“The mind of man at one and the same time is both the glory and the shame of the universe.”

- BLAISE PASCAL, mathematician and theologian, after whom the computer language and operating system PASCAL was named

CHANGE OF PACE

By David Hay, Chief Investment Officer

We would like to take this opportunity to update EVA readers on a couple of changes to our publishing efforts. First, Worth Wray’s brief tenure as a contributing author to our EVA team came to an end this month. We have amicably parted ways and he is homeward bound for Texas. Worth is an informed and bright young man. We are appreciative of his past work and wish him well.

Second, in what we think is very good news for EVA readers, my great friend and partner Louis Gave, has graciously given us his permission to share a much greater amount of Gavekal’s publications with all of you. In the past, we have run a limited number of their reports each year as part of our “Guest” EVA rotation. This week begins the first in what we hope will be a long series of regularly relaying essays from one of the world’s leading economic and financial market research firms.

Our initial edition in this regard is based on the work of Gavekal co-founder Anatole Kaletsky and two regular Gavekal contributors, Cedric Gemehl and Nick Andrews. In recent weeks, they have written on one of the most fascinating—and controversial—topics in today’s financial world: Negative Interest Rate Policy (NIRP). As noted in recent EVAs, nearly 40% of the “rich” world’s economies are operating under the influence of NIRP. It’s looking more and more like that isn’t too dissimilar from operating a motor vehicle under the influence—it might feel like a good idea at the time, but there are likely to be some serious negative consequences.

Anatole and Cedric published their work on Monday, shortly after last week’s dramatic announcements by the European Central Bank (ECB) and its highly creative chief, Mario Draghi. Mr. Draghi is often referred to by financial commentators as “Super Mario”. This is due to his magician-like skills in coming up with a steady stream of monetary tricks to keep the European economy on track and prevent a financial system meltdown. Anatole believes that Mr. Draghi has finally gotten ahead of the curve—in the case of Europe, one that is persistently downward sloping—with radical measures such as paying banks to make loans (Good Lord!). If your head swims a bit when you try to follow all that Super Mario is doing to keep Europe on the rails, don’t feel bad. The various acronyms like TLTRO and his convoluted “remedies” are enough to flummox even veteran market observers.

On the other hand, Nick and Cedric teamed up last month to write a notably less approving piece on the ECB’s push into negative interest rates and other extreme measures to revive Europe’s chronically comatose economy. As they note, the track record of NIRP in countries where this has been in place for awhile is far short of impressive.

It’s safe to say that we are witnessing an unparalleled experiment in monetary policy on a global scale. In fact, this extreme experimentation has been going on for many years. And as with NIRP, the results have been resoundingly underwhelming. This is despite interest rates being lower than at any time since the days when what happened in Babylon stayed in Babylon.

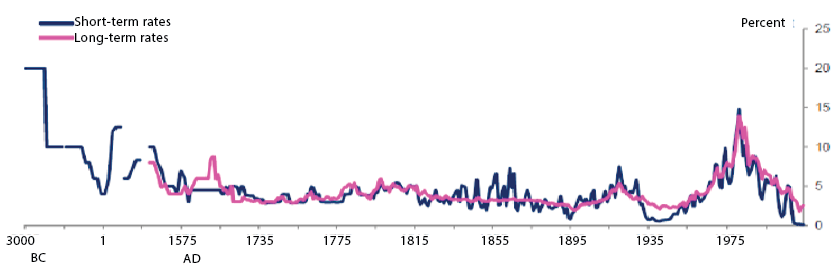

SHORT-END AND LONG-TERM INTEREST RATES BACK TO BABYLONIAN TIMES: TODAY APPEARS TO BE THE LOWEST EVER

Source: Macquarie Research

Source: Macquarie Research

It’s safe to say that we are witnessing an unparalleled experiment in monetary policy on a global scale. In fact, this extreme experimentation has been going on for many years. And as with NIRP, the results have been resoundingly underwhelming. This is despite interest rates being lower than at any time since the days when what happened in Babylon stayed in Babylon.

Yet, never fear—our intrepid central bankers are poised to take us even further down the proverbial rabbit hole.

DAVID HAY / Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

SUPER MARIO: HERO TO ZERO TO HERO

By Anatole Kaletsky & Cedric Gemehl

As markets plunged following Thursday’s European Central Bank (ECB) meeting, it seemed as if Super Mario had turned into Dumb Draghi—a worthy successor to Dim Wim and Tone-deaf Trichet, his two predecessors as ECB president. As Bloomberg commented on Thursday evening: “Draghi’s first message amounted to ‘We have plenty of monetary policy ammunition, and we intend to use it.’ His subsequent clarification was ‘Come to think of it, maybe we don’t have that much’.”But by the next morning Draghi had again gone from Zero to Hero, with risk-on assets racing ahead in virtually every market around the world. As often happens following important policy events, the market’s delayed reaction after a few days’ consideration is likely to be a better guide to the significance of the ECB’s action than the immediate response, which is often dominated by speculative positioning.

Nobody knows if the risk-on rally that began on February 11, mainly because of exhaustion among the bears, will continue in the weeks and months ahead; but if it does, Draghi’s actions last Thursday will deserve substantial credit for at least four reasons:

1) The ECB clearly proved that central banks have not “run out of ammunition”. The cut in the deposit rate from -0.3% to -0.4%, may not have been impressive, especially after Draghi’s warning that further cuts were unlikely. But the increase in monthly bond purchases to €80bn, the extension of quantitative easing to corporate bonds and, most importantly, the targeted long-term refinancing operations (TLRTRO) went well beyond expectations. In particular, the signal sent by TLTRO II—providing banks with ECB liquidity at potentially negative rates until 2021—was very powerful. Bank shares in the periphery* soared by up to 8% on the news that the ECB will give them ultra-cheap loans. The fact that the ECB will pay banks a large subsidy if they expand their lending to the business sector will help them to mitigate the impact of the central bank’s negative interest rate policy (NIRP). This should help reduce financial credit risk in Italy, Spain and Portugal, which for the past two months have been forced to rely on short-term Target 2** funding because inter-bank markets were again showing signs of freezing, with banks in Germany preferring to keep their excess liquidity with the Bundesbank despite the negative interest rate penalty, rather than lending money to “periphery” banks.

2) The ECB chose front-loading. The ECB had previously revealed its policy instruments step-by-step, but this time it announced all of them at once. That wasn’t necessary, because several measures—purchases of corporate bonds, TLTRO II—won’t be effective before the end of the second quarter and the increase in QE could have been implemented gradually. So it looks as if the ECB really did mean to fire its big bazooka this time. It could be because of a worrying downward revision in ECB forecasts (which include the impact of all measures taken up until December 2015). The ECB now expects annual gross domestic product growth of 1.4% in 2016 (against 1.7% in its December forecast), accelerating to 1.7% in 2017 and 1.8% in 2018. And the forecast for 2016 annual Harmonised Index of Consumer Prices (HICP***) inflation has been slashed from 1% to 0.1%, only recovering to 1.3% in 2017 and 1.6% 2018.

3) Looking ahead, the ECB policy path will not be towards even deeper negative rates and a weaker euro, but instead towards other unconventional measures. This should be seen as good news. After all, widespread skepticism about the benefits of negative interest rates is probably justified. The initial stages of NIRP have a positive impact on credit growth, but there is little evidence that keeping interest rates negative for longer or pushing them deeper into negative territory have any additional benefits (see Down The Negative Rate Rabbit Hole following this piece). The emphasis on subsidized ECB liquidity, instead of negative interest rates, is especially good news for European banks. On the currency side, there is growing evidence that the euro’s seemingly inexorable decline actually ended a year ago and that the bull market in the US dollar is now well and truly over. If so, then the euro, like the yen, is unlikely to weaken substantially from here, regardless of what happens to interest rates or what central banks may or may not want. In that case, it is all the more sensible for the ECB to invent new monetary instruments such as the subsidized TLTRO II to inject credit directly into the real economy, instead of following the BoJ example and mindlessly relying on ever-deeper rate cuts.

4) The ECB has become serious about the “second derivative” of its actions. The big positive shock required to restore economic growth in the eurozone happened last year when the ECB announced the world’s largest QE program by promising to buy 2.5 times the net issuance of all eurozone government bonds. As we noted at the time this was roughly five times bigger than Fed’s QE3 program and 50% bigger than the Japanese one in relation to the flows in the relevant bond markets.

As a result, the ECB effectively monetized all eurozone government deficits and mutualized a significant part of the outstanding debt stock, thereby circumventing the two existential flaws of the euro project—the Maastricht Treaty bans against monetizing or mutualizing government debts. Economic data suggest that this policy delivered a positive shock to economic activity, although not to inflation because of the oil price effect. Eurozone GDP grew by 1.6% in 2015, closely in line with economic forecasts. So the ECB helped to fix the “first derivative”. The issue this year is that economic growth has begun to decelerate. In other words, the second derivative—the rate of change of the rate of change—has become negative. Super Mario clearly intends to turn it positive again.

*Europe’s periphery countries are Portugal, Italy, Greece, and Spain.

**TARGET 2 is a payment system that enables real-time settlement of national and cross-border payment in central bank money.

***The European version of the CPI.

DOWN THE NEGATIVE RATE RABBIT HOLE

By Nick Andrews & Cedric Gemehl

“Curiouser and curiouser,” as Alice remarked on falling down the rabbit hole and entering Wonderland. Released yesterday, the minutes of the European Central Bank’s January meeting strongly hinted at further monetary easing measures when the governing council next meets in March. Already committed to €60bn in asset purchases per month until March 2017 and charging a negative interest rate of -0.3%, the ECB now looks likely to push its deposit rate even further into negative territory in its efforts to kick-start credit creation and reflate the eurozone economy. Whether it can succeed is questionable.

The introduction of negative rates may have worked as a signaling device. But after more than six months of negative interest rate policies in Switzerland, Denmark, Sweden and the eurozone itself, the evidence for their effectiveness is mixed at best. Differentiating cause and effect is difficult, but it is clear that where NIRP has been in force for the longest, and rates have been pushed most deeply negative, credit to the non-financial sector is contracting rather than expanding. As a result, it is hard to be optimistic about the ECB’s chances of success, or to conclude that the benefits of negative interest rate policy (NIRP) are worth the cost of the damage it inflicts on banks’ profitability and on debt market liquidity.

To be fair, credit creation was not the primary goal of NIRP when it was introduced in Switzerland, Denmark and Sweden in early 2015. Rather, the target was exchange rates. For Denmark the aim was to protect the krone’s peg to the euro. For Switzerland and Sweden it was to limit deflation imported as a result of the impact of eurozone monetary policy on the euro. But for the ECB, as chief economist Peter Praet has made clear, the explicit goal of NIRP is to stimulate credit creation by discouraging commercial banks from sitting on ECB deposits at negative yields, and instead incentivizing them to take more risk by lending to the real economy at positive rates of return. But is that the effect NIRP has?

-In Denmark, there is evidence that the initial move to mildly negative rates in mid-2012 did indeed encourage lending by reducing the interest rates on loans to the private sector. However, cutting rates to a deeply negative -0.75% at the beginning of 2015 had no discernible benefit in terms of credit creation. Lending to non-financial companies slowed from a year-on-year growth rate of 2.7% in December 2014 to -0.2% YoY in December 2015. Loan growth to households slowed from 3.4% in July 2014 to 2.7%.

-In Switzerland, which also cut rates to -0.75% at the beginning of 2015, lending growth to non-financial companies slumped from 2.5% in December 2014 to zero in the latest data release. Over the same period loan growth to households fell from 3.4% to 3%.

-In Sweden, which cut rates in stages from zero in early 2015 to -0.5% earlier this month, the picture is more mixed. Lending to businesses slowed from 4.8% YoY growth in February 2015 to 2.7% in December. At the same time lending to households accelerated from 6.3% to 7.4% as low rates helped to pump up an already inflated housing market, although in recent months the pace of the acceleration has slowed.

-In the eurozone, the ECB introduced negative rates in June 2014. In concert with the asset quality review, targeted longer term refinancing operations and quantitative easing, NIRP helped to bring down business borrowing costs. As a result, in Germany composite borrowing costs for non-financial businesses fell from 2.73% to 2.04%, while in France they fell from 2.22% to 1.73%. In response, lending growth to the private sector picked up from 2014’s dismal levels to reach 2.3% in Germany and 3.2% in France.

In conclusion, it seems that the initial stages of NIRP are indeed accompanied by an increase in credit creation. However, there is little evidence that keeping rates negative for a prolonged period, or reducing them more deeply into negative territory, has any additional benefits. And although it is difficult to separate cause and effect with any confidence, there is some suggestion that deeply negative rates may prove counter-productive, as the damaging impact on bank profitability and market liquidity leads to a fall—rather than a rise—in banking sector risk appetite. As a result, it is hard to be enthusiastic about the prospect of further reductions in the ECB’s already negative deposit rate, even with a possible tiered deposit rate scheme. As Alice would have said, the idea “sounds like uncommon nonsense”.

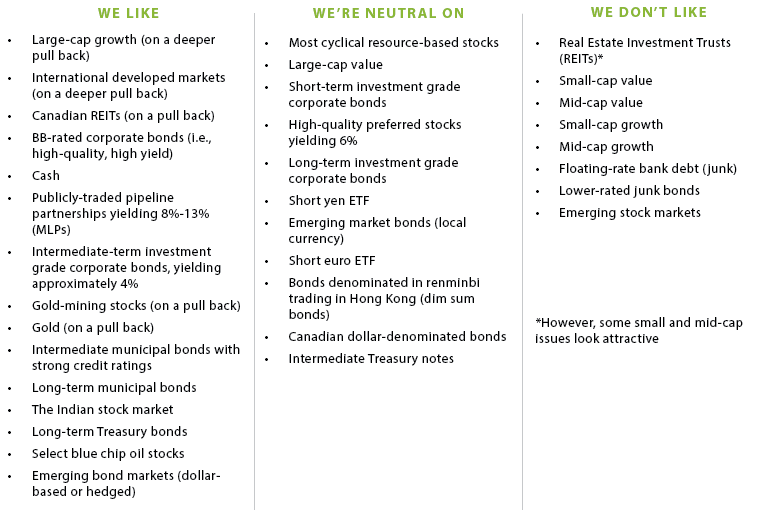

OUR LIKES AND DISLIKES.

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.