"Where you see wrong or inequality or injustice, speak out, because this is your country. This is your democracy. Make it. Protect it. Pass it on."

-THURGOOD MARSHALL, former US Supreme Court justice

Generally speaking, the purpose of EVA is to communicate Evergreen’s overall outlook on the markets and economy. We tend to stick to this script by writing on topics such as central bank policy, inflation, the stock market, the bond market, and energy. One theme we try to avoid – or at least stay neutral on – is politics.

The reason for this orchestrated side-step is pretty simple: politics are messy, polarizing, and tend to be biased. And while the happenings in Washington have become increasingly intertwined with market movements and the economy, the purpose of this week’s EVA is not to ignite a political discussion, per se. Rather, what we hope to accomplish in this week’s missive is to share a key finding we believe is worth considering at an ideological level: that democracies around the globe are in, many cases, under siege.

U.S.-based readers need not travel far from home to understand the truth in this statement. A nearly two-year string of Russian-meddling headlines has tainted the resilience of our once-esteemed free-and-fair election process. A leftward lurch this November could shine an even brighter light on this issue and result in consequences that extend to the Oval Office. The possibility of an impeachment for this (or another) issue – which will increase in likelihood if Democrats win control of the House – would represent a significant hit to the American political system. But let’s not get too far ahead of ourselves.

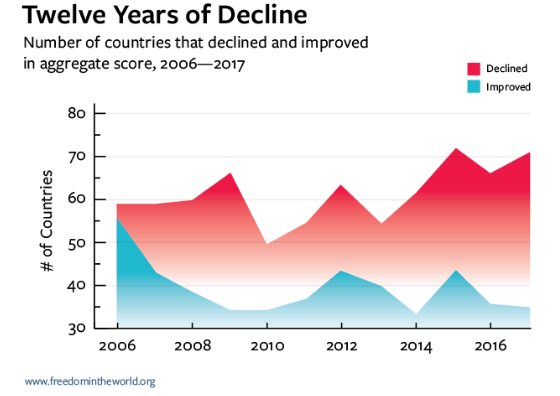

Taking a much wider view of the global democratic crisis, Freedom House, an independent watchdog organization dedicated to the expansion of freedom and democracy around the world, recently published their annual “Freedom in the World 2018” report. Many of their findings support the view that democracy is in a significant state of retreat. In fact, over the last year, 71 countries suffered net declines in political rights and civil liberties, with only 35 registering gains. And this is far from a new phenomenon. As the chart below illustrates, 113 countries have seen net declines and only 62 have seen net improvements over the past twelve years.

The rise of populist movements springing out of Europe - the modern world’s birthplace of democracy - underscores this global shift. France, the Netherlands, Germany, and Austria all faced increasing pressure to reorient towards left-of-center thinking. But it isn’t just a push towards populism that has threatened the foundations of democracy; there have been dramatic declines in measures of freedom in every region of the world over the last decade.

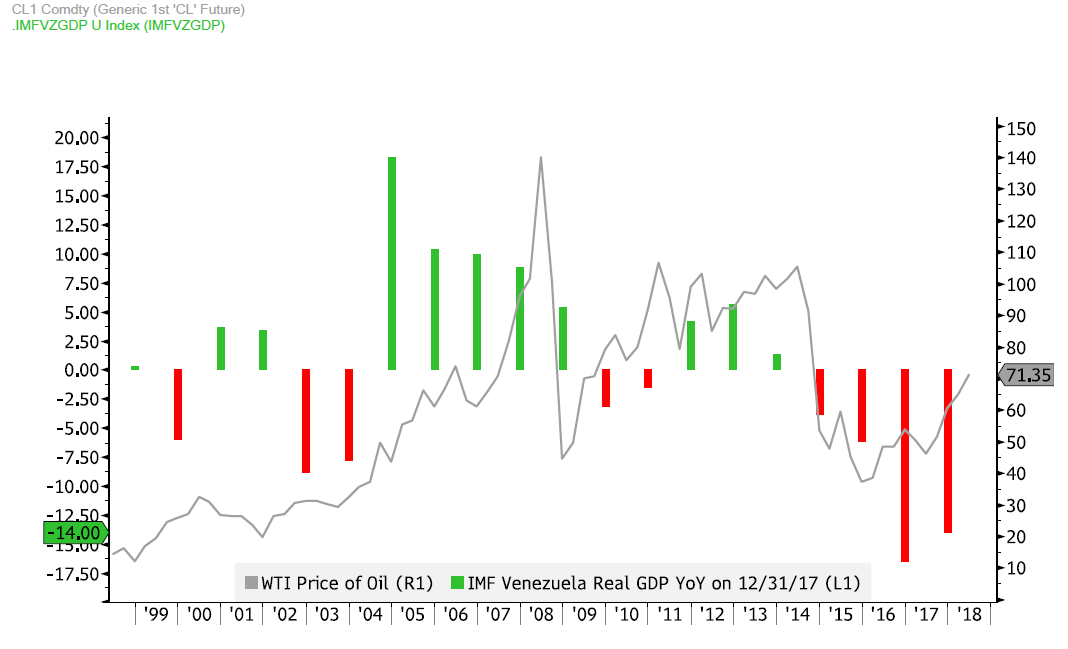

Perhaps most alarming are examples from Turkey, Hungary and Venezuela – three countries that were once promising examples of instituting democratic reforms in the developing world but have now slipped into chaos as a result of authoritarian rule. In the case of Venezuela, president Nicolas Maduro has continued in the footsteps of his deceased predecessor, Hugo Chavez, by devolving his country from being one of the wealthiest countries in the Southern Hemisphere into one of the most devastating humanitarian crises in recent memory. Inflation in Venezuela is just slightly out of control, running at an annual rate of 13,000%.

Certainly, crashing oil prices from 2014 to 2017 have played a big role in this tragedy, as revenue from petroleum exports account for more than 50% of the country’s GDP and roughly 95% of total exports. But the reality is that the country was on the path to economic disaster and was becoming increasingly totalitarian even before the oil bust. Moreover, Venezuela’s heartbreaking economic implosion has worsened even as crude prices have nearly tripled from their early 2016 lows.

PRICE OF OIL (WTI) VS. VENEZUELA REAL GDP

Source: Bloomberg, Evergreen Gavekal (as of 5/15/2018)

Source: Bloomberg, Evergreen Gavekal (as of 5/15/2018)

The case study of Venezuela shows how the rise of socialism in a country can sometimes morph into a much more extreme form of authoritarianism. Socialism and police states are oftentimes joined at the hip. And, speaking of autocracies, two world powers – China and Russia – have been bolstered by the dysfunction of typically strong democratic nations. They have both seized the opportunity to step up repression within their own countries, while also spreading their antidemocratic influence to other nations. One example of this is Chinese president Xi Jinping’s recent proclamation that “China is blazing a new trail for developing countries to follow.”

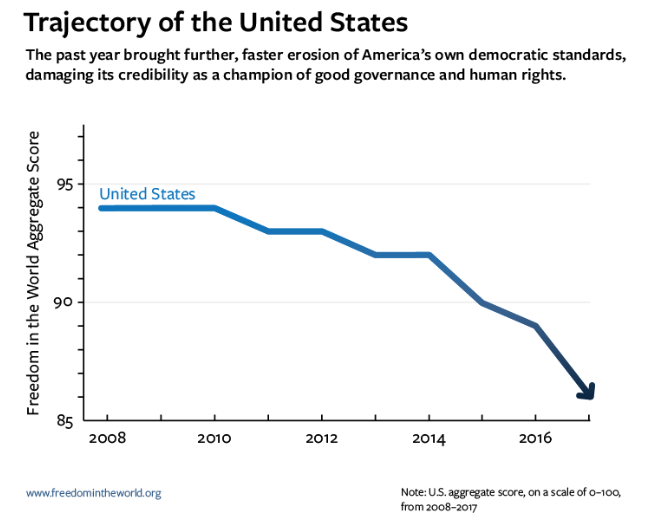

The United States, which has been a long-term global champion and exemplar of democracy, has fallen from its post as the global leader in this area in a dramatic way over the last ten years. As the chart below shows, the trajectory that the U.S. is on is far from optimistic for those hoping the United States will take charge while world powers like China and Russia spread their antidemocratic messages.

Among the most disturbing realities of recent times is the rising popularity of socialism among America’s young people. The surprisingly strong showing by avowed socialist Bernie Sanders in the 2016 Democratic primaries was an obvious indication of this trend. Yet, unfortunately, it goes beyond a fleeting infatuation with Mr. Sanders’ fiery rhetoric. Polls show that Americans under 30 have nearly as much confidence in socialism as capitalism. This is despite history’s recurring lesson that extreme socialism leads to economic disaster and, all too frequently, civil liberty repression, if not outright “thugocracies”.

Source: Wall Street Journal.

Source: Wall Street Journal.

Black line represents % of respondents with positive views of capitalism;

gold line represents those with positive views of socialism.

One of Evergreen’s overarching worries is that when the next market crash and/or recession occurs, capitalism will get the blame and socialism will be portrayed as the solution. We are additionally concerned that radical central bank policies, which have inflated asset prices to dangerous levels and have widened the wealth gap between rich and poor, have greatly increased the risk of an anti-capitalist backlash.

What is clear, and what history shows us, is that when countries are free, they are safer and more prosperous. When countries are repressive, nations become unstable and extremism takes hold, which spurs abuse and radicalization (take Venezuela as a “shining” example). The extent to which freedom is widespread throughout the world has direct implications for the economy and the general welfare of citizens, both locally and globally. To be fair, the rise of antidemocratic sentiment over the past twelve years hasn’t put the slightest dent in the second-longest bull run in market history. However, as threats of totalitarianism take root in developed and developing nations, the proliferation of these antidemocratic ideologies could have much more sweeping implications for the global balance of power—and the future path of financial markets.

Socialism is on the rise. Totalitarianism is on the rise. Democracy is in crisis. Eventually, even the S&P 500 might notice.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.