“Risk comes from not knowing what you’re doing.” -WARREN BUFFETT

“When you combine ignorance and leverage, you get some pretty interesting results.” -WARREN BUFFETT

Better to be lucky…

The clear and present danger

Premature capitulation syndrome

No bubbles, eh?

Wait ‘til next quarter.

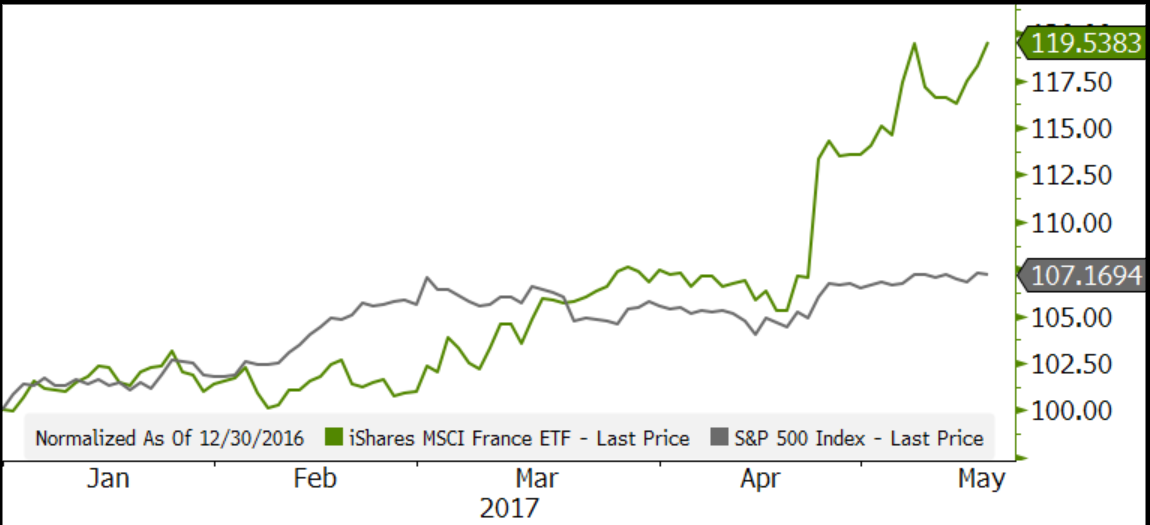

Better to be lucky... One of this year’s “Unexpected Outcomes” from our January 20th EVA was that the long-comatose French stock market would be one of the world’s better performers in 2017. My rationale was that, at the time, Francois Fillon, a credible and reform-minded candidate, was leading the polls for president of France. Moreover, considering his flawed and/or relatively obscure opponents, his election looked highly probable.

My confidence in his eventual victory didn’t wane much even when news broke of a scandal involving his family being on the government payroll for lofty salaries and minimal work (don’t those two almost always go together when it comes to working for the French government?). But subsequent news of him accepting suits worth $14,000 from a shady businessman proved too much for even the cynical French populace to tolerate. As a result, Mr. Fillon didn’t make it to the second round which saw the youthful and charismatic Emmanuel Macron decisively trounce populist firebrand Marine Le Pen.

Just 39 years old and lacking the backing of a traditional party, Mr. Macron sounds like he might embrace many of the same policy measures advocated by Mr. Fillon. His recently announced appointments of young but moderate and technocratic individuals to senior government posts would seem to validate this view.

Regardless, Mr. Macron appears intent on excising as much of the blockage from the French economy’s arteries as he possibly can. Certainly, its stock market has been performing nicely of late, up 19% and nearly tripling the S&P 500’s respectable 7% rise this year.

S&P 500 VS FRANCE ETF (JANUARY 2017 – PRESENT)

Despite his charm and eloquence, Mr. Macron will have his hands full trying to create a parliamentary majority, not to mention dealing with France’s notoriously belligerent labor unions which fight tooth and nail—or should that be hammer and sickle?—against even modest reforms. His presidency could turn out like the once-hopeful administration of Matteo Renzi in Italy (another boyish and engaging politician, but one who was unable to overcome his country’s entrenched special interests).

However, my dear friend and colleague Louis Gave, a native of France, believes that its economy is a coiled spring, ready to vault to life once some shackles are removed. To most Americans, this seems unlikely but there are already signs the capitalist spirit is stirring in a country where the government’s share of total GDP is nearly 60%. We believe France will “de-socialize” simply because it has no other choice.

The clear and present danger. It seems that the threat of North Korea deploying a nuclear bomb has drawn on-and-on for decades (CNN has a full timeline on North Korea’s nuclear ambitions if you care to look). While the threat has been present for some time, the fear of an imminent attack has picked up steam in recent months. Despite the increased focus on North Korea, it’s become obvious to me that most people are still oblivious to one of the biggest threats this totalitarian dictatorship poses to the US (not to mention the world).

The younger members of our investment team—which are, actually, all of them—have grown weary of hearing me drone on about the grave risks posed by an “EMP”. For those of you not familiar with this little initialism, it stands for Electromagnetic Pulse.

While EMPs can be caused by natural phenomenon, namely massive solar flares, scientists and military experts worry that one could also be generated through the detonation of a nuclear device. Late last month, the rogue state of North Korea launched what was widely thought to be another failure in a long list of missile tests. But, as with many other similar “failures”, the medium-range missile blew up at a height of 72 kilometers (or 45 miles) above the Earth. Coincidentally—or not—this is precisely the altitude that is believed to be optimal for taking out the unprotected electric grid, which is most of it.

If a detonated EMP had sufficient intensity, it could potentially “fry the grid”, essentially short-circuiting the electrical infrastructure. This would, along with other catastrophic occurrences, shut down the internet. It doesn’t take a tech savant to realize the economic devastation this would cause.

Billionaire hedge fund operator Paul Singer of Elliott Management Corporation has been among those warning of this for years. More recently, in a short letter buried on page A14 of the March 17th Wall Street Journal, Karna Small Bodman, Former Senior Director of the Reagan administration’s National Security Council, outlined her concerns. The letter was titled Missiles Pose Dire Threat to Electricity Grid and, in it, she quotes the former head of the US Ballistic Missile Defense system who told her that in the event of a successful nuclear detonation in the upper atmosphere: “We would have no communications, computers, cell phones, refrigeration, sanitation, transportation…it would set us back to the year 1910.”

Late last month, the Executive Director of the Task Force on National and Homeland Security, and Chief of Staff of the Congressional EMP Commission, Dr. Peter Vincent Pry, made the point that North Korea’s missile mishaps are anything but failures; rather, they are successful practice exercises based on a former Soviet strategy from the Cold War era.

Even South Korean officials have warned that the world is failing to appreciate the significance of the these tests. On April 30th, officials told both The Korea Times and YTN TV that these were not failures, but rather tests to “develop a nuclear weapon different from existing ones.”

Those downplaying the risk point to Starfish Prime, a 1962 mission carried out by the United States over the Pacific Ocean, as a prime (no pun intended) example of this being an overblown possibility. In that mission, a 1.45-megaton hydrogen bomb was detonated 250 miles above Earth with approximately 100 times more power than the atomic bomb dropped on Hiroshima in 1945.

The result was significant but not devastating (though 45 miles above earth is a lot different than 250 miles!). Almost immediately after the detonation, streetlights in Hawaii went out, burglar alarms went off, and telephone services shut down. Additionally, six satellites fell victim to radiation emitted from the blast. In response, the Soviets tested their own high-altitude thermonuclear device that year, which further impacted satellites in orbit.

If all of this sounds like the storyline of an action movie to you, you’re not alone. The plot of the 1995 James Bond film GoldenEye, strikes an eerily similar resemblance.

But to dismiss this as fiction (or insignificant) would be a mistake.

As North Korea conducts more “failed” tests, it will learn more about its ability to deploy and detonate high-altitude weapons with potentially dire implications for our infrastructure and economy. The result of a nuclear-armed North Korea might not be a cloud of smoke in the Pacific; rather, it might be a dazzling display of lights in the sky followed by complete darkness.

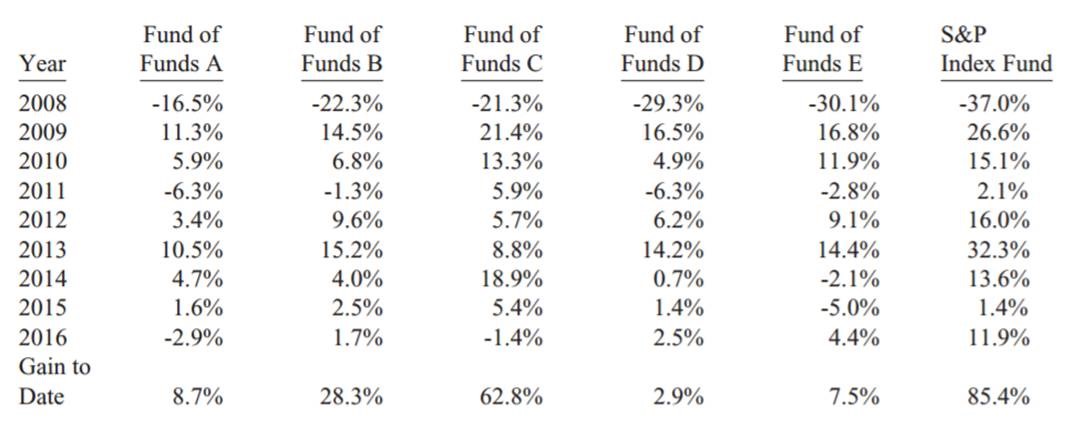

Premature capitulation syndrome. Undoubtedly, many EVA readers are familiar with the million-dollar wager Warren Buffett made nearly 10 years ago with a hedge fund true-believer, Ted Seides. The winner agreed in advance to donate the proceeds to charity. It’s certainly fortunate for Mr. Buffett that it looks unlikely he’ll need to pony up the million smackers because, at last count, he’s down to his final $73 billion!

The terms of the bet were that Mr. Seides could pick five hedge funds and Mr. Buffett would take a plain-Jane, low-cost S&P 500 index fund. The Oracle of Omaha’s prediction was that the S&P would outperform the average returns of these “alternative” investment vehicles.

As of December 31st, 2016, the S&P index has over a 20% lead on the BEST performing hedge fund selected by Mr. Seides. This seemingly insurmountable advantage with just eight months to go caused Mr. Seides to throw in the towel. Based on the modest returns of his weaker performing funds, which, as you can see in the table below, are much further behind the S&P, I can’t say I blame him. (However, if Mr. Buffett was interested, I’d be willing to make a sizeable wager that our typical Evergreen balanced portfolio will beat the S&P over the next 3, 5, and, even 10 years.)

Regular EVA readers realize that we’re no fans of hedge funds and their outrageous lavish fees. But we worry that the results of this contest, which will certainly be widely publicized once it officially ends, may cause investors to ignore the benefits of thoughtful investing, with an eye toward downside protection, as well as international diversification. After so many years of steady and above average S&P 500 returns, it’s easy to conclude all you need to do is put your money in an index fund, sit back, and collect the profits. Yet even the Oracle himself has said that successful investing is simple but it’s not easy. But more on that in a moment…

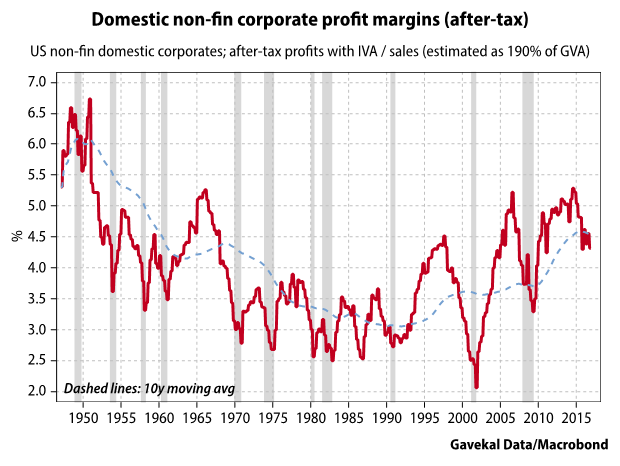

In a similar vein, the nearly mythic Jeremy Grantham, of Boston money management colossus GMO, so often quoted in these pages, recently wrote an essay titled “This Time is Different”. In it, he laments that a value investor’s best friend—mean reversion—may have gone AWOL. One important example of this, in Mr. Grantham’s view, pertains to profit margins. He has noted for years that: “Profit margins are probably one of the most mean-reverting series in finance, and if profit margins do not mean revert, then something has gone badly wrong with capitalism.”

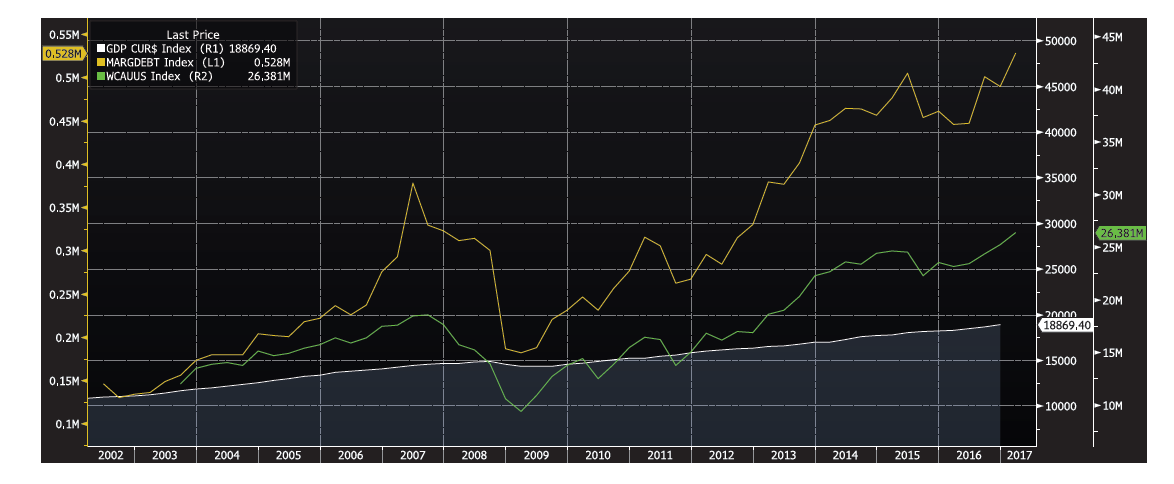

Don’t let the term “mean reversion” throw you for a loop. It’s just geek-speak for returning to normal or, loosely, what goes up must come down. Say, for example, if you were to plot a line of the economy’s growth over time versus the stock market’s price chart over the same period, you would see that the two are closely linked. Yet, there are many instances when the stock market soars well above the economy’s trend-line, only to fall back to it and, during nasty bear markets, even below. (The behavior of margin debt is another example of this and should further put rational investors on-guard.)

MARGIN DEBT (YELLOW) AND STOCK PRICES (GREEN)

OUTPACE GDP (WHITE) FROM 2002-2017

As you can see below, profit margins are cyclical, as well, even if their trend varies. Corporate America’s profitability entered a long decline after the USA’s golden years of the 1950s and 1960s, when we were rebuilding the world post-WWII. Margins bounced around at relatively depressed levels from 1970 to 1990 but, interestingly, without a lot of volatility. Yet, even then, margins would rise during expansions, flatten out, and, eventually begin to fall. During that two-decade stretch, profit margins tended to bottom around where they had in past recessions. They would also typically peak out near where they had during prior growth cycles, as you can see below…

But, things began to change about 25 years ago. Margins started to make higher highs and, for the most part higher lows (with the profits crash in 2001 – 2002 due to the tech bust being an exception). Thus, the dotted blue line in the chart above, showing the long-term trend, began to turn up and its slope has actually increased in recent years, which is likely a leading cause behind Mr. Grantham’s exasperation. This phenomenon has almost certainly been a major factor in the market trading at far higher valuations than it did in the years prior to 1990.

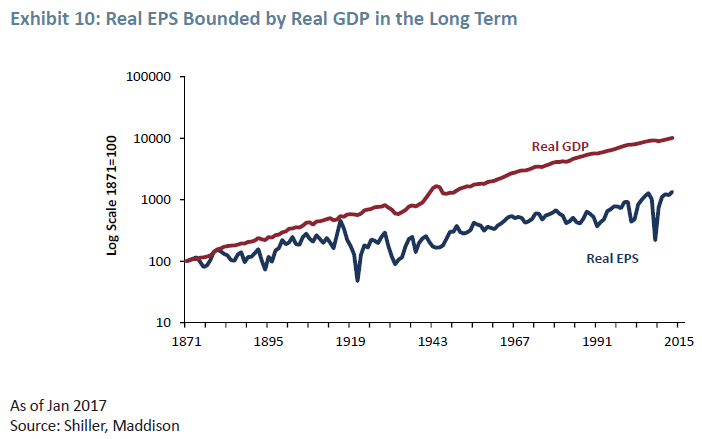

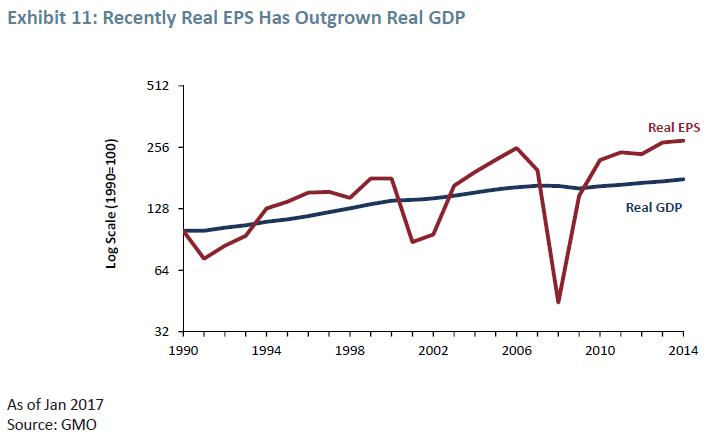

The unusual nature of the last 25 years is also demonstrated by looking at real, or inflation-adjusted, earnings during that timeframe versus history. Whereas the economy tended to grow at a faster rate than the stock market prior to 1990, since then the inverse has been true: stocks have grown faster than the economy. Here are a couple of charts showing this trend.

REAL EPS BOUNDED BY REAL GDP IN THE LONG TERM (1871-2015)

RECENTLY REAL EPS HAS OUTGROWN REAL GDP (1990-2014)

Earnings growing faster than the economy is highly unusual since this measure of profits only considers publicly-traded enterprises; in other words, privately-held companies are excluded and they play a considerable part in economic growth. It’s much more typical—and logical—for earnings to increase less than the economy does for that and other reasons. So once again it’s reasonable to wonder if the economic rules that applied for decades have been repealed or if it’s just a case of a very delayed mean-reversion looming up ahead. Regardless, for now, there’s scant evidence the S&P 500’s profitability up-trend is approaching its sell-by date.

To be candid, this is why Evergreen’s preferred stock market valuation metric of price-to-sales needs to be recalibrated. Because each unit of sales is now more profitable, it’s reasonable to assume that the price/sales ratio deserves to be higher than in the past. That’s a valid point that we readily concede but with the median price-to-revenues ratio now 47% above the epic ultimate bubble peak of early 2000, we’d also say this rising trend is fully priced in…and then some.

Then there is the issue that Mr. Grantham brought up in his quote, “…something has gone badly wrong with capitalism.” We would suggest that the rise of populist candidates and even elected leaders, such as Donald Trump, indicates it has. There are several indicators that reveal this, including that the planet’s leading central banks feel they need to inflate asset prices to keep consumers from sitting on their wallets. This, in turn has had the undesirable side effect of aggravating the wealth divide, as has been extensively documented.

Another factor in this chasm between haves and have nots is the trend in the share of the economy that accrues to businesses versus workers. It has been heavily skewed in favor of Corporate America but lately there’s been a shift back toward labor. That’s good news for Main Street but not such a pleasant development for Wall Street and those still lusty profit margins mentioned above.

Maybe folks like Messrs. Seides and Grantham are waving the white flag just when mean reversion is poised to make a dramatic, if long-delayed, reappearance.

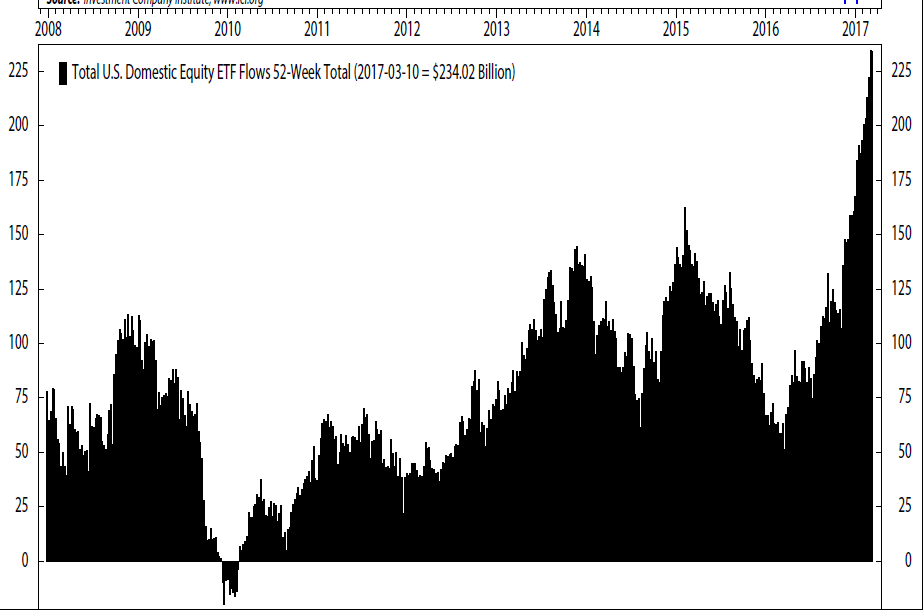

No bubbles, eh? For months now, Evergreen has conceded that the stock market’s trend is clearly up, mostly due to the soaring “animal spirits” post the US presidential election. But that doesn’t mean we are doing a Seides/Grantham and rationalizing today’s valuations which remain laced with copious amounts of helium.

We do allow that many formerly bloated bubbles like Miami condos and Manhattan penthouses have had a close encounter of the pin-prick kind. However, plenty of other gaseous orbs continue to grace the financial market’s firmament.

Let’s just do a quick recap of a few items that are directly or indirectly reflective of gravity-free asset prices:

TOTAL US DOMESTIC EQUITY ETF FLOWS (2008-2017)

There are many other indications of speculative-mania running amok we could cite– including margin debt as a percent of GDP now exceeding early 2000 (the apex of the biggest stock market bubble in US history) – but we think you get the idea. To paraphrase a former Supreme Court Justice referring to pornography, I might not be able to define a bubble but I sure can tell one when I see it…or, in this case, them.

The plural part is important because it’s fair to say that there isn’t one grotesquely distended bubble these days, as was the case with tech stocks in the late 1990s or housing circa 2006. But maybe it’s even worse to have a series of investment areas (aka, asset classes) priced as if there is an endless supply of greater fools.

It’s been my experience in 38 years plying the investment trade that, in bull markets, all investors seem to care about is relative performance. In other words, is he or she keeping up with the S&P (or whatever else is the best behaving major index)? This gets back to my worries about the Buffett/Seides contest bestowing a misleading air of infallibility to S&P index funds. Remember that since the peak of the great market mania at the end of the Roaring ‘90s, the S&P 500 has returned a mere 4.8% per year. Over that timeframe, the Credit Suisse Hedge Fund Index has actually outperformed it, by about 1% per year, or roughly 159% versus 127%, cumulatively. And far more relevant to Evergreen’s investment process, the MLP index has produced a cumulative return of 733% or 13% annually, despite still being down 40% from its 2014 peak!

On the other hand, in bear markets, the only thing that matters to investors is absolute performance (i.e., am I making or losing money?). This is what Evergreen calls the “floating benchmark syndrome” – comparing to a prominent equity index during frothy times and then comparing to cash or CDs during inevitable bust phases. That mentality often leads back to another version of the premature capitulation syndrome, where terrified investors bail out at, or near, a bear market bottom.

The above-documented mad dash into ETFs—which are, by definition, fully invested in whatever their mandate is, like small cap stocks – is setting the stage for a major rediscovery of the importance of absolute return investing. But, as mentioned above, that epiphany often happens at the worst possible time instead of when it should – during euphoric phases, even if that means getting off the bull bandwagon prematurely. Circling back to Buffett once again, a wise investor should be greedy when others are fearful, and vice versa, but that’s extremely contrary to human nature.

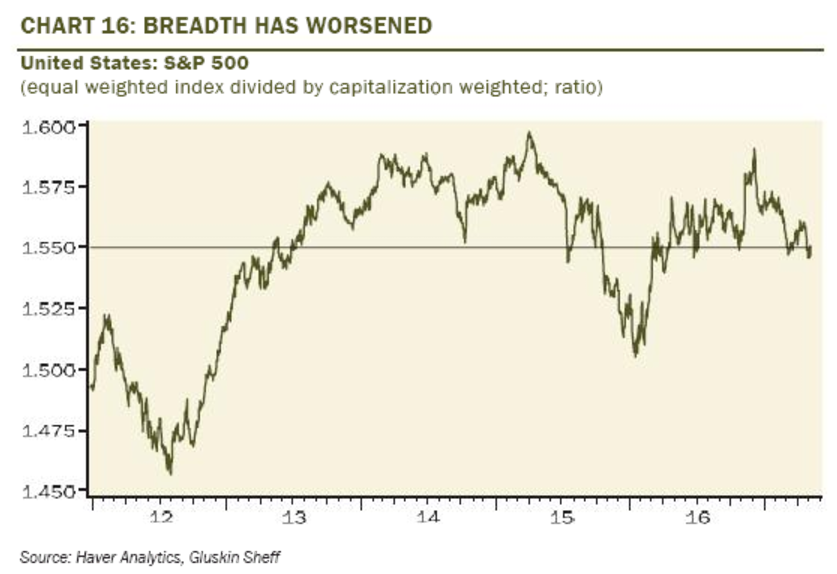

Meanwhile, to our eyes, the market’s up-trend is looking less and less impressive. Developments such as the shrinking number of stocks that are powering the market’s advance (only six companies have been responsible for 40% of this year’s gains in the S&P), a level of complacency that implies investors are on heavy doses of Xanax (the volatility index is at half of its normal level), and tremors out of China (including an inverted yield curve), are increasingly reminding us of the lead-up to the fear-wracked summer of 2015.

S&P 500: EQUAL WEIGHTED INDEX DIVIDED BY CAPITALIZATION WEIGHTED, RATIO

Consequently, we believe the now mostly forgotten Wall Street axiom of “sell in May and go away” is likely to be reaffirmed this summer in a big and painful way. Maybe it’s time to at least “sell some in May and go pray”? (In the latter case that we only have a 2015-like swoon and not something far more sinister.)

Wait ‘til next quarter. This is a refrain we’ve all heard for so long regarding hopes for better future economic and earnings growth it’s almost like those N. Korean missile warnings. Yet, to be fair to the optimists, the first quarter of this year looks to have been one of the strongest in recent memory for corporate profits, despite an economy that grew less than 1%. On a year-over-year basis, earnings are likely to be up in low double-digits. Naturally, that is being loudly trumpeted (though, surprisingly, not by our Trumpeter-in-chief) among those whose bonuses are heavily dependent on the continuation of this ancient bull market.

As you might expect, there are some “buts” involved with this superficially sunny scenario. For one thing, the big catalyst for this bump has been the profits recovery in the energy sector. Recall that in the first quarter of 2016, which our most recent interval is being compared against, we saw oil fall below $30 per barrel. The bluest chip oil and gas companies were reporting profit implosions while the less blessed were disclosing huge losses. And mass bankruptcies have taken out some 250 small- and mid-sized energy-related entities. (Ironically, the worst performing sector in 2017 from a stock performance standpoint has been energy, likely a function of its over-popularity per our warning earlier this year.)

Looking out to the rest of the year, stock market bulls are calling for more of the same—continuing double digit earnings gains. They are using this to justify stocks trading at levels rivaled only by a few of the priciest episodes in market history.

Of course, they could be right. However, with the aforementioned profit margin downturn, due in part to higher labor costs, combined with an increasingly late-stage economic cycle, they also might be wrong. A key reason they could be in error—as they were in 2000 and 2007—is the full-blown Fed tightening cycle that is clearly underway per our March 17th Fed Storm Rising EVA (click here to access).

But, putting aside the Fed for a moment, how truly “late-stage” is the US economy? Members of our investment team have reminded me that I’ve been pointing this out for some time… and they are right. But my response to that is, while I’ve said it’s late innings, I haven’t said it was the ninth inning – as in forecasting an imminent recession.

Admittedly, though, I did move to high-alert last summer and early fall when several advanced indicators were looking ominous. Love him or hate him, Donald Trump wiped away those fears literally overnight. As I’ve noted in simply stating the obvious – something I excel at – the global confidence surge after his election was breathtaking.

Yet we also made the repeated point that confidence surveys were racing way ahead of economic reality, setting the stage for disappointment. We even warned that Trumphoria might someday morph into Trumphobia. Perhaps it’s not to that point yet, but Mr. Trump is working hard at getting there. At least it’s fair to say we’re at the Trumpapathy phase. Have you noticed that his proclamations of things like “phenomenal tax plans” no longer move the market?

Thus, it seems the market’s love affair with The Donald has cooled considerably. But, the bulls have wasted no time in justifying today’s obese valuations with the earnings revival mentioned above. Yet, in addition to the irony of the once again out of favor energy sector leading this recovery, there is also the oddity of companies with the greatest foreign exposure being in the profits vanguard.

The Wall Street Journal reported last week that the US companies with the most overseas sales are seeing 15% profit gains versus 6.8% for the more domestically-focused (also on a year-over-year basis). This is exactly the opposite of what bulls were saying earlier in the year when it was supposed to be the small-cap, US-centric firms that were allegedly in the sweet spot.

Since this EVA is getting almost as long in the tooth as the current economic expansion, I’m just going to give a you few economic nuggets to chew on:

S&P 500 AIR FREIGHT AND LOGISTICS

S&P 500 MINING AND METALS

US CORE GOODS CPI

The bottom-line is if Corporate America’s bottom-line is going to be hitting those double-digit targets, it’s going to be despite some serious headwinds. In fact, David Rosenberg is musing that the US may already be in recession. It doesn’t feel that way to us—yet. But with the Fed intent on repeatedly raising rates in what is clearly a tired, if not exhausted, economy, our views may change sooner rather than later.

Recessions, like bear markets, still happen, no matter how badly Wall Street doesn’t want them to. Perhaps Wednesday’s sudden meltdown is a preview of what may lie ahead this summer. If so, well-prepared investors might soon have a flashback to Buffett’s experience in the mid-1970s when he famously said he felt like an oversexed man in a house of ill-repute. Yes, he was a bit more risqué in those days but buying into that grueling bear market—and others after it—is why he’s got those $73 billion bucks today.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.