or recession, which in turn would give Donald Trump a much more plausible route to the White House than seemed likely 24 hours ago.

Finally, and perhaps most disturbingly, the British referendum has produced an extremely fractured and polarized society—with huge majorities for Brexit among elderly and poor voters and in relatively under-developed rural regions vehemently opposed by almost equal majorities that supported EU membership among young and highly educated voters and in the prosperous cities—not only London, but also Manchester, Bristol, Newcastle and the whole of Scotland. This extreme polarization on a national issue of existential importance would raise risks of social and political tension even in benign economic conditions. If, as is likely, Britain now suffers some kind of financial crisis and recession, the people who voted for Brexit will discover that leaving the EU has not resolved any of the economic problems and social grievances that provoked their protest against the political establishment. If this happens, public anger will presumably intensify, rather than calm down. A similar disillusionment is likely in other countries whose voters decide simply to overthrow political elites and dismiss the analysis of economic “experts”, without having any serious alternatives to put in their place.

At some point, these political and economic tensions will presumably stabilize and the popular revolts could ultimately have positive outcomes if new political leaders and economic policymakers come forward with constructive ideas for reform. That is what happened after the crisis of the 1970s with the rise of Reagan and Thatcher and in the 1930s in America under Roosevelt. But the 1930s should remind us that there could be much less benign outcomes. And even in the 1980s, the benefits for investors only became apparent after several years of big losses and extreme turbulence. When a society and an economic system is turned upside down, which is what voters have now decided to do to Britain and perhaps the whole of Europe, one can never be sure about the long-term outcome. The rational first response is to raise cash and reduce risk.

*The seven largest developed economies in the world.

By Tyler Hay

Yesterday, regardless of the financial market reaction, we all witnessed a moment of human progress. Arguably the most contentious political decision facing the developed world in decades came to a dramatic and polarizing climax without the traditional backdrop of a bloody war. I’m no expert on UK politics, but I’m not sure that’s needed to decode the ripple effect the world is waking up to following this momentous decision by the British people.

On some level, what we saw was plain and simple; a nation felt compelled to restore its rightful sovereignty and spoke up. Perhaps it is that basic, but let me pose another viewpoint: Maybe we aren’t seeing a country speaking out against immigration, trade, jobs, or national pride. Instead, perhaps this is the first tremor of a global and seismic shift. The vote that occurred in the UK was a rejection of something far larger than it appears on the surface. Today, in the US, both ends of the political spectrum are raging with desperation. Bernie Sanders has lambasted big businesses and the rich in favor of movement toward economic equality. Donald Trump—who couldn’t embody something more diametrically opposed to Sanders— has defied the odds to become the GOP’s nominee. At the moment, despite a seemingly incalculable number of political missteps and objectionable statements, Trump can’t be considered more of an underdog than the Brexit movement in Britain. How is it possible to have two men so different in their view both so embraced by voters? Perhaps Thursday’s ballot gave us a clue. The voters have come to the conclusion that choosing change—whether it’s changing economic policy, immigration, sovereignty, national security, or all of the above—it’s time to roll the dice. People are sick of the current prescriptions being administered and no matter how dangerously uncertain the path ahead maybe it cannot be worse than the one we’ve been on.

If it’s true that the developed world is bucking establishment party lines in favor of a new direction, the current volatility we saw this morning is just a sneak preview of what lies ahead. The post financial crisis recovery “guided” by the central banks has experienced a historically low amount of volatility. If investors begin to digest the idea that the world in which we live is not as stable as they’ve come to believe, it could get very ugly. Should this play out, central bankers are in an unenviable position and they have no one but themselves to blame. For years, we (and countless others) have warned that attempting to keep artificially low interest rates in place to spur economic growth was a fool’s errand.

This morning, US investors woke up to their equity accounts briefly down 5% before stabilizing. Google was swamped by people trying to figure out what “Brexit” even means. Already, 8 of the top 10 trending topics being searched on Google are related to the UK vote. As the painful reality sets in that central bank cosmetic surgery can’t mask the more structural problems facing the developed world economies, markets will face an ugly readjustment. For years, those investors who’ve suggested remaining cautious—and there are many—have appeared out of synch and too bearish as equity prices have outpaced economic fundamentals. It’s been painful at times to remain defensive, but investors need to remember that volatility is a force of nature within capital markets. It may leave, but it’s never gone. In fact, typically the longer it’s gone the more violent its return will be.

For Europe, these events will threaten the entire integrity of its political and economic union. It, along with other developed nations, will again turn to central banks looking for a cure to structural woes that need to be solved with something other than strong rhetoric and the failed experiment of zero (or negative) interest rate policies. Perhaps it will be voters, not investors, who are first to realize that central banks don’t know what they are doing. In the meantime, politicians will pounce opportunistically on the accelerating frustration of citizens who are confronting the realities of slowing economic conditions.

Certainly, no one can accurately predict whether what took place Thursday in the UK will encourage other countries to follow suit, leading to what would ultimately be a very complex and ugly disintegration of the European Union. That being said, the vote serves as a stark reminder there are many people who don’t find themselves safe or economically better off. Ignoring this group of people could prove a very costly mistake for politicians. Despite this warning, some investors—like those who’ve neglected sound portfolio practices in favor of chasing returns—will be caught with their pants down. But I have good news for Evergreen clients: We are not surprised that markets react violently to uncertainty and we’ve been preparing for it. It’s nearly impossible to pinpoint when a market panic will strike, but discipline and a proven process can turn uncertainty into opportunity. We earn our money by acting rationally when others lose their cool. We stand ready to do so once again should we see the type of mass liquidation that hit the energy sector last year spread to the broader market.

By Charles Gave

In 1988, I wrote a research piece I called at the time, “History moves again”.

The theme was simple. According to Arnold Toynbee, the world is dominated by ideas that he called “missionary ideas” and more often than not these ideas find their source in religion(s).

Our time has been dominated for the last three hundred years by three missionary ideas.

Two of the missionary ideas came from the Christian religion, one from the Muslim faith.

The UK and US took the idea of individual freedom inherent in the “Gospels” and tried to build societies where the goal was individual freedom, the political tool was Democracy, and the economic tool was free markets based on property rights.

The French, one century later took the idea that the goal to achieve in a society was “equality”, as in the first days of Christianity. The political tool to achieve this was technocracy and the economic tool was an economy directed by the government (with much less regard for the sanctity of private property rights).

As far as the Muslims were concerned, the goal of the society was to reach a state of “submission” to the will of God as expressed in the Koran, (Islam means submission), the political tool had to be a theocracy (no separation between the State, the Law and the Religion), and this meant economic and cultural stagnation through the banning of interest rates (the latter being a process the West is now rapidly emulating!).

When the Soviet Union, the real heir of the French Revolution, started to implode, I drew two conclusions in the above-referenced research piece published 18 months before the fall of the Berlin wall:

1. The demise of the French ideas was going to lead to a massive vacuum and that some kind of religious war would have to start to fill that vacuum.

2. This war was going to take place between the US and the Muslim world since freedom and submission are philosophically incompatible, while the French ideas were easily compatible with Islam.

I did not however expect two developments which took place after 1990.

The first one was that successive US governments were going to be incompetent enough to lose that war.

The second was that the proponents of the French ideas were going to try to recreate a “new and improved” Soviet-Union, using the European construction as their tool. But this is what the Trichet, Mitterrand, Delors, Chirac, and Sarkozy immediately started to work on—recreating a Soviet Union that would become the genuine philosophical opponent of the US, as it always should have been.

It became obvious that such was their goal when they created the Euro, a Procust bed (i.e, forced conformity) if I ever saw one. Since that date, I have known that it will end in failure, the same causes producing the same effects. It HAD to fail... and I never waived in that belief.

Strangely enough, this attempt to recreate a soft Soviet Union was joined by a big part of the ruling class in the US. The administrative class in Europe merged with the crony capitalists class in the US to take over the central banks, in order to gain control of the local economies.

Together, they constituted what I have called the “Davos men”, trying to rule the world through a global “informal” government. Mrs Thatcher, in her memoirs stated that this class was by far the biggest danger to our democracies—ever! As a result, we have lived since 1998, at least, under the yoke of an unholy alliance between a technocratic class in Europe and a plutocratic class in the US.

But the results of the British referendum change everything, since these elitist ideas are totally incompatible with the “ethos” of the UK or of Holland, or of Poland or of Sweden. Pretty quickly, resistances started to appear which the Brussels authorities discarded violently as they did in Greece (to make an example).

But, as I hoped, the British people have decided to regain their lost freedom and regain it they did. And in so doing they saved our culture, once more.

This is the best news that I have had since Mrs. Thatcher’s election, when she singlehandedly defeated the Marxists which were killing the UK at the time (remember Scargill, another avatar of the French Revolution?).

And from there, the evil empire started to retreat.

The fight will be long, but I have no doubt that the British people are on the right track.

As my father, a French soldier used to say: The English lose all the battles and win all the wars.

By David Hay

It may be fitting, it may be ironic, but it’s a statement of fact that yesterday’s Brexit vote was a non-violent choice by a sovereign people to break away from an unelected foreign political body. As with the Minute Men at Lexington and Concord 240 years ago, British citizens yesterday rejected what they believed to be overseas domination and oppression. (Remember, the Minute Men were British citizens, as well.) The good news, as Tyler has noted, is that it happened in this case without resorting to armed conflict.

Putting aside the profound political decision and all of its implications for the great European unification experiment, my belief is that millions of American investors are wondering today what it means to their portfolios. Seeking to answer that puts me, uncomfortably, in much the same position as all of those pundits who so confidently predicted the UK would “Bremain”. But I will attempt to do so as humbly as possible—and humility isn’t all that hard for someone who has been predicting a major shake-out in US stocks for several years.

In fairness to my guarded equity market outlook, while the S&P 500 has continued to levitate at nosebleed valuations, especially by our preferred price-to-sales metric, it has essentially gone sideways for a year and a half. That’s a long time of nothingness for what is supposed to be a full-blown bull market but there certainly has been no enduring weakness other than some brief convulsion last summer and at the start of this year. Lately, though, there has been a change underway in the US economy. Yet, even American investors have been so obsessed with Brexit in recent weeks that they have turned a blind-eye to mounting evidence that the next recession may be close at hand (note the “may”, befitting my aforementioned humility).

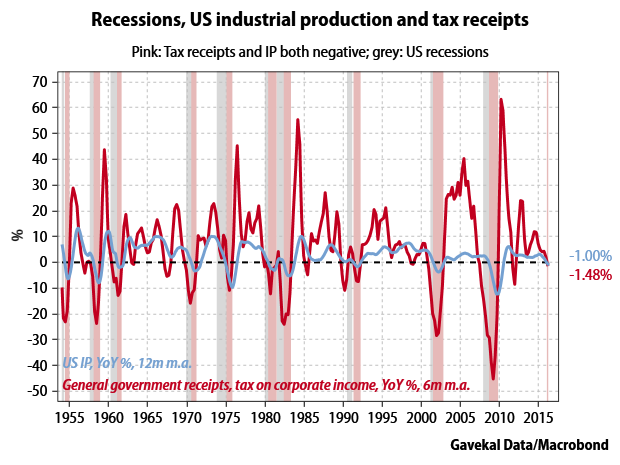

As always, there is conflicting data but, for the first time since the fall of 2007—when we were among the very few to predict a recession was looming—Evergreen is becoming a believer that our long expansion is on borrowed time. A few recent items have grabbed our attention in that regard. First, going all the way back to 1919, the US has never avoided a recession when industrial production has been in such a long-lasting downtrend. Maybe this time is different, but those words are usually very costly in the world of finance. Additionally, US corporate tax receipts are also heading quite clearly in the wrong direction.

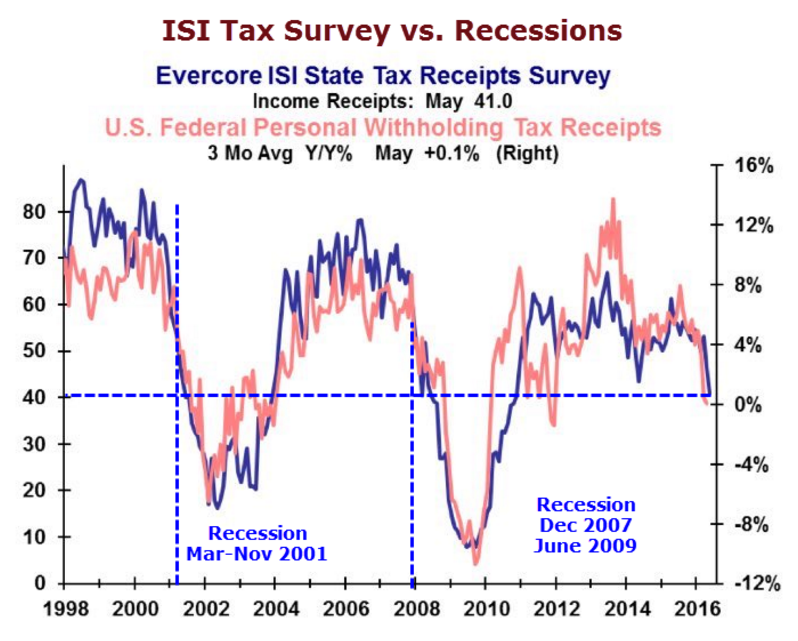

Ominously, this isn’t just a corporate phenomenon. Both state tax receipts and personal withholding are following the same southerly path. Since companies and individuals rarely cheat the IRS and other tax authorities, this strikes us as significant.

Yet, unsurprisingly, the consensus view is that the US economy isn’t close to another downturn, just as the majority opinion was overwhelmingly assuming Britain would stay in the EU. Further, Fed Chairwoman Janet Yellen just told the world this week that the odds of a recession are “quite low”. That would be comforting had the Fed’s forecasting record not been absolutely abysmal throughout this entire expansion, consistently overestimating its vitality. It’s also noteworthy that the Fed--with its PhD-stuffed staff and elaborate economic models—has accurately predicted precisely zero past recessions.

This is where Brexit might become a major domestic factor. If our economy was already starting to tip over, a global confidence shock like this is exactly what the doctor didn’t order. As always, though, there are winners in times of turmoil. One of them is very likely to be volatility, as Tyler touched on. Despite a few hiccups here and there, volatility has largely gone the way of interest rates in recent years. Per my friend and market maven extraordinaire, Ben Hunt, we haven’t seen the volatility index (VIX) over 20 for more than 2 months over the last four years. From 1996 to Sept 2003, the heart of what was the “Great Moderation”, the VIX rarely went below 20.

Whenever volatility flared up in recent years, the Fed, or one of its print-happy global peers like the Bank of Japan or the European Central Bank, would whip up a trillion or two of magic-wand money, immediately soothing investor nerves. Once calmed, they would again plow money into stocks or other so-called “risk” assets.

However, this constant mitigation of downside risk has become almost totally reliant on confidence in central banks which are the ultimate embodiment of the established political order. This is another way in which the Brexit vote may have extreme implications. If we are in the early stages of rejecting the status quo, as seems likely, central banks may be next to incur a no-confidence vote. If so, that is almost certain to play out in the financial markets. To alert and agile investors, this is actually good news, as it should create a number of chances to buy on the cheap and then trim back into rallies. Yes, that means higher portfolio turnover but we are convinced being an opportunistic buyer and seller is one of the few ways to produce respectable profits in a mostly return-free environment.

Another winner, in addition to volatility, is likely to be US government bonds, at least for the relatively near future. It’s probable America will continue to be viewed as the ultimate safe haven. With yields on German and Japanese government bonds going deeper into negative territory, the 1 ½% rate on the 10-year T-note, as miserly as that is, should fall further, elevating treasury prices even more. As longtime EVA readers know, one of the better forecasts made in these pages was the Japanization of the advanced world. This meant microscopic interest rates, sluggish growth, and relentless debt accumulation. Unfortunately, that’s exactly we’ve seen and are continuing to see, notwithstanding a stubbornly expensive US stock market.

If conditions continue to devolve globally, we believe Evergreen’s current investment strategy of being overweight securities with high cash flows paired with a similar hefty allocation to cash, treasuries and gold, remains sound. In that regard, we are encouraged by the resilient behavior of our balanced portfolios in today’s intense “risk-off” atmosphere (knock on several cords of wood!).

Certainly, the Wall Street consensus is that Brexit is just another bump on the road to bull market nirvana. But remember that timely quote from last week’s EVA by Samuel Clemens, aka, Mark Twain: “Whenever you find yourself on the side of the majority, it’s time to pause and reflect.” There are a lot of political experts, busy wiping the omelets off their faces today, who should have done considerably more pausing and reflecting.

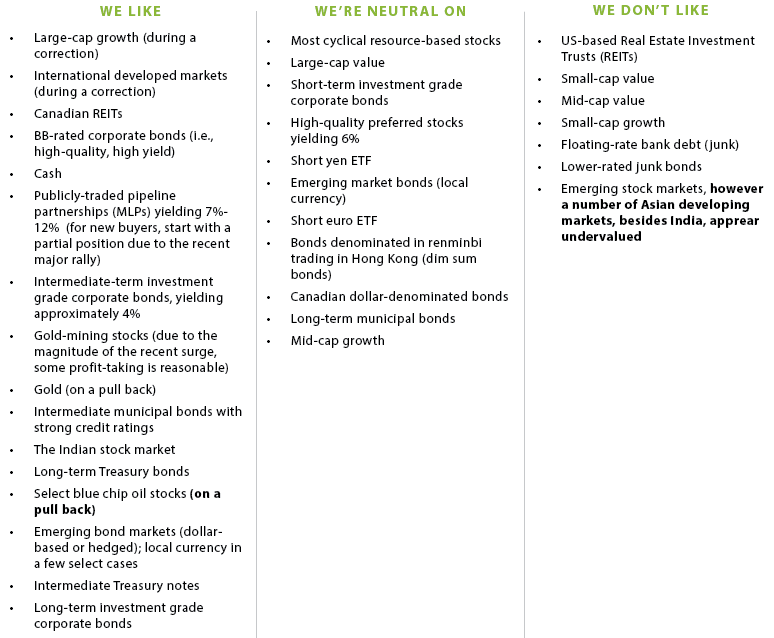

OUR LIKES AND DISLIKES

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.