“The planned US restrictions on Chinese investments in ‘industrially significant technology’ are in large part fueled by American concerns about ‘Made in China 2025,’ Beijing’s plan to boost industries like robotics, electric cars and aerospace with the aim of becoming a global leader in those areas.”

–JETHRO MULLEN, CNN

In previous EVAs, we have discussed the ongoing trade tensions between China and the United States in detail. For those that might have missed our previous missives on the hot topic, here are links to those articles:

In our second attempt at a rundown on the trade war, we highlighted briefly that the Trump administration is working hard to resolve two things through this strategic dispute: reducing bilateral trade deficits through tariffs and limiting China’s access to IP and technology. While most of the ongoing national coverage is focused on the former, this week’s EVA from Dan Wang at Gavekal takes aim at the latter.

Specifically, Dan outlines how the Committee on Foreign Investment in the United States (CFIUS) and new US policy in the form of the Foreign Investment Risk Review and Modernization Act (FIRRMA) target Chinese investment in American companies. While FIRRMA was only recently inked into law on August 13th, the passage will increase the scope of CFIUS, which will likely lead to even more attention and blocked attempts on foreign investment deals.

The question is whether these steps will be effective in limiting Chinese access to valuable IP that could enhance its technological capability for military and business purposes, or whether loopholes and workarounds will limit the impact of CFIUS and FIRRMA. Only time will tell, but there is no questioning that the current administration is keen on clogging China’s pipeline to US tech.

Michael Johnston

Tech Contributor

To contact Michael, email:

mjohnston@evergreengavekal.com

CLOGGING CHINA'S CASH PIPELINE TO SILICON VALLEY

By Dan Wang

Most coverage of the mounting US-China strategic tensions has focused on tariff threats. Equally significant are moves by the US to choke off Chinese investments in the US technology sector. These moves are part of a strategy to ensure that China can’t catch up to the US in critical technology fields by buying, or buying into, cutting-edge American firms.

Alarm bells began ringing in 2014, when Chinese investors started to surge into venture-capital funding rounds in Silicon Valley. In 2016 the total annual Chinese direct investment of all kinds in the US tripled to US$46bn. The targets of Chinese acquirers were varied, but a good chunk of that money went into technology firms. Some observers believe the wave of spending was prompted by a mandate under Beijing’s Made in China 2025 industrial policy for Chinese firms to boost their technological capacity through foreign acquisitions.

The first response to this wave was an increase in the number of China-funded deals blocked by the Committee on Foreign Investment in the United States, the interagency government panel that vets inbound direct investments for national security concerns. Two new laws enacted this month have greatly strengthened the ability of the US government to restrict incoming investments from China or any other country. Their key feature is expanding the remit of CFIUS and the export-control agency to block deals, not just on narrow defense-related grounds as in the past, but to protect American control of a wide range of technologies.

Based on conversations I’ve had this month in Silicon Valley, investors with Chinese connections have already found it harder to do deals. As the stringent new investment regime takes hold, companies in biotechnology, vehicle autonomy, artificial intelligence, and other fields may find themselves being treated as sensitively as semiconductor or defense companies.

High-tech anxiety

The US national security establishment’s concerns about Chinese technology investments were laid out in a January 2018 report by Defense Innovation Unit Experimental, a Defense Department organization set up to absorb innovations from Silicon Valley. The report documented major investments in California tech companies and argued that these deals resulted in technology transfers that harm national security.

California has indeed been the biggest target of incoming Chinese money, attracting US$30bn, or one-fifth of all Chinese greenfield investment and acquisitions in the US since 2000, according to the China Investment Monitor. More than a third of these investments have gone into tech sectors such as electronics, information and communications technology, health and biotech.

The DIU report recommended three main policy responses: a more stringent investment review regime, enhanced export controls, and a stricter immigration policy for Chinese students in science and technology fields. The first two of these have now been put into law, and anecdotal evidence suggests that Chinese tech students and workers are having a tougher time getting into the US.

On August 13, President Donald Trump signed the Foreign Investment Risk Review and Modernization Act, which sailed through both houses of Congress with overwhelming bipartisan support. FIRRMA doesn’t name China, but Senator John Cornyn, one of the act’s sponsors, cited the DIU report as an inspiration. And the law states that the US should work with allies to counter the “unprecedented industrial policies of certain countries of special concern, including aggressive efforts to acquire United States technology, and the blending of civil and military programs.” This evidently refers to Beijing’s Made in China 2025 and military-civil fusion policies.

FIRRMA expands the scope of CFIUS in two important ways. First, CFIUS may now review non-controlling investments, so long as the investment allows a foreign person to view material, nonpublic information or offers decision rights. Second, it authorizes CFIUS to scour deals not just for narrow defense and national security concerns, but also to safeguard “critical technologies,” and “emerging and foundational technologies.”

These terms are as yet undefined, and their meaning will be established by an expert committee managed by the Commerce Department’s Bureau of Industry and Security (the office that runs US export controls). If the DIU report is a guide, they will likely encompass artificial intelligence, robotics and autonomous vehicles. Many other sectors could potentially be included, such as cybersecurity, big data and financial technology.

The first draft of FIRRMA granted CFIUS another power which fell out of the final version after pushback from business: the right to review outbound investments by American firms. Scrutiny of outbound technology deals instead has been covered by the Export Control Reform Act, which passed Congress this month as part of the annual authorization of defense expenditures. This authorizes the Bureau of Industry and Security to block exports of “emerging and foundational technologies” if the transaction would compromise national security. Again, just how big a deal this is will depend on how broadly these technologies are defined.

Lots of Chinese check-writing in California

It will take at least a year for FIRRMA to come fully into force, but the prospect of stricter scrutiny has already begun to stigmatize Chinese investment in Silicon Valley, and companies and venture-capital firms have begun to view it as financing of last resort.

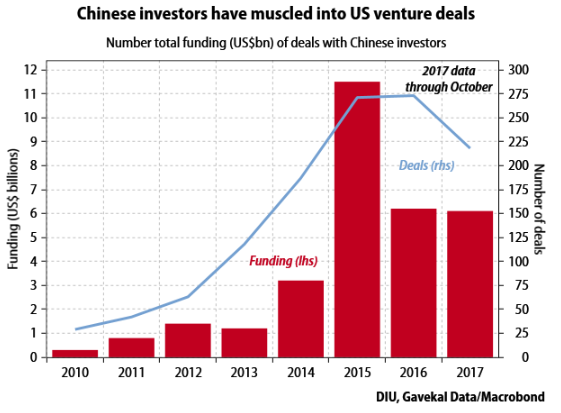

Just how big a financial hit Silicon Valley will take is not easy to say: VC investments are hard to track due to a lack of disclosure requirements. The DIU report identified 218 deals with a total value of US$6bn in 2018 that had at least some Chinese participation. Both figures were down from the peak level in 2015 (274 deals worth US$11bn), and the Chinese share of the total value is unclear. Other sources estimate that Chinese VC investments have been on the order of US$2bn a year since 2015.

Chinese tech investments come in four broad types. The first are government-linked funds and the investment arms of state-owned enterprises. Examples include Westlake Ventures, a small fund owned by the Hangzhou government which claims to have funded 35 tech startups; and the SAIC Motor Technology Fund, which has invested in battery, autonomy, and mapping companies.

Next are private companies like Baidu, Alibaba, and Tencent, which mainly make strategic investments, typically minority stakes. The third category is Chinese VC funds, for example IDG Capital and ZhenFund. Finally, there are wealthy individuals, who may want to diversify their portfolios with investments in the next hot thing or may simply be looking for ways to move money out of China into a safer place.

Deals involving money from any of these sources are now potentially at risk of CFIUS scrutiny. The one type of Chinese money that should still be safe is limited-partner investments in venture capital funds controlled by American general partners.

Chinese interest in Silicon Valley took off in 2014 when, according to one seed investor in Palo Alto, rich Chinese were writing checks to any Stanford student with an idea to pitch. Bigger checks soon followed from venture funds and the Chinese internet giants. Baidu led a US$1.2bn round in Uber in 2015, and the next year Alibaba participated in a US$800mn round in Magic Leap, a maker of augmented reality headsets.

Chinese funds pulled back at the end of 2015 thanks to capital controls imposed by Beijing to stem capital flight and support the renminbi. The sudden inability of Chinese investors to deploy capital caused consternation in target companies. From that point on, US firms became more cautious about taking Chinese investors, simply because they couldn’t rely on them to meet capital calls.

Chinese tech investors mainly focus on “deep tech” companies in fields like semiconductors, artificial intelligence and biotechnology—which are organized around their intellectual property—rather than the other main type of Silicon Valley startup, consumer internet firms (which are less IP-centric). This may be because consumer internet companies can raise all the money they need from conventional American VCs, while nerdier ventures need to scrounge harder for capital. Or it may reflect a hunger by Chinese tech firms and venture funds (driven either by commercial need or government directive) to gain access to new IP that can be commercialized in China.

Companies are now getting allergic to Chinese cash

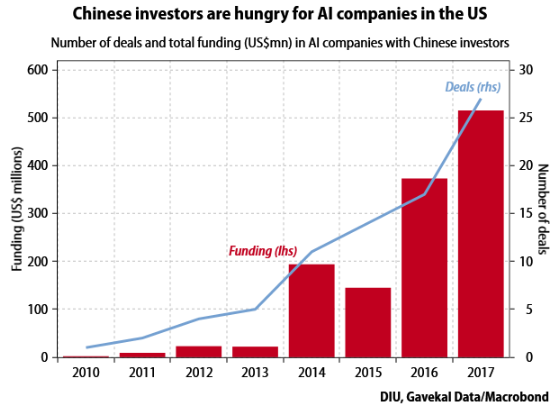

This deep-tech focus—especially noticeable in AI, where Chinese participation in funding rounds has risen sharply—is precisely what concerns US national security officials, since a lot of these technologies have potentially large military applications.

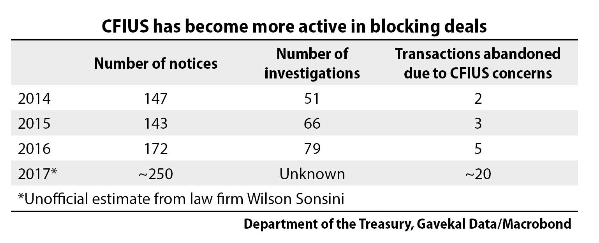

Partly thanks to these concerns, CFIUS has scrutinized more deals, and become more forceful in blocking them. Until 2013, CFIUS reviewed around 100 transactions a year, and only rarely were deals canceled because of its objections. By 2016, the last year of official data, the number of transactions swelled to 172, and five deals were abandoned due to CFIUS objections. In 2017, an estimated 250 transactions were reviewed, with 20 cancellations. CFIUS has reviewed more investment attempts from Chinese firms than those of any other country, and most of its high-profile rejections involved Chinese firms.

All this was before CFIUS’s powers were expanded. The prospect of even fiercer scrutiny will probably cause many startups to reject Chinese funding out of hand. A Chinese investor who invests in technology companies with the intention of commercializing their IP in China—exactly the sort of transaction that CFIUS wants to look at—told me that one of her target companies refused her money because it didn’t want to go through an expensive and time-consuming CFIUS review. Two prominent VCs told me that they have started to advise companies that Chinese money is risky, because of the likelihood of a CFIUS review.

Of course, where there is a regulation, there is a workaround: one investor told me that bankers have already started dreaming up exotic legal structures to help companies evade CFIUS reviews. But FIRRMA anticipated this. It authorizes CFIUS to investigate not only direct-investment deals but also “any other transaction, transfer, agreement or arrangement designed to circumvent CFIUS jurisdiction.” Defense and tech firms that do business with the Pentagon have always been careful to screen their investors; now companies working in a wide range of other technology sectors including AI, autonomous vehicles and biotechnology will have to learn to do the same.

A separate question is whether reduced access to US tech firms will significantly slow China’s own technological progress. I think probably not. Technological development depends ultimately on people, and even if Chinese technology firms are unable to invest in US companies, there is nothing to stop them from hiring international talent and putting it to use in the increasingly dynamic Chinese market.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

** Due to recent weakness, certain BB issues look attractive.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.