“It is better to be three hours too early than a minute too late.”

-Falstaff, in Shakespeare’s The Merry Widows of Windsor.

“Put simply, the Fed has created the third speculative bubble in 15 years in return for real economic improvements that amount to literally a fraction of 1%.”

- John Hussman, referring to a recent influential research paper by the University of Chicago’s Cynthia Wu and Fan Dora Xia.

SUMMARY

- The latest Hollywood blockbuster The Big Short evokes strong memories here at Evergreen of the bubbly days leading up to the subprime housing bust in 2007 and 2008.

- Like the film’s protagonists – hedge fund managers Mark Baum and Dr. Michael Burry – we spent several years warning about the risks to the creaky housing market and the overleveraged US financial system. While our caution was a source of frustration for some clients, it ultimately paid off for the patient majority who stuck with us.

- While our defensive posture in the face of rising prices was eventually vindicated, that process did not happen overnight. As the movie reminds us, mortgage-backed security (MBS) valuations actually continued to rise even as defaults rose sharply. Being early in recognizing bubbles can be extremely painful for a year or two, but what matters most is being right in the long run.

- Once again, we find ourselves in that uncomfortable position at Evergreen. After years of overly accommodative Fed policy, we see bubbles all around us and also signs that many of them are beginning to pop. Once the reality of how much people have lost in this correction/bear market sets in, panic is likely to develop.

- That said, we are also keenly aware of the opportunities (or “anti-bubbles”) now beginning to present themselves in beaten-up investment sectors (aka asset classes) like energy. In the not-too-distant future, possibly even in the next few months, we expect many other asset classes to fall into the anti-bubble category. It will be terrifying for investors who are overextended in overpriced assets, but a tremendous opportunity for patient and disciplined investors with cash on hand.

EVERGREEN VIRTUAL ADVISOR

By David Hay

No thanks for the memories. On a recent stormy Sunday afternoon, my wife and I went to see the new hit movie, The Big Short, about the most severe financial storm since the Great Depression. As you may know, the film is based on the bestseller of the same name by Michael Lewis (who also wrote Liar’s Poker and Moneyball).

Like all entertaining movies, The Big Short is about a battle between the good guys and the bad guys. The heroes were those who saw the apocalypse in sub-prime mortgages coming. The villains were all those who denied and/or profited from the inflation of the housing bubble and all the lax credit extension that kept filling it with helium.

As I watched the film, vivid memories came rushing back to me—recollections of all the warnings I had issued about the housing bubble starting as early as 2005 and continuing through 2007 (read our November 2006 EVA.) The accepted and dominant view of housing at the time was that since home prices hadn’t fallen since the Great Depression, they certainly wouldn’t do so during a reasonably healthy economy, such as we had back then. It was also not a pleasant experience to be warning clients about the dangers in housing. Most of them were benefiting from the booming Seattle-area real estate market. Telling them that the good times were on borrowed time—and were being fed by way too much borrowed money—wasn’t a welcome message. Consequently, I felt lonely—very, very lonely.

It wasn’t until the bubble burst that I found out there was a small group of obscure mavericks who had sniffed out the emerging disaster. These individuals mostly ran hedge funds and, as The Big Short revealed, they pioneered the use of sophisticated tools to produce massive gains when the crash came. Since then, a few of them have become household names, especially the articulate and telegenic Kyle Bass. But the real heroes of the movie were a couple of social misfits, Dr. Michael Burry and Mark Baum, played by Christian Bale and Steve Carell, respectively. (As a footnote, Michael Burry is the only main character in the film whose name wasn’t changed; the Mark Baum role apparently was based on real-life hedge fund manager Steve Eisman.)

It was Dr. Burry who first recognized how creaky the entire housing and mortgage finance edifice truly was. Although he had built his $500 million fund and track record on stock picking, by 2005 he was approaching firms like Goldman Sachs to create de facto short positions on pools of particularly rancid sub-prime mortgages. Since no one had done this before, the Goldmans of the world needed to create these just for him. They were only too happy to oblige—for a juicy fee, of course—even as they snickered among themselves at Dr. Burry’s foolishness.

The next two years seemed to confirm their skepticism. Despite a few rumblings here and there, the great housing bubble kept inflating. The terms of his deal with Wall Street required Dr. Burry’s fund to pay roughly 6% per year for his negative stance which he kept raising. Eventually, he had over a $1 billion short position on sub-prime mortgages, costing his fund in excess of $60 million per year. As home prices continued to rise and defaults stayed low, his fund began to post losses at a time when most investors were making money. The S&P 500 was still rising in 2006 and 2007, as it clawed its way back toward 1550, the peak it had hit in early 2000, prior to the collapse of the tech mania. Consequently, investors in the handful of funds betting against sub-prime debt became increasingly restless.

Burry’s investors became particularly unhappy. One of the largest threatened to pull out his money unless Dr. Burry gave up on his quixotic quest. But by 2007, it was clear there was a major problem brewing in housing. Defaults began to soar and, in June of that year, two prominent Bear Stearns mortgage funds blew up, saddling their investors with huge losses.

Consequently, it must have been redemption time for Dr. Burry and the other housing bears, right? Actually, not so much…

Little indication of vindication. One of the most intriguing parts of the movie is how sub-prime mortgage valuations actually rose even as the crisis was unfolding. The rating agencies were a prime factor in this bizarre situation as they avoided downgrading mortgage pools. This was despite the fact that the underlying loans were defaulting at an increasingly rapid rate. Firms like Moody’s and S&P, the two dominant rating agencies, were being paid by Merrill Lynch and Goldman to rate the mortgage-backed securities the latter had created.

As a result, Moody’s and S&P were highly reluctant to kill the golden goose by issuing broad downgrades. Many of these securities had even attained the coveted AAA-rating through a complex securitization process. (The film cleverly explains this convoluted process in terms that most lay people can at least roughly understand; actress Margot Robbie in a bubble bath, appropriately enough, describing the alchemy of converting junk mortgages into AAA-rated issues is the highlight.)

Therefore, even as the sub-prime mortgage market was beginning to tank, those betting against it were still losing money. Mark Baum/Steve Eisman—who ran his hedge fund, ironically, at Morgan Stanley, one of the big players in the mortgage market--came into the game later than Dr. Burry. But he was still losing money when he should have been winning, and his volatile personality didn’t take this lightly.

One of The Big Short’s more interesting scenes is a meeting Baum had with a senior official at S&P. In it, the S&P executive admitted that if they didn’t give Wall Street the ratings it wanted, it would lose business to Moody’s. So even though they knew defaults were rocketing, S&P maintained high ratings on these troubled securities for far longer than they should have.

Things got so bad for Dr. Burry that he had to invoke a provision in his fund agreement allowing him to restrict investor withdrawals. As you would expect, that went over about as well as Cam Newton’s post-Super Bowl press conference.

Eventually, though, housing came crashing down in a thunderous explosion. Almost overnight, the Burrys and Baums went from laughable losers to superstars. In some cases, like Kyle Bass, they literally became billionaires. Dr. Burry’s fund went from deep losses to almost a 600% return by the time he took his gargantuan gains and shut it down.

As my wife and I watched this remarkable story unfold on the big screen (and we were seated in the front row of a packed theater so it was a REALLY big screen), my déjà vu feelings just kept mounting. And one of the sensations I experienced was that, since I, too, saw it coming I should have done more for clients to profit from its demise than I had.

But the reality is that Evergreen isn’t a hedge fund, and never was, so using items like credit default swaps wasn’t an option. Still, I was mentally kicking myself for holding any financial stocks or bonds. Yet, as the movie pointed out, even the major players in

The Big Short were stunned to find out the leading financial firms weren’t just packaging and selling these “securities”, thereby off-loading the risks. Incredibly, their investment divisions were buying them in copious quantities.

Our plan back in 2007 and early 2008 was to load up on defensive income securities. Our reasoning was that these were likely to rise in value as the Fed cut interest rates to prevent a recession due to the housing bust. But, as did Burry and Baum, we were soon to get a rude shock. Despite the Fed furiously slashing rates, which typically drives up the value of defensive income securities, even high-grade corporate bonds and preferred stocks plunged, some by as much as 40%.

NORDSTROM'S BOND PRICE IN 2008*  Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

As long-time clients and EVA readers know, this horrific twist actually worked in our favor as we added to our income holdings at throw-way prices—and extraordinary yields. Accordingly, this turned out even better for our clients than if these issues had reacted as planned (something MLP investors today might want to keep in mind). But to say it was an agonizing time is putting it much too mildly.

There are a number of lessons to be learned from the housing debacle. One is that being early to recognize bubbles can be extremely painful. But the film also underscores that what matters most is being right in the long run, not over a year or two. Another lesson is that the majority of Wall Street pundits are either so conflicted, or so deeply in denial, most of them cannot, or will not, see a financial disaster in the making.

Prior to my big jihad against housing, I had also raged against the tech bubble in the late 1990s. That wasn’t a very pleasant experience either with Seattle, once again, caught up in the middle of that frenzy. And there were precious few high-profile strategists who were warning clients in 1999 to avoid stocks with no earnings, or selling at over 100 times the profits they did have, or otherwise calling out what was the biggest stock market bubble in US history. If they dared, they were likely to be fired as Wall Street was feasting on the fees the tech IPOs were generating. In other words, being a bubble-basher is a long exercise in frustration, humiliation, and, at times, even career risk.

Speaking of which, let me tell you about my last few years…

Bubblemania, 3.0. One of the realities of the financial markets is that every cycle is different. There are similarities but there are also differences, sometimes significant ones. For example, the tech bubble didn’t involve much leverage, leaving the banking system minimally exposed. The housing boom and bust, however, was all about debt, and banks ended up at the center of the storm.

These days, I find myself once again in the uncomfortable position of battling against the conventional “wisdom” that says there isn’t a bubble. (By the way, a bubble is generally believed to occur when market prices soar far above any reasonable assumption of intrinsic value. This is always subjective but my contention is that, like a Supreme Court justice once said about pornography, I can tell a bubble when I see one.)

Among the differences of this up-cycle versus the late 1990s and the 2003-2007 period is that there isn’t an obvious mega-bubble like tech or housing. Yet it’s been Evergreen’s contention that there have been a series of more modest, but still dangerous, bubbles.

Contenders for the “B’ designation include, but are not limited to:

On the art topic, a couple of years ago, one of our EVAs ran a chart of art auction giant Sotheby’s. We noted the linkage between its prior ascent and previous bubble peaks. When we ran that, it had once again vaulted to a point matching its previous highs. But as you can see, things have changed in a big way.

LONG-TERM PRICE CHART OF SOTHEBY'S STOCK* Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

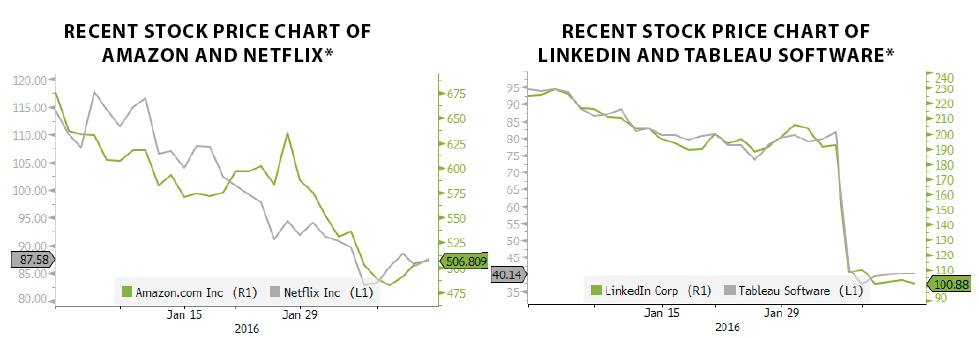

The breakdown in the various asset classes listed above has become quite inclusive. Even the once mighty FANGs—that propped up the US stock market last year—have lost their gravity-defying abilities. Two of them, Amazon and Netflix*, are down nearly 25% already in 2016’s first month and a half. Similar shooting-star issues, like LinkedIn and Tableau*, have fallen even harder.

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

Inventories of unsold high-end real estate are beginning to build even in the biggest US cities. Small- and mid-cap stocks are either in or on the verge of bear markets. The biotech index is now down 37% from its apex. Prices for collectibles are, appropriately, more art than science but, based on Sotheby’s stock price action, it’s likely they aren’t still heading in an upward direction.

You would think that based on all of the above, Evergreen’s many warnings since 2013 about bubbles caused by reckless Fed policies would have had some degree of exoneration. But, as with the main characters in The Big Short when the housing bubble first began to deflate, the reality is much less satisfying.

The Big Long. A fair criticism of our repeated expression of concerns about rampant overvaluation since 2013 is that we were early. As one of the characters in The Big Short screamed at Michael Burry, being early and being wrong is the same thing. Certainly, all of those who saw the dangers to the economy coming from the day of reckoning for sub-prime debt, NINJA (no income, no job, and no assets) loans, and adjustable rate mortgages, such as Burry and Baum/Eisman, were early.

Like us, then and now, they fretted over the Fed aiding and abetting the bubble formation by suppressing rates for much longer than they should have. (The movie lets the government itself off the hook much more than it should have by not emphasizing how certain members of Congress—and even presidential administrations—pressured banks to issue junk mortgages.) But it wasn’t until the full extent of the collapse was evident that they were truly vindicated. And even that was a bittersweet victory given the carnage inflicted on the global economy by the housing crash and the suffering it meant for millions, if not billions, of people around the world.

That bittersweet taste is what I am experiencing now. It’s becoming clear that American investors were duped into piling into stocks and bonds at inflated prices because the Fed has destroyed interest rates.

As we observed last week, we believe that the summer of 2014 will be viewed, in the fullness of time, as the high water market of this financial cycle. Since then, almost all asset classes (aka, major investment sectors) have been under pressure. In some cases, as with master limited partnerships (MLPs), it has been unrelenting.

Once the reality of how much people have lost in this correction/bear market sets in, panic is likely to develop. With interest rates non-existent—outside of those areas like MLPs, emerging market debt, junk bonds, etc, that have been crushed and of which investors are now terrified—returns are minimal. As in 2008, millions of them are likely to head to cash at the worst possible time.

Even though Evergreen was screaming to buy almost everything back in late 2008 and early 2009, our persistent warnings of the dangers of this latest Fed-created bubble, or series of bubbles, have led some to now view us as perma-bears. Yet, we not only feel we need to bash bubbles when prices get silly on the upside. We also strive to identify anti-bubbles, those situations where prices have fallen far below normal valuations and investor sentiment is fiercely negative. For us, that’s a lot more fun than warning of looming problems. An example right now of an anti-bubble is anything connected with energy.

In the not-too-distant future, possibly even in the next few months, we expect many other asset classes to fall into the anti-bubble category. For those loaded to the gunnels with cash, this will be a wonderful development. For those who bought into the Fed’s con game of dumping cash to hold overpriced securities, it will be a third terrifying plunge down the other side of the mountain, similar to 2000 to 2002 and 2008 to early 2009.

If we’re right, we are approaching another time for The Big Long—a glittering chance to buy stocks and bonds at stunningly cheap prices. Some of the folks who got The Big Short right, actually did pivot and buy mortgage debt when it was being given away (at the time, we wrote that AAA-rated sub-prime mortgage pools trading at 30 cents on the dollar were exceptional bargains). In our case, we sucked it up and bought (among other securities) high-grade corporate debt 30% to 40% below face value and MLPs, in some cases, yielding 25% or more.

This time will be different, of course, at least in terms of where the extreme bargains will be found. But the outcome won’t vary much. The cash-heavy and brave will end up collecting the spoils. The fully-invested and shocked will, once more, wind up taking it in the shorts (or being taken by the shorts). And we have no doubt that Evergreen will again be a very lonely bullish voice, as we are currently with energy. It won’t even be a surprise if some people start referring to us as perma-bulls. But we can live with that.

**The specific securities identified and described do not represent all of the securities purchased, held, or sold for advisory clients, and you should not assume that investments in the securities were or will be profitable. Facebook, Amazon, Netflix and Google, frequently used in market commentary using the FANG acronym, are used for illustrative purposes. The price chart of the Nordstrom bond is used to illustrate the severity of decline experienced in even securities which were considered by many to be high quality, in 2008. The price charts of Sotheby’s, Amazon, Netflix, LinkedIn and Tableau are use specifically for illustrative purposes, to demonstrate specific examples of market deterioration that has occurred. ECM currently holds Google (aka Alphabet) and recommends it for client accounts if ECM believes it is suitable investments for the clients, considering various factors such as investment objective and risk tolerance. It may not be suitable for all investors. Certain clients may hold Facebook, Amazon, Nordstrom, Sotheby’s, Tableau or Netflix in their accounts, at their discretion; these securities are not recommendations of Evergreen. Please see important disclosures included following this letter.

OUR LIKES AND DISLIKES.

Changes are bolded below.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.