“The Fed’s too savvy to let a recession happen.”

– Jim Cramer, October 2019

“Where will the money come from to buy these bonds and fund these deficits? It will almost certainly come from central banks, which will buy the debt that is produced with freshly printed money.”

– Ray Dalio, billionaire investor (and another policy mistake!)

______________________________________________________________________________________________________

At the beginning of 2018, we initiated a new EVA series titled “Bubble 3.0” with excerpts from David Hay’s upcoming book titled “Bubble 3.0: How Central Banks Created the Next Financial Crisis”.

If you are just joining us in the middle of this ongoing series, which will eventually culminate in a full-length publication, please read the prior installments in the series here:

In this month’s Bubble 3.0 missive, David discusses the differences and similarities between markets now and in 2015, questioning if we are in store for another soft-landing, as we had then, or something of the much less cushy variety.

Ned Davis has earned one of the most stellar reputations in the investment industry over his roughly 50-year career. He has built a firm that fuses stock market technical analysis (charts, volume, momentum, et al) and sound fundamental research. Ned himself was channeling the latter when he wrote: “Never in history have household financial assets been higher relative to the disposable income that must support these assets and the humongous debts behind them. If the Fed has created a financial bubble, it makes it very tricky to unwind its stimulus.”

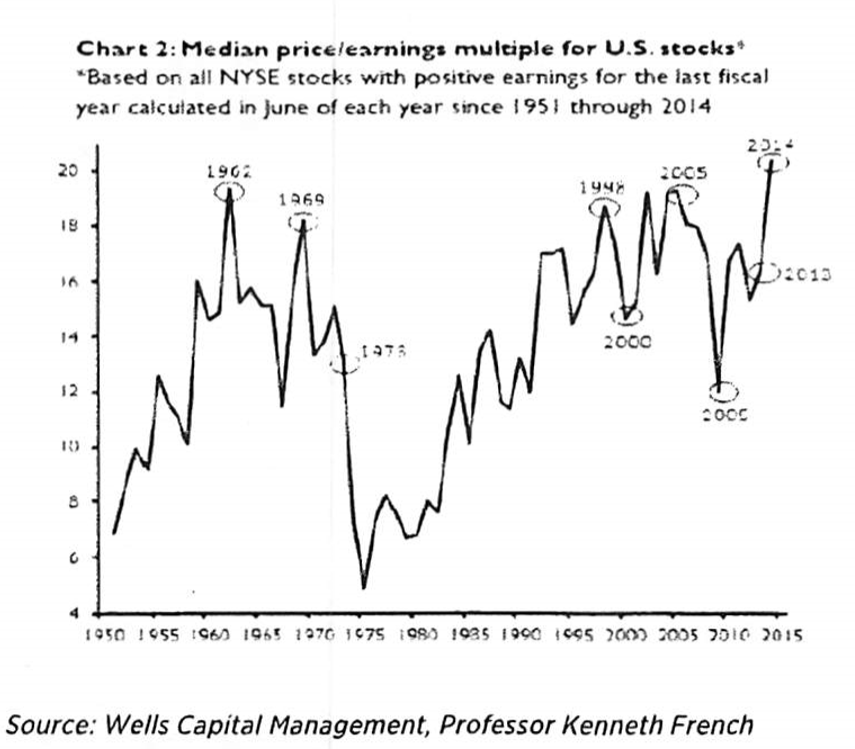

Another legendary member of the investment community is the secretive Seth Klarman. He has crafted an outstanding performance track record over the past 40 years, particularly on a risk-adjusted basis (i.e., his clients’ accounts typically hold up relatively well during panics and bear markets). He is also rumored to be a billionaire. In a letter to his investors that was leaked to the public, he wrote: “The US stock market, at 19 times trailing earnings, is overvalued on an historic basis, yet real improvement is far from certain…Weak fundamentals accompanied by expensive and rising financial markets is almost always a dangerous combination for investors.”

One element both comments have in common is that they were based on hard facts, not opinions. Another is that they were written in years past—actually, way past. In the case of Ned Davis’ assessment, it was published in October of 2014. Seth Klarman’s warning goes even further back, to June of 2013.

Far be it from me to be casting aspersions because long-time EVA readers know that this author was pointing out similar facts and concerns around the same timeframe. In fairness to all of us who were worried about both market valuations and the Fed’s artificial inflating of asset prices back five years ago, 2015 and early 2016 did turn out to be a time of market stress. The S&P 500 experienced two 12% plus corrections in the summer of 2015 and the winter of 2016. The Chinese market was absolutely pummeled, tanking by 43%. The overall emerging market index plunged 36% and the developed world stock market index, excluding the US, was slammed by 28% (both from their September 2014 highs).

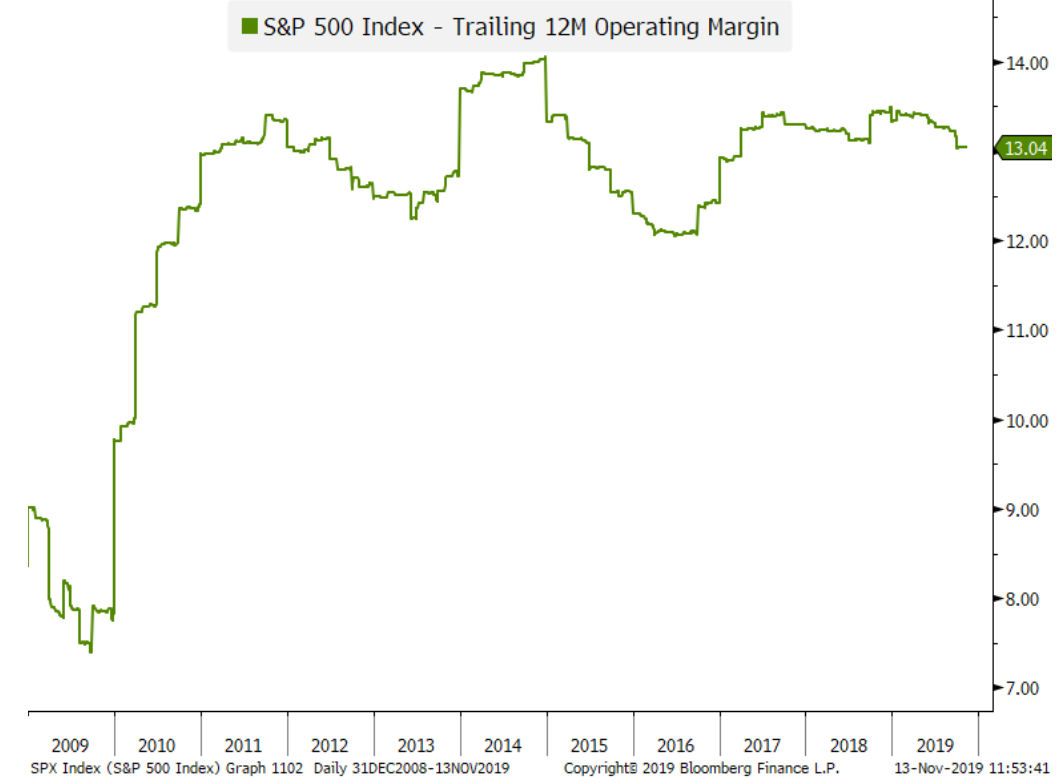

The causes of that difficult phase were, as usual, multiple. The Fed had stopped its magical money manufacturing machine known as QEs 1, 2, and 3. It was even timidly attempting to raise rates from near zero. Profits for the S&P 500 were also under pressure as were, naturally, profit margins. As we and others had warned back in 2014, the latter were unsustainably high and, indeed, they fell hard as 2015 unfolded.

Source: Bloomberg, Evergreen Gavekal

Actual S&P 500 earnings experienced an official recession in 2015, commonly defined as two consecutive quarters of contraction. As usual when conditions go south, Wall Street was blindsided. Going into 2015, the Wall Street profits forecasting community was projecting $131 of profits per S&P 500 share. They were a tad high. The final number turned out to be $109. Undoubtedly, this shortfall played a key role in the twin corrections seen that year and then again in early 2016.

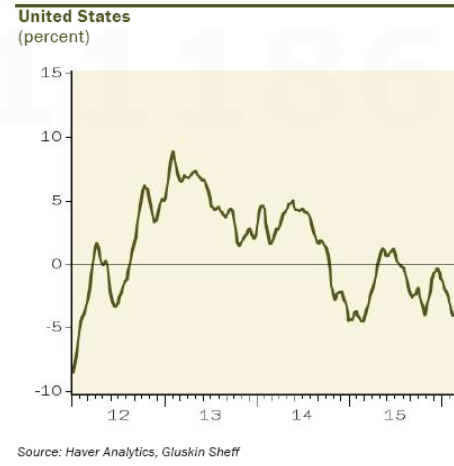

Although Wall Street was wrong-footed by the profits recession, the prestigious economic forecasting firm ECRI (one of the very few of its peers to predict the official recessions of 2001 and 2009), was not. Its Weekly Leading Index had been sounding a strident warning since late 2014.

ECRI Weekly Leading Index Growth Rate

Based on how extended the stock market was versus economic growth after the end of the Great Recession, it was reasonable to believe the US stock market had a lot more than 12% downside.

Source: Bloomberg, Evergreen Gavekal

In fact, the Financial Times’ John Authers wrote an article during the chaotic month of August 2015, titled “Mess of the Fast Few Days Suggests Entrance to True Bear Territory.” In it, he quoted Ned Davis who stated “fair value” for the S&P was around 1558, suggesting another 15% decline from a level that was already down low double-digits from where it traded earlier that summer.

Even though stocks rallied briskly from August 2015 to year-end, the first two months of 2016 brought another air-pocket. This caused Charles Gave, co-founder of our partner firm, to muse that this was probably the start of an “Ursus Major”, otherwise known as a big, bad, bear market.

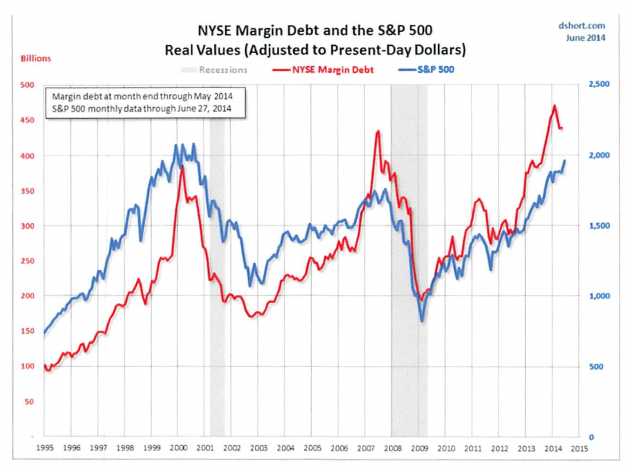

Another oversized red flag flying in those days was due to both the level of margin debt and stock valuations. Each were clearly in the danger zone, at heights that had presaged the twin market collapses of March 2000 to July 2002 and October 2007 to March 2009. Both of those definitely qualified for the “Ursus Major” designation, with the S&P getting cut in half (also in 2000 – 2002, the NASDAQ, the darling of the late 1990s, evaporated by nearly 80%).

Source: Grant Williams, TTMYGH

Source: Ned David Research

Yet, despite all of the threats and extreme overvaluation, a dual 12% correction was as bad it got. A healthy rally followed the 2016 swoon, led by energy and gold stocks. By July of 2016, the S&P was right back up at the 2015 peak. However, as the presidential election approached, stocks began to soften a bit. Even though Donald Trump was expected to lose, the possibility of him winning caused stocks to ease by almost 3% that October.

One of the great ironies in 2017 was, despite how negatively most of the investment world viewed Donald Trump, his election not only triggered a bull market extension, but it also revived the planet’s moribund economy. By the end of that year, the pervasive term being used to describe economic conditions was “synchronized global expansion”. Growth was back! Secular stagnation was out!

After a rousing 2017, stocks worldwide got off to a similarly strong start in 2018, led by the S&P which rose by 10% in just the first few weeks of the new year. The bulls were romping and stomping and vast sums were being made by those reckless clever enough to short the VIX (the Volatility Index).* In fact, one Target middle manager reportedly parlayed a few hundred thousand dollars into over $10 million by shorting the VIX.

Suddenly, in early February of last year, volatility reared its homely head. It was, as usual, downside volatility that created the almost instantaneous consternation (upside volatility never seems to bother anyone except old curmudgeons like me who worry about the eventual payback.) It only took a 10% dip to trigger what became known as Volmaggedon. ETFs (Exchange Traded Funds) that were designed to profit from selling the VIX atomized by 90% almost overnight. The Target manager lost most of his nouveau riches along with them. Almost coincidental to this trouncing of speculative behavior, the biggest bubble in human history—the one enveloping Bitcoin and the other crypto currencies—began to deflate as explosively as it had expanded.

A key trigger for this sobriety check was a sharp rise in the 10-year T-note yield to around 2 ¾%. At the time, it looked to us and others (such as the reigning King of Bonds, Jeff Gundlach) that the interest rate on the 10-year might be poised to break above 3% (as it did later last year). This potentiality began to terrify market participants.

Simultaneously, the Fed was in the midst of its first ever double-tightening. This meant that it was both raising rates AND shrinking its balance sheet (i.e., selling rather than buying government bonds; the Fed was in the process of sucking out what would be close to one trillion dollars from the financial system, partially reversing its infamous QE—quantitative easing—schemes.) These twin threats from the Fed and the bond market caused stock investors to go from pedal-to-the-metal risk-on mode to slam-the-brakes-to-the-floorboards risk-off.

Fortunately for the endless bull market, some soothing words from Jay Powell, a still strong economy, corporate profits swollen by the Trump tax cuts, and the continuation of the ultimate helium infusion—stock buy-backs—caused the flagging bull market to start romping again. By the summer of last year, the S&P made a new high. Most overseas markets, however, were not following in its hoof steps. Moreover, even in the US the number of rising stocks had shrunk considerably.

Meanwhile, the Fed, encouraged by the healthy economy and the market bounce-back, had resumed its double-tightening program. In October, Mr. Powell raised rates again and made the mistake of saying its liquidity contraction effort was on “auto-pilot”. The market was not amused, and another nose-dive promptly ensued. An additional rate-hike occurred in early December. Again, Mr. Powell’s words implied many more to come in 2019. Stocks quickly plunged another 10% during the normally cheery Holiday Season. The typical Santa Claus rally turned into a rout. By Christmas Eve, the S&P was down nearly 20% and stocks were on the eve of something much less pleasant—as in, the start of the first bear market since 2009.

*This involved the equivalent of selling an insurance policy to the buyer of the contracts that stocks would not fall significantly and collecting a hefty premium to provide this “coverage”.

The Fed’s pain tolerance was clearly exceeded. Mr. Powell immediately began to back off his tightening stance. That was good enough for a 13% rally in the first quarter of this year. Yet, as the months rolled on, it became apparent that the world economy was struggling. By late spring, there was mounting evidence that even the muscular US economy and the equally powerful Corporate America profit-making machine were misfiring. The S&P fell nearly 6 1/2% in May as fears of a global recession began to be discounted and the easy-to-win trade war intensified rather than abated.

Basically, it was beginning to look a lot like the summer of 2015 with the big difference being there wasn’t a trade war back then, which now includes some of America’s closest allies. A key similarity was that there are again dual recessions in the US industrial part of the economy and in corporate profits.

Certainly, stock markets around the world have been in rally mode over the last five weeks with cyclical stocks being among the recent stars. For example, Caterpillar shares are flying, not crawling, up 31% since its summer trough. A prime rationale for this latest bull market extension is a spreading conviction that we’re seeing a replay of 2015, i.e., a soft-landing for the economy with the recession contained in corporate profits and the manufacturing sector. The prevailing mind-set is that the all-important US consumer will not go into hunker-down mode.

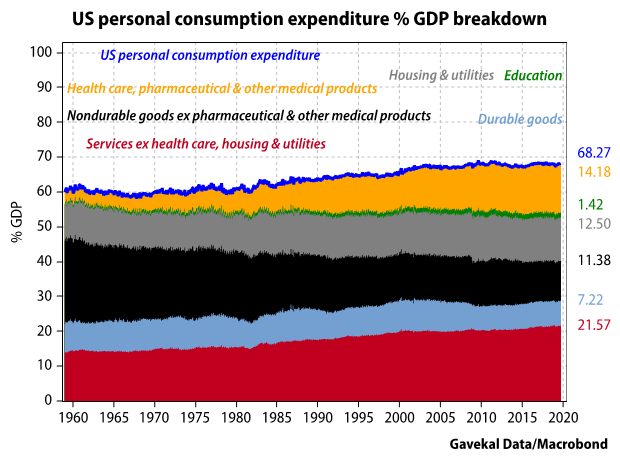

You probably hear and read all the time that consumers make up 70% of the US economy. That’s true but about 14% of that is for medical care spending which now costs about $23,000 per American family. Of that, $15,000 is paid by employers with the other $8,000 being out-of-pocket for consumers. (Note that 44% of Americans between age 18 and 64 are considered low-wage, making only $18,000 per year.) Healthcare costs tends to rise at a faster rate than inflation over time (as we all painfully know) and it is also largely immune to the economic cycle. Housing is the other biggie at about 13% of GDP. Then, there are expenditures on other essentials, such as food. Thus, perhaps around 35% of GDP, or roughly half of consumer spending, is actually the component that expands and contracts, influencing the economy.

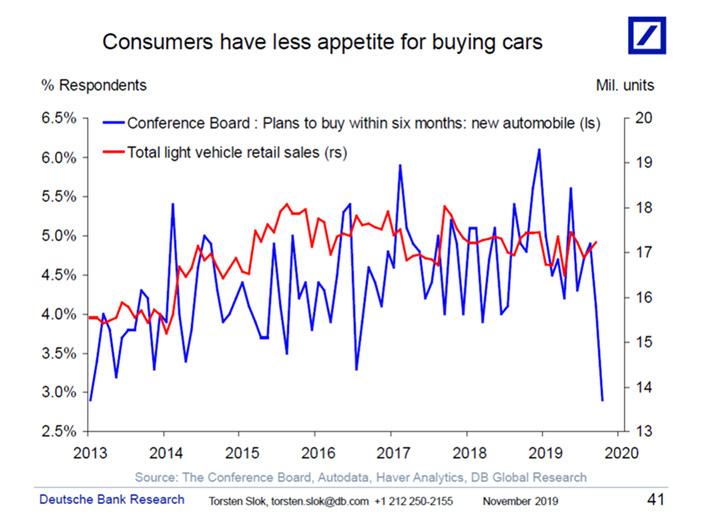

Manufacturing is only about 10% of GDP these days so it’s often dismissed as irrelevant. Yet, that is likely a mistake since there is a material multiplier effect into the service sector of the economy (think car dealers and other distributors of industrial products). On the topic of autos, there is compelling evidence that this key sub-sector may soon be in a world of hurt.

Because the thesis that we are going through a 2015-style soft-landing again is such an important topic, I want to home in on the similarities and differences to try to determine the probability of a repeat. For starters, it’s illuminating to realize that over the last 60 years there have been only three soft-landings (i.e., economic slowdowns that don’t morph into a true recession, primarily because the US consumer doesn’t cave in). Thus, odds against these “growth pauses” are fairly long.

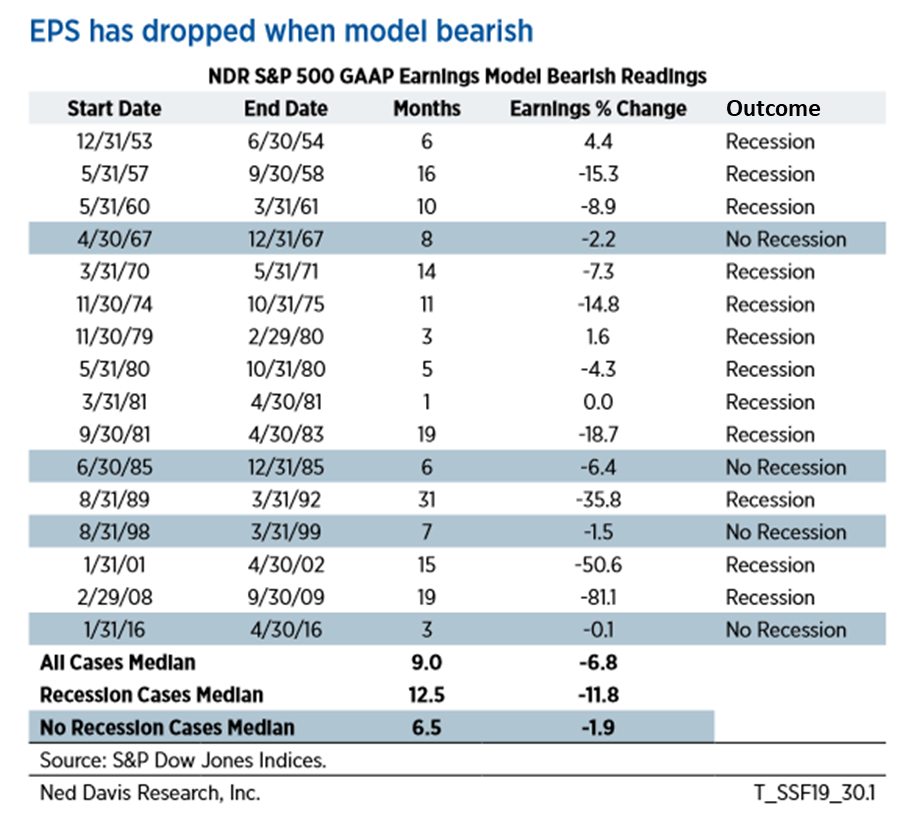

Another point to ponder—and one of the precious few observations that I haven’t “borrowed” from someone smarter than me—relates to the earnings recession part. Again, we are in the second of those in the last five years. As you can see below in the table on profit downturns from Ned Davis, there have never been two consecutive profits recessions without a full-blown recession occurring. Maybe this time is different but that doesn’t strike me as a great bet. Yet, I haven’t heard a single pundit highlight this, which is why I consider it a rare novel insight from yours truly.

At this point, I thought it might be helpful to create a little T-chart of the differences and similarities between 2015 and today. Certainly, some factors are better than they were then, particularly the ultra-vital credit spread aspect (but more on that in a bit).

To put a little flesh on the above bones, I thought it would be helpful to have some visuals for a number of these. Then, I’ll zoom in on a few that I think are particularly crucial.

A Recession Alarm Bell Stops Ringing. That Doesn’t Mean There’s No Fire.

Source: Bloomberg, Evergreen Gavekal

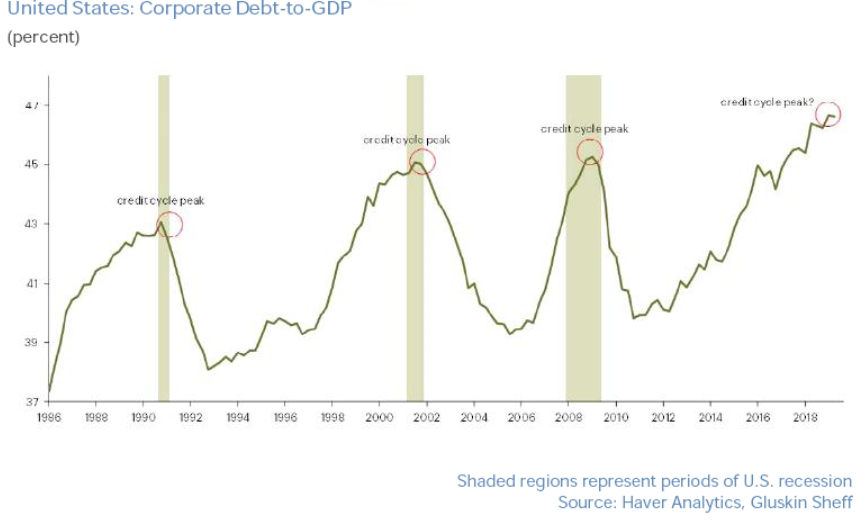

Corporate Balance Sheets are Not in Good Shape!

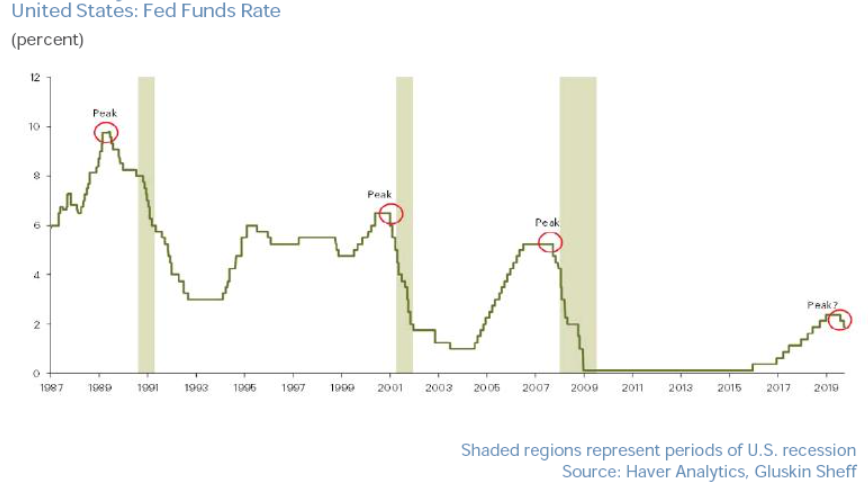

Cycle Peak Follows Fed Funds Peak

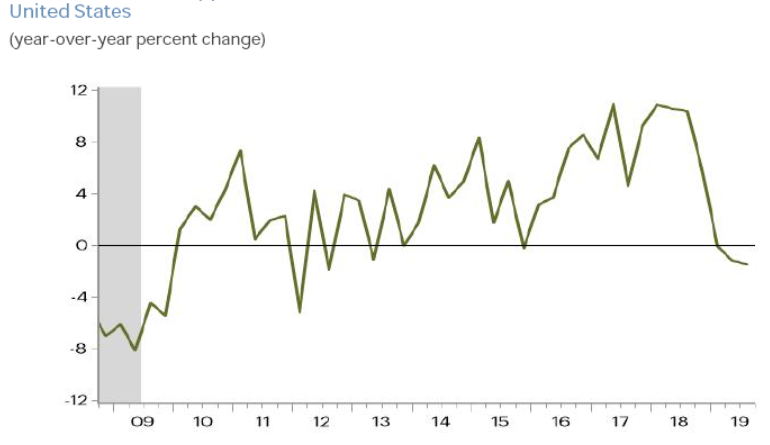

Business Applications

Non-Farm Payroll Revisions: 1st Estimate Minus Final Number

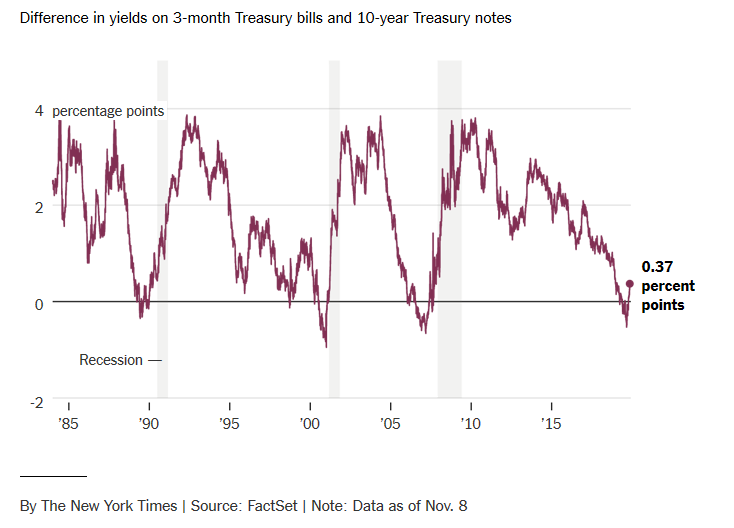

The yield curve deserves special attention for the simple reason that it has had a nearly flawless recession forecasting track record over the past 60 years. This is particularly true when the 3-month T-bill vs the 10-year T-note stayed inverted (the rate on the 3-month was higher than the rate on the 10-year) for at least four months which happened this summer. Very recently, as the soft-landing meme has gone viral, the yield curve has un-inverted. Several commentators have taken this as an all-clear signal, reinforcing the new risk-on attitude. Yet, referring again to the King of Bonds, Jeff Gundlach, the recession warning actually is amplified when an inverted curve starts to un-invert. You can see this in the NY Times chart shown above. Even going back as far as 50-years, a reversal of a sustained inversion of the 10-year/3-month spread has been a signal that a recession is coming within the next two quarters.

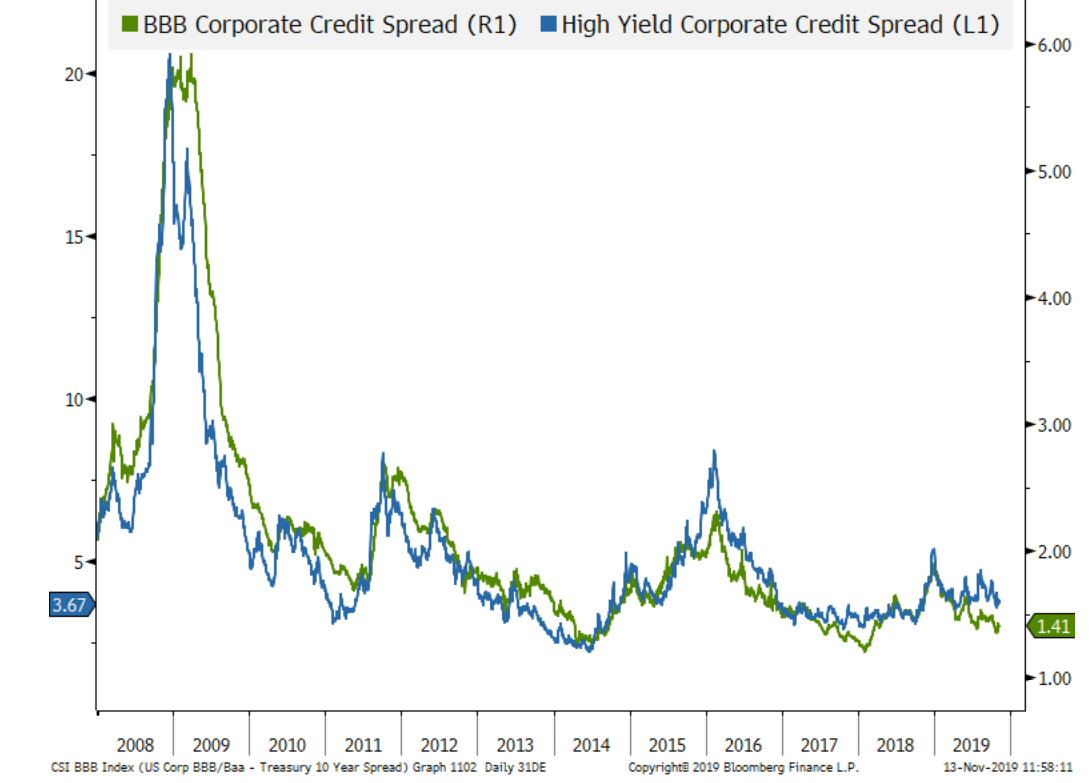

On a much more upbeat note, credit spreads remain well-behaved. These track the excess yield companies have to pay versus government securities. When this gap or spread widens, especially significantly, it is a major red flag. So far, it’s no worries other than in the riskiest parts of the corporate bond and loan market. However, it is important to be aware of the deterioration occurring right now with Collateralized Loan Obligations (CLOs).

These are packages of junk loans very similar to the Collateralized Debt Obligations (CDOs) that nearly nuked the global financial system 11 years ago. In those days, CDOs were mostly made up of junk mortgages vs corporate debt today. It’s the latter that now worries us the most per the above chart of corporate balance sheets. Moreover, these potentially unsecure securities now own over half of all leveraged loans outstanding. Almost one-third of that is rated B- or B3. This is one tenuous rung above CCC which is, in turn, one rung above default. Should there be a spike in B-minus CLOs getting downgraded to CCC, it is likely to cause serious stress because the pool of buyers willing to hold such tainted paper is quite small. A considerable amount of CLOs have been used to finance the $3.5 trillion of private equity-driven corporate takeovers so this is not just a disturbing footnote.

It’s Evergreen's view that the next blow-up is likely to be caused by an eruption in defaults on corporate debt. There are already straws, if not 2 by 4s, in the wind. Per Bloomberg in an October 23rd article: “The situation’s only getting worse (referring to CLOs) as downgrades by S&P outpace upgrades by the most since 2009. And the ratio for Moody’s isn’t far behind.” Note the part about “most since 2009”. That should be an attention grabber since 2009 was when the Great Recession was at its worst. Further, spreads on CLOs vs. high grade junk bonds (BB-rated) have recently blown out by 3% (300 bps). That’s a big deal and sign of spreading stress.

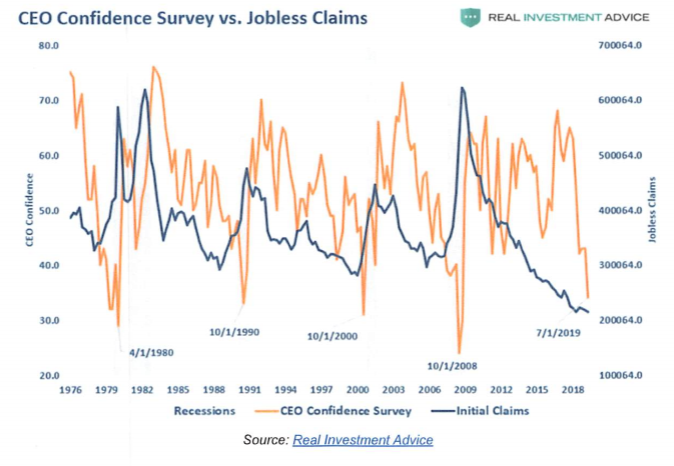

Similarly, the current subterranean level of CEO confidence is unsettling. This is because it’s these men and women who make hiring and firing decisions. Based on the above, it’s reasonable to expect there will be a lot less of the former and a lot more of the latter.

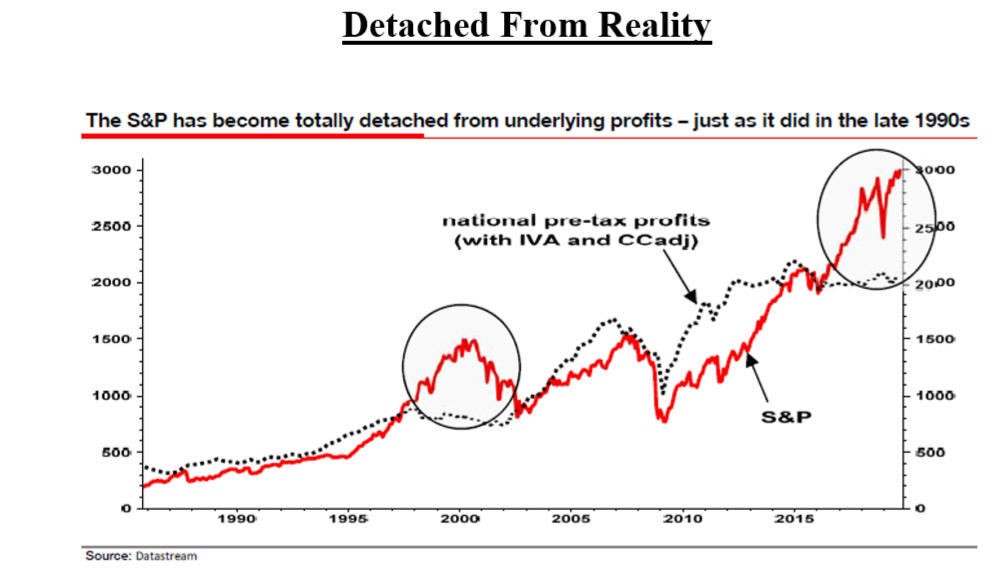

The chart from my friend Michael Lewitt of The Credit Strategist is also worthy of special inspection. Note that the last time stocks were as far above the earnings trendline as they are now was during the late 1990s right before one of the most epic market collapses in history. Again, maybe this time is different but given the weight of the foregoing evidence, is that a logical conclusion? Of course, this is not to say that the S&P can’t have one more explosive upside move. But I do worry that the further it goes up, the more painful the return to earth will be.

The chart from the estimable David Rosenberg showing past Fed rate hiking cycles is also key, in my view. This is because soft-landings typically are associated with mild, not prolonged, rate-hiking episodes (the mid-1990s were a possible exception). Remember, this was the Fed’s first ever double-tightening campaign. Some experts, like David, believe the combination of actual hikes and the sell-down of the Fed’s securities portfolio (which drained about $800 billion out of the system) was equivalent to around another 0.75% (75 basis points) of rate increases. Ergo, this was a serious tightening cycle, especially considering the low level it started at, and those have almost never led to mid-cycle growth pauses (aka, soft-landings).

The charts on new business applications and non-farm payroll downward revisions are connected. Logically, it’s not a good thing when business formations are in a serious downtrend, as they are currently. But this also impacts the official unemployment numbers that have been such a source of comfort to consumers and market strategists alike.

The connection lies in the way the Bureau of Labor Statistics (BLS) comes up with their spontaneously released jobs reports. The BLS relies heavily on something called the Birth-Death model (applying to businesses not people!) When business formations are in a normal trend, this works fine. But when new company creation is in a major bear market, as it is now, this means that the numbers reported at the time by the BLS are too high. The tell is what happens with the revisions that “true up” (or down) the original releases. As you can see in the NFP Revisions chart above, these negative revisions are definitely flashing red. By the way, there were five consecutive downward revisions to the jobs number lately, something that almost always precedes a full-blown recession. You should also keep in mind that whenever you hear unemployment is the lowest since 1969, a recession started four months after that jobless trough!

Alright, let’s pull things together. If this isn’t a repeat of 2015’s soft-landing, what is likely to happen? First, the Fed is almost certain to resume cutting its overnight rate. The current 1 ½% to 1 ¾% range is likely to be slashed close to zero. Second, the recent sharp back-up in the 10-year T-note yield to near 2% should be reversed, with its rate plunging below 1%. Thus, there are strong returns to be made on longer-term treasuries in the recession scenario.

However, I view this potential rate decline and concomitant price rise in the 10-year T-Note to be the final act of a spectacular bull extravaganza for the bond market that started in 1981 at around 14%. A recession right now, especially if it’s deep, is almost certain to catalyze the kind of extreme fiscal stimulus that an increasing number of politicians and economists are advocating.

As discussed in prior EVAs, this may entail something like MMT, or Modern Monetary Theory, essentially government spending almost without restraint. If this fiscal stimulus is combined with Fed money printing, the end result will probably be much higher inflation than we’ve seen in a very long time. It’s critical to realize the Fed is now running its digital printing presses at a QE-type rate – $60 billion a month into next year’s second quarter—even though it refuses to refer to this latest binge-print as quantitative easing. However, almost everyone else is.

Some EVA readers periodically point out that Evergreen is always bearish. But that ignores the fact we were screaming to buy almost everything in late 2008 and early 2009. It also overlooks our January 4th, 2019, EVA urging investors to buy the bombed-out areas of the stock market which, at the time, were extensive. Similarly, at this point, we want to state that we are extremely bullish—on hard assets. Having a large portion of your wealth backed by real—vs fiat or paper—assets could be the difference between maintaining your wealth in real terms versus having it substantially eroded by the extreme policies that are being bandied about in various political quarters.

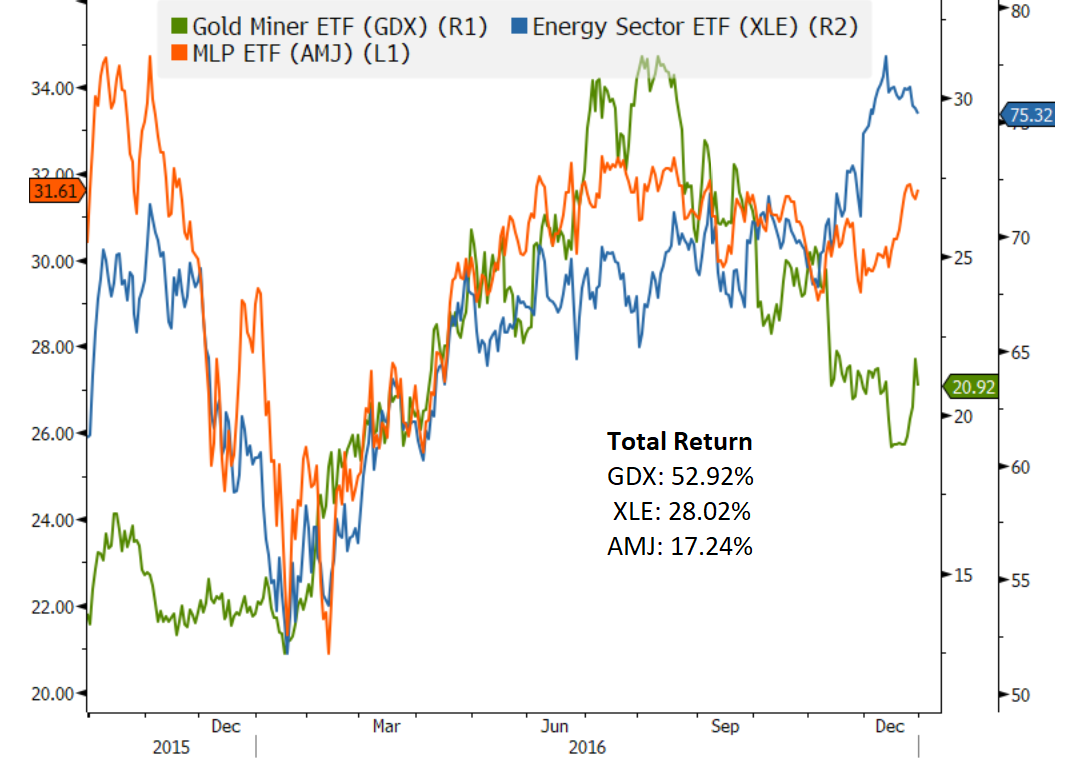

Interestingly, even if we’re on the cusp of a reprise of 2015, this would likely still be a sound strategy. The following chart shows the performance of gold and energy stocks in 2016. That would be a pretty good outcome if this really is the pause that refreshes, wouldn’t it?

Source: Bloomberg, Evergreen Gavekal

When I first entered the securities industry in 1979 (yikes!), paper assets were very cheap, and about to get cheaper, while hard assets were quite pricy and poised to get even pricier. It was a great time to be gradually shifting out of oil, gold, silver, copper, farmland, et al, and be moving into stocks and bonds. Of course, almost no one wanted to do so. Today, the exact opposite is true—buying and holding a passive balanced portfolio of US stocks and bonds—heavily tilted toward stocks these days—is assumed to be all an investor needs to do to generate superior returns. Based on the way the economy and politics are trending in the US these days, that’s likely to be just as return-crushing as bailing on stocks and bonds was forty years ago.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.