"Unfortunately, Mr. Paul has maintained his consistency by ignoring reality, clinging to his ideology even as the facts have demonstrated that ideology’s wrongness…"

-PAUL KRUGMAN, referring to Ron Paul

"The Fed never admits it, and the Congress disregards it out of ignorance, but the serious harm done by artificially low interest rates—leading to malinvestment, overcapacity, excessive debt and speculation causes the distortions that always guarantee the next recession."

-RON PAUL, September 6th, 2001

Battle of the Paul's. Opinions—everybody's got one, especially when it comes to economics and finance. Further, it's human nature to assign special credibility to those opinions that are expressed via respected media channels, such as, for example, the New York Times. Even more credence is bestowed on those who have won a Nobel prize, which seems logical enough until you do some retrospective fact-checking.

Several weeks ago I wrote in these pages about two books I read while on vacation and that I would discuss them in future EVAs. Well, the future has arrived and somehow I suspect most of you haven’t exactly been waiting in breathless anticipation for this issue. But I strongly believe the subject matter is both important and extremely relevant to the market as well as prevailing economic conditions.

First, let me start with an admission: I’m not a card-carrying member of the Paul Krugman fan club. As many of you are aware, Krugman is the Nobel Prize-winning columnist for the New York Times. My less than adoring views of him are merely an assessment, the close cousin of opinion. However, I’ve also never been an admirer of Ron Paul, who certainly occupies the polar opposite side of the economic spectrum. Thus, it was with a relatively equal negative bias going in that I read a book titled Ron Paul vs Paul Krugman by Jeremy Hammond.

As most Americans are aware, the gentleman from Texas, with the last—not first—name Paul, has been unflinching in his scathing attacks on US fiscal, monetary, and economic policies, utilizing, until he ran for president, the bully pulpit of Congress.

The other Paul (first name) has been just as vociferous and relentless in expounding his opinions, in this case using America’s most famous metropolitan paper as his platform. His Nobel Prize in economics, awarded in 2008, has emboldened him, so that even an occasional reader cannot help but notice his air of supreme confidence which, in my opinion view, borders on hubris. (In case you think I’m being unduly harsh, lately he has begun referring to himself, with his usual modesty, as the "Krugtron.") But, as I wrote regarding Woody Brock a few weeks ago, arrogance combined with competence can at least be justified, if not particularly attractive.

Thus, the key question is, looking back over the last 15 years or so, which Paul has done a better job of recommending effective policies and accurately anticipating future events?

Bubble 1.0! In my mind (note: I didn't say opinion, although it is), the labels "liberal" and "conservative" are misleading and even harmful, especially when it comes to economics. They should really be classified as rational as opposed to irrational or productive versus counterproductive. Naturally, determining which is which is merely an exercise in opinion expression until—and this is where the rubber meets the road—the future becomes the past. At that point, the advisability and effectiveness of a particular set of policy recommendations can be determined. Please stay with me here: I'm convinced, with a lot of history on my side, that this matters very much to the future direction of the US economy and financial markets.

To begin this investigation, we need to go back to the late 1990s, as Jeremy Hammond did, and review what Mssrs. Paul and Krugman (how ironic to conflate those into one name!) had to say. Fortunately, both of them had a lot to say, publicly recorded, not just then but also in the years to come, and up until right now.

As most of us remember, the late 1990s were close to economic nirvana for the US (although thunderheads were forming on the horizon). The economy was growing rapidly, inflation was subdued, at least in consumer prices, and the unthinkable was occurring: The US actually began to run budget surpluses and pay down debt. Thus, it was understandable that the architects of the boom, and their apologists, were euphoric, even though to many, including your truly, a massive and alarming bubble had been allowed to inflate.

Certainly, Paul Krugman was unperturbed. Here are some excerpts describing his outlook in early 2000 on the eve of one of the most vicious bear markets of all time, particularly in tech stocks: "Current stock prices already have built in the expectation of economic performance that not long ago we would have considered incredible; performance that is merely terrific would be seen as a big letdown. So which will it be—terrific or incredible?" Accordingly, per Krugman, a brief early-year plunge was attributed to "merely terrific" rather than "incredible" economic performance. He then closed this article by writing: "But hey, it’s still a terrific economy. Or do I mean incredible?"

In fairness, as was also the case some seven years later, Krugman did wonder if there might be a bubble at the time, though his views were highly ambiguous. To wit: After celebrating the economic boom and "extraordinary prosperity," he went on to write on the topic of whether there was a stock bubble that he was "sympathetic but not entirely convinced." Moreover, he said, "I’m not sure that the current value of the NASDAQ is justified, but I’m not sure that it isn’t."

Even as the massive dirigible that was the tech bubble began to implode, he reassuringly wrote: "The US economy has broken all the old limits…almost every fresh economic statistic (is) a cause for celebration."

By the end of 2000, with the NASDAQ down 39% and economic data deteriorating, he began to express some concerns, though highly sugarcoated: "But even if we have a recession, so what?" He went on to opine that a brief recession would not "reflect any fundamental problems in the economy." Early in 2001, though, he began to inform his readers that the NASDAQ had been "a classic bubble" even though he had been at best equivocal before it burst.

Meanwhile, the Fed, which Krugman had repeatedly praised in the late 1990s, but had earned his ire by raising rates in 2000, was now in frantic rate cutting mode as the tech meltdown intensified. This monetary easing restored his love for Alan Greenspan: "The Fed’s move has already made a noticeable difference, stemming the rout in the NASDAQ and producing a striking recovery in the corporate bond market. Another few shots in the arm like that and talk of a recession might well evaporate."

Unfortunately for Krugman’s forecasting track record, despite the Fed repeatedly cutting its overnight interest rate to the unprecedented (since the 1950s) level of 1%, the rout in the NASDAQ was anything but stemmed. It went on to plunge a Great Depression-like 78% and corporate America endured one of its worst profit recessions since the 1930s.

To end this section, I’d like to highlight some of Krugman’s assertions written in March and July of 2001 that have, in my opinion (sorry), enormous reverberations today: "During a financial bubble (my note: the one he didn’t see), many bad investments get made. So what? The nation should write those investments off and move on…And, if people are hesitant about spending enough money to keep those resources employed, well, the central bank should just cut interest rates until spending money is an opportunity too good to refuse."

In July 2001: "It wasn’t true when Richard Nixon said it, but it is true today: We are all Keynesians now…Only as a result of the Keynesian revolution did it become obvious to everyone—so obvious that people take it for granted—that the problem during a slump is too little spending, not too much, and that recovery depends on persuading the public to start spending again."

To Krugman’s credit, the words "the central bank should just cut interest rates until spending money is an opportunity too good to refuse" did in fact predict what the Fed would do—with disastrous implications almost beyond comprehension.

The Bubble Buster. In the late 1990s, when both the Fed and Paul Krugman were wearing bubble blinders, Ron Paul was saying things like: "(The Fed) comes along and they crank out the credit and they lower interest rates artificially, which then encourages business people and consumers to do things that they would not otherwise do. This is the expansion of the bubble part of the business cycle, which then sets the stage for the net recession."

Similarly, in September 1998, he railed against "…a fiat monetary system that allowed the financial bubble to develop. Easy credit and artificially low interest rates start a chain reaction that, by its very nature, guarantees a future correction. Fiat money and its low interest rates cause malinvestment, over-capacity…excessive debt and over-speculation."

He then uttered words that would be even more profound a decade later in the wake of a far more serious bubble implosion: "Capitalism erroneously is being blamed. No mention is made that no country today is truly capitalist in following sound monetary policy. The largest of all bubbles is now bursting (my note: that is, up until that point). Central banks generously create credit out of thin air (which is) welcomed and applauded as the boom part of the cycle (producing) illusions of wealth brought about by artificial wealth creation that end when the predictable correction arrives."

To put the above into context, when Paul wrote those words, the world, which mere weeks before seemed to be awash in prosperity, was suddenly beset by the twin terrors of the Asian crisis and the collapse of Long Term Capital Management (tellingly run by two Nobel Prize-winning economists). Tech stocks, already in a mini-bubble, were obliterated. The Fed, which previously had been gently raising rates due to an overheating economy, ignored economic considerations and responded to the plunging market by cutting rates. To make matters worse, the Fed injected massive sums of liquidity into the economy in 1999 due to misguided fears of Y2K (remember that one?) and worries, again misplaced, over deflation caused by Asia’s trauma. As a result, tech stocks entered the ionosphere as 1999 drew to a vertiginous close, sucking in millions of retail investors who simply couldn’t resist the allure of lavish, easy profits.

Quoting Jeremy Hammond as the Fed stood by and watched a stock bubble inflate that put 1929 to shame and Paul Krugman was waxing euphoric about the economy (and was cavalier about the tech mania), the other Paul was issuing vigorous, and prophetic, admonishments: "In November 1999, Ron Paul again warned that, in addition to fueling borrowing and spending, inflation was showing up in the rising prices in assets, rather than consumer goods. The Fed’s monetary policy was responsible for the financial bubble, he said…In addition, he warned that their (Fannie Mae’s and Freddie Mac’s) securitization of mortgages might reduce risk for individual financial institutions, but increased the risk to the economy as a whole. This spelled trouble when coupled with the government’s longstanding policy of bailing out troubled institutions, which created a moral hazard and put taxpayers on the hook for the risky business practices. Such government interventions in the market, he argued, did not bode well for the future."

Even though Ron Paul was decidedly in the minority with his opinions, he managed to hit the trifecta: Excessive credit creation had created inflation not in the cost of living but in asset prices, the Fed had enabled the bubble in stocks through said credit explosion, and, anticipating the next disaster years in advance, huge problems were coming out of housing.

As we shall see, on the third and, as it would turn out, most important point, Paul Krugman had a very different view. Or, should I say opinion?

Bubble 2.0! William Shakespeare wrote that when sorrows come they come not as single spies, but in battalions, and that was certainly the case in the late summer of 2001. With the NASDAQ continuing to crater and the economy now in recession, Krugman didn't see coming, the horrific events of 9/11 transpired. As the nation reeled from the murder of thousands of innocents, he wrote these bizarre words: "Ghastly as it may seem to say this, the terror attack—like the original day of infamy, which brought an end to the Great Depression—could even do some economic good...If people rush out to buy bottled water and canned goods, that will actually boost the economy."

A month later, on October 7, 2001, when it was becoming obvious that the purchases of bottled water and canned goods weren’t sufficient to offset the shock to business and consumer confidence that occurred after 9/11, he began to advocate a new plan: "Economic policy should encourage other spending to offset the temporary slump in business investment. Low interest rates, which promote spending on housing and other durable goods, are the main answer." Thus, his proposed solution was to inflate a new bubble to cure an old bubble, an exhortation he would repeat in the years to come, at least until it belatedly dawned on him that he had gotten what he wished for—good and hard.

By the end of 2001, after having repeatedly assured his readers that interest rate cuts would achieve a soft landing or, at worst, a mild recession, Krugman wrote: "The Fed has now cut interest rates 11 times this year, and has yet to see any results."

In August of 2002, as the economy was tremulously recovering from the dual shocks of tech’s spectacular collapse and the wrenching events of 9/11, Krugman was fretting over a double-dip recession. "As I’ve repeatedly said in this column, the arguments of the double-dippers made a lot of sense and their story now looks more plausible than ever." Consequently, he spells out his remedy in very clear terms: "To fight this recession the Fed needs more than a snapback; it needs soaring household spending to offset moribund business investment. And to do that, as Paul McCulley of Pimco put it, Alan Greenspan needs to create a housing bubble to replace the NASDAQ bubble" (my emphasis).

In mid-2003, Krugman was miffed at the Fed for allowing long-term rates to rise from extremely depressed levels, threatening the housing bubble he had endorsed: "Mortgage rates did indeed fall briefly to historic lows, extending the home-buying and refinancing boom that has helped keep the economy’s head above water…This week rates on 30-year mortgages hit their highest levels since January. And Mr. Greenspan bears some of the responsibility."

Despite his contention that Mr. Greenspan should shoulder the blame for this relatively short-lived rate spike (30-year mortgage rates eased back 75 basis points by late summer), supposedly jeopardizing his "home-buying and refinancing boom," by the second half of 2003 the US economy was off to the races. Yet, the Fed left its overnight rate at 1% until mid-2004 and what was already a bull market in housing soon morphed into outright bubblemania.

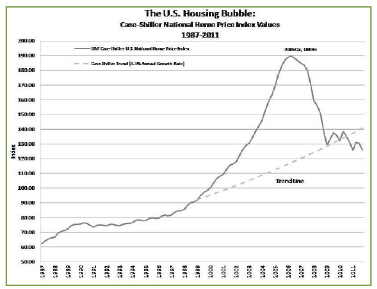

Along the way, Mr. Greenspan even began advocating that consumers use adjustable-rate mortgages to fully take advantage of the Fed’s inexplicable suppression of interest rates despite a robustly expanding economy. The "maestro" also stood idly by, as did most US policymakers and regulators, as the finance industry created "innovations" like zero-down and no-doc (aka liar) loans. Even more incredibly, by the middle of the last decade, when US home prices were as far above their long-term trend line as stock prices had been in 1999, the Fed could not detect any signs of a bubble.

At that point, however, one of the original helium-meisters had begun to have second thoughts.

Piper Paying Time. It was in the spring of 2006, at the John Mauldin conference in LaJolla, that I first heart Paul McCulley speak on his profound fears about the speculative frenzy that had gripped housing. If he had advocated inflating a bubble a few years earlier, he was certainly preaching a different sermon at that time. In fact, his mesmerizing presentation at that event was a key reason my fears about housing—already manifesting themselves in July 2005 when I wrote Anatomy of a Bubble—became an obsession for me over the next couple of years (as longtime EVA readers no doubt remember, to their chagrin).

At around the same time, in May of 2005, Krugman was acknowledging the housing bubble but, remarkably, already looking for another area that could be inflated to offset the adverse impact of the former’s eventual demise. "Now the question is what can replace the housing bubble? Nobody thought the economy could rely forever on home buying and refinancing. So what happens if the housing bubble bursts? It will be the same thing (my note: recession) all over again, unless the Fed can find something to take its place."

Nearly two years earlier, in September 2003, as home prices were embarking on their moon shot, which was precisely what Dr. Krugman had prescribed, Ron Paul was on record with the following views: "The easy credit policy is welcomed by many: stock market investors, home builders, home buyers, congressional spendthrifts, bankers and many other consumers who enjoy borrowing at low rates and not worrying about repayment. However, perpetual good times cannot come from a printing press or easy credit created by a Federal Reserve computer. The piper will demand payment, and the downturn in the business cycle will see to it…Lowering interest rates…will produce the desired effects and stimulate another boom-bust cycle."

Krugman’s housing bubble epiphany has allowed him to claim that he warned of its implosion and possibly played a significant role in his 2008 Nobel Prize. However, the reality is that he was one of the leading cheerleaders in its early stages. By the time he woke up to the impending disaster in 2005, it was much too late, with home prices already in the parabolic phase. Conversely, Ron Paul had presciently cautioned from the outset that such reckless asset inflation, which also put the banking system at risk, could only end catastrophically.

Coincidentally, the other book I read on my vacation was Economics in One Lesson by Henry Hazlitt. It is an essential read for anyone who is mystified and distressed by current US economic policies. Like Ron Paul, he excoriates politicians from both parties who advocate programs that are nonsensical and counterproductive (more to follow on this classic in a future EVA).

Given that the edition I read was first published in the late 1970s, Hazlitt’s tocsin is even more clairvoyant than Ron Paul’s. "Government-guaranteed mortgages, especially when a negligible down payment, or no down payment whatever, is required, inevitably mean more bad loans…They encourage people to ‘buy’ houses that they really cannot afford. They tend eventually to bring about an oversupply of houses…and may mislead the building industry into an eventually costly overexpansion. In brief, in the long run they do not increase overall national production but encourage malinvestment."

There’s that word again, "malinvestment," the one Ron Paul also used in referring to both the tech and housing bubbles. In my opinion, this is really the crux of the entire juxtaposition between the Krugman worldview and that of Paul/Hazlitt. Further, I also believe the malady of malinvestment should be the uber-concern of all rational investors right now.

Bubble 3.0? The main point of looking back at these two very opposing schools of thought over the last 15 years isn’t to vilify Paul Krugman or exalt Ron Paul. In fact, I vehemently disagree with Ron Paul’s contention that the Fed and the US Treasury should have let the financial system implode back in 2008. Rather, the objective of this EVA is to consider what excessive credit creation and, in recent years, the fabrication of $3 trillion of reserves, has meant to our economy. (Also, let me reiterate a point made in numerous past EVAs: it is often the so-called liberal party that rejects destructive economic policies and brings their country back from the brink of insolvency, Canada and Sweden being two salient examples.)

Rather than giving us true prosperity, this tsunami of funny money has created two bubbles and two busts. That ‘s not an opinion, that’s a fact. Now, what is literally the multi-trillion-dollar question is whether a third bubble has been blown. Paul Krugman is arguing that this is not the case. In his opinion, the problem is that we haven’t printed enough money or run large enough federal deficits to cope with the aftermath of bubbles he either didn’t see or actively encouraged. He believes this despite the fact that the national debt has increased by $8 trillion, almost doubling in six years what took more than 200 prior years to accumulate, and that the Fed is actually monetizing the government’s deficits with its bogus money.

Unsurprisingly, Ron Paul is convinced we have set the stage for the next crisis. "What is obvious to most people not captured by the system is that the Fed’s loose monetary policy was the root cause of the current financial crisis…the current crisis resulted from the creation of money and credit by the Federal Reserve, which led to unsustainable economic booms. Rather than allowing the malinvestments and bad debts caused by its money creation to liquidate, the Fed continually tries to prop them up. It pumps more and more money into the system, piling debt on top of debt on top of debt. The phony recovery we find ourselves in is only due to the Fed’s easy money policies. But the Fed cannot continue to purchase trillions of dollars of assets forever. Quantitative easing must end sometime, and at that point the economy will face the prospect of rising interest rates, mountains of bad debt and malinvested resources…"

So, which Paul is going to be right this time? Naturally, I have an opinion, and perhaps not totally the one you might think. Even though Ron Paul has obviously been far more accurate in the past than Paul Krugman, he hasn’t gotten it all right (who does?), and I don’t agree with every prediction he makes above, at least over the next few years.

If he is correct that the malinvestments of this latest Fed-induced asset levitation do blow up soon, the likelihood is that safe interest rates will fall not rise (rates on trashy credits are a very different story). My team and I continue to believe that aging boomers, and those a touch more aged, should be capitalizing on the selling frenzy occurring with yield instruments, particularly at year-end when there is obviously intense tax-loss selling occurring.* However, with the Fed’s taper looming more likely, and tremendous uncertainty as to whether a "melt-up" in stocks lies ahead, it’s prudent to hold some cash and hedges even though they have been tremendous performance drags this year.

What isn’t in doubt is that over the last 15 years, and especially the last five, US monetary and fiscal policies have been much closer to the Paul Krugman model rather than the Ron Paul approach to running the system. Unfortunately, based on past history, the Krugtron’s opinions, largely adopted by those in positions of power, have been running it into the ground.

*One of our favorites yields 12%, has seen significant insider buying, and has greatly reduced its exposure to higher interest rates. At today’s depressed price, we believe it offers material price appreciation potential in addition to the lofty yield.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.